1. Gold is becoming 'cryptoized'

One important reason for gold's continuous new highs this year is the market's strong expectations for the expansion of stablecoins.

Currently, the demand for stablecoins in the capital market is robust. From the perspective of trading volume, the market widely acknowledges two sets of data from ARK Invest and Deutsche Bank: ARK Invest's report shows that the total trading volume of stablecoins globally is expected to reach $15.6 trillion in 2024; while Deutsche Bank's data indicates that in 2024, the total trading volume of global stablecoins is expected to reach $27.6 trillion, surpassing the combined transaction volume of Visa and Mastercard.

Driven by strong demand, the scale of stablecoins is rapidly expanding. As of mid-June this year, the total market value of global stablecoins has exceeded $250 billion; mainstream market expectations are quite explosive, predicting that by 2035, the global stablecoin market size will not be less than $4 trillion, corresponding to a CAGR as high as 32%; the current U.S. government expects that by early 2030, the market size of stablecoins will reach $3.7 trillion, with a corresponding CAGR even reaching 80%.

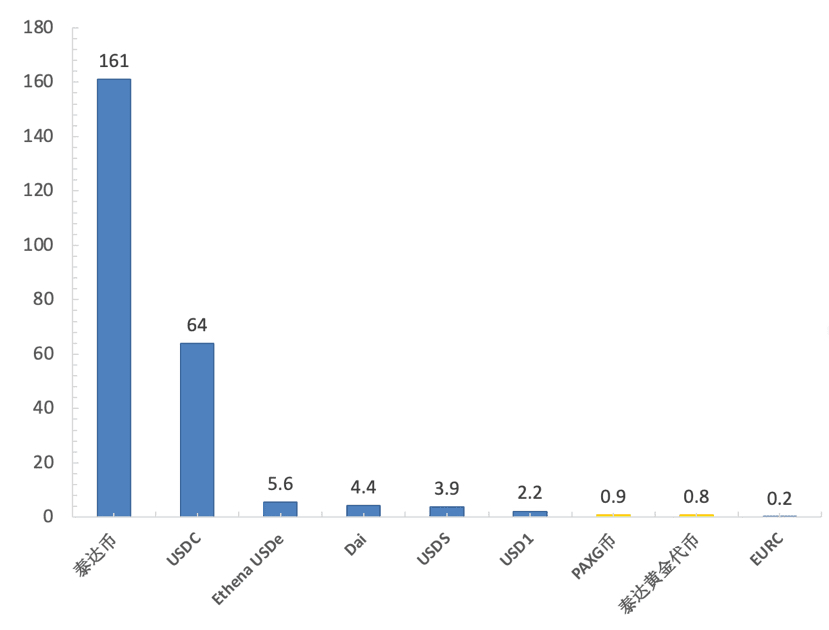

From the perspective of stablecoin types, the main anchoring assets of current stablecoins are the U.S. dollar and U.S. Treasuries, while the scale of gold-backed stablecoins is still very small. As of July this year, the market value of the largest and second-largest gold-backed stablecoins, PAXG and Tether Gold tokens, was only $900 million and $800 million, respectively, while the total market values of USDT and USDC during the same period reached $161 billion and $64 billion, respectively. Thus, it is evident that both in terms of current scale and future market expectations, gold-backed stablecoins still have significant growth potential.

From the perspective of asset allocation, the core logic behind market expectations for the continuous expansion of gold-backed stablecoins lies in: compared to other types of stablecoins, the core advantage of gold-backed stablecoins stems from the scarcity and anti-inflation properties of their anchor—gold.

The aforementioned two properties of gold not only help maintain the long-term stability of the value of gold-backed stablecoins but also provide clients of gold-backed stablecoins with a certain capacity to resist systemic risks. Especially during times when there is a need for risk aversion, the stable value of gold-backed stablecoins, combined with the expansion of gold-backed stablecoins driving up gold prices, constitutes a double insurance for risk aversion.

For gold prices, as the demand for trading gold-backed stablecoins continues to grow, their market size will thus expand continuously; due to the fixed proportion anchoring of stablecoins, the trend of continuous expansion of gold-backed stablecoins will become one of the important forces supporting the long-term rise of gold prices in the future.

Taking Tether, the world's largest stablecoin issuer, as an example, the scale of its issued Tether Gold tokens has grown rapidly; the total market value was approximately $800 million in July this year, and by October 16 it had increased to about $1.6 billion, achieving a doubling in a short period. More notably, Tether announced mid-year that it had established its own independent vault in Switzerland for storing approximately $8 billion in gold reserves, with plans to expand its gold reserves in the future.

In the future, as the entire stablecoin market approaches a trillion-dollar scale, Tether, as the industry leader, and its issued Tether Gold tokens will also reap the benefits of first-mover advantage. Considering the 1:1 anchoring relationship between Tether Gold tokens and physical gold, Tether's gold reserves will be a key factor constraining the scale of its gold-backed stablecoins, and this logic also applies to other types of gold-backed stablecoins.

Therefore, against the backdrop of a long-term prosperous gold-backed stablecoin market, issuers like Tether are also motivated to expand their gold reserves to cope with the rapid expansion of gold-backed stablecoins. Currently, there are market rumors that Tether buys 2 tons of physical gold each week, which is comparable to the monthly gold reserves purchased by the People's Bank of China.

Looking at the recent gold prices, major central banks around the world have significantly continued to purchase gold, making supply and demand relationships gradually become the core factor affecting gold prices. Now, with stablecoin issuers joining the ranks of gold buyers, this further strengthens the pricing logic of supply and demand affecting gold prices. Currently, gold is, in a sense, undergoing a 'crypto-circle' evolution.

II. Optimistic about the long-term strengthening of gold prices

Regarding the recent surge in gold prices, particularly the historic high reached during trading on October 17, one important short-term factor is the disclosure of bad debt issues by two regional banks in the U.S., Zions and Western Alliance, which raised concerns among investors, leading to a significant drop in U.S. bank stocks. Driven by risk aversion sentiment, a large amount of funds flowed into gold, helping gold prices reach a new historic high. Besides this short-term factor, it can be said that various factors are quite favorable for gold.

From the current pricing logic of gold to foresee its future, in terms of supply and demand, the central bank's willingness to purchase gold remains strong and relatively persistent. Combined with stablecoin issuers continuing to buy gold to expand the scale of gold-backed stablecoins, these two important long-term purchasing forces provide stable support for the long-term strengthening of gold prices.

The reason why the central bank will actively and significantly increase its gold holdings lies in risk aversion. On a macro level, in recent years, frequent geopolitical conflicts and trade frictions have continuously impacted the global credit system; at the same time, the scale of U.S. debt remains high, and the credibility of the dollar is being torn apart, indicating potential systemic risks within the dollar system.

Looking back in history, gold prices are usually negatively correlated with the credibility of the dollar. Each round of sustained weakening of dollar credibility tends to usher in historic gold market conditions. The ongoing de-globalization obviously shakes the foundation of dollar credibility, and looking at a recent key event undermining dollar credibility, the Federal Reserve's interest rate cut in September was widely perceived as a 'submissive cut' made under pressure. As the independence of the Federal Reserve further deteriorates, the re-evaluation of dollar credibility enhances the allocation value of gold.

On the other hand, the Federal Reserve has now entered a rate-cutting cycle; similarly, based on the historical correlation between gold prices and the dollar, the easing expectations brought about by rate cuts and the strong demand driving gold prices higher resonate with the core pricing logic. Coupled with recent events such as trade frictions and the sharp decline in U.S. bank stocks, which have triggered a surge in risk aversion sentiment, under the dominance of the aforementioned factors, gold prices have continuously reached new historic highs recently. From a long-term perspective, the sustainability of the rate-cutting cycle will provide continuous and stable support for the upward movement of gold prices.

From a funding perspective, as the valuation of technology sectors represented by artificial intelligence overseas reaches high levels, one possible scenario in the market is: the tech sector peaks and adjusts, and market risk aversion gradually spreads from the geopolitical side to the trading side. Given gold's intrinsic property as a safe-haven asset, along with its prominent long-term allocation value, it is expected to attract some funds, thereby pushing gold prices into a new round of surging trends.

In terms of safety margins, although multiple institutions, including the Shanghai Gold Exchange, the Shanghai Futures Exchange, Industrial and Commercial Bank of China, and China Construction Bank, have issued risk warnings regarding the continuous surge in gold prices, the latest view from the World Gold Council indicates that, from a strategic perspective, the overall holdings of gold remain low, and speculative positions in the futures market, as well as net long positions, have not yet reached historical peaks, suggesting that the market is not yet saturated and gold still possesses sustained attractiveness.#Strategy增持比特币 #美联储利率决议 $BTC