"This contributor article explores how banks in the US, UK, Australia and more handle crypto deposits. Country-by-country comparison table and how to check before you trade."

Most traders assume that a simple bank transfer to an exchange is a routine task. However, in 2026, the reality is far more nuanced. Many only realize there is a hurdle once a payment is "pending" indefinitely or capped by a hidden daily limit. Taking five minutes to audit your bank’s specific stance can save you from the frustration of frozen funds or missed market opportunities.

Why Banks Treat Crypto Differently

Banks aren't just being difficult; they are balancing a complex set of risks that changed significantly with the global regulations of 2025 and 2026.

• Fraud Reimbursement: Banks often face pressure to reimburse victims of "investment scams," leading them to preemptively block payments to exchanges they deem high-risk.

• Compliance & AML: Anti-Money Laundering (AML) monitoring is stricter than ever. What looks like a normal transfer to you may trigger an automated flag for "unusual activity" if it's your first time funding an exchange.

• Reputational Risk: Some traditional institutions still prefer to keep a distance from retail crypto volatility to maintain a "stable" brand image.

What To Check Before You Deposit

A bank might look friendly on its homepage but apply friction at the point of transaction. Here is your checklist for 2026:

1. Payment Method Restrictions

Check if your bank distinguishes between bank transfers (ACH/SEPA/Faster Payments) and card purchases. Many banks allow direct transfers but block debit or credit card buys entirely.

2. The "Hard Caps" and Hidden Limits

Several major banks have introduced rolling allowances.

• Monzo (UK): Generally keeps a £5,000 rolling 30-day crypto allowance.

• CommBank (Australia): Often caps transfers at A$10,000 per month and may hold payments for 24 hours for security reviews.

3. App-Level Controls

Modern banking apps now include specific toggles for digital assets. For instance, ANZ Plus uses a "Crypto Protect" feature that is often enabled by default, blocking payments until you manually switch it off in your settings.

4. First-Time Flags

Even with a friendly bank, a large, first-time transfer to a new exchange payee is almost guaranteed to trigger a manual review. Start small to "warm up" the payment rail.

How Banks Handle Crypto Across Key Markets: A Regional Breakdown

The banking climate for cryptocurrency is highly localized. While some regions are moving toward total integration, others are tightening their grip through spending caps and mandatory security delays. Here is the current state of crypto-banking across major global markets:

• United States: Warming

The U.S. market is becoming increasingly open to digital assets. While bank transfers (ACH) are generally smooth, many banks still distinguish between funding methods; credit card blocks remain common, whereas debit and direct transfers face fewer hurdles.

• United Kingdom: Restrictive but Usable

The UK presents a mixed landscape. Most major banks lean toward caution, driven by fraud-prevention mandates. It is common to encounter rolling spending caps or blanket blocks on specific high-risk exchanges.

• Australia: Usable with Limits

Australian banks generally permit crypto activity but have implemented significant "guardrails." Traders often face 24-hour payment holds and monthly limits—typically around A$10,000. Some banks even require you to manually disable "opt-out" security features in their apps before a transfer will clear.

• South Africa: Relatively Open

This market is surprisingly accessible. Domestic transfer rails are reliable, and while standard daily payment limits apply, specific anti-crypto blocking is rare among the country's major financial institutions.

• Germany & Japan: Restrictive for Retail

Both nations are leaders in institutional digital asset infrastructure (such as tokenization and custody), but this hasn't fully trickled down to the average consumer. Finding a clear, friction-free path for retail exchange funding remains a challenge.

• Switzerland: Restrictive for Retail

Despite its reputation as a "crypto hub," Swiss banking remains tiered. Crypto services are largely reserved for private banking or wealth management clients, leaving standard retail account holders with limited options.

• Singapore: Friendly with Conditions

Singapore is highly open but emphasizes eligibility. While some banks offer integrated crypto trading directly within their apps, these features are often gated behind "accredited investor" status or high minimum balance requirements.

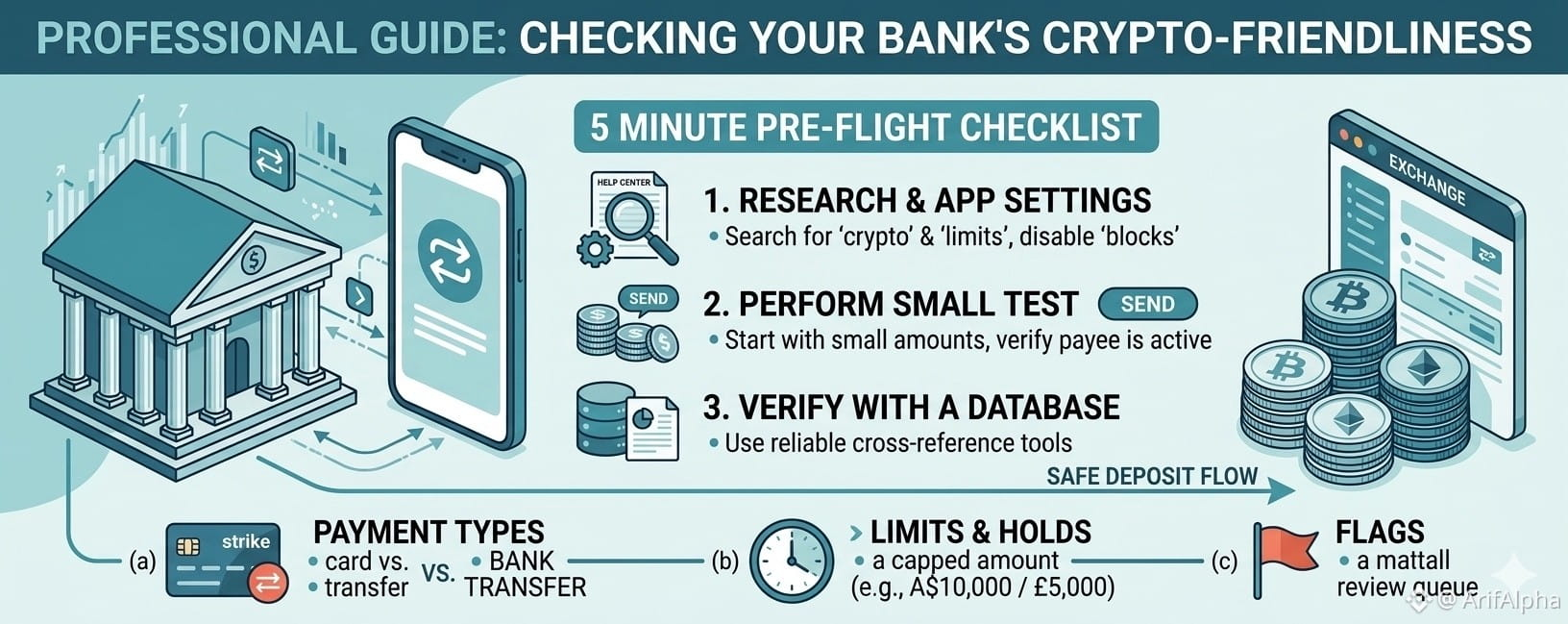

How to Verify Your Bank Before Trading

Don't wait for a blocked transaction to find out where your bank stands. Use these three proactive steps:

1. The "Keyword" Search: Go to your bank’s Help Center. Don't just search for "Crypto." Search for "fraud prevention," "payment limits," or specific payment rails like "Faster Payments" or "PayID." Restrictions are often tucked away in fraud-prevention FAQs.

2. The Small-Scale Test: Before moving a significant amount, send the minimum allowed deposit (e.g., $10 or £10). This confirms that the link between your bank, the payment rail, and the exchange is active.

3. Use Policy Databases: Reference tools like BankToBTC. These databases track real-time compatibility and community reports on which banks are currently processing exchange transfers without friction.

The Bottom Line

In 2026, "crypto-friendly" is no longer a binary Yes or No—it is a spectrum of limits and settings. By understanding your bank's specific guardrails, you can ensure your capital moves when you need it to, not when the bank decides it's safe.

#CryptoBanking #FinancialFreedom #DigitalAssets #CryptoEducation #ArifAlpha