Introduction: The Abstraction of Currency Value and the Foundation of Trust

In today's monetary system, a dollar bill that costs less than 10 cents to produce, or a piece of stablecoin code recorded on the blockchain, can both buy real goods and services not because of the 'amount of metal it contains,' but rather due to the entire trust structure built around credit. To understand stablecoins, especially those backed by the dollar, one must unpack the value basis of the dollar as a global reserve currency.

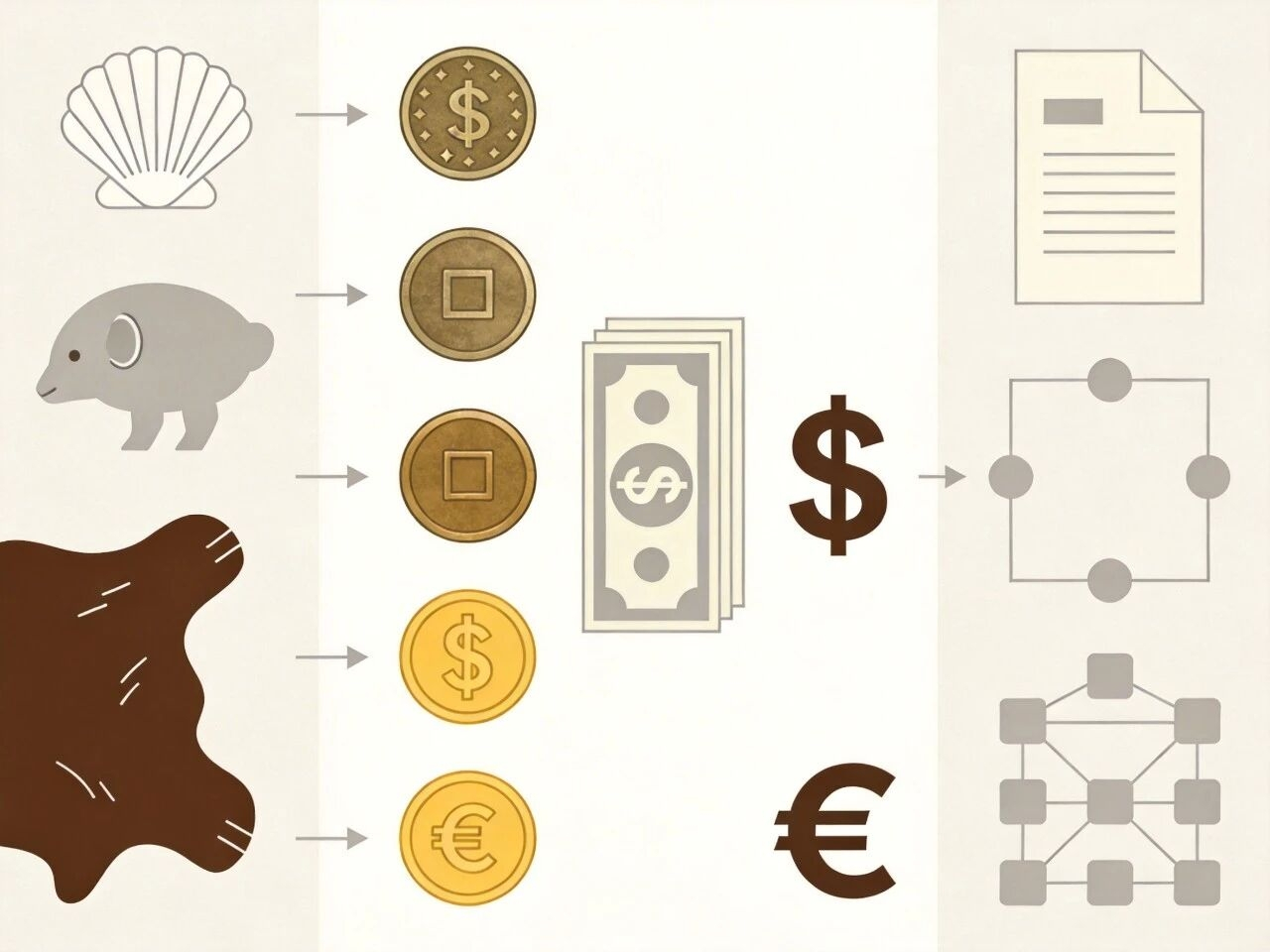

From a longer historical perspective, the things humans have used as 'money' have increasingly moved towards abstraction: initially, they were items of inherent utility (shells, grains), then scarce metals (gold coins, silver coins), and today, we have a fiat currency system entirely supported by credit. With each step forward, the physical properties of 'money' recede, replaced by institutions, consensus, and agreements. The dollar is the representative of this journey, no longer backed by physical commodities like gold, but maintained through social consensus, geopolitical arrangements, and a legal framework.

However, a pure credit system is not a free lunch. Maintaining this trust requires continuous investment in institutional building, military spending, and global financial infrastructure. The dollar can remain at the center of the global monetary system for a long time not only because of the "backing" of the U.S. government but also because it has locked in the world's continued demand for dollars through the petrodollar system, global clearing networks, and military strength. Stablecoins merely transfer this dollar credit mechanism to distributed ledgers, adding a layer of rules written in code on top of those originally inscribed in treaties and laws.

The transfer of trust in the history of currency evolution: from the gold standard to the fiat currency system

To understand how the dollar has reached this point, we must start with the Bretton Woods system. Although the modern monetary system is now firmly in the era of fiat currency, memories of the old era still linger in the institutions. Under the Bretton Woods system from 1944 to 1971, central banks still habitually held large amounts of gold, which was referred to at the time as the "Bretton Woods gold mystery." According to institutional design, they did not necessarily need to hold so much gold, but the inertia of central bankers' thinking remained rooted in the gold standard era; what truly reassured everyone was still that pile of tangible metal.

The Bretton Woods system established a "dual peg" mechanism: the dollar was pegged to gold (at $35 per ounce), while other countries' currencies were pegged to the dollar. During this period, the dollar was regarded as the "equivalent" of gold. The United States established the central position of the dollar in the system by holding approximately 75% of the world's official gold reserves at the end of World War II. At this time, trust was hybrid, containing both recognition of U.S. economic strength and dependence on gold conversion commitments.

The Triffin dilemma and the collapse of the Bretton Woods system. There was an unavoidable design flaw in the Bretton Woods system, later summarized as the "Triffin dilemma." To provide enough dollars for global trade, the U.S. had to continuously run trade deficits, sending dollars all over the world. However, once dollars spread too widely, the amount of dollars held overseas would inevitably exceed the actual gold reserves held by the U.S., making gold redemption commitments increasingly seem like an empty promise. By 1971, the U.S. official gold reserves had dropped from about 20,000 tons in 1944 to around 8,000 tons.

In August 1971, President Nixon unilaterally announced the cessation of the dollar's convertibility into gold, known as the "Nixon Shock," marking a complete transition of human monetary history into the era of credit money. Since then, the dollar has no longer had physical support, and its value is entirely based on credit. This shift forced the international monetary system to seek new anchor points.

The establishment of the petrodollar system and demand locking. After the closure of the gold window, the dollar faced a severe trust crisis. To re-lock global demand for dollars, the U.S. reached a series of key agreements with Saudi Arabia in 1974 against the backdrop of the 1973 oil crisis. These agreements formed the foundation of the "petrodollar system": oil exports are priced in dollars, and in return, the U.S. provides military protection to oil-producing countries, which in turn recycle surplus funds back into the U.S. financial system through purchases of U.S. Treasuries.

This mechanism tightly binds the value of the dollar to the lifeblood of human economy—energy. As long as there is global demand for oil, countries must reserve dollars. In this way, the U.S. has achieved rigid constraints on the demand for its currency, expanding it from domestic legal requirements to global economic activities.

The multidimensional pillars of dollar credit: institutions, economy, and military

Government credit and the U.S. Treasury market. If we treat the dollar as a company, its "credit" is most directly reflected in the U.S. Treasury market. This market is the largest sovereign bond pool in the world, with the best liquidity, and by 2024, its total scale had exceeded $27 trillion. The U.S. Treasuries held by central banks and institutions are, on one hand, foreign exchange reserves, and on the other hand, the benchmark for global interest rate pricing. In other words, those holding dollars are essentially holding tickets to U.S. Treasuries, which can be exchanged for relatively stable interest income and what seems to be a safe asset position at present.

The U.S. political system appears chaotic from the outside, but for capital, it is "predictable." The framework of separation of powers, along with relatively stable rule of law, lets investors approximately know what the worst-case scenario looks like. Over the past few decades, the U.S. has repeatedly engaged in political tug-of-war over the debt ceiling issue, yet has ultimately repaid its debts on time without a true technical default, significantly affecting the market consensus of "the dollar = risk-free asset."

Economic strength and innovation networks. The dollar has a more intuitive support behind it: this economic machine of the United States itself. Even if the U.S. GDP fluctuates in global share, its position in key industries like high technology, finance, and military-industrial complex is difficult to replace in the short term. Startups in Silicon Valley, structured products on Wall Street, and funding flows in top global research institutions are mostly denominated in dollars. Over time, the dollar has become not just a means of payment but the "default language" of an entire set of technological and financial innovation networks.

This resilience is not theoretical but has been built through several rounds of crises: whether it was the 2008 financial crisis or the 2020 pandemic shock, the U.S. economy was initially hit hard and then gradually recovered. The market's expectations for long-term U.S. growth do not stem from the belief that it won't face issues but from the notion that "it can recover after problems arise," which ultimately translates into patience regarding the dollar's long-term purchasing power.

Financial clearing and payment infrastructure. The dollar's hegemonic position depends not only on "who is using it" but also on "how it circulates." The U.S. has built a comprehensive, efficient, and hard-to-replace financial infrastructure around the dollar:

At the top level is a cross-border financial messaging network like SWIFT, which connects about 11,000 institutions globally and is responsible for securely and standardizing the transmission of payment instructions;

In practical funding settlement, private dollar clearing systems like CHIPS handle about $1.9 trillion in cross-border dollar payments daily, utilizing multilateral netting to maximize the "reutilization" of the same unit of liquidity;

At the final settlement layer, there is the Fedwire system operated by the Federal Reserve, serving as a real-time gross settlement network for central banks, processing about $4.5 trillion in large payments daily, providing irretrievable finality for financial transactions.

SWIFT's statistics for 2025 show that the dollar's share in global payments remains above 47%, and in international payments excluding transactions within the Eurozone, it reaches as high as 58.8%. This extremely high network effect creates a strong path dependence: switching to another currency requires not only changing the pricing system but also rebuilding a complementary clearing network with equal efficiency.

Military power: the final safety net of credit. Military power is the underlying guarantee of dollar credit. The U.S. protects major global trade routes (such as the Strait of Malacca and the Suez Canal) with its 11 carrier battle groups and military bases in over 140 countries around the world. This provision of global security public goods ensures that trade priced in dollars can proceed smoothly. The deterrent effect of military strength also places any attempt to challenge the dollar's position on a large scale and quickly in the face of significant geopolitical risks.

The logic of fiat currency value: network effects and "everyone is using it"

The entire set of systems, military power, and clearing networks ultimately serves a very simple question: why is a piece of paper valuable? Understanding the value of the dollar can begin with a simple entry point: it is essentially a piece of paper with very low costs, but people around the world are willing to exchange real goods and services for it. What supports this willingness to exchange is the fact that "everyone is generally willing to accept it," rather than any physical properties behind the paper.

Once this acceptance is formed, it will self-reinforce: the more stable the historical performance, the stronger the trust; the clearer the institutions, the more controllable the expectations; the more users there are, the higher the convenience of using it as a payment medium, and the weaker the motivation to switch to other currencies. For the dollar, the switching costs involve not just "modifying the system" but also rebuilding trust and sacrificing existing liquidity benefits, among other hidden costs.

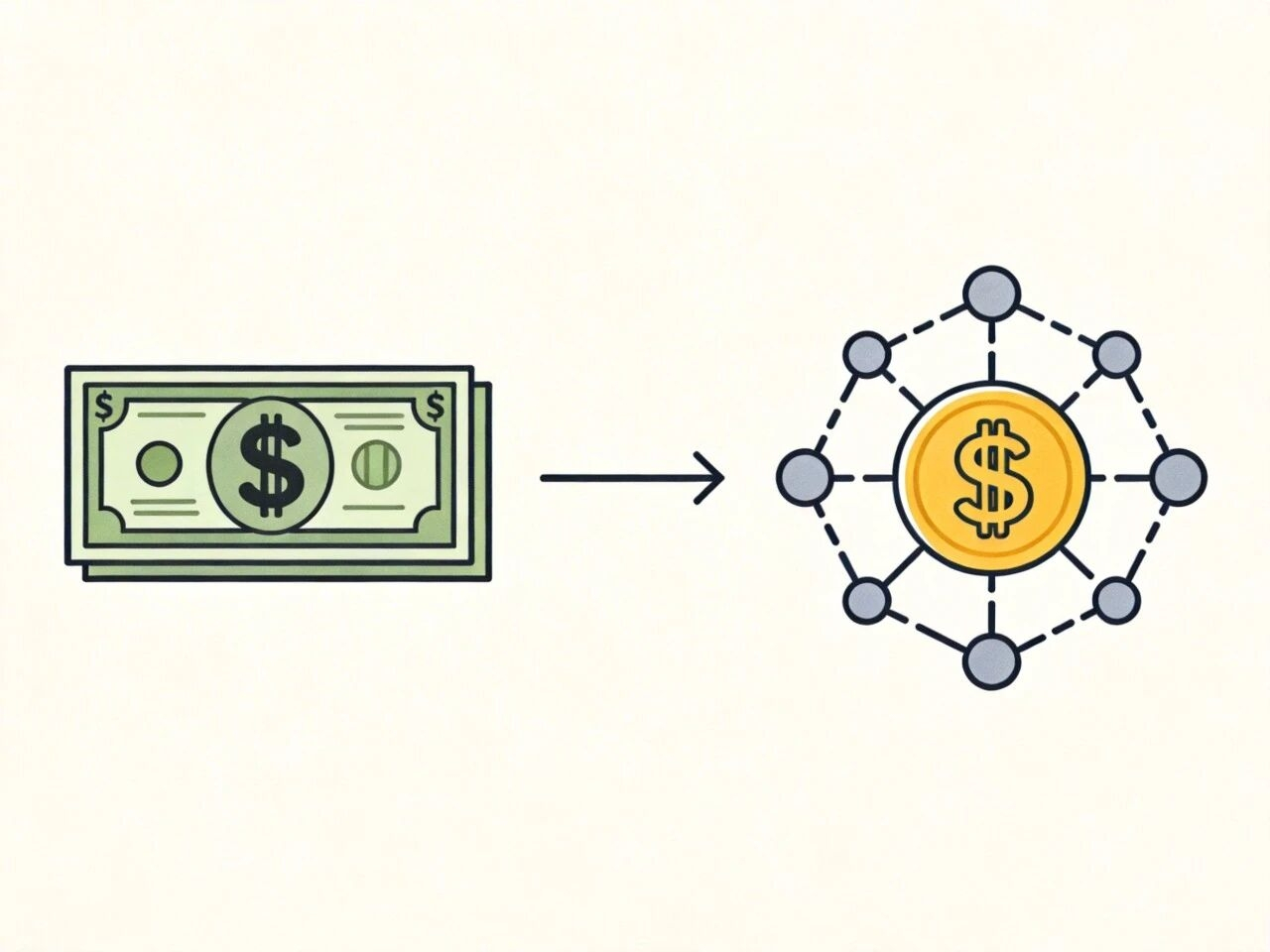

The logic of stablecoins is similar. The code of the token itself is not valuable; what is truly valuable is the dollar assets locked behind it, as well as the network and infrastructure formed around its use.

Stablecoins: the "second leg" of dollar credit in the digital world

If we apply the previous logic of "acceptance + network effects" to the blockchain, stablecoins are essentially answering another version of the same question: in the digital world, who plays the role of the money that "everyone is willing to accept"?

Stablecoins as "digital dollars." In the blockchain ecosystem, stablecoins play a key role in completing the monetary loop of the crypto economy. The most common practice is to peg them to the dollar at a 1:1 ratio, bringing the dollar credit from the traditional financial system into the digital world. As of November 2025, the global circulation of stablecoins has reached approximately $304.36 billion, becoming an important part of supporting daily settlement flows.

Rather than saying that stablecoins are a "completely new currency," it is more accurate to state that they are a digital extension of dollar credit. When users hold USDT or USDC, they are essentially holding a form of "on-chain dollar bonds," with their value supported by the dollar collateral held by the issuer.

To maintain a 1:1 exchange rate stability, leading stablecoin issuers have made their balance sheets very "conservative". For example, by 2025, Tether (USDT) had an exposure to U.S. Treasuries of approximately $135 billion in the third quarter, a single entity large enough to rank as the 17th largest holder of U.S. Treasuries globally, surpassing many sovereign nations. Circle (USDC) disclosed in November 2025 that its exposure of about $68.2 billion was primarily in government securities and related repos, with an additional approximately $9.6 billion held in systemically important bank accounts, and about $49.7 billion allocated to regulated overnight reverse repo agreements.

The key differences between the two in terms of "risk appetite" are: Tether allocates part of its reserves to risk assets like Bitcoin and gold—such as approximately $9.9 billion in Bitcoin and about $12.9 billion in precious metals positions—and maintains about $6.8 billion in excess reserves to cover redemption pressure in extreme situations; while Circle basically avoids such volatile assets, emphasizing the compliance and liquidity of reserve assets, locking almost all funds in government securities, reverse repos, and high-rated bank deposits.

Why stablecoins are so "usable". The reason stablecoins can quickly penetrate the cross-border payment market is that they hit several structural pain points of the traditional agency model.

Settlement time: traditional SWIFT cross-border remittances usually take 1 to 5 business days, involving multi-level agency account reconciliations; while stablecoin transfers based on Solana or Ethereum Layer 2 can often be completed in seconds to minutes, providing 24/7 service.

Transaction costs: under traditional cross-border payment models, intermediary fees, exchange rate spreads, and operational costs often account for 3% to 5% of the transaction amount, with smaller remittance ratios even higher; on-chain fees for stablecoin transfers are typically very low (e.g., as low as $0.01 for Solana), and comprehensive costs are likely to be significantly compressed.

Transparency and programmability: every stablecoin transfer is traceable on the chain, fundamentally eliminating the uncertainty of "funds in transit"; simultaneously, through smart contracts, automatic settlement, custody, and conditional payment can be achieved, providing more granular tools for corporate financial management.

The watershed moment of regulation in 2025: the GENIUS Act and its impact

When stablecoins have run ahead in both scale and efficiency, the question is no longer whether "the technology is feasible" but whether "the system can hold it together." The transition of stablecoins from the margin to the mainstream largely began when regulators were willing to "draw boundaries" for them. In 2025, the U.S. passed the (GENIUS Act) (Payment Stablecoin Act), which basically defined what kind of stablecoins could be considered compliant.

The core requirements of the GENIUS Act. The Act stipulates that compliant payment stablecoin issuers must maintain 1:1 reserves, and the reserve assets are strictly limited to U.S. Treasuries, physical cash, custodial deposits, specific repurchase agreements, and Federal Reserve deposit reserves. In other words, regulation has placed stablecoin issuers on a "narrow bank" track, sacrificing some yield space in exchange for system robustness.

The "compliance dividend" brought by regulation. With clearer rules, traditional financial institutions (TradFi) have begun to enter the market on a large scale. By 2025, approximately 80% of global jurisdictions announced new digital asset plans, and financial institutions began viewing public blockchains as a compliant settlement layer. The MiCA framework in Europe also officially took effect, promoting the emergence of compliant euro stablecoins (like EURC) and forcing non-compliant currencies out of the market.

Stablecoins are no longer seen as a threat to financial stability but rather as a tool for maintaining the influence of the dollar. By locking stablecoin reserves in U.S. Treasuries, the U.S. government has effectively created new rigid demand for Treasuries globally through the private sector.

The modern Triffin dilemma: shortage of safe assets and fiscal pressure

From the perspective of U.S. regulators, the GENIUS Act addresses how to turn stablecoins into compliance tools; but from the perspective of fiscal and international monetary systems, the fact that stablecoins buy U.S. Treasuries is embedded in a larger, older contradiction. In the era of pure credit money, the Triffin dilemma has taken on a new form, which can be bluntly called "Triffin 2.0." This time, the contradiction is not with gold but with the "safe assets" themselves—mainly U.S. Treasuries. The global appetite for such assets that can serve as collateral is growing, but the U.S. cannot indefinitely increase leverage to meet this demand, or else its fiscal sustainability will be the first to face issues.

As non-bank financial intermediaries play an increasingly prominent role in global credit creation, the portion of high-quality assets available for repurchase collateral becomes particularly scarce. Related studies consistently indicate the same thing: dollar-denominated safe assets are now "structurally in short supply." If the U.S. issues more debt to fill this gap, it will drag down its own debt repayment capacity in the long run; if it issues too little, it will lead to a situation where the global credit system faces "insufficient collateral," tightening liquidity.

The rise of stablecoins has added an extra layer of cushioning to the U.S. Treasury market in response to the question of who buys safe assets. Stablecoin issuers themselves are natural buyers of short-term government bonds: as long as the issuance scale grows, they must passively buy more government bonds to convert users' dollars or bank deposits into high-quality liquid assets. By the end of 2024, these issuers are expected to hold about $166 billion in U.S. Treasuries, and by the end of 2025, the market widely expects this number to rise to a range of $250 billion to $500 billion.

In contrast, the stock of U.S. Treasuries in central bank foreign exchange reserves, although large (approximately $7.5 trillion), is more inclined towards long-term holdings, contributing limited marginal liquidity; while the approximately $6 trillion in assets managed by money market funds, which also largely allocate to short-term instruments, face obvious competition in funding sources and investment scope with stablecoins. The addition of this type of "on-chain buyer" further amplifies the turnover efficiency of U.S. Treasuries as global collateral, thus marginally lowering issuance costs.

Analysis of liquidity dynamics in the U.S. Treasury market in 2025

If Triffin 2.0 is about whether the total amount of safe assets is sufficient, then the next thing to watch is whether these assets can still be traded smoothly in extreme situations. The U.S. Treasury market is a "foundation" of the global financial system, and the stability of this foundation directly relates to whether the "building" of the dollar can remain stable. In 2025, this market underwent several substantial stress tests.

Liquidity shocks triggered by tariff announcements. In April 2025, due to macroeconomic uncertainty caused by changes in tariff policies, liquidity in the Treasury market experienced a brief deterioration.

Bid-ask spreads: significantly widened after the announcement on April 2, although the severity was lower than during the initial pandemic in March 2020, it reflects the market's sensitivity to policy fluctuations.

Order book depth: dropped to its lowest level since the banking crisis of 2023 on April 9, and then rapidly recovered in the summer as policies became clearer.

Price volatility: volatility peaked in April, forcing market makers to reduce positions to manage risk.

The Federal Reserve's liquidity support mechanism. The Federal Reserve successfully controlled interest rate trends through standing repurchase operations and overnight reverse repos. In December 2025, the Federal Reserve lifted the $50 billion daily limit on SRP operations, using it as an important tool to respond to extreme market pressures. This decision reinforced the functional resilience of the Treasury market in extreme situations.

External forces challenging the dollar hegemony: mBridge and BRICS Pay

Internally, the U.S. is using various tools to strengthen the foundation of U.S. Treasuries; externally, more and more countries are attempting to build paths that do not rely on this foundation. Superficially, the dollar still possesses overwhelming advantages across various indicators, but the methods of external challenges have shifted from mere dissatisfaction to "building their own roads and networks."

mBridge: A breakthrough in multilateral central bank digital currency platforms. Project mBridge is currently the most technically threatening project to dollar hegemony. It establishes a shared technology platform through multiple central bank digital currencies (CBDCs), allowing real-time cross-border settlements of local currencies without reliance on dollar transfers or the SWIFT system.

In October 2024, the Bank for International Settlements (BIS) announced its exit from the project due to geopolitical pressure, but the project had reached the minimum viable product stage and continued to be promoted by countries like China, Saudi Arabia, and the UAE in 2025. The EVM compatibility of mBridge allows it to connect with other blockchain platforms, providing a second option for global payments outside the dollar system.

The expansion of BRICS+ and trade settlement in local currencies. The BRICS countries (BRICS+) showed a strong trend of de-dollarization in 2025. In terms of local currency settlements, about 65% of trade among member countries adopted local currency settlements in 2024; after Russia faced sanctions, about 90% of its trade with BRICS countries switched to non-dollar currencies.

China's Cross-Border Interbank Payment System (CIPS) had connected 1,467 banks in 119 countries by January 2025, with the average daily transaction amount rising rapidly, indicating the practical space for the RMB to serve as an alternative to the dollar in trade financing.

In terms of payment innovation, projects like BRICS Pay and DCMS (Decentralized Cross-Border Messaging System) are in planning, aiming to build a cross-border payment framework independent of Western control and based on blockchain.

If we lay out several major cross-border payment channels together, we can roughly outline three types of routes:

One is the traditional SWIFT/CHIPS combination, covering about 11,000 banks globally, relying on common standards like ISO 20022, with advantages in deep liquidity, broad counterparties, and almost all major institutions already connected, thus creating strong path dependence;

The second element is the new multilateral CBDC platform represented by mBridge, primarily serving core trading countries like Saudi Arabia, China, and the UAE, using EVM-compatible blockchain technology to avoid dollar transfers and achieve real-time settlement of local currencies against each other, while also enhancing "anti-sanction" capabilities to some extent;

The third element is the CIPS represented by the RMB clearing network, which also supports ISO 20022 but generally adopts a more proprietary technology stack, primarily covering countries in Asia and Africa. Its core demand is to cooperate with the internationalization of the RMB and gradually reduce dependence on a single U.S. dollar clearing channel.

Even so, the fundamental obstacle to challenging the dollar's status lies in the "liquidity trap." Most non-dollar currencies lack sufficiently deep capital markets and stable legal expectations. As a result, while trade can increasingly be settled in local currencies, in terms of ultimate value storage, funds still tend to flow back into dollar assets.

The profound impact of stablecoins on domestic monetary policy

Externally, new paths are being built, while internally, adjustments are being forced. For the Federal Reserve, stablecoins are not only tools for the dollar's internationalization but also new variables for reshaping the bank's liability structure. The expansion of stablecoins is quietly rewriting the familiar set of game rules for the Federal Reserve. A research report in December 2025 mentioned that the bank's liability structure is gradually being reshaped by stablecoins.

Deposit substitution and the weakening of bank intermediaries. When stablecoins become mainstream payment tools, they will create a "deposit migration" effect. Retail users convert bank deposits into stablecoins, and these funds leave the banking system and enter the hands of stablecoin issuers, who then invest them in U.S. Treasuries or reverse repos.

Funding source analysis: Early demand for stablecoins primarily came from investment conversion, but the trend in 2025 shows it starting to erode transaction-based deposit accounts.

Rising bank costs: due to the loss of core deposits, banks are forced to rely on costlier wholesale financing, which could lead to an increase in average financing costs of about 24 basis points and reduce the supply of loans to the real economy.

Changes in the transmission paths of monetary policy. Stablecoin issuers hold vast amounts of cash and short-term bonds, making them significant "non-bank financial institutions" in the monetary market.

The interest rate floor effect: the use of stablecoin reserves in the ON RRP facility has enhanced the Federal Reserve's ability to set lower bounds on interest rates, but it also means that the Fed's balance sheet must maintain a large scale to absorb this non-bank liquidity.

The monetary multiplier is impaired: as a "narrow currency," stablecoins' 1:1 full backing requirement weakens the traditional banking system's credit creation capacity. This "narrowing" increases local stability in the financial system but may reduce the speed of money circulation at the macro level.

Future outlook: global distribution of the digital dollar and sovereign games

The value foundation of the dollar is undergoing a transition from "paper money guaranteed by the rule of law" to "code-driven digital credit." Looking back from 2025 onwards, several directions can be observed.

Stablecoins will become increasingly "tool-like." With the implementation of regulations such as the GENIUS Act, stablecoins will transition from being "internal circulation chips" in the crypto circle to routine configurations in corporate financial management and cross-border trade, with issuers themselves playing a more stable long-term buyer role in the U.S. Treasury market.

Financial infrastructure may move towards a "dual-track parallel" system. If projects like mBridge continue to advance, the world will gradually enter a "dual system era": on one side is a high liquidity system centered on the dollar, SWIFT, and stablecoins; on the other side is a regional system centered on local currency settlements, CBDCs, and CIPS, emphasizing anti-sanction and regional cooperation.

The competition for sovereign credit will be pulled into the digital realm. Stablecoins have "retailized" U.S. dollar credit to any individual with internet access, and this penetration method is more detailed and deeper than traditional bank accounts, almost destined to lead to digital hedging and responses from other sovereign credits.

Conclusion: A piece of paper, a token, behind which lies that entire system

Returning to the original question: why can a piece of paper without commodity value, or a segment of code without physical support, be trusted for the long term?

The key lies not in the paper or code itself but in the entire system built around them: military power provides security, legal systems offer predictability, financial infrastructure provides efficiency, global trade creates rigid demand, and digital technology further amplifies its reach and ease of use.

In this sense, stablecoins are not the terminators of the dollar, but rather a new shell added to the dollar in the digital age. They utilize the global accessibility of blockchain to bring dollar credit into scenarios that previously could not access dollar accounts, and partially embed the concept of "trust" into publicly verifiable code and networks, moving it away from paper contracts and institutional arrangements.