In financial markets, the greatest danger is often not what everyone is talking about.

It's the surface-level calm that hides a much larger storm beneath it.

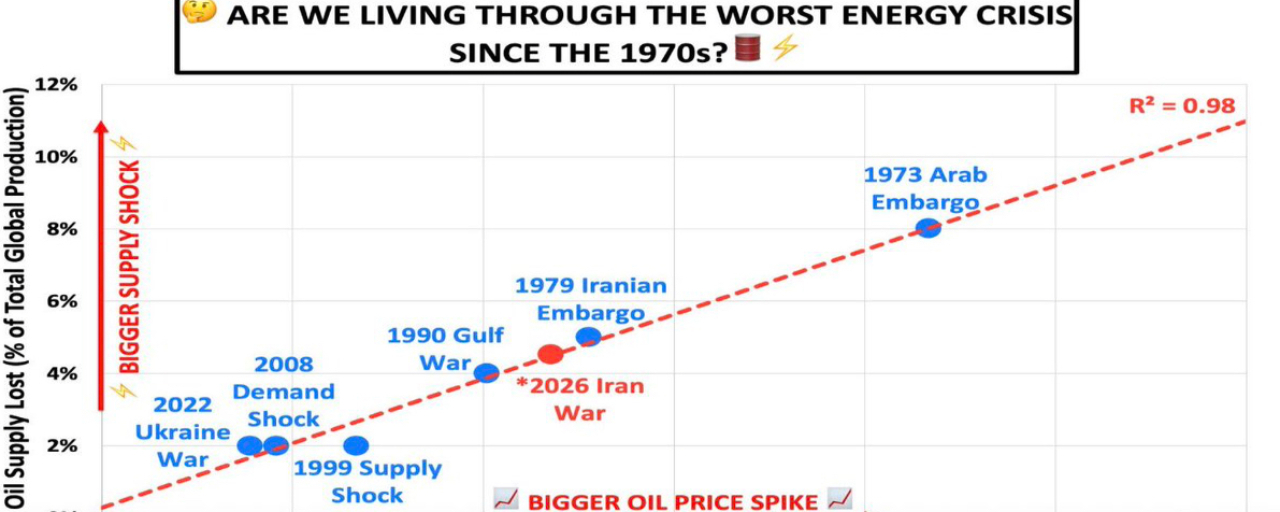

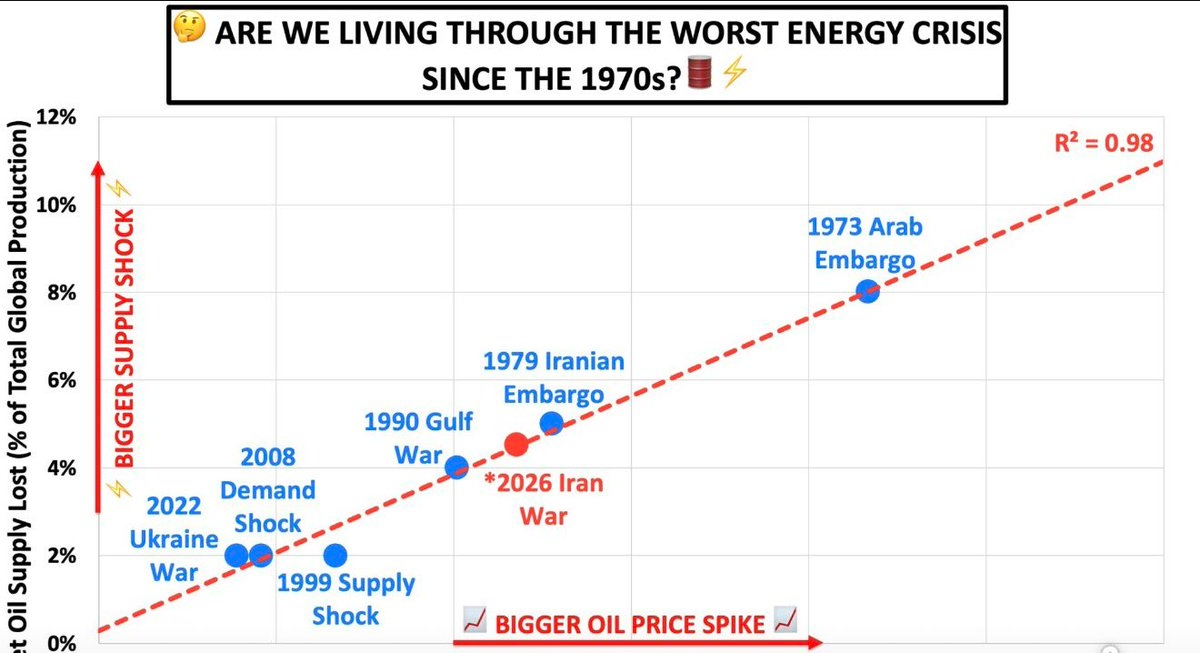

Current indicators and emerging market signals suggest that crude oil prices could face a genuine risk of surging toward levels few investors are prepared for potentially even $200 per barrel if global supply disruptions continue to intensify.

The obvious question:

If the situation is that serious, why do markets appear relatively calm today?

The answer lies in a series of temporary "painkillers" that have masked the true impact of disruptions across global energy markets.

For months, markets have relied on three key mechanisms:

1/ Strategic Reserve Drawdowns

Governments have repeatedly tapped emergency stockpiles to ease supply pressures and artificially smooth price spikes.

2/ Supply Re-Routing

Oil shipments have been redirected through longer, more expensive routes to avoid conflict zones and geopolitical chokepoints.

3/ Temporary Workarounds

The industry has found short-term solutions to keep barrels flowing despite growing logistical and geopolitical challenges.

⚠️ But the period of adjustment may be nearing its limits.

The physical oil market where real barrels are bought and sold, far away from financial speculation, is increasingly signaling that the supply story is not over.

In fact, the most difficult phase may still lie ahead.

Many investors may soon be forced to confront a reality in which these temporary solutions lose effectiveness and the underlying supply imbalance becomes impossible to ignore.

A move toward extreme oil prices would not simply mean more expensive gasoline.

It could trigger:

• A new global inflation wave

• Higher transportation and manufacturing costs

• Increased pressure on central banks

• Delayed interest-rate cuts

• Slower economic growth worldwide

The market's biggest mistake is often assuming that today's calm reflects tomorrow's reality.

Sometimes the quietest period arrives just before the most violent repricing event.