Vanar is trying to onboard people who do not want to become crypto users, and it is building the rails to make that possible. VGN pushes Single Sign On as the front door, Virtua is a consumer world that can keep attention inside an experience, and Vanar’s fixed fee design aims to make costs predictable in dollar terms so someone can sponsor the activity without frightening surprises. If that combination works, it can bring scale. It can also make VANRY easy to avoid, because the best mainstream UX usually removes the token from the user’s decisions, and sometimes from the actual flow of value.

VGN is the part that tells you what Vanar really wants. A walletless login is not a convenience feature, it is a statement about who the customer is. The studio is the customer. The player is the passenger. That flips the usual token story. The moment the studio pays for transactions, the user stops acquiring VANRY for utility, and the demand moves upstream into a small set of operators who can buy, batch, hedge, and optimize. If only a few entities end up doing that at scale, VANRY can become an operational inventory held by gatekeepers, not a broadly demanded asset across the user base.

The other clue is how comfortably the VGN narrative leaves room for off chain assets and adjacent economies that still feel like Web2. That design choice raises adoption odds, but it also creates an escape hatch. The economic loop can live inside in app credits, points, and internal ledgers that settle on chain only when it is convenient. This is where distribution and value capture start to separate. You can onboard millions and still have thin token throughput if the moments people care about, earning, spending, trading, are mostly accounted for off chain and only occasionally reconciled on Vanar.

Virtua intensifies that tension because it is already a complete consumer surface with its own gravity. When a metaverse experience and a marketplace sit side by side, it becomes easy for the daily loop to happen in one place and the settlement loop to happen in another. If the metaverse loop is where engagement lives, and the marketplace is where ownership changes are finalized, then VANRY’s relevance depends on how often those worlds actually touch in a way that forces on chain settlement. If most activity stays inside experience-level balances and only the final edge cases settle on chain, the chain can be present without being economically central.

Vanar’s fixed fees are not a cosmetic promise, they are the backbone that makes sponsorship workable. The tiers priced in USD terms are an attempt to turn transaction costs into something closer to a predictable bill. But the more interesting part is the mechanism that keeps the USD pricing stable. It relies on a token price process that is updated frequently so the protocol can translate dollar priced actions into VANRY amounts. That arrangement is basically an economic contract offered to studios and brands. It also introduces a trust surface, because a predictable fee regime requires a credible, resilient price feed and disciplined governance around updates.

Once you see that, a common assumption breaks. If fees are anchored to USD, the simple idea that more usage automatically means more token demand stops being reliable. When VANRY price rises, each fixed fee consumes fewer tokens. When VANRY price falls, each fixed fee consumes more tokens. The system is designed to keep the experience stable in fiat terms, not to maximize token consumption per action. That is the point for mainstream onboarding, and it is exactly why a retail thesis like “players will buy VANRY to play” weakens the moment walletless onboarding and sponsored gas become the default.

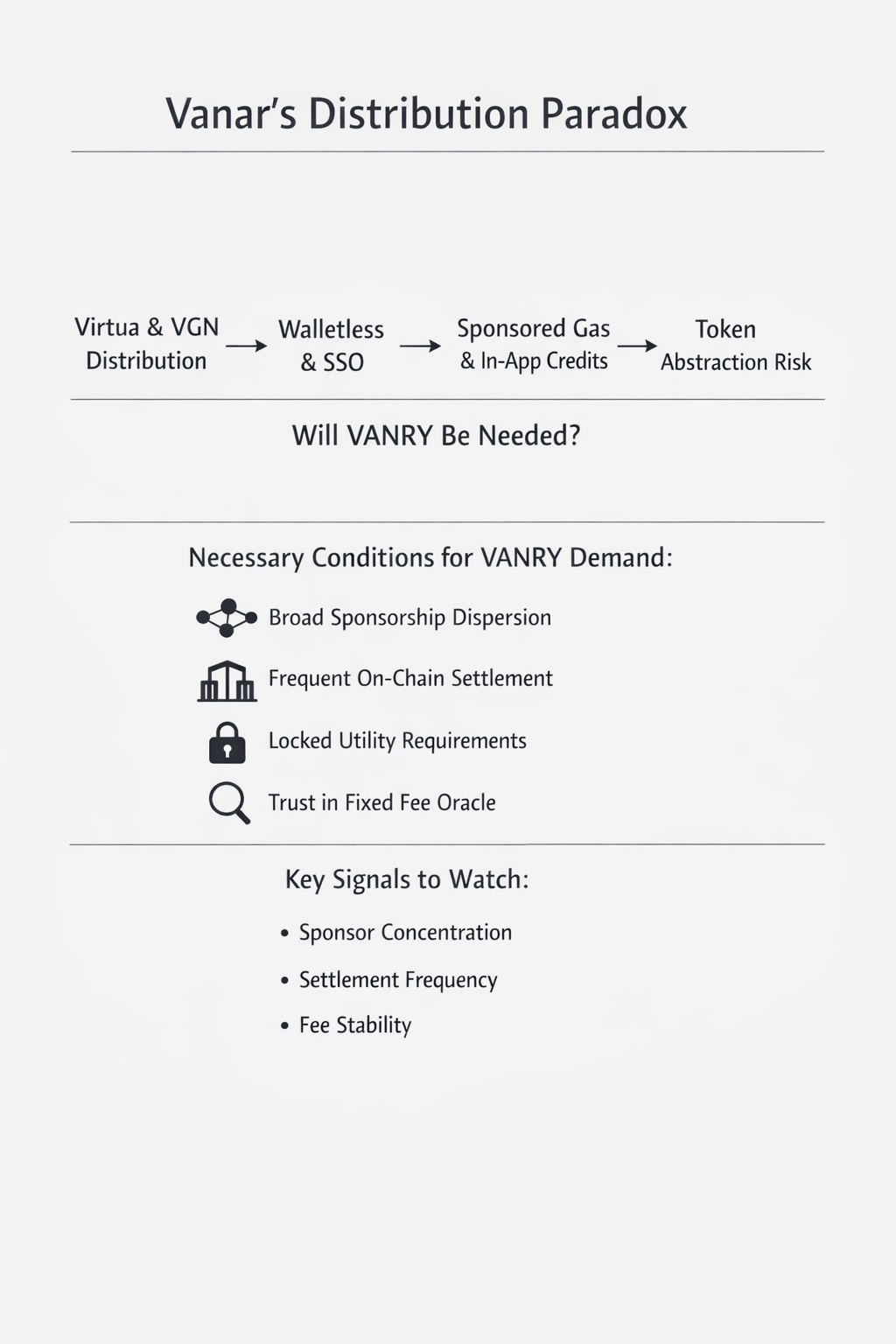

So the real question becomes simpler and harsher. Under what conditions does VANRY remain unavoidable even when the user never touches it.

The first condition is dispersion. Many separate operators need to keep buying and holding VANRY as working inventory, not a single super intermediary that does it for everyone. If one payments layer can take fiat from every studio, manage custody, sponsor transactions, and net flows internally, then VANRY demand becomes concentrated and strategic. That concentration can reduce the steady marginal buying pressure people assume comes from growth, because the intermediary can time purchases, warehouse inventory, and smooth volatility in ways a broad user base never could.

The second condition is settlement density inside Virtua and VGN. It is not enough for the chain to exist behind the scenes. The high value actions have to be actions that naturally settle on Vanar with meaningful frequency. If the default pattern becomes “earn and spend in credits, settle occasionally,” then the most valuable parts of the economy are insulated from the token. This is where design decisions that feel user friendly can quietly drain token relevance. If the chain is only the archive, the archive does not create demand, it only records outcomes.

The third condition is that VANRY has to be more than a pass-through. Gas spending alone can look like a temporary flow that reaches validators and then returns to the market. If Vanar wants persistent demand, some core services that power Virtua and VGN need to require an ongoing VANRY balance, or a lock, or a holding-based entitlement that cannot be replicated with internal credits. The hint that matters is the existence of holding-based access logic in Vanar’s brand and marketplace narrative. That is the kind of mechanism that turns the token into the cost of running distribution, not the optional currency of users.

The fourth condition is credibility for the kind of operators Vanar is courting. The consensus and validator onboarding approach is structured to favor known entities early and to keep stability high. That stability is not a philosophical statement, it is a practical one. Sponsored transactions and consumer-grade experiences do not tolerate chaotic fee spikes, unpredictable finality, or governance drama. But stability comes with trade-offs. If the governance model makes large partners feel safe while crypto natives complain about control, the token’s value capture has to come from operational necessity, not from broad permissionless speculation. That is fine, but it changes what “success” looks like for VANRY.

My personal read is that Vanar is implicitly shaping VANRY into a wholesale input for consumer scale funnels, more like prepaid operational credits that studios and platforms keep on hand because their user experience depends on it. That model can work, and it fits the way Virtua and VGN are positioned. The danger is that the better Vanar gets at hiding complexity, the easier it becomes for complexity to be hidden in the wrong place, inside consolidated treasuries, inside off chain ledgers, inside credit systems that only settle when they feel like it.

If Vanar delivers mainstream adoption through Virtua and VGN, the market will celebrate the top line numbers first. The deeper signal will be whether VANRY remains structurally necessary in the plumbing. Watch whether sponsorship stays fragmented or consolidates. Watch whether the most meaningful economic actions settle on chain as a habit or as an exception. Watch whether fixed fees stay predictable without becoming a point of distrust. Vanar’s strongest distribution path is also its sharpest economic test. The project does not need users to care about VANRY. It needs the system to make VANRY impossible to ignore.