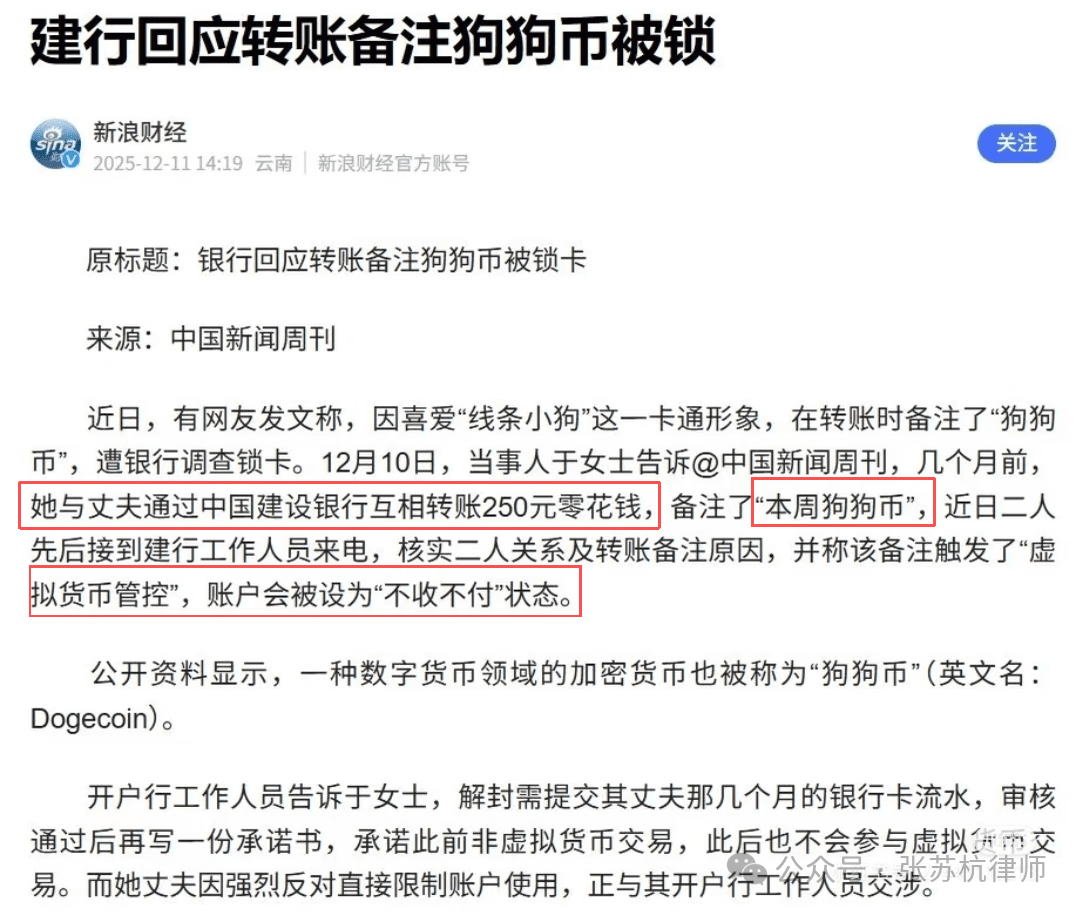

On December 11, China News Weekly reported a story about a transfer remarking 'Dogecoin' that resulted in the Construction Bank freezing the card.

The incident was triggered when a netizen transferred 250 yuan pocket money to her husband through the Construction Bank and noted 'this week's Dogecoin'.

Essentially, it's just a playful remark between a couple. However, it was deemed by the bank's risk control system to trigger virtual currency regulations, and the account was set to a state of no deposits or withdrawals and was subjected to review.

Last month, after the joint meeting of thirteen ministries, I emphasized this point in my article interpreting the regulatory policies on virtual currencies and the future of the industry, as well as during a private live broadcast with friends from the member group.

I remind everyone to pay attention to avoiding inflow risks.

However, many friends still maintain a skeptical attitude because many people’s understanding of the inflow and outflow of virtual currencies is still stuck at the stage where the outflow should avoid receiving illicit funds.

In other words, many people believe that inflow will neither freeze cards nor have any legal basis for freezing cards.

Veteran investors believe that since there is no prohibition on virtual currency, inflow of virtual currency should not be restricted.

However, banks’ actions such as freezing cards and stopping payments are not without legal basis; many people simply do not study policies and regulations, let alone know the source.

The 2021 notice (on further preventing and handling risks of virtual currency trading speculation) (referred to as the 'September 24 announcement') clearly states in Article 9:

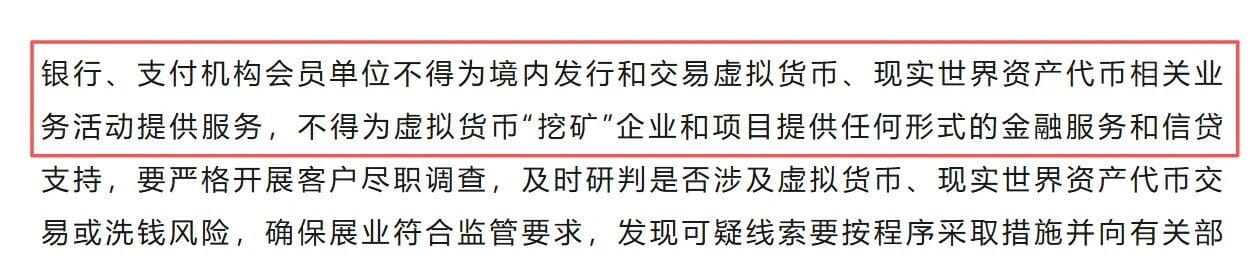

Financial institutions and non-bank payment institutions are not allowed to provide account opening, fund transfer, and clearing services for activities related to virtual currencies.

At this point, someone will definitely jump out and say that the September 24 announcement is not law and does not have the authority to restrict my payment and transfer?

This understanding is incorrect.

First, the September 24 announcement was jointly issued by the People's Bank of China along with the Supreme Court, the Supreme Procuratorate, the Cyberspace Administration, and six other departments. Although it is not law, it is a regulation and still has binding force on banks.

Second, the September 24 announcement clearly states that services for the transfer of virtual currency funds are not allowed. If banks discover any virtual currency inflow and outflow activities, they can naturally refuse to provide any services, including card freezing, payments, and investigations. This is fulfilling the obligations stipulated in Article 9 of the September 24 announcement.

Friends who see this can probably understand why banks can restrict your deposit and withdrawal services when they find that you have virtual currency inflow and outflow activities.

In order to crack down on virtual currencies and stablecoins, the source must be attacked, but this source is neither Tether nor Satoshi Nakamoto.

In the village, the channels and entrances for inflow and outflow are the source.

With this case, I am even more convinced that in the future, not only banks will impose restrictions on inflow and outflow, but all third-party payment tools will encounter similar situations.

It is not difficult to draw this conclusion. On November 28, a special meeting was held by thirteen ministries to jointly combat virtual currency, emphasizing that the prohibitive policy on virtual currency should continue and that virtual currency should still be cracked down on.

On December 5, the seven associations stated that member units are not allowed to participate in virtual currency, real-world asset token issuance, and trading activities within the country, nor directly or indirectly provide relevant services for clients to issue and trade virtual currency and real-world asset tokens within the country.

Although the meeting is not legislation, if you can see through the content of the meeting and perceive the future where virtual currency cannot be legalized and the contradiction that it cannot be controlled technically yet must be controlled objectively, you will definitely draw the above conclusion.

The Dogecoin case may be an isolated incident, but we can see that the regulatory boundaries of the industry have become very clear, and the focus of regulation has long been determined.

For interpretations of specific policies and the future of the industry, you can read this article. It is no exaggeration to say that this article should be a compulsory course for everyone in the circle.

Follow me, and you can get rich!