A key debate in Bitcoin is where the real price-moving force is concentrated.

For years, spot was seen as the natural center of price formation. But with derivatives, perpetual futures on CEX, and the entry of the CME (Chicago Mercantile Exchange), the largest derivatives market in the world, Bitcoin’s structure has changed

The question is no longer whether Wall Street participates in Bitcoin. It does. The real question is:

Which segment concentrates greater exposure and structural pressure on price: spot, CEX derivatives, or CME Bitcoin futures?

To answer this, we use Open Interest (OI) as the main futures metric. OI measures open futures exposure, not traded volume. It helps identify where leveraged capital remains active and capable of amplifying price movements

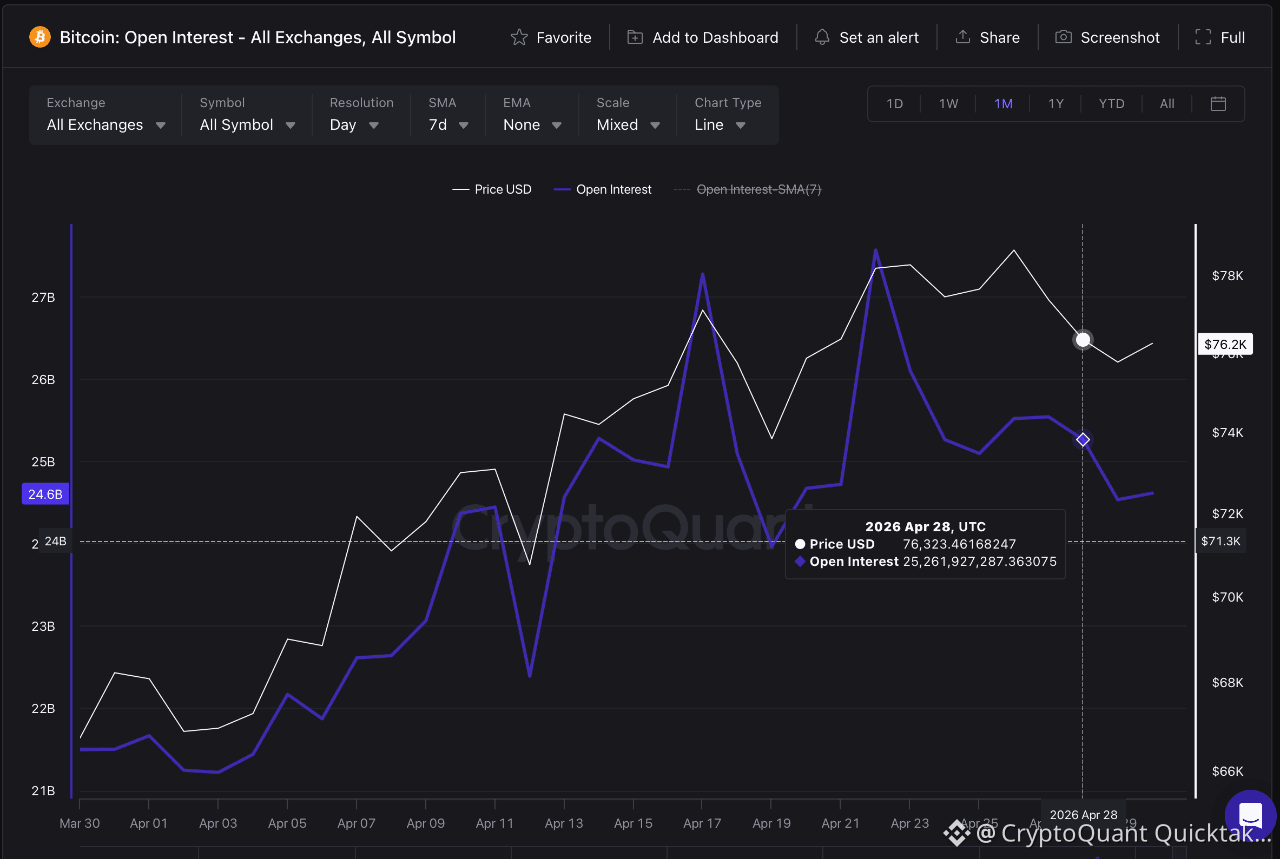

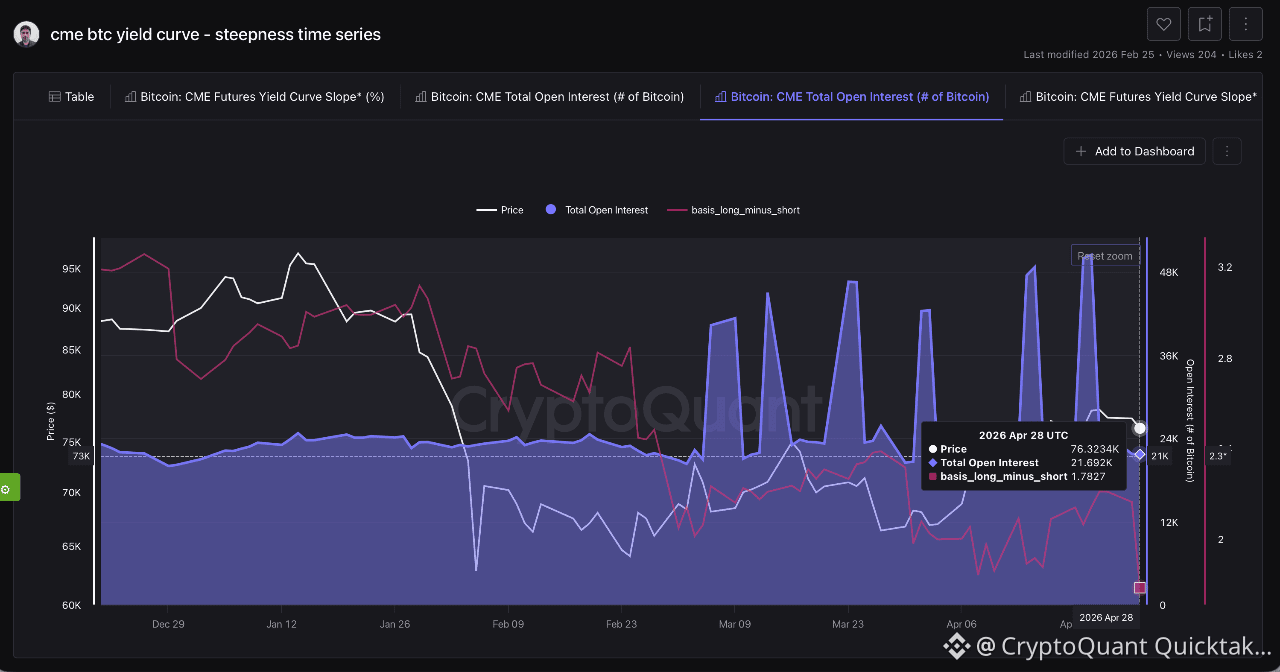

Using April 28, 2026 as reference, the structure is clear:

Open Interest on CEX: 25.26B USD

Open Interest on CME: 8.32B USD

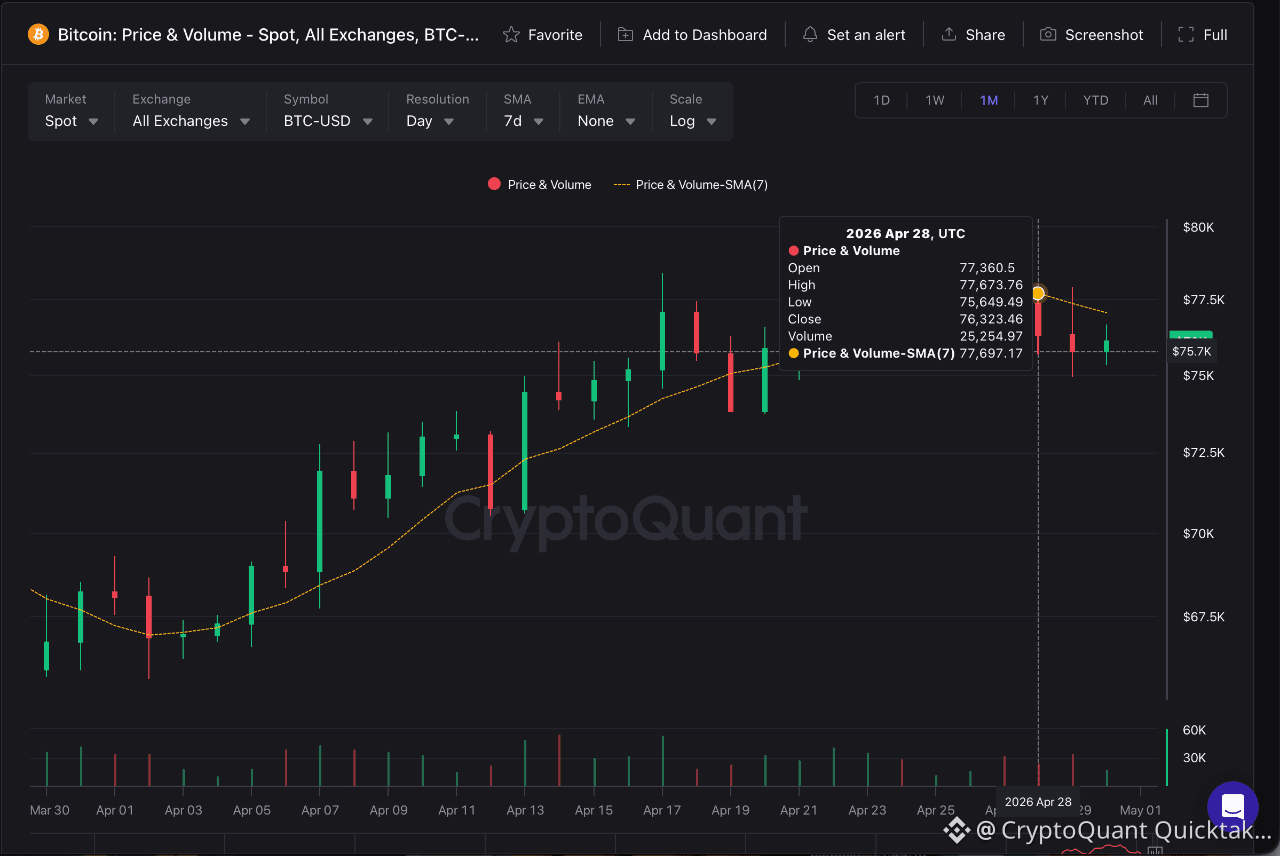

Spot volume converted to USD: 1.92B USD(25,254.97 BTC × ~$76,000 ≈ $1.92B)

Together, CEX and CME futures represent 33.58B USD in derivatives exposure. Including spot, the total reaches 35.50B USD

The direct comparison is decisive:

25.26B / 8.32B ≈ 3.0x

In other words, CEX concentrate roughly three times more Open Interest than the CME.

This does not make the CME irrelevant. It represents meaningful institutional positioning through fixed-expiry futures, but not the main center of gravity

The dominant weight remains on CEX, where perpetual futures, leverage, liquidations, and funding rates directly shape price dynamics

In terms of open exposure, derivatives represent ≈94.6% of the analyzed structure: CEX ≈71.2%, CME ≈23.4%, while spot accounts for only ≈5.4%

Therefore, the CME reinforces Bitcoin’s institutionalization, but it does not displace the market’s center of gravity

Wall Street participates, but CEX still dominate

Methodological note: OTC trades and wallet-to-wallet transfers are excluded because they may not pass through order books or impact price formation

Written by Carmelo_Alemán