Overall Market

Bitcoin Consolidates While Precious Metals Surge

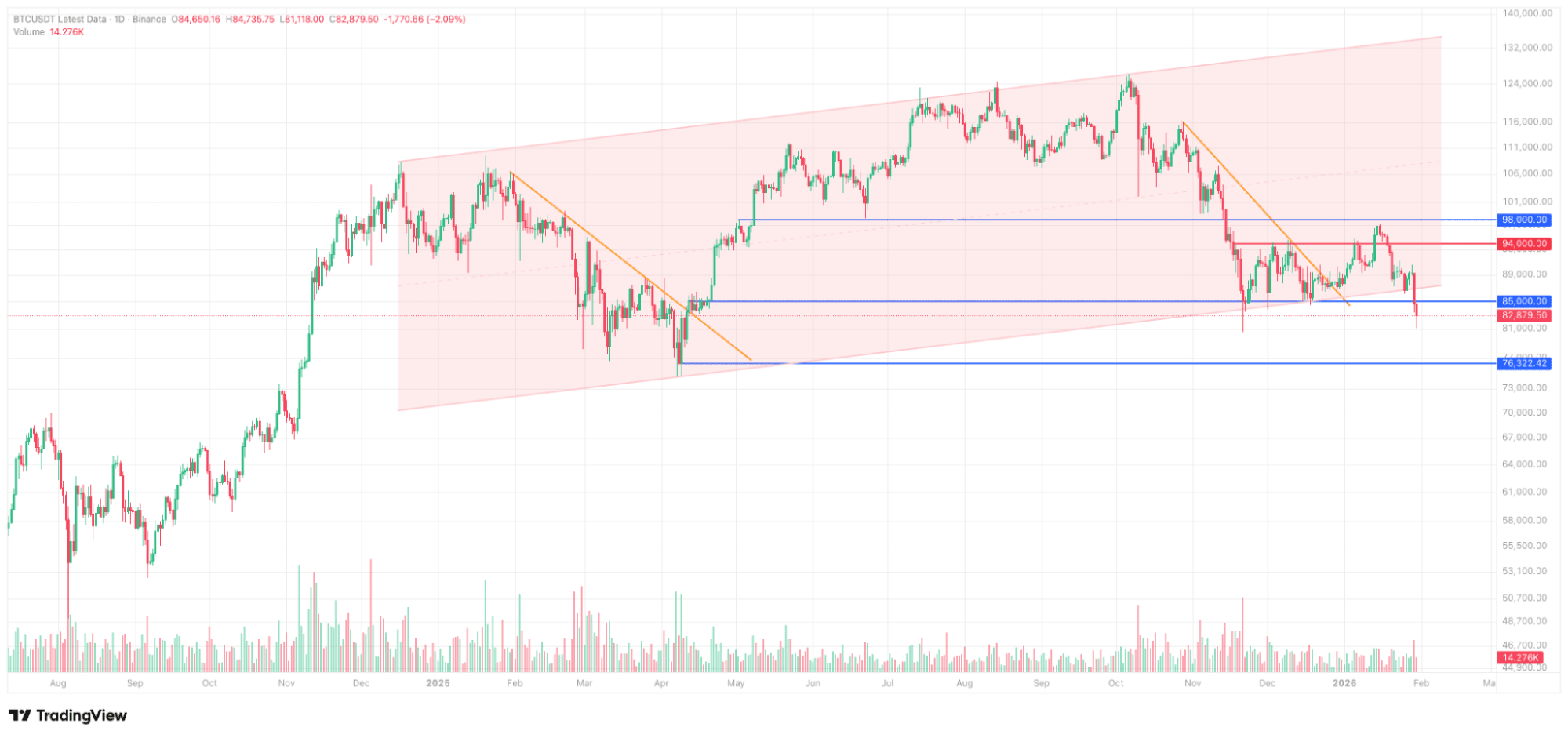

As we noted in our recent analysis, Bitcoin has tested the lower bound of its established channel multiple times since mid-November, following its retreat below the $100,000 psychological threshold. While these tests have generated short-term bounces, they have yet to catalyze a sustained reversal. This persistent weakness has increased the probability of a near-term breakdown.

In contrast to the crypto market's sluggish performance, precious metals have delivered exceptional returns over the past two months. Gold and silver have achieved consecutive all-time highs with volatility reminiscent of crypto assets. Interestingly, this bullish sentiment and FOMO-driven momentum has not extended to Bitcoin—the so-called "digital gold"—which remains sensitive to macro headwinds, including President Trump's tariff announcements targeting EU and Canadian trading partners.

Thursday's Multi-Factor Selloff

Microsoft's post-Wednesday earnings release triggered notable market movement. Despite beating consensus on both revenue and EPS, elevated capital expenditure guidance raised investor concerns about AI investment returns. MSFT declined approximately 10% on Thursday, pressuring most AI-related equities lower, with Meta being a notable exception.

Concurrently, escalating US-Iran geopolitical tensions drove a flight to safety, propelling oil, gold (briefly touching $5,600), and silver (exceeding $120) sharply higher. The parabolic price action suggested a potential blow-off top, which materialized as both metals subsequently retraced 8-10%, adding to broader market pressure.

Bitcoin and the wider crypto market absorbed these headwinds acutely, breaking decisively through the $84,000 support level we've previously highlighted as critical. The inability to quickly reclaim this threshold has opened downside space toward the $80,000 support level and even the $74,600 low marked in April 2025.

Our Market Outlook

Near-Term Perspective

Current conditions remain challenging, with long liquidations accelerating the sell-off. Bitcoin is exhibiting elevated correlation with US technology equities during risk-off periods, while sustained outflows from crypto ETFs underscore a rotation toward AI-focused investments. Notably, several Bitcoin miners are repurposing infrastructure for AI and high-performance computing workloads—reflected in a 4%+ decline in mining difficulty over the past 30 days. This signals a temporary capital and narrative shift away from crypto.

Longer-Term Outlook

We remain constructive on Bitcoin and digital assets over an extended horizon. Several structural tailwinds support our view: improving global liquidity conditions, innovative crypto applications across PayFi and Real-World Assets gaining traction, potential spillover from precious metals momentum as dollar weakness persists, and meaningful progress on regulatory frameworks in the US and internationally. We believe these factors will ultimately restore capital inflows and upward momentum to the crypto ecosystem.

Macro at a glance

Weekly Macro Highlights (January 22 - January 28, 2026)

Thursday, January 22, 2026

US GDP expanded 4.4% (QoQ) in Q3 2025, exceeding consensus estimates of 4.3% and accelerating from Q2's 3.8% growth rate

US initial jobless claims totaled 200,000, below the 209,000 forecast, while continuing claims declined to 1,849,000 from 1,875,000, signaling labor market resilience following the Federal Reserve's recent rate reduction

US PCE Price Index and Core PCE Price Index both registered 2.8% year-over-year growth in November, aligned with market expectations

Friday, January 23, 2026

Japan's national core CPI rose 2.4% year-over-year in December, decelerating from November's 3.0% increase

The Bank of Japan maintained its policy rate at 0.75%, as widely anticipated

The BoJ revised its economic growth forecast for FY2025 (ending March 2026) upward to 0.9% from 0.7%, and raised its FY2026 GDP outlook to 1.0% from 0.7%

Monday, January 26, 2026

US durable goods orders increased 5.3% month-over-month in November, surpassing the 3.1% consensus forecast

Tuesday, January 27, 2026

The Conference Board Consumer Confidence Index declined to 84.5 in January from 94.2 in December, falling short of the 90.6 estimate

Wednesday, January 28, 2026

The Bank of Canada held its policy rate steady at 2.25%, consistent with market expectations

The Federal Reserve maintained the federal funds rate at 3.75%, in line with forecasts. During the subsequent press conference, Chair Powell refrained from providing specific forward guidance on the rate path, declined to address USD volatility, and avoided commenting on matters related to the administration.