Today OMG I am so surprised by new pump of maret in $SIREN and $XAG Buy right now

And I've watched a lot of crypto projects announce their TGE on the back of a whitepaper and a roadmap that looked more like a wish list than a plan. Sign was different.

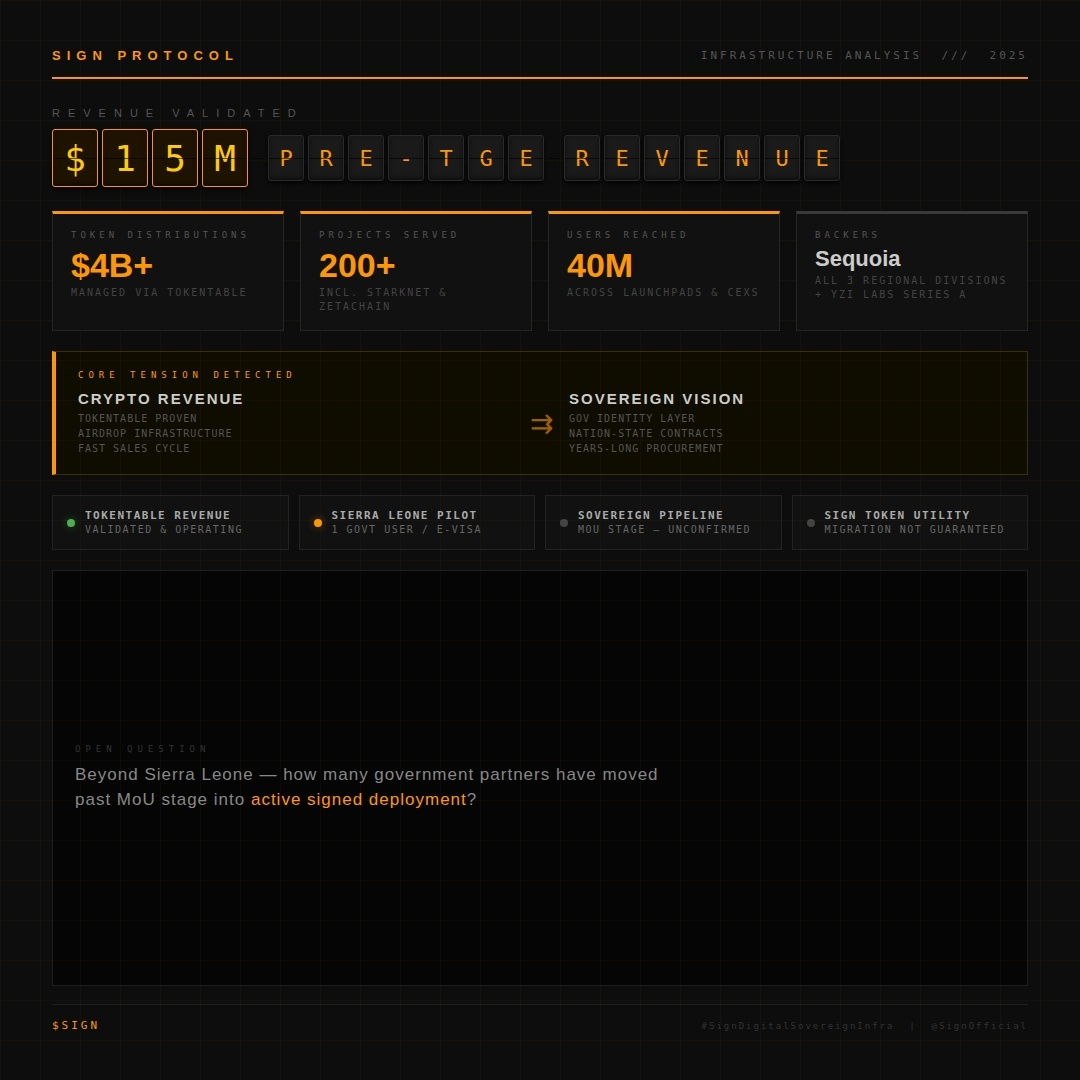

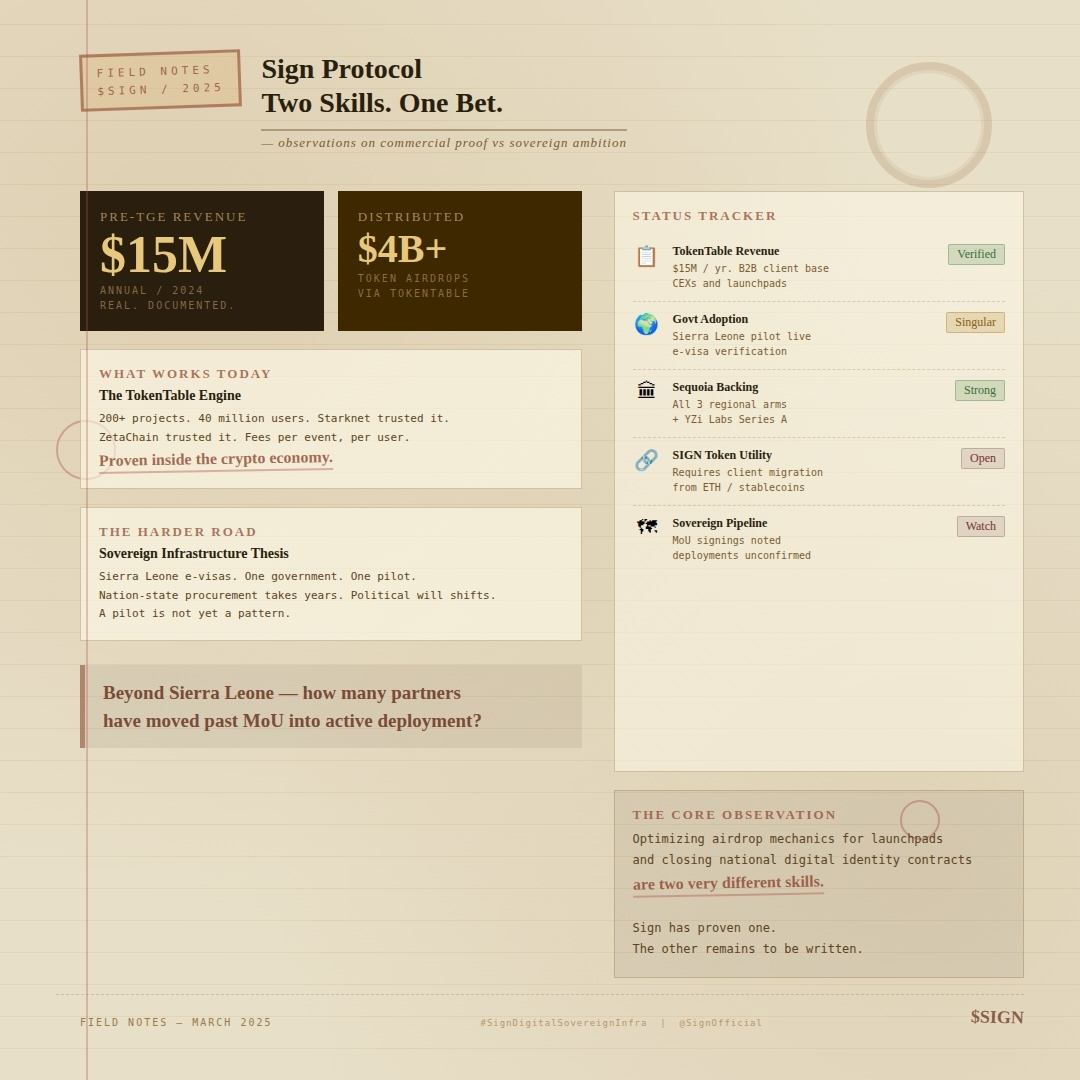

Fifteen million dollars in real revenue before the token even launched. That is not a common story in this space.

TokenTable processed over four billion dollars in token distributions for more than 200 projects. Starknet used it. ZetaChain used it. Movement used it. These aren't obscure projects padding a client list they are some of the most technically demanding teams in the ecosystem, and they trusted Sign to manage their distribution infrastructure without incident.

That kind of track record is worth something.

Sequoia Capital backed the seed round across all three regional divisions, a rare exception to how the firm typically invests. YZi Labs led the Series A. The team comes out of Harvard, Cornell, Columbia and Berkeley. For a blockchain infrastructure play, Sign has the credentials that institutional evaluators actually look for.

So the optimistic read is easy to make. And it is fair.

Here is where I start to think harder.

TokenTable's revenue model is built around serving other crypto projects. Fees per distribution event. Fees per user reached. That model works well when new projects are launching weekly and everyone needs managed airdrop infrastructure. The potential client base expands with market activity.

The Sign Protocol itself the attestation layer, the sovereign infrastructure vision, the government partnerships operates on a completely different timeline and a completely different sales cycle.

Sign onboarded Sierra Leone as its first government user, using its system to verify e-visas. That is a genuinely impressive milestone. One government. One use case. Cited repeatedly across every piece of Sign coverage I've read. It is notable precisely because it is singular.

The gap between "we have one government user" and "we are sovereign-grade infrastructure for nation-states" is enormous. Selling to governments involves procurement cycles that can last years. Regulatory compatibility varies by jurisdiction. Political will shifts. A single pilot does not establish a pattern.

TokenTable earns money inside the crypto economy. Sign Protocol is trying to earn trust from the physical world. Those are two fundamentally different motions requiring two entirely different institutional relationships.

The $SIGN token is positioned at the center of both powering fees across the protocol, attestation creation and governance. The commercial logic requires that TokenTable's existing client base transitions to using SIGN for operational fees rather than ETH or stablecoins. That transition is not guaranteed. Crypto projects have historically resisted adding friction to their workflows when alternatives already exist.

The vision is coherent. The team is credible. The revenue is real.

What I keep returning to is this: TokenTable built its fifteen million in 2024 revenue by serving the crypto industry's internal distribution needs. The sovereign infrastructure thesis requires winning entirely different institutions with entirely different risk appetites and procurement timelines that have nothing to do with airdrop season.

The same team that optimized airdrop mechanics for launchpads now needs to close national-level digital identity contracts at scale.

Those are two very different skills. Sign has proven one of them. The other remains an open question.

So here is what I want the team to answer directly: beyond Sierra Leone what is the concrete pipeline of government or institutional partners who have moved past an MoU stage into active signed deployment agreements for Sign Protocol's attestation layer?

#signdigitalsovereigninfra #SignDigitalSovereignInfra @SignOfficial