Bitcoin's famous 4-year cycle has long suggested that the year following a post-halving bull market becomes a bear market. By that framework, 2026 should be a weak year for Bitcoin.

Interestingly, on-chain data points in the same direction—but for a different reason.

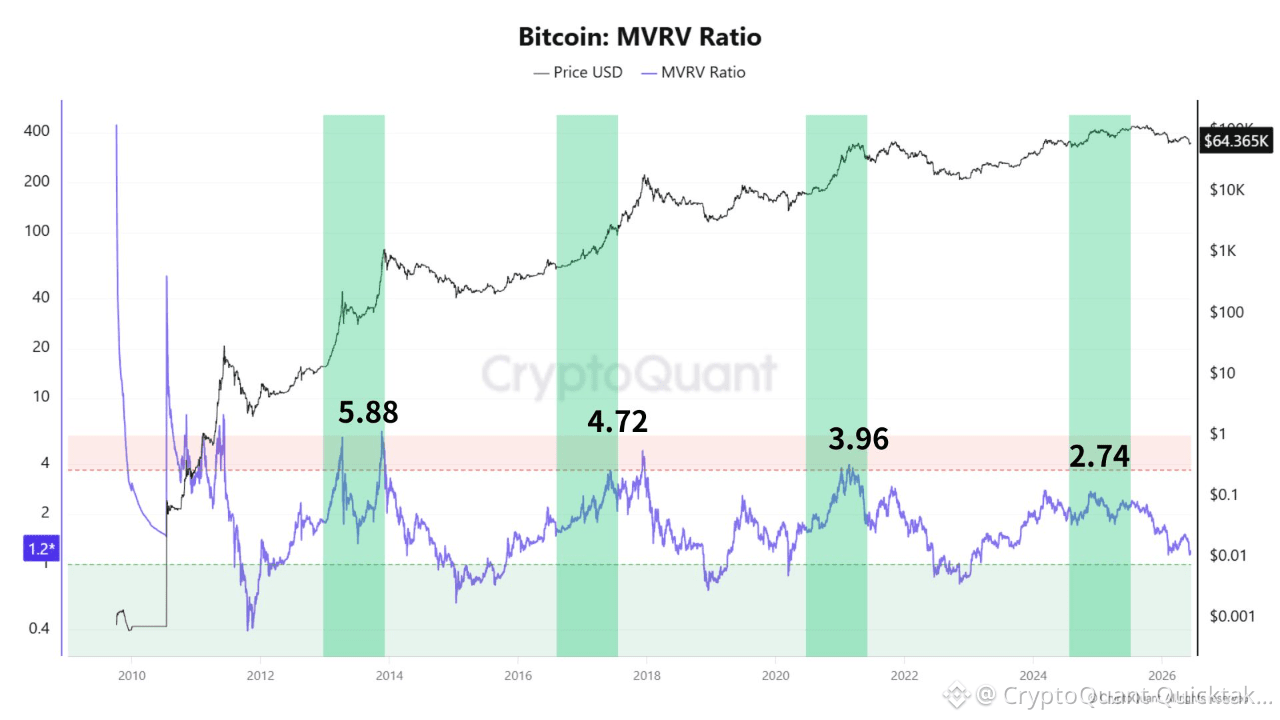

CryptoQuant data shows that Bitcoin's MVRV peak has steadily declined across cycles: 5.88 (2013), 4.72 (2017), 3.96 (2021), and 2.74 (2025). Despite Bitcoin reaching new all-time highs, speculative excess has become progressively smaller, suggesting a more mature market driven by institutional participation and spot ETFs.

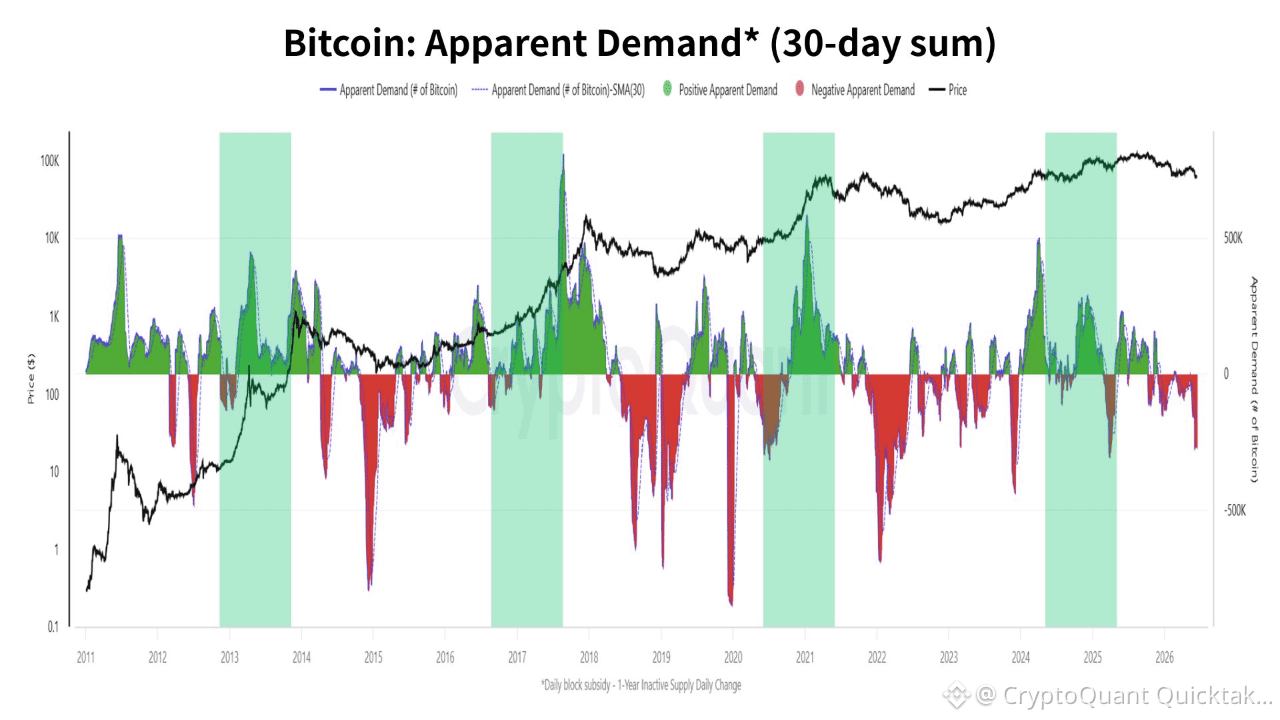

At the same time, Apparent Demand—a measure of whether the market is absorbing newly issued Bitcoin—has turned negative. Historically, major bull markets occurred when demand remained positive, while bear markets in 2014, 2018, and 2022 coincided with prolonged demand weakness.

This suggests that Bitcoin may not be declining simply because "the cycle says so." Instead, demand growth has slowed.

Futures data tells a similar story. Open Interest has fallen significantly from its 2025 peak, indicating that excessive leverage has been flushed from the market. However, positions remain elevated enough that a full capitulation event may not have occurred yet.

At xWIN, we believe the key question for 2026 is not where Bitcoin sits in a 4-year cycle, but whether demand returns. ETF inflows, stablecoin liquidity, and corporate Bitcoin accumulation may ultimately matter more than the calendar itself.

Written by XWIN Japan