Semiconductors fell sharply. Samsung, SK hynix, and even the ones listed in the U.S. market all dropped a lot. But I think this move isn’t at the end yet. The panic this time mainly comes from the news that meta’s AI computing capacity was idle. However, you have to know that its late-July earnings report will definitely still look good; a single piece of news can’t immediately affect the earnings report. So what you should do, you probably already know.

Then let’s continue with the U.S.-listed semiconductor series. Earlier, I talked about AMAT, the “deposition leader,” LRCX, the “etching leader,” and KLAC, the “inspection leader.” And there’s also ASML, the lithography machine leader.

1.ASML

There’s probably no need to say more: the name should be extremely well-known. Back when the semiconductor cycle wasn’t booming yet, this company was heavily promoted. You’ve definitely heard, to one degree or another, about the “lithography machine.” During the period when China’s chips were blocked, the media also reported on why China couldn’t make chips: one of the core steps is the “lithography machine.”

Currently, only ASML worldwide can mass-produce EUV (extreme ultraviolet) lithography machines. All 5nm, 3nm, 2nm, and even future 1.4nm chips must use its equipment.

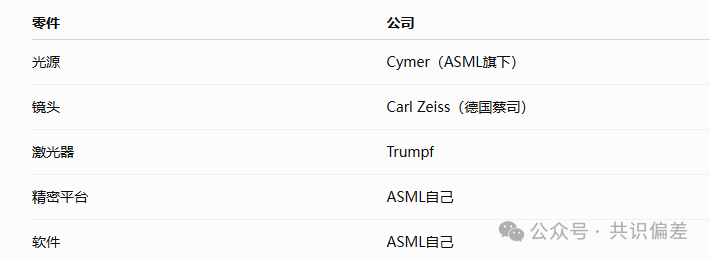

Also, EVU lithography machines are not something that only one company, ASML, can manufacture. Its components are as follows

Among them, Zeiss’s lens precision reaches the atomic level, with an error of no more than 0.1 NM—no one else can do this!

Then the price of a single EVU lithography machine is about $200–300 million. It contains more than 100,000 parts, weighs 180 tons, and takes one year to complete optical calibration.

In the top-tier lithography machine field, ASML is #1 in the world. Its technical accumulation cannot be surpassed within the next 10 years!

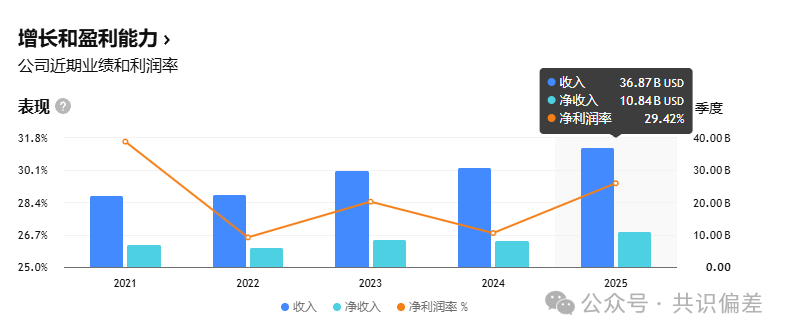

The current market cap is 713.4 billion yuan, with a P/E ratio of 61. Revenue has grown steadily in recent years. In 2025, revenue was 36.8 billion, and net income was 10 billion. Currently, institutions project a 10% year-over-year revenue growth rate each year.

The stock price rose from 3 in 1999 to 1,769 today—a gain of 580x. I looked at the historical K-line chart, and it’s almost impossible to have a large pullback. So if you want to play long term with this, I think there’s no big problem.

2. CRDO

This is also a company for high-speed interconnection of AI server data, and it is very focused on doing just this. Its official mission is: to provide faster, more energy-efficient, and more reliable high-speed connectivity solutions for AI, cloud computing, and hyperscale data centers. It’s in the same track as the previously mentioned Astera Labs, but there’s a slight difference: Astera Labs focuses specifically on high-speed interconnection between GPUs and memory.

And CRDO is currently more focused on server-side externals—for example, from server A to a switch to server B.

Its main products include:

1. SerDes IP. This is also CRDO’s core product. It mainly converts data from GPUs into a super-high-speed signal, then restores it at the other end—for example, at another server.

2. AEC (dynamic cables)

3. Optical DSP, optical modules

4. PCIe Retimer

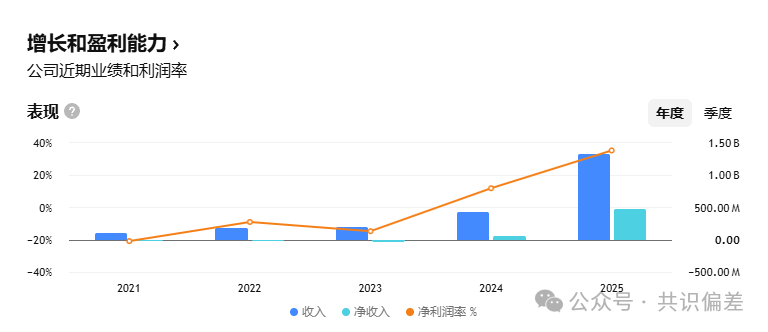

The current market cap is 45 billion yuan, with a P/E ratio of 104. Revenue started to surge in 2025: annual revenue was 1.3 billion, and net income was 470 million. The 2026 revenue forecast is 2.4 billion, doubling compared with 2025. So my calculation puts the P/E at 50, but it’s still somewhat high.

The stock price rose from the 2025 low of 30 to the current 240, a 7x increase. So you definitely can’t jump in on the short term—you need to wait for a pullback.

For the long term, I think it may be a bit tough. I estimate this semiconductor cycle will only last about 1–2 years. After AI really breaks out, it’s probably harder to play.

In summary, as of now, the four major equipment-related leaders still look worth considering. The fundamentals are very strong, and their moats are extremely deep!$CRDO.US