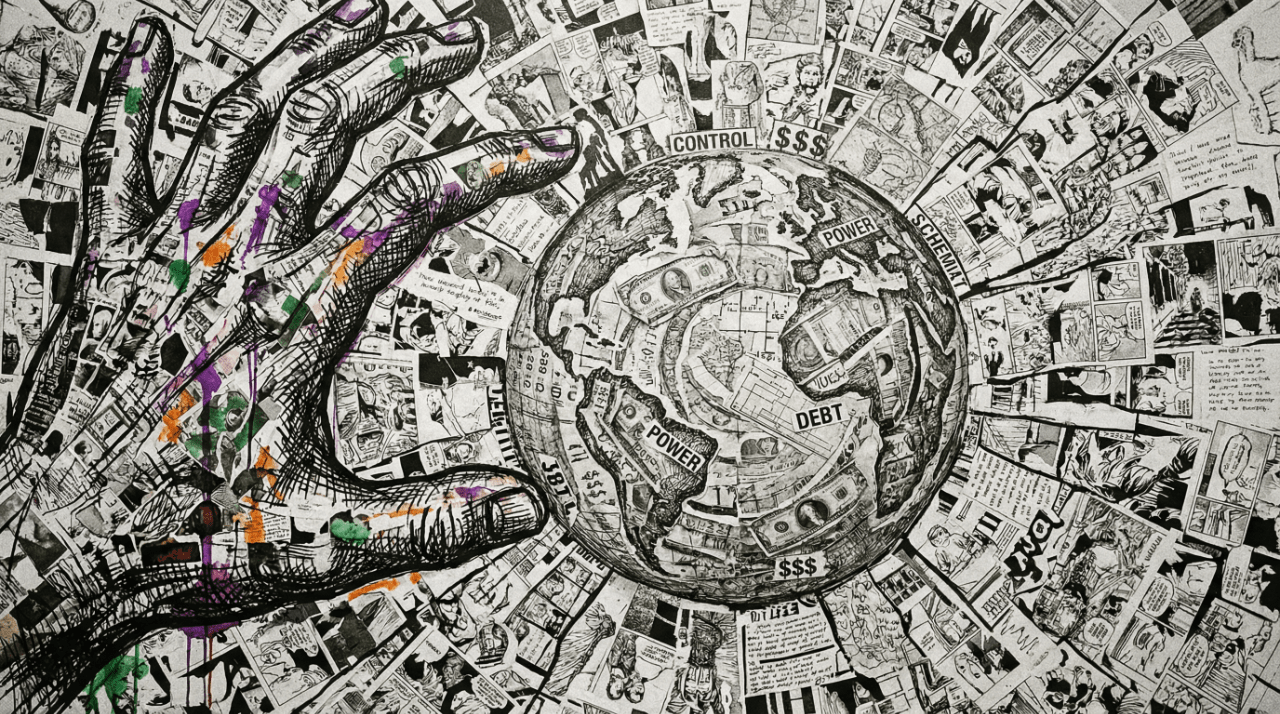

Currency is the underlying protocol of human societal operation; it is not only a medium of exchange but also the deepest power mechanism within social organization. History has proven time and again: the right to issue currency is the most covert and powerful authority in human history; whoever holds it can first access purchasing power and thereby influence economic order and even the political landscape.

Whoever controls the currency controls the future; a new competition has begun. Blockchain is not about eliminating currency, but about democratizing the right to issue currency—allowing algorithms to replace some functions of central banks, enabling private institutions to challenge state issuance, and letting communities replace elites in governance. It is not just an evolution of technology, but a redefinition of power: from the natural scarcity of the golden era to the state monopoly of the fiat currency era, and now to the algorithmic autonomy of the blockchain era, monetary power is returning from extreme centralization to distributed networks.

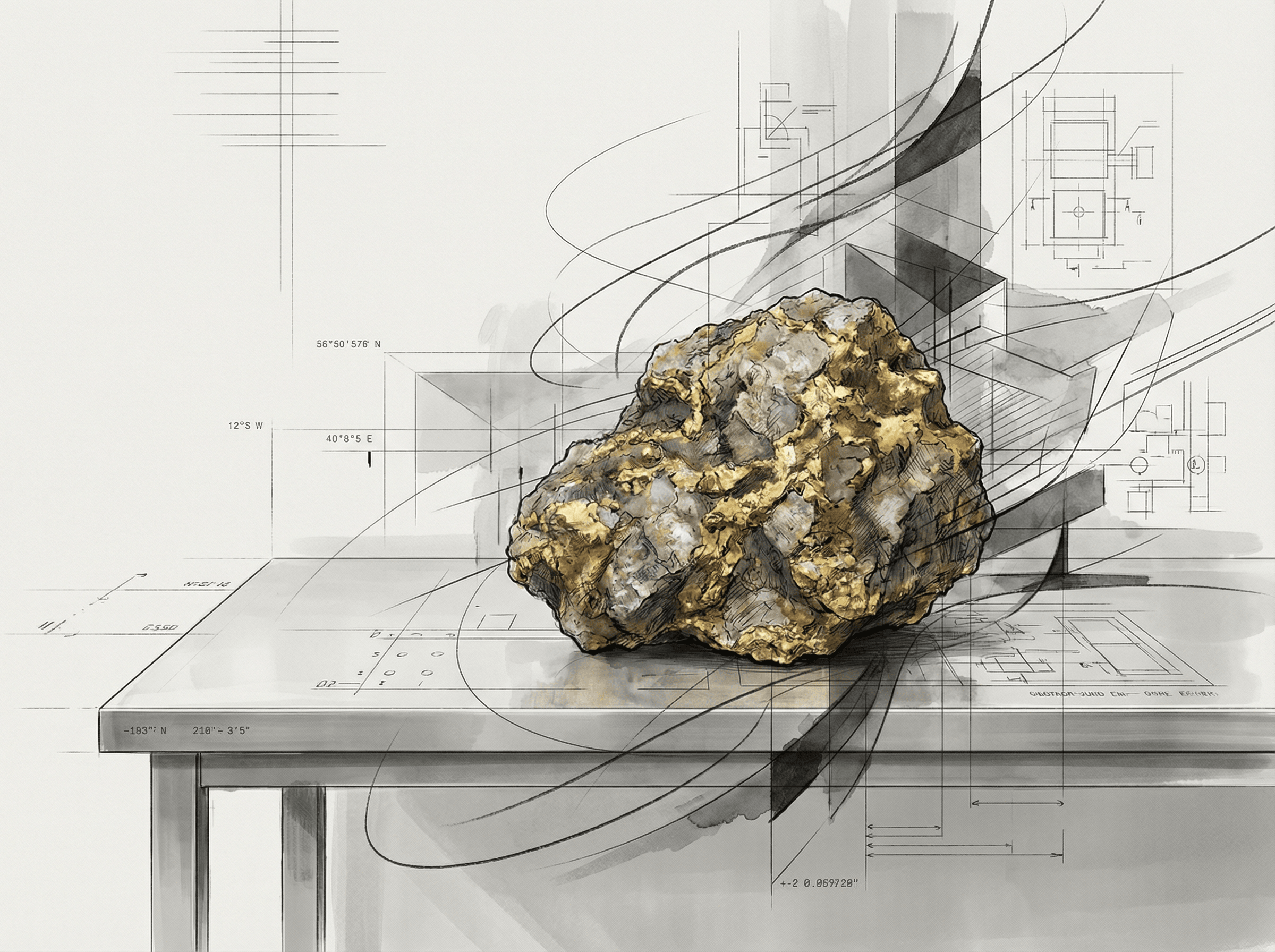

Gold: The Physical Prototype of Power

The source of monetary power can be traced back to the time when gold was regarded as 'natural money.' Unlike fiat currency, gold does not have a centralized issuer; it relies on physical scarcity, divisibility, and cross-civilization verifiability to form a de facto monetary power structure.

The global stock of gold is approximately 208,000 tons, of which central banks and official institutions hold about 35,000 tons, accounting for about 17% of the total. This means that most gold is held by private or market entities, with issuance and distribution being naturally decentralized. The annual increment of gold is less than 2%, and supply is determined by geological conditions and mining costs, making it difficult for any single entity to manipulate on a large scale. Physical scarcity provides a credible constraint on the 'total amount of money.'

Gold has constructed a power closed loop that is completely different from fiat currency:

Physical scarcity limits the supply ceiling, establishing a fact of issuance rights that cannot be arbitrarily increased, thus forming a cross-border pricing consensus, ultimately constructing a natural distribution order based on labor and exchange.

However, this 'decentralized order' dominated by natural scarcity was soon disrupted by political power. Rulers discovered that if they could control the issuance of currency, they could seize social wealth without directly taxing. The emperors of the Roman Empire realized early on that by reducing the purity of gold and silver coins (counterfeiting), they could create more money out of thin air to pay for military expenses. This primitive method, although crude, established a core principle: money is no longer merely a commodity, but the will of the sovereign.

The establishment of the Bank of England in 1694 was a turning point — it exchanged the privilege of exclusive issuance of banknotes for loans to the government. This model reached its peak with the establishment of the Federal Reserve in 1913. Since then, the decentralized private issuance rights have been completely nationalized, and a carefully designed 'central bank-commercial bank' system has replaced the original market competition.

The ultimate driving force behind this monopoly comes from the seigniorage. In the era of fiat money, the marginal production cost of paper (or digital) currency is nearly zero, and its purchasing power is backed by the coercive guarantees of the state. This means that whoever holds the issuance rights has the privilege of mobilizing social resources 'out of thin air.' This temptation is so great that no centralized power can resist the urge to issue currency recklessly for long.

In response to this systemic abuse of power, Hayek offered his most radical prescription in his later years: denationalization of money. He sharply pointed out that if governments are allowed to monopolize currency issuance, money will inevitably become a subordinate of politics. Only by introducing competition mechanisms and allowing private banks to issue different currencies for market selection can we force currency issuers to maintain the stability of currency value for survival. This is not only an economic reform but also a political philosophy declaration about freedom: stripping the government of its monopoly over currency issuance is to deprive it of the ability to plunder wealth at will.

Fiat Currency: The Hidden Extraction Mechanism

The modern credit currency system is not controlled solely by central banks, but is a complex network woven together by 'central banks - commercial banks - the treasury.' In this network, power is no longer a one-way control but reflects a complex game of vertical control and horizontal creation.

Textbooks often describe banks as 'intermediaries' of funds — first absorbing deposits, then issuing loans. But the logic of modern finance is precisely the opposite: loans create deposits. When a bank manager presses the return key to issue a loan, he is not transferring existing savings but creating new purchasing power out of thin air in the borrower's account through double-entry bookkeeping.

This is the 'horizontal issuance right' that commercial banks hold. The supply of broad money (M2) is not entirely determined by central banks, but largely depends on the lending willingness of commercial banks. Data from the Bank for International Settlements shows that the top 25 globally systemically important banks control over 70% of cross-border credit. These financial giants not only decide where the funds flow (into the real economy or asset bubbles) but also effectively share the privilege of currency issuance.

Although commercial banks have the ability to 'create money,' central banks hold the decisive reins — base money. By adjusting reserve ratios and interest rates, central banks control the cost at which commercial banks acquire base money, thereby setting invisible boundaries for credit expansion.

However, this 'central bank-commercial bank' binary structure often becomes distorted in times of crisis. To prevent systemic collapse, central banks must act as 'lenders of last resort,' providing unlimited liquidity support to financial institutions that are too big to fail. This mechanism objectively leads to the socialization of risks and the privatization of returns: banks enjoy the exorbitant profits of credit expansion during prosperity, while during downturns, the costs are borne by the public through inflation.

In the design of power structures, the independence of central banks should be a firewall against monetary over-issuance. But under the reality of political gravity, this defense line is often weak. When war breaks out or economic recession leads to uncontrolled fiscal deficits, governments tend to bypass taxes and directly seek financing from central banks. This phenomenon of fiscal dominance turns central banks from 'inflation gatekeepers' into 'government ATMs.' Once this defense line collapses, money loses its function of value measurement and becomes a covert tool for wealth transfer.

Silent plunder

The concentration of monetary power will ultimately project onto the landscape of social distribution. This is not only a matter of economic efficiency but also a question of fairness. When we shift our gaze from the central bank's balance sheet to the bills of ordinary people, we find a hidden wealth transfer mechanism quietly at work.

Inflation is often downplayed as 'price increases,' but its essence is the dilution of purchasing power. Hayek once pointed out sharply that inflation is not a mild phenomenon but a systematic fraud against the public. It directly weakens the actual purchasing power of ordinary people's savings, constituting a form of involuntary, covert plunder of social wealth — seigniorage.

More cruelly, this dilution does not occur evenly. The 18th-century economist Richard Cantillon discovered a secret long overlooked by modern finance: the process of money flowing into society has a time lag.

Newly added currency always flows first into the groups closest to the 'printing press' — large financial institutions, government contractors, and asset holders. They can use cheap capital to purchase core assets (stocks, real estate) before prices rise. When this currency ultimately flows through layers to the groups furthest from the printing press (salaried workers, savers), the prices for the entire society have already been pushed up.

This kind of 'time difference' leads to systematic wealth plundering: the early birds reap the rewards of the latecomers, and asset holders reap the rewards of laborers. This is why after every round of monetary easing, we can always see the frenzy in the stock market and real estate market, accompanied by a sharp widening of the wealth gap. This is the Cantillon effect; newly created money does not enter the economic system evenly. The people or institutions that receive it first benefit more than those who receive it later, resulting in an uneven distribution of income and wealth.

This long-term abuse of power is eroding the foundation of the fiat currency system — trust. When people realize that the currency in their hands is no longer a container of value but is being diluted at will, seeking alternatives becomes an instinctive choice. The collapse of credit provides the most solid ground for the emergence of 'depoliticized currencies' like Bitcoin and blockchain.

The game between algorithms and centralization

In the face of various shortcomings of the traditional currency system, two forces are reshaping the future monetary landscape: one is a bottom-up algorithmic revolution attempting to build trust without permission through code; the other is a top-down government counterattack trying to use technology to strengthen sovereign control.

In 2009, the genesis block of Bitcoin not only gave birth to a new asset but also announced a new form of power: ownerless currency. It has no board, no central bank president, only a set of openly transparent code rules. Through a hard cap of 21 million coins, it replicates the 'absolute scarcity' of gold in the digital world, cutting off the possibility of inflationary plunder; through the cryptographic design of private key as ownership, it gives individuals the ultimate shield against censorship.

This is precisely the echo of Hayek's prophecy of 'denationalization of money.' Bitcoin proves that the credit of money does not have to stem from the coercive power of the state, but can derive from mathematical certainty. It acts like gold in the digital age, providing an immutable value anchor in a world flooded with credit.

If Bitcoin has reshaped 'money,' then DeFi (decentralized finance) is reshaping 'banks.' In the traditional world, financial power is in the hands of bankers — they decide who can borrow and at what interest rates. In the world of DeFi, all of this is taken over by smart contracts. Borrowing rates are adjusted in real time by algorithms based on supply and demand, and collateral liquidation is automatically executed by code. 'Decentralization' not only reduces friction costs but also breaks down the barriers to entry for financial services.

At the same time, stablecoins (USDT, USDC) and RWA (real-world assets) are connecting the new and old worlds. Stablecoins allow fiat currency to flow freely on the blockchain, breaking through the physical barriers of bank accounts; while RWA technology has revived the monetary function of gold as an ancient value anchor — by mapping physical gold onto the chain, gold not only gains unprecedented liquidity but also possesses programmable payment attributes. An open financial market driven by code, parallel to the traditional banking system, is taking shape.

Faced with the encroachment of algorithms, sovereign states have not stood idly by. CBDC (Central Bank Digital Currency) is a national-level strategy in this game. Unlike decentralized currency, CBDC aims to strengthen rather than weaken the control of central banks. It allows central banks to bypass commercial banks and directly issue currency to the public. While this increases efficiency, it also brings unprecedented monitoring capabilities: every transaction can be tracked, and the use and validity of the currency can even be programmed (e.g., expired vouchers).

This could lead to an unprecedented concentration of monetary power — evolving from 'macro-control' to 'micro-manipulation.' If Bitcoin represents the ultimate in anonymity and freedom, then CBDC may lead to the ultimate in transparency and control. This is not only a technical dispute but a fundamental opposition between two social governance philosophies.

Division and symbiosis

The global monetary system is undergoing an unprecedented revolution. We are not heading towards a single conclusion, but are very likely entering a new era of pluralistic coexistence.

On the one hand, sovereign currencies (including CBDCs) will continue to dominate daily payments and tax systems. Governments will not easily give up their macro-control over the economy; efficient and stable fiat currency remains the lubricant for social operations. But the cost is that financial privacy will have to yield to 'panoramic visibility' regulation.

On the other hand, decentralized currency will become a 'digital ark' to resist inflation and censorship. It provides a way out for individuals who distrust the fiat currency system or find themselves on the brink of turmoil. This is just like Hayek envisioned 'competitive currency' — it does not have to replace fiat currency, but merely needs to exist as a balancing force to compel sovereign currency to maintain restraint.

This will be a long-term game: efficiency and security (centralized advantages) will repeatedly tug against freedom and privacy (decentralized advantages). Money is no longer merely a payment tool but will become a choice of lifestyle: do you choose to trust the cold logic of code or the credit endorsement of institutions?

Conclusion

From the natural order of gold to the political monopoly of fiat currency, to the algorithmic autonomy of blockchain, the game of monetary power has completed a historical return.

Gold proves that currency can stem from natural scarcity; fiat currency proves that credit can arise from state coercion; and Bitcoin and blockchain are proving that consensus can derive from mathematics and community. These three are not simply alternatives but will coexist in the long term in the future.

For ordinary people, the greatest significance lies in the return of choice. For the first time, we have the opportunity to step out of a single currency dependency, to vote with our feet, choosing who will safeguard the fruits of our labor. This game about 'who controls money' may never have a final winner, but as long as the game continues, the monopoly of power cannot run amok — perhaps this is the greatest gift that blockchain brings to this world.