Written by: Ethan (@ethanzhang_web3), Planet Daily

On December 12, 2025, the Office of the Comptroller of the Currency (OCC) in Washington, D.C., announced conditional approval for five digital asset institutions: Ripple, Circle, Paxos, BitGo, and Fidelity Digital Assets, to transition into federally chartered national trust banks.

This decision has not been accompanied by significant market fluctuations, but it is widely viewed by regulators and the financial community as a watershed moment. For the first time, cryptocurrency companies that have long been on the fringes of the traditional financial system and frequently encountered interruptions in banking services have been formally incorporated into the U.S. federal banking regulatory framework under the identity of 'banks.'

The changes did not come suddenly, but they are thorough enough. Ripple plans to establish the 'Ripple National Trust Bank,' while Circle will operate the 'First National Digital Currency Bank.' These names themselves clearly convey the signals released by the regulatory authorities: digital asset-related businesses are no longer just 'high-risk exceptions' passively subject to scrutiny but are allowed to enter the core layer of the federal financial system under clear rules.

This shift stands in stark contrast to the regulatory environment of a few years ago. Especially during the turbulent banking period of 2023, the crypto industry found itself deeply mired in the so-called 'de-banking' dilemma, being systematically cut off from the dollar settlement system. With the signing of the (GENIUS Act) by President Trump in July 2025, stablecoins and related institutions gained a clear federal legal status for the first time, providing the institutional basis for OCC's centralized licensing.

This article will focus on four aspects: 'What is a federal trust bank?', 'Why is this license important?', 'The regulatory shift in the Trump era,' and 'The responses and challenges of traditional finance,' to sort out the institutional logic and real impact behind this approval. The core judgment is that the crypto industry is transitioning from being 'external users' reliant on the banking system to becoming a part of the financial infrastructure. This not only changes the cost structure of payments and settlements but is also reshaping the definition of 'banking' in the digital economy.

What is a 'federal trust bank'?

To understand the real weight of this OCC approval, it is first necessary to clarify a commonly misunderstood issue: this is not five crypto companies receiving traditional 'commercial bank licenses.'

The OCC has approved the status of 'national trust bank.' This is a type of bank charter that has existed for a long time in the U.S. banking system, primarily serving legacy management, institutional custody, and other business forms in the past. Its core value lies not in 'how much business can be done,' but in the regulatory hierarchy and infrastructure status.

What does a federal charter mean?

In the U.S. dual banking system, financial institutions can choose to be regulated by state or federal governments. The two are not simply parallel in compliance intensity but have clear power hierarchy differences. A federal charter bank license issued by the OCC means that the institution is directly regulated under the Treasury Department system and enjoys 'federal priority,' no longer needing to adapt one by one to state regulatory rules in compliance and operational aspects.

The legal foundation behind this can be traced back to the (National Bank Act) of 1864. Over the next century and a half, this system became an important institutional tool for the formation of a unified financial market in the U.S. This is particularly critical for crypto companies.

Prior to this approval, whether it was Circle, Ripple, or Paxos, wanting to operate compliantly across the U.S. had to apply for money transmission licenses (MTL) in all 50 states, facing a 'puzzle' system with completely different regulatory standards, compliance requirements, and enforcement scales. This not only incurs high costs but also severely limits business expansion efficiency.

After transitioning to a federal trust bank, the regulatory subject shifts from various state financial regulatory agencies to the OCC. For enterprises, this means a unified compliance pathway, a national business passport, and a structural elevation of regulatory credibility.

A trust bank is not a 'miniature commercial bank.'

It is important to emphasize that a federal trust bank is not equivalent to a 'fully functional commercial bank.' The five institutions approved this time are not allowed to accept public deposits insured by the FDIC, nor can they issue commercial loans. This is also one of the core reasons why traditional banking organizations (such as the Bank Policy Institute) have questioned this policy, as they believe it represents an unequal entrance of 'rights and obligations.'

However, from the perspective of the business structure of crypto enterprises, these restrictions are highly compatible. Taking stablecoin issuers as an example, whether it is Circle's USDC or Ripple's RLUSD, their business logic is built on 100% reserve asset backing. Stablecoins do not engage in credit expansion and do not rely on partial reserve lending models, thus there is no systemic risk arising from the 'mismatch of deposit and loan terms' that traditional banks face. Under this premise, introducing FDIC deposit insurance is neither necessary nor would it significantly increase compliance burdens.

More importantly, the core of the trust bank license lies in fiduciary responsibility. This means that licensed institutions must legally strictly separate client assets from their own funds and prioritize client interests. This is of strong practical significance for the entire crypto industry, especially after the FTX incident of misusing client assets, where asset separation is no longer a company promise but a mandatory obligation under federal law.

From 'custodian' to 'payment node.'

Another layer of significance to this change is that regulatory agencies have made a critical shift in interpreting the scope of 'trust bank' business. OCC head Jonathan Gould has explicitly stated that the new federal bank entrance 'provides consumers with new products, services, and sources of credit, and ensures that the banking system is dynamic, competitive, and diverse.' This lays the policy foundation for accepting crypto institutions.

In this framework, the 'conversion' completed by Paxos and BitGo from state trust to federal trust bank carries strategic value far beyond mere name change. The core is that the OCC system grants federal trust banks a critical right: the qualification to apply for access to the Federal Reserve payment system. Therefore, their true goal is not the title of 'bank' but rather to seize the channel to directly access the central bank's core settlement system.

Taking Paxos as an example, although it had previously become a compliance benchmark under strict regulation by the New York State Department of Financial Services, state licenses have inherent limitations: they cannot directly integrate into the federal payment network. The OCC's approval document clearly states that the newly converted entity can continue to engage in stablecoin, asset tokenization, and digital asset custody businesses. This is equivalent to formally recognizing at the institutional level that the issuance of stablecoins and asset tokenization has become legitimate 'banking business.' This is not just a breakthrough for individual companies but a substantial expansion of the functional scope of 'banking.'

Once finalized, these institutions will likely connect directly to central bank payment systems like Fedwire or CHIPS, no longer needing to rely on traditional commercial banks as intermediaries. The leap from 'managed asset managers' to 'direct nodes in the payment network' is the most structurally significant breakthrough in this regulatory shift.

Why is this license so valuable?

The true value of the federal trust bank license lies not in the identity of 'bank' itself, but in the potential to open a direct channel to the Federal Reserve's clearing system.

This is also why Ripple CEO Brad Garlinghouse referred to this approval as a 'huge step forward,' while traditional banking lobby groups (BPI) expressed significant unease. For the former, it represents an enhancement of efficiency and certainty; for the latter, it means that the long-standing monopoly of financial infrastructure is being redistributed.

What does direct connection to the Federal Reserve mean?

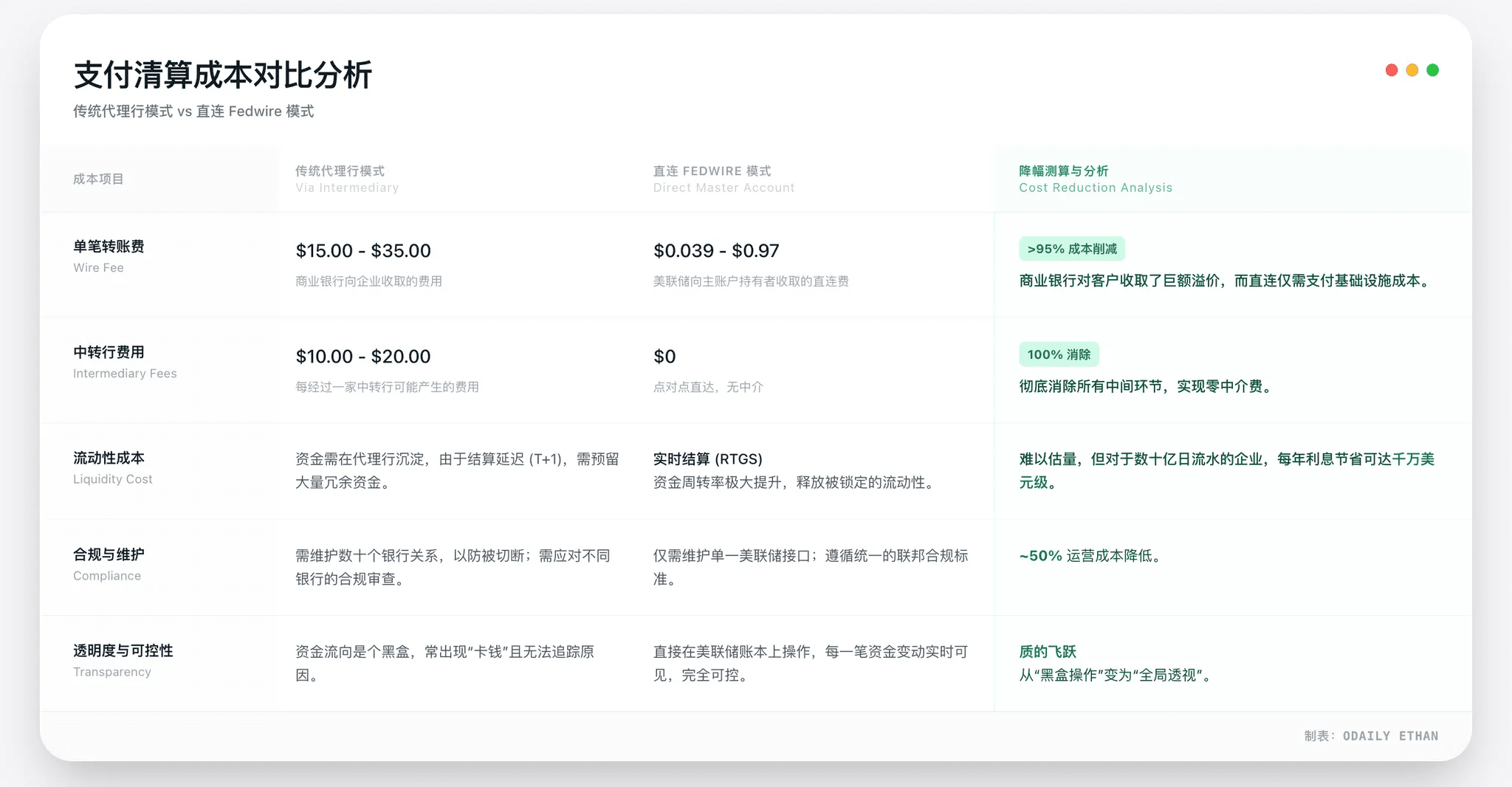

Prior to this, crypto companies had always been on the 'periphery' of the dollar system. Whether Circle was issuing USDC or Ripple providing cross-border payment services, any final settlement involving dollars had to be completed through commercial banks as intermediaries. This model is referred to in financial terms as the 'correspondent banking system.' On the surface, it only seems to be a longer process, but in essence, it brings three long-standing issues that trouble the industry.

First is the uncertainty of survival rights. In recent years, the crypto industry has repeatedly encountered situations where banks unilaterally terminated services. Once correspondent banks withdraw, the fiat channels of crypto enterprises can be cut off in a very short time, causing their operations to come to a halt. This is what the industry refers to as the 'de-banking' risk.

Secondly, there are issues of cost and efficiency. The correspondent banking model means that every capital flow must go through multiple layers of bank clearing, each layer accompanied by fees and time delays. This structure is inherently unfriendly to high-frequency payments and stablecoin settlements.

The third is settlement risk. The traditional banking system generally adopts T+1 or T+2 settlement rhythms, during which funds in transit not only occupy liquidity but also expose themselves to banking credit risk. When Silicon Valley Bank collapsed in 2023, Circle had approximately $3.3 billion of USDC reserves briefly stranded in the banking system, an incident that is still viewed as a cautionary case for the industry.

The federal trust bank identity changes exactly this structure. At the institutional level, licensed institutions have the qualification to apply for a Federal Reserve 'master account.' Once approved, they can directly access federal-level clearing networks like Fedwire, completing real-time, irrevocable final settlements in the dollar system without relying on any commercial bank intermediaries.

This means that in the key process of fund settlement, institutions like Circle and Ripple are standing for the first time at the same 'system level' as JPMorgan and Citibank.

Extreme cost advantages, rather than marginal optimization.

The reduction in payment costs through obtaining a master account is structural rather than marginal. The core principle lies in the direct connection to the Federal Reserve payment system (such as Fedwire), which completely bypasses the multi-layer intermediaries of traditional correspondent banks, thus eliminating corresponding intermediary fees and markups.

We can extrapolate based on industry practices and the Federal Reserve's public rate mechanism in 2026. After calculations, it is found that in high-frequency, large-value scenarios like stablecoin issuance and institutional payments, this direct connection model could reduce overall settlement costs by about 30%-50%. Cost reductions mainly come from two aspects:

Direct rate advantage: The Federal Reserve's single charge for Fedwire large payments is far lower than commercial banks' wire transfer quotes.

Simplified structure: Various fees, account maintenance costs, and liquidity management costs associated with intermediary banks have been eliminated.

Taking Circle as an example, the nearly $80 billion USDC reserves it manages face tremendous capital flow daily. If direct connection is achieved, just in terms of payment channel fees alone, the amount saved annually could reach hundreds of millions of dollars. This is not a minor optimization but a fundamental cost restructuring at the business model level.

Therefore, the cost advantage brought by obtaining master account eligibility is certain and significant, and it will directly translate into a core moat for stablecoin issuers in rate competition and operational efficiency.

The legal and financial attributes of stablecoins are changing.

When stablecoin issuers operate as federally chartered trust banks, the attributes of their products also change accordingly. Under the old model, USDC or RLUSD was closer to 'digital certificates issued by technology companies,' with its security highly dependent on the issuer's governance and the robustness of cooperating banks. However, under the new structure, the reserves of stablecoins will be placed under the fiduciary system regulated by the OCC and legally isolated from the issuer's own assets.

This is not equivalent to central bank digital currencies (CBDC), nor does it have FDIC insurance, but under the combination of '100% full reserve + federal-level regulation + fiduciary responsibility,' its credit rating is significantly higher than that of most offshore stablecoin products.

The more realistic impact lies in the payment aspect. Taking Ripple as an example, its ODL (On-Demand Liquidity) product has long been constrained by banking hours and the opening rhythm of fiat channels. Once it enters the federal clearing system, the switching between fiat currencies and on-chain assets will no longer be constrained by time windows, significantly enhancing the continuity and certainty of cross-border settlements.

The market's reaction has been more rational.

Although this development is seen as a milestone within the industry, the market reaction has not shown dramatic fluctuations. Whether for XRP or USDC related assets, price changes have been relatively limited. However, this does not mean that the value of the license is underestimated; rather, it likely indicates that the market has viewed it as a long-term institutional change rather than a short-term trading topic.

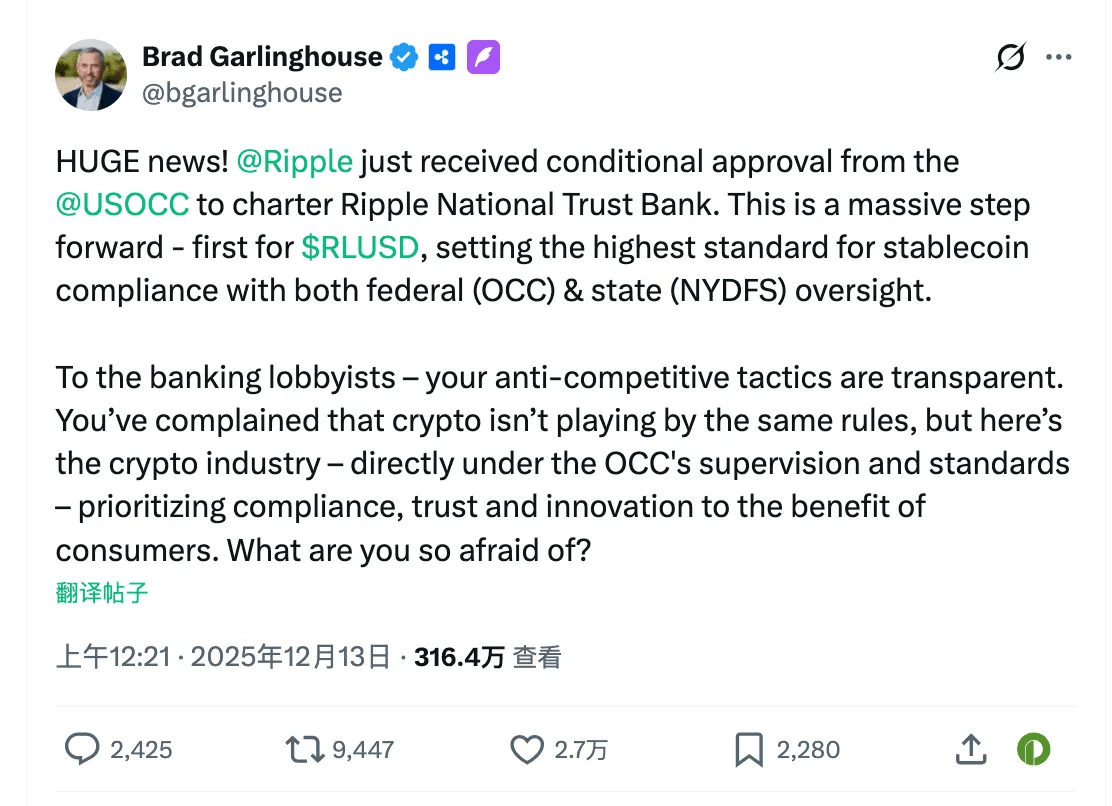

Ripple CEO Brad Garlinghouse defined this development as the 'gold standard for compliance pathways for stablecoins.' He not only emphasized that RLUSD is now under the dual regulation of federal (OCC) and state (NYDFS) oversight, but also directly challenged traditional banking lobby groups, stating: 'Your anti-competitive tactics have been exposed. You complain that the crypto industry does not follow the rules, but now we are under the direct regulatory standards of the OCC. What are you really afraid of?'

At the same time, Circle also pointed out in related statements that the national trust bank charter will fundamentally reshape institutional trust, allowing issuers to provide more fiduciary digital asset custody services to institutional clients.

The statements of both converge: from 'being served by banks' to 'becoming part of banks,' crypto finance is entering a whole new phase. The federal trust bank license is not just a permit; it also paves a safe path for institutional capital that has been hesitant due to compliance uncertainties to enter the crypto market.

The 'golden period' of the Trump era and the (GENIUS Act).

Looking back three to four years, it is hard to imagine that crypto companies could gain federal recognition as 'banks' by the end of 2025. The driving force behind this change is not technical breakthroughs but fundamental shifts in the political and regulatory environment.

The return of the Trump administration and the implementation of the (GENIUS Act) together paved the way for crypto finance's access to the federal system.

From 'de-banking' to institutional acceptance.

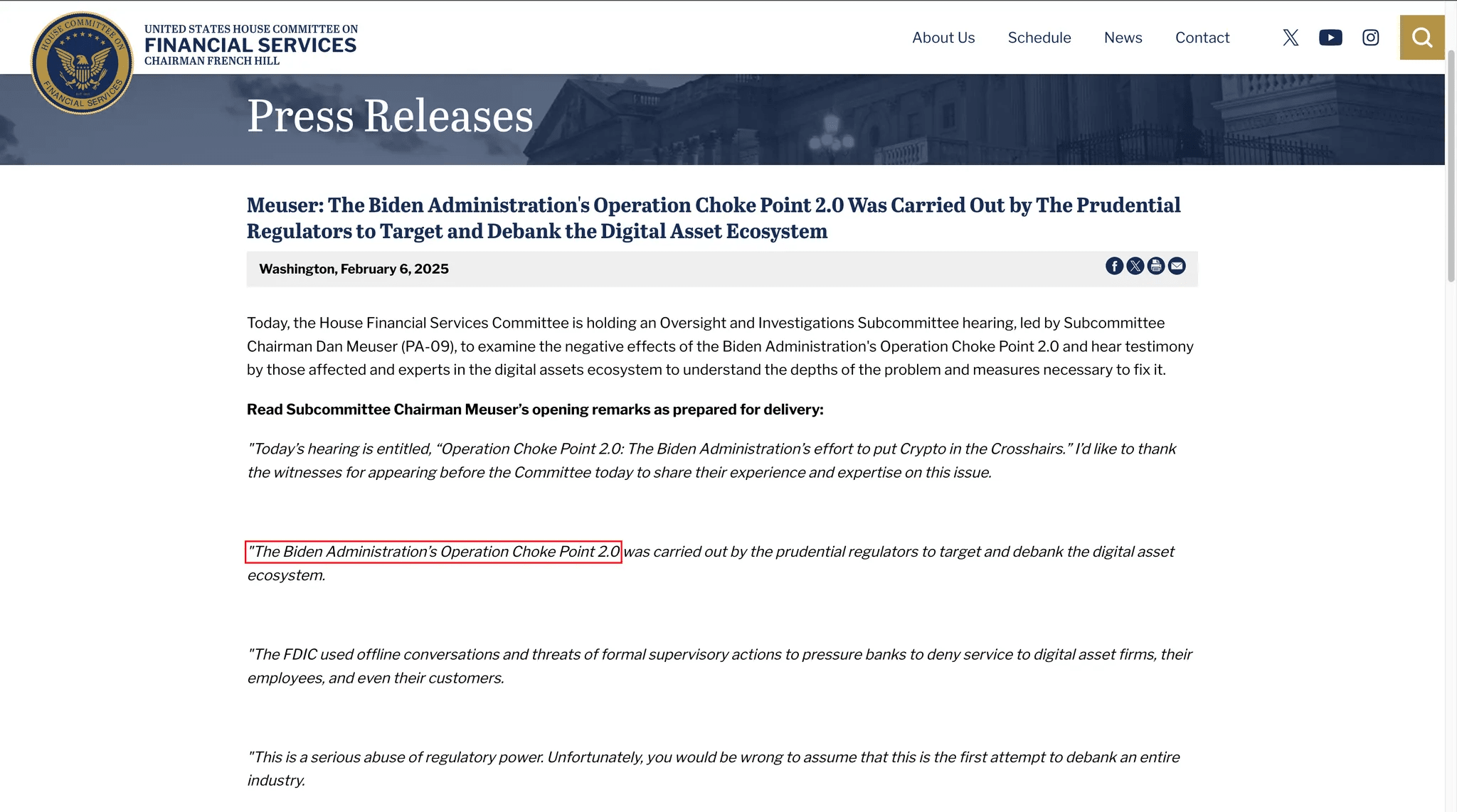

During the Biden administration, the crypto industry has been in an environment of strong regulation and high uncertainty. Especially after the collapse of FTX in 2022, the main regulatory tone shifted towards 'risk isolation,' with the banking system being required to distance itself from crypto businesses.

This phase is referred to internally within the industry as 'de-banking' and has been described by some lawmakers as 'Operation Choke Point 2.0.' According to the subsequent investigations by the House Financial Services Committee, multiple banks severed their cooperation with crypto enterprises under informal regulatory pressure. The successive exits of Silvergate Bank and Signature Bank are a concentrated reflection of this trend.

The regulatory logic at the time was very clear: rather than struggling to regulate crypto risks, it is better to isolate them outside the banking system.

This logic underwent a fundamental reversal in 2025.

Trump publicly supported the crypto industry multiple times during his campaign, emphasizing the goal of making the U.S. a 'global center for crypto innovation.' After regaining power, crypto assets were no longer simply viewed as sources of risk but incorporated into a broader financial and strategic consideration.

The key shift is that stablecoins are beginning to be viewed as extensions of the dollar system. On the day the (GENIUS Act) was signed, the White House statement clearly pointed out that regulated dollar stablecoins help expand demand for U.S. Treasury bonds and strengthen the international status of the dollar in the digital age. This essentially redefines the role of stablecoin issuers in the U.S. financial system.

(GENIUS Act) institutional role.

In July 2025, Trump signed the (GENIUS Act). The significance of this act is that it establishes a clear legal identity for stablecoins and related institutions at the federal level for the first time. The act explicitly allows non-bank institutions to be accepted for federal regulation as 'qualified payment stablecoin issuers' after meeting certain conditions. This provides an institutional entry point into the federal framework for companies like Circle and Paxos that were originally outside the banking system.

More importantly, the act imposes strict requirements on reserve assets: stablecoins must be fully backed 100% by highly liquid assets such as U.S. cash or short-term U.S. Treasury securities. This effectively eliminates the space for algorithmic stablecoins and high-risk allocations, and aligns closely with the trust bank model of 'not taking deposits, not lending.'

Moreover, the act establishes a priority repayment right for stablecoin holders. Even if the issuing institution goes bankrupt, the relevant reserve assets must be prioritized for settling stablecoins. This clause significantly reduces regulatory concerns about 'moral hazard' and enhances the credibility of stablecoins at the institutional level.

In this framework, the OCC granting federal trust bank licenses to crypto companies has naturally become a regulatory implementation.

Defenses of traditional finance and future challenges.

For the crypto industry, this is a long-overdue institutional breakthrough; but for the entrenched interests on Wall Street, it feels more like a territory invasion that must be countered. The OCC's approval of five crypto institutions transitioning to federal trust banks has not led to unanimous applause; rather, it quickly triggered fierce defenses from traditional banking alliances represented by the Bank Policy Institute (BPI). This 'war between new and old banks' has only just begun.

The fierce counterattack from BPI: three core accusations.

The BPI represents the interests of giants like JPMorgan, Bank of America, and Citibank. At the first moment the OCC made its decision public, its executives issued sharp criticisms, with core arguments directly targeting the deep conflicts in regulatory philosophy.

First, it concerns the regulatory arbitrage of 'hanging a sheep's head while selling dog meat.' The BPI pointed out that these crypto institutions applying for 'trust' licenses are essentially covering their ears while stealing a bell, and they are actually engaged in core banking activities such as payments and settlements, with systemic importance even exceeding that of many mid-sized commercial banks.

However, through the trust license, its parent company (such as Circle Internet Financial) cleverly avoids the Federal Reserve's consolidated supervision that must be accepted as a 'bank holding company.' This means that regulators have no right to review the parent company's software development or external investments—if the parent company's code vulnerabilities lead to bank asset losses, this will create a huge risk exposure in a regulatory blind spot.

Finally, there is the panic regarding systemic risks and the lack of a safety net. Since these new trust banks do not have FDIC insurance backing, once the market panics about stablecoins losing their peg, traditional deposit insurance cannot serve as a buffer. The BPI argues that this unprotected liquidity exhaustion could spread rapidly, evolving into a systemic crisis similar to that of 2008.

The Federal Reserve's 'last hurdle.'

The OCC's issuance of licenses does not equal everything is settled. For these five newly designated 'federal trust banks,' the final and most critical hurdle to accessing the federal payment system—the right to open a master account—remains tightly held by the Federal Reserve.

Although the OCC recognized their banking identity, under the dual banking system in the U.S., the Federal Reserve has independent discretion. Previously, Wyoming-based crypto bank Custodia Bank initiated a lengthy lawsuit after being denied by the Federal Reserve to open a master account, and this precedent indicates that there is still a huge gap between getting a license and truly accessing Fedwire.

This is also the next main battlefield for traditional banking (BPI) lobbying. Since it is impossible to prevent the OCC from issuing licenses, traditional banking forces will inevitably pressure the Federal Reserve to set extremely high thresholds when approving master accounts—such as requiring these institutions to prove their anti-money laundering (AML) capabilities are on par with comprehensive banks like JPMorgan, or require their parent companies to provide additional capital guarantees.

For Ripple and Circle, this struggle has just entered the second half: if they obtain licenses but cannot open a master account with the Federal Reserve, they will still have to operate through the correspondent banking model, and the gold-plated 'national bank' title will lose much of its value.

Conclusion: The future is not just a regulatory game.

It is expected that the future struggle surrounding crypto banking will clearly not stop at the level of licensing.

On one hand, the attitude of state regulatory agencies remains uncertain. Powerful state regulators, represented by the New York State Department of Financial Services (NYDFS), have long played a leading role in crypto regulation. As federal priorities expand, whether state regulatory authority will be weakened may trigger new legal disputes.

On the other hand, while the (GENIUS Act) has already come into effect, many implementation details are still pending formulation by regulatory agencies. Specific rules such as capital requirements, risk isolation, and cybersecurity standards will become policy focuses in the coming period. The competition among different stakeholders is likely to unfold around these technical terms.

In addition, changes at the market level are also worth noting. As crypto institutions gain banking identities, they may become either cooperative partners of traditional financial institutions or potential acquisition targets. Whether traditional banks acquire crypto institutions to fill technological gaps or crypto companies reverse-enter banking, the financial landscape could undergo structural adjustments as a result.

It is certain that this approval from the OCC is not the end of the controversy but a new starting point. Crypto finance has entered the institutional framework, but finding a balance between innovation, stability, and competition will still be a question that U.S. financial regulation must answer in the coming years.