The Federal Reserve officially announced at the FOMC meeting on October 29, 2025, that it will end quantitative tightening (QT) starting December 1, 2025, ceasing the active reduction of Treasury holdings (previously allowing up to $5 billion in maturing Treasury bonds not to be rolled over each month) and will reinvest the full principal of all maturing securities (including MBS), primarily shifting to purchasing short-term Treasury bills (T-bills). This marks the effective end of the QT cycle that began in June 2022, with the Federal Reserve's balance sheet size expected to stabilize around $6.6 trillion (no longer net shrinking).

The core reason for stopping QT

Bank reserves are approaching the lower limit of 'ample reserves', with recent signs of tightening in the money market (such as the SOFR rate briefly surging and increased pressure in the repo market).

Avoid a repeat of the 'cash crunch' incident in September 2019.

The Federal Reserve hopes to stop reducing the balance sheet in advance when reserves are slightly above adequate levels, ensuring smooth transmission of monetary policy.

Note: This is not a restart of quantitative easing (QE), but a shift from 'passively withdrawing liquidity' to 'neutral reinvestment'. MBS will still naturally roll off (about $15-25 billion per month), but will be replaced by an equivalent amount of short-term government bonds, keeping the overall size of the balance sheet roughly stable.

Overall impact on the market (mainly positive, but partially priced in in the short term)

Stopping QT is equivalent to removing the 'invisible tightening headwind' on the market that has lasted for more than three years, no longer withdrawing hundreds of billions of dollars of liquidity from the system each month. Historical experience (after the pause of QT in 2019, U.S. stocks, especially tech stocks, surged) shows that such liquidity turning points are often powerful catalysts for risk assets.

Key timing points and risk reminders

December 1Officially effective, the estimated reinvestment scale for the month is about $80-90 billion (maturity principal of government bonds + MBS), equivalent to a one-time 'replenishment' to the system.

December 9-10 FOMC meeting: the market is concerned about whether to cut interest rates by 25bp (current probability is about 60%). If the rate cut and the end of QT happen simultaneously, it will form a 'double easing' combination, and the market rebound will be stronger.

Risk:

If inflation rebounds beyond expectations (core PCE still close to 2.9%), the Federal Reserve may slow down or even pause interest rate cuts, offsetting some of the benefits of ending QT.Although the U.S. government shutdown has ended, the fiscal deficit is huge (interest expenditure in FY2025 is nearly one trillion dollars), which will continue to push up the supply of U.S. Treasuries in the long term.

The current market has priced in quite a bit in advance (U.S. stocks have rebounded since November), and may 'sell the fact' in the short term.

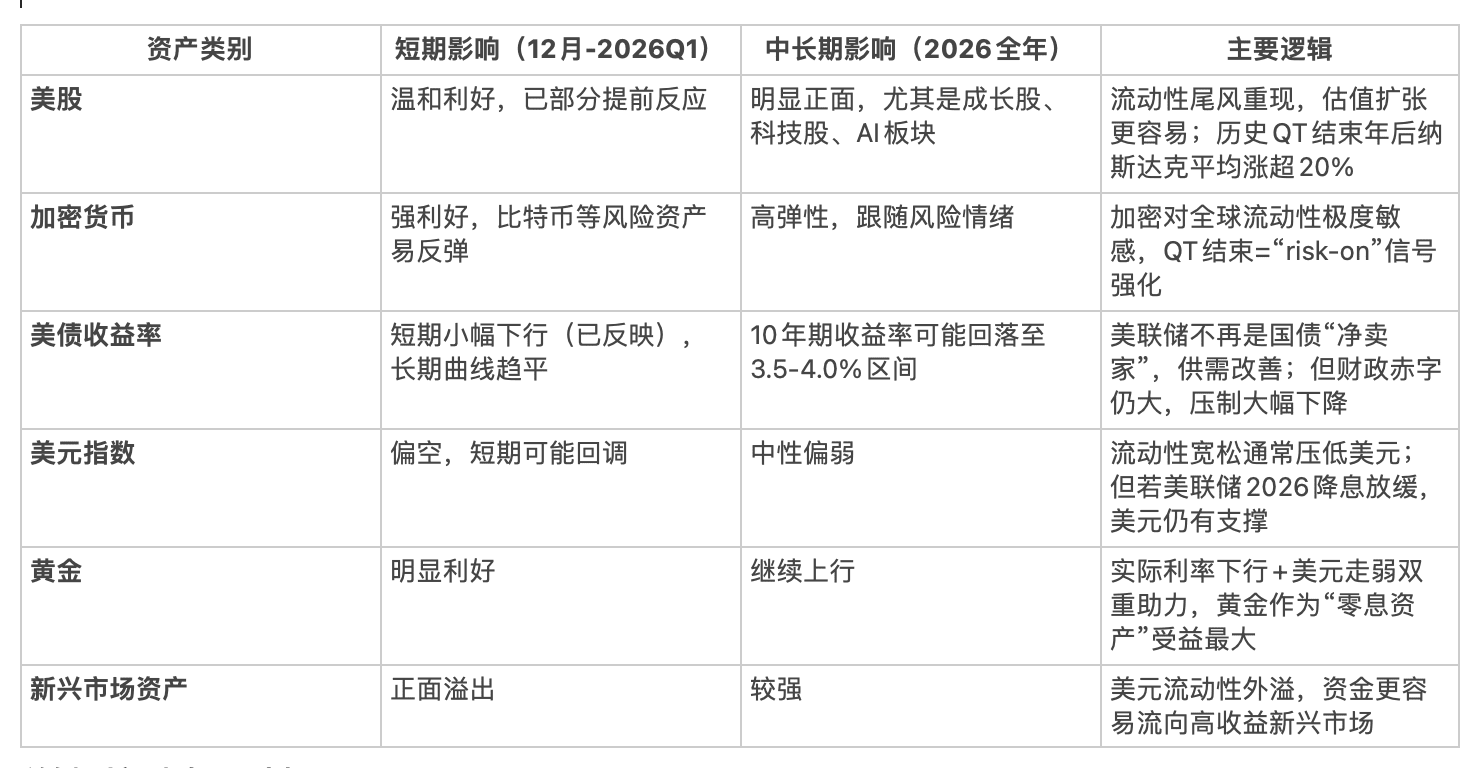

Summary: Stopping QT in December is one of the most important positive liquidity events from the end of 2025 to 2026, equivalent to completely releasing the 'invisible brake' of the past three years. Overall, this is a medium to long-term positive for risk assets (stocks, crypto, gold), especially benefiting high valuation growth stocks and high beta assets like Bitcoin. The market may experience short-term fluctuations to digest this, but the trend has shifted from the 'tail end of tightening' to 'the eve of easing', suggesting to pay attention to the accelerated performance of risk assets after the December FOMC meeting.