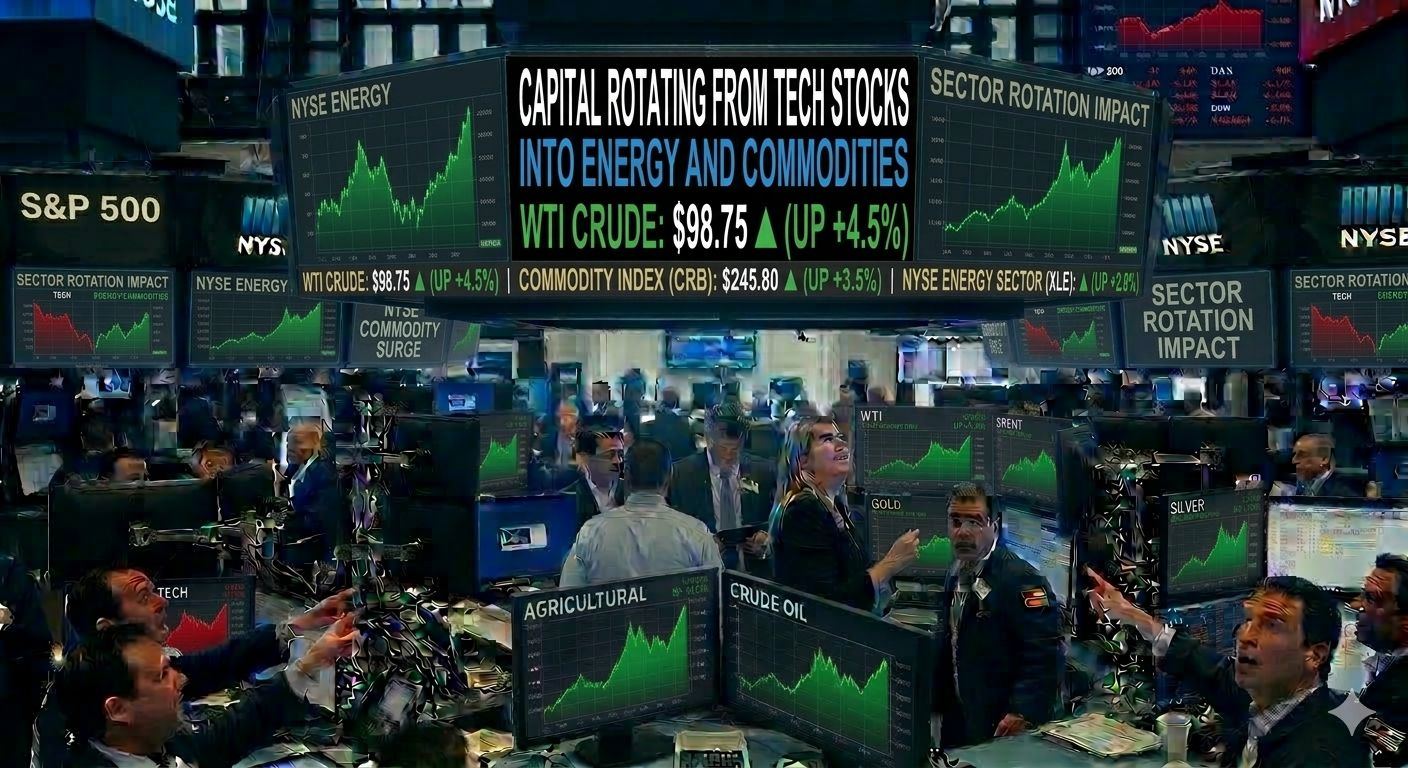

Global markets are experiencing a noticeable sector rotation as investors shift capital away from high-growth technology stocks and into energy and commodity-linked assets. This repositioning is largely driven by rising oil prices, geopolitical risks, and renewed inflation concerns that are reshaping market sentiment.

Energy Prices Driving the Shift

The surge in crude oil prices has significantly strengthened the outlook for energy companies and commodity producers. As oil markets tighten and supply risks increase, energy firms are expected to benefit from higher revenues and improved margins.

Investors often move capital toward commodities during periods of inflation risk because raw materials tend to rise in value when prices across the economy increase. Benchmark energy contracts such as Brent Crude Oil have been trending higher, attracting both institutional and hedge fund flows.

Pressure on Technology Stocks

At the same time, technology stocks have faced growing pressure. Higher energy prices can push inflation higher, which in turn may force central banks to maintain tighter monetary policy for longer.

Higher interest rates reduce the present value of future earnings, a key factor in the valuation of growth-oriented tech companies. This dynamic has weighed on major technology-heavy indices such as the Nasdaq Composite, which is heavily influenced by large technology firms.

Companies in the semiconductor and AI sectors—including major players such as NVIDIA—have experienced increased volatility as investors rebalance portfolios toward sectors that benefit more directly from rising commodity prices.

Commodities as an Inflation Hedge

Commodities historically perform well when inflation expectations increase. Energy, metals, and agricultural products often act as natural hedges because their prices rise alongside broader economic costs.

Institutional investors frequently respond to these conditions by reallocating capital into commodity-linked equities, exchange-traded funds, and futures markets. Energy producers, mining companies, and resource-focused funds tend to attract increased inflows during such periods.

Broader Market Implications

Sector rotation does not necessarily signal a structural decline in technology companies. Instead, it reflects a tactical adjustment in response to changing macroeconomic conditions.

If oil prices remain elevated and inflation concerns persist, energy and commodity sectors could continue outperforming in the near term. Conversely, if inflation begins to ease and central banks signal a path toward monetary easing, technology stocks may regain momentum as growth expectations improve.

Outlook

For now, the global market narrative is being driven by energy dynamics and inflation risks. As investors navigate this environment, capital flows are increasingly favoring sectors tied to physical resources while growth-oriented technology stocks experience intermittent pressure.

This rotation highlights a classic macro pattern: when inflation fears rise and energy markets tighten, commodities tend to attract capital while technology stocks temporarily lose market leadership.