The logic of income-generating stablecoins (YBS) mimics the banking industry; this is just the surface. It also needs to address where user income comes from, how it is generated, and how to maintain the long-term operation of the project. The collapse of DeFi projects is commonplace in finance, as evidenced by SBF's incarceration, but the systemic risk from Silicon Valley Bank requires immediate action from the Federal Reserve.

Era of Excess Leverage

Seeking profit reflects product thinking; in financial terms, it expresses speculation, while significant price differences are the source of arbitrage, and long-term volatility requires risk hedging.

The opposite of the principle's movement, after introducing computer technology, the financial industry has undergone three stages in quantitative speculation:

• Portfolio Insurance: Diversify investment targets for value preservation, quantify risk levels and price them;

• Leverage (LTCM): Accumulate sand into a tower; tiny trading profits can be leveraged for larger gains;

• Credit Default Swaps: CDS is not a demon; derivative risk control fails, devolving into pure gambling;

In the current financial world, significant price differences in space have disappeared. Daily, small, and decentralized transactions are the norm. On-chain MEV and off-chain CEX are Web3's imitation of TradFi.

Long-term preservation of value in time is no longer mainstream; leveraging, extremism, and speculation are now the goals, with hedging itself becoming the purpose. Forward risks will never bring about the future.

In the above context, YBS project parties essentially face a dilemma: if APY/APR is not high enough, it is difficult to attract funds to increase TVL; but if promises are too high, it will inevitably lead to a Ponzi scheme, ultimately resulting in a collapse in any of the TGE, financing, harvesting, scoring, VC, or exchange processes.

Hedging is essentially arbitrage; momentum cannot be avoided.

Stablecoins now exhibit three schools: replacing Visa, imitating USDT, and the small 'Ethena' version. 1 Visa relies on terminals, channels, and fees to occupy most of the income from the clearing system. Payment is merely an entry point; the core is the B-end advantage of the clearing network. However, we see crypto-native funds and projects beginning to work towards this direction.

Stablecoins now exhibit three schools: replacing Visa, imitating USDT, and the small 'Ethena' version.

① Visa relies on terminals, channels, and fees to occupy most of the income from the clearing system. Payment is merely an entry point; the core is the B-end advantage of the clearing network. However, we see crypto-native funds and projects beginning to work towards this direction.

Ripple only wants to sell coins; replacing #swift is just a gimmick. Starting from Stablecoin payments is more appropriate and more suitable for commercialization. SWIFT is a game of power, not a commercial domain.

② Imitating USDT reaching its peak after @circle IPO, USD1 is merely a small trial run for Little Trump. More banks and other TradFi entities will join the fray; this is the opportunity left for the defeated party of the old era in the new age.

③ People only remember the first; Armstrong is the first person to land on the moon and the first height of Mount Everest.

@Ethena has many imitators, but how many can become the second? The following five have the highest winning chances, with Sky's USDS resembling Ondo, which has already given up on the ultimate dream on-chain.

First, let's take YBS out of the stablecoin market. Currently, stablecoins have three branches:

• The first is for institutional use, primarily a clearing network for cross-border, cross-industry, and cross-entity purposes, aimed at supplementing or replacing existing products like Visa and SWIFT, such as JD.com or JP Morgan;

• The second is USDT-like products promoted by TradiFi, which can be divided into dollar-pegged and non-dollar stablecoins, as well as alternative attempts by large financial institutions, such as USD1;

• The third is competitors of Ethena, such as Resolv, which is also the main subject of this article.

The market always has a kind of 'impulse', rising vigorously when it can and continuing to explore the bottom when it is expected to fall, known as momentum. YBS aptly fits this, as many projects will compete with Ethena, pulling APY to the highest, then the market clears, leaving the king of this track, with hedging ultimately becoming indistinguishable from arbitrage.

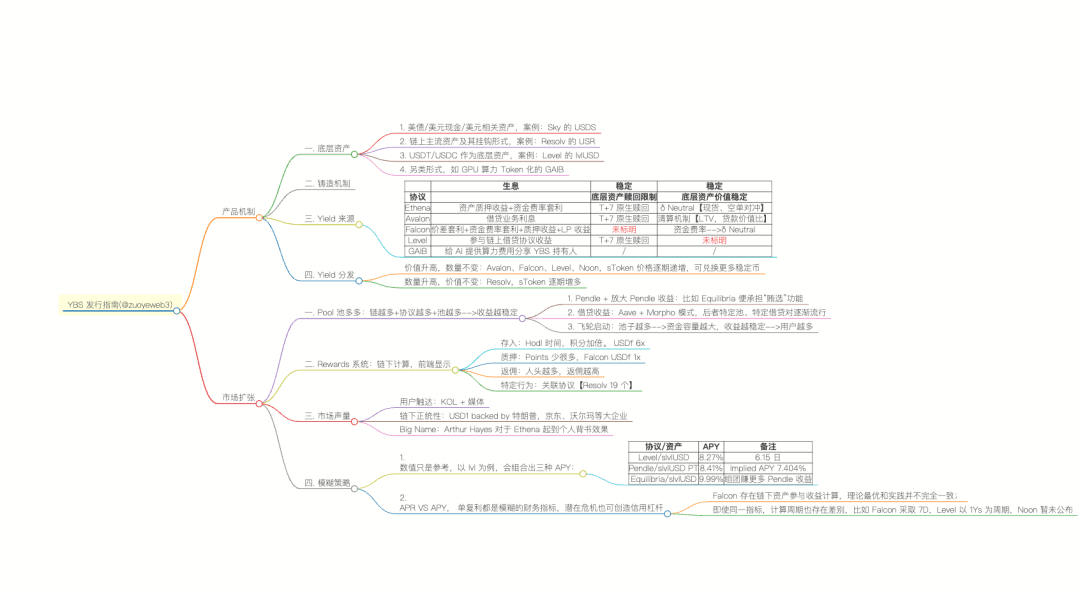

Image description: YBS Issuance Guide

Still the familiar formula. After analyzing over 100 YBS projects frame by frame, we extracted the issuance guide for income-generating stablecoin projects and roughly divided them into product mechanism and market expansion. Among them, the product mechanism consists of four parts: underlying assets, minting mechanism, yield sources, and distribution. This is the common formula for YBS project parties, with only the proportions and webpage packaging differing.

The second is the market. In an era of formula convergence, the market is fundamentally a handicraft, testing the aesthetic of project parties. This can only roughly outline the strategies of Pool Duo Duo, Rewards design, market volume, and blurred strategies.

Let’s start with the product. After Delta Neutral, it is merely a magical modification of Ethena.

Products lack distinctive features, with large distributions in U.S. Treasuries.

Income-generating stablecoins differ from USDT's 'historical stability'. Year after year of FUD instead fosters resilience. YBS requires a strong asset reserve; the cycle of credit leverage models is hard to start cold. A brief explanation is needed.

In the early stablecoin market, project parties could issue a 1 dollar stablecoin by 'claiming' to possess an equivalent asset of 1 dollar, then stake it, circulate it off-chain, and infinitely cycle.

After the collapse of UST and FTX, the difficulty of operations like the above has increased significantly. Although there are still disconnections on-chain and off-chain, in the context of increasingly mature real-name entrepreneurship and regulation, it can be assumed that most YBS project parties have relatively sufficient reserves.

The YBS project parties prefer to use the credit leverage model of banks, that is, the reserve system to deal with regulation, insufficient liquidity to handle withdrawals, and the rest is used for lending and generating income. This is the fundamental reason why dollar/U.S. Treasury has become the mainstream choice for YBS. Only dollar/U.S. Treasury can flow seamlessly in Web2 and Web3, maximizing profit from the income combination.

The GENIUS Act is not the beginning of regulation, but a summary of past practices.

I. Underlying Assets

In terms of underlying asset selection, the dollar/U.S. Treasury is the mainstream choice. However, directly adopting the fundraising model of MakerDAO/Sky to purchase U.S. Treasuries seems a bit crude. The market space left here is to help Web3’s YBS project parties buy real assets and assist Web2 financial giants in issuing compliant YBS.

For example, the new work SuperState by the founder of Compound helps DeFi's older capital manage finances. One of its important business lines is USTB, compliant U.S. Treasury tokenization, with Resolv being its client.

For instance, since Ondo brought in Kaite Wheeler, who previously worked at BlackRock and Circle, their relationship with Wall Street has become closer, and Wheeler was responsible for fixed-income products for institutional clients at BlackRock. In Ondo, his title is also in charge of institutional cooperation.

If we sort out the representation using dollar/U.S. Treasury, it can be divided into the following four types:

• U.S. Treasuries/dollar cash/dollar-related assets, case: Sky's USDS

• Mainstream on-chain assets and their pegged forms, case: Resolv's USR

• USDT/USDC as underlying assets, case: Level's lvlUSD

• Alternative forms, such as GPU computing power tokenization GAIB.

Among them, Resolv's BTC/ETH reserves represent an imagined state. Currently, they are still closely related to USDC and U.S. Treasuries, just like Ethena initially planned to use BTC but ultimately chose ETH. Compromise is the norm.

Mainstream on-chain assets, especially BTC/ETH/SOL, have seen poor progress in YBS reserve transformations. It is worth noting that Ethena's ETH hedging mechanism is for stability and does not completely align with reserves.

I believe that mainstream on-chain assets need to be more widely accepted by traditional financial markets to be directly used by YBS as reserves. We can observe from three angles: ETFs, national reserves, and (micro) strategies that on-chain stablecoins need to first gain off-chain recognition, which is quite darkly humorous.

The most interesting new forms like GAIB do not use some assets as reserves, but rather some 'utility'. The essence of currency is a general equivalent, and the computing power in the AI era indeed has this characteristic, hoping to achieve something.

II. Minting Mechanism

Earlier, we confused the minting and income-generating processes of YBS, but YBS's minting should refer specifically to the 'issuance of stablecoins based on underlying assets', a one-way process that should not involve subsequent income-generating mechanisms, redemptions, or other reverse operations.

By referencing the CDP (Collateralized Debt Position) mechanism of lending products, we incorporate all YBS within this scale, allowing for both positive and negative to accommodate non-fully collateralized YBS types.

Theoretically, unlike MakerDAO (DAI), Aave (GHO), and Curve (crvUSD), which generally adopt excess collateralization models, the new era YBS generally operates under a 1:1 full collateralization, at least in mechanism design. However, the reality of the situation remains unknown, which is also what YBSBarker hopes to penetrate.

Additionally, a few non-fully collateralized products mostly adopt credit or guarantee mechanisms, making it difficult to become mainstream choices in this cycle; therefore, they will not be introduced.

III. Yield Sources

Based on underlying assets and minting mechanisms, we consider two dimensions of yield sources: income generation mechanisms and stability, forming a complete process for the minting, income generation, and redemption of income-generating stablecoins.

Taking Ethena as an example, the Delta mechanism consists of ETH spot and short hedging, where hedging itself ensures USDe is pegged 1:1 to the dollar, while the funding cost rate arbitrage from opening short positions serves as the source of income for paying sUSDe holders.

Image description: Sources of income.

Ethena also chooses ETH with self-staking income-generating versions like stETH to enhance income capture capability. The above is the minting process for sUSDe and USDe, which also needs to consider the redemption process.

1. sUSDe reverts to USDe (unstaking) requires a 7-day cooling-off period before entering the withdrawal process, or can directly be exchanged in DEX in real-time;

2. USDe reverts to ETH, subject to T+7 restrictions. Of course, USDe itself is a stablecoin and can be directly exchanged for any asset in CEX or DEX, but this is not the official asset redemption function.

Aside from Ethena, the remaining YBS projects simply have more income scenarios and improved asset value stabilization mechanisms. A slight difference is Avalon’s liquidation mechanism, which is more akin to traditional lending products, used to control the price stability of stablecoins.

IV. Yield Distribution

There are only two types of distribution mechanisms: one where value remains unchanged while quantity increases, and another where value increases while quantity remains unchanged:

• Value increases while quantity remains unchanged: Avalon, Falcon, Level, Noon, with sToken prices increasing periodically, redeemable for more stablecoins.

• Quantity increases while value remains unchanged: Resolv, with sTokens increasing periodically, but the price of sTokens remains pegged 1:1 with their stablecoins.

Looking at the entire product mechanism design of YBS, there are two main difficulties. The first is the establishment of reserves. Other DeFi projects, such as DEX, under the AMM mechanism, adding liquidity is user behavior. DEX itself mainly involves technical development, product design, and market promotion, making it hard to say that self-owned funds are needed to create a successful product.

YBS is inherently a 'currency'-linked asset or equivalent form. Insufficient capital reserves cannot gain user trust. In other words, people prefer to use YBS issued by wealthy individuals. In this regard, YBS will naturally exclude ordinary entrepreneurs but is particularly suitable for large VCs to heavily invest in cultivating Ethena’s second, Circle IPO’s second, or USDT’s second printing machine.

The second is Yield sources. Referring to the quantitative history of traditional finance, only by being ahead of peers can one earn α returns. Afterwards, it’s either about keeping the secret of the grand prize like Simmons or competing in hardware and software resources, ultimately becoming a 'law of large numbers', using capital scale to overwhelm opponents and triggering a systemic crisis, repeating until the end of the world.

Income competition, high volume and excitement.

Alright, after organizing the meeting, you have established an excellent YBS team, successfully secured huge funding from Big Name VCs after completing project naming, front-end, back-end, and smart contract AI outsourcing. Now, you need to attract big players and retail investors to deposit funds and get the yield and yield scale running.

Then a major problem arises: the yield and yield scale seem incompatible.

I. Pool Duo Duo

The most effective customer acquisition method for YBS is to provide high returns, but as the capital scale increases, the stable high return rate will decrease. From A16Z’s investment returns to BlackRock’s asset management returns, the myth of Aave creating a thousand-fold return is just a thing of the past.

YBS must find its flywheel: provide users with more income choices, or simply put, find all chains, protocols, and pools that can build income.

Around the income of YBS, three perspectives are formed.

• Coin-based: data from the issuance of stablecoins and sTokens.

• Pool-based: usage and income data of stablecoins and sTokens.

• Protocol-based: overall governance structure of stablecoins and sTokens.

The three levels of abstraction and complexity increase sequentially. The simplest perspective is that the issuance volumes, staking volumes, and holding addresses of USDe and sUSDe are coin-based, while their trading pools in Pendle and Curve are pool-based, involving USDe, sUSDe, ENA, sENA, and protocol income, distribution mechanisms, and historical data are protocol-based.

Coin-based is very intuitive, while Pool-based complexity lies in the accumulation of multi-protocol, multi-pool cross-chain.

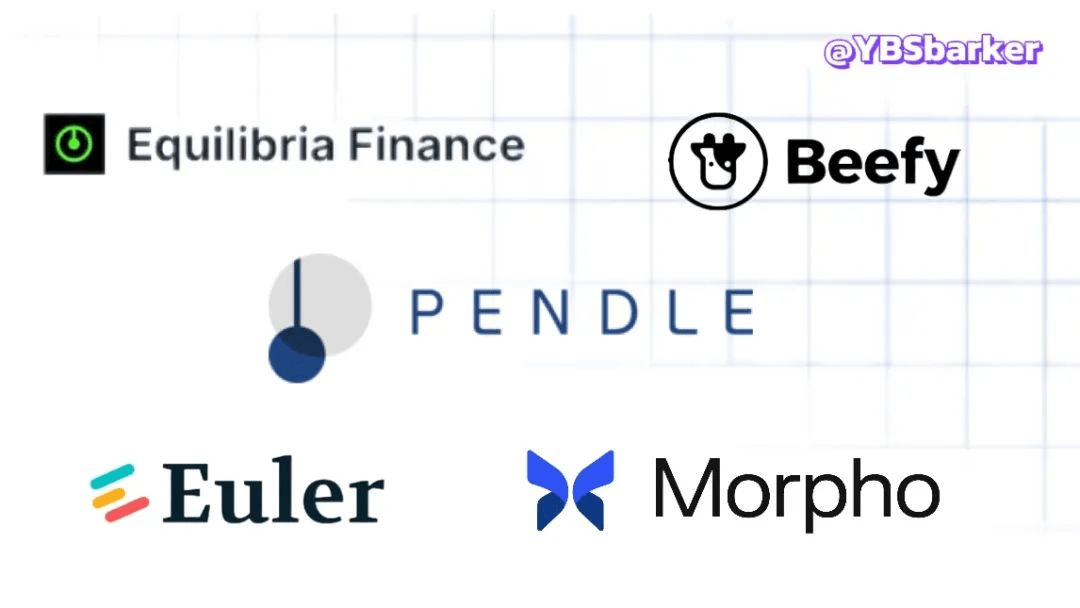

Image description: YBS related protocols

Among them, Equilibria serves as Pendle's 'bribery platform', allowing users to collectively stake ETH through Equilibria, reducing investment costs and increasing final profits.

Following this line of thought, Pool Duo Duo presents three characteristics:

• Pendle and Amplifying Pendle Returns: Pendle and Equilibria, similar to Curve and Convex;

• Aave and Morpho's lending mechanisms amplify returns, with specific pools and lending pairs in the Morpho model gradually gaining popularity;

• Replacing old with new: Pendle/Morpho/Euler is replacing the importance of older DeFi protocols like Curve and Uniswap for YBS.

Most importantly, Pendle has become the infrastructure of the YBS industry. Only by logging into Pendle can YBS take root on-chain, achieving a similar effect to USDC binding with Coinbase.

Flywheel initiation: the more pools, the greater the funding capacity, the more stable the income, the more users.

II. Rewards System

The rewards system can be summarized simply, but it is exceptionally complex in practice. How to evaluate user behavior while balancing the witch-hunt against genuine customer acquisition is a challenge. The abandonment of U card business by Onekey and Infini stems from the uncontrollable profit model for C-end users.

The rewards in the YBS field are more like a battle for points, as some users want investment returns while others aim for expected airdrops, trying to align their behavior with reality.

• Deposit: Hodl time, points doubled. USDf 6x

• Staking: Points are much less, Falcon USDf 1x

• Rebates: The more people, the higher the rebates.

• Specific actions: Associated protocols, such as Resolv 19.

However, the points system is not synonymous with airdrops and tokens. Under the usual 'off-chain calculation, front-end display' model, whether one can receive Farm rewards on time is left to fate.

III. Market Volume

The success of Ethena undoubtedly stems from its excellent design, but cannot be separated from Arthur Hayes' personal support. Drawing from past successful cases, three models can be summarized:

• User outreach: KOL + media, the effect is diminishing, closer to routine actions.

• Off-chain legitimacy: USD1 backed by Trump, major companies like JD.com and Walmart.

• Big Name: Arthur Hayes provides personal endorsement for Ethena.

Regarding market volume, I feel that my understanding is not quite on point. If any viewers have thoughts, feel free to discuss in the comments.

IV. Blurred Strategies

APR vs APY, both simple and compound interest are vague financial indicators, and potential crises can also create credit leverage.

Falcon has off-chain assets participating in yield calculations, and theoretical optimization does not fully align with practice;

Even for the same metric, the calculation periods may differ. For instance, Falcon uses a 7-day period, Level uses a 1-year period, while Noon has not yet disclosed.

Even if the calculation methods are the same, the off-chain parts of each YBS will also participate in the calculations, such as CEX opening data, or foundations, audits, etc., all of which are black boxes that cannot be tracked in real-time. There is considerable operational space in the various details in between.

The market of YBS is still a battlefield of yield data, while the specific strategies used require users' proactive exploration to amplify yield and participate in this gold rush.

Conclusion

The less demand, the closer to divine.

The surface of YBS is incredibly simple; a 1:1 peg to the dollar brings lasting security, but the complexity behind it is immense.

Aimed at the public, involving savings and lending has always been a social and political event, both East and West alike. Based on this, we delve into the inside of YBS to describe the fundamental attributes of a healthy project party. Starting a business is tough; how many of the 100 YBS projects can survive?