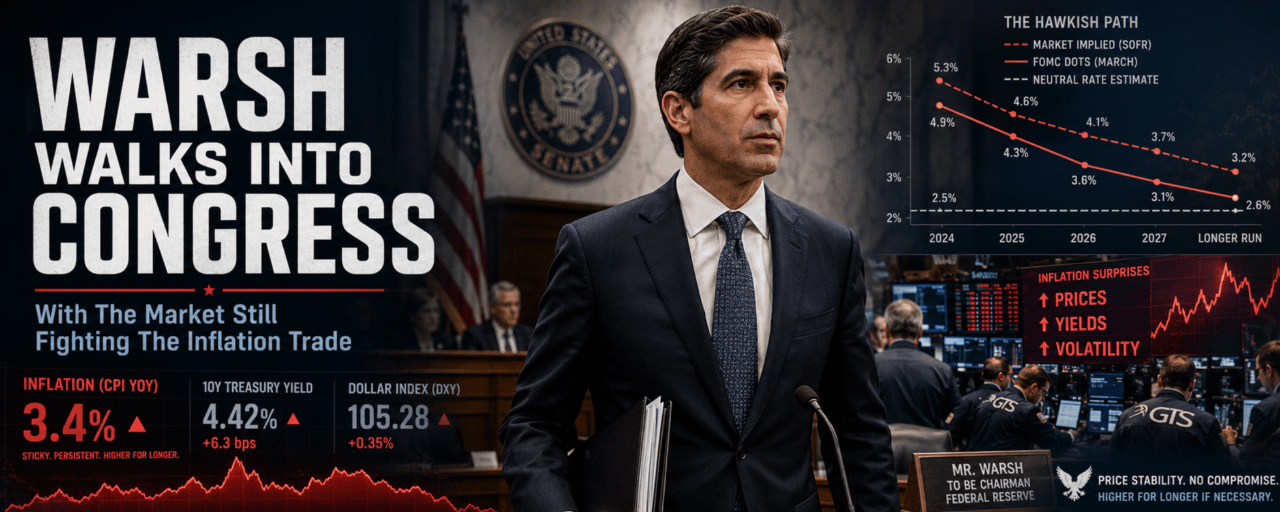

Kevin Warsh’s first monetary policy testimony as Fed chair is supposed to be one of those scripted Washington rituals. Semiannual report, prepared remarks, questions from lawmakers, careful answers about inflation, employment and data dependence. That is the official version. The market version is uglier. Warsh is walking into the House Financial Services Committee at 10:00 a.m. ET on July 14 with traders still arguing over whether the Fed he now leads is about to turn far more hawkish than they have been willing to price.

Bank of America has already made the turn. The bank now expects three straight 25 basis point hikes in September, October and December 2026, after previously looking for no policy changes this year. That kind of forecast does not sit quietly in a rates market. It forces portfolio managers to ask whether their whole 2026 path is stale, whether duration is too comfortable, whether the easing story they kept alive for months has finally run out of oxygen.

Prediction markets are not there yet, which is the problem. Kalshi puts the probability of a July hike at just 25%, with a 76% chance that the Federal Open Market Committee leaves rates unchanged at the July meeting. So the market is not dismissing a hawkish Fed, but it is still trying to buy time. July is being treated as too soon. September is where the anxiety is building. CME FedWatch shows a 51.9% probability of a quarter-point hike at that meeting, which means traders are already hedging the first move while still pretending the near-term Fed reaction function has not fully changed.

Then comes the inflation data.

Economists expect the May Personal Consumption Expenditures price index, the Fed’s preferred inflation gauge, to rise 0.5% month over month after April’s 0.4% increase. The year-over-year rate is projected at 4.1%, up from 3.8% in the prior reading. That is not a number Warsh can easily talk around. A 4.1% PCE print would land right in the middle of the market’s weakest assumption, that the Fed still has enough room to wait, soften the language and avoid forcing a bigger repricing before the July 28-29 FOMC meeting.

This is where the testimony becomes awkward. Warsh is also penciled in to appear before the Senate Banking Committee on July 15, though Senate staff has not confirmed the date. Under normal conditions, the two-day congressional circuit would give him room to repeat the Fed’s standard line and avoid saying anything that boxes in the committee. But if the inflation data comes in hot, every cautious phrase starts to sound defensive. Lawmakers will push on prices. Traders will push on the path. Desks will be watching less for what Warsh says than for whether he still sounds like he has control of the story.

The uncomfortable part is that Bank of America’s call no longer looks like a random hawkish outlier if PCE prints at 0.5% on the month and 4.1% on the year. It starts looking like the trade the market was late to respect. That is the trap. Warsh can sit in front of Congress and talk about patience, balance and incoming data, but a bad inflation print strips those words down fast.

If that number is on the tape when Warsh takes the hearing room chair, he is not explaining policy anymore. He is explaining why the Fed is not already moving.