Many times when observing a currency crisis in a particular country, I automatically map it into the model of the cryptocurrency circle; the underlying logic, capital flow, and game structure are almost identical. We first need to establish a basic correspondence, which is critical!

The so-called ultimate value storage is all limited, all decentralized, and all serves as a hedging asset when fiat currency systems collapse. We see that whenever there is a geopolitical crisis, gold prices rise, and Bitcoin follows suit. Whenever a country's currency has issues, the wealthy's first reaction is to either exchange for gold or buy Bitcoin. Why? Because these two assets are not controlled by any single country, that is their core value. Of course, Bitcoin's volatility is greater because it is still a relatively young market with insufficient depth, but in terms of functional positioning, they are essentially the same.

The US dollar is equivalent to stablecoins represented by USDT; the dollar in the traditional currency system is exactly like USDT in the cryptocurrency circle, being the primary trading medium and the unit of valuation for other assets. Everyone uses it for hedging and as a transit medium. What are the most active trading pairs in any foreign exchange market? They are all some currency against the dollar—euro against the dollar, yen against the dollar, RMB against the dollar. Similarly, in the cryptocurrency circle, the most active trading pairs are all some coin against USDT.$BTC Against USDT,$ETH Against USDT,$BNB Against USDT.

Moreover, have you noticed that USDT is actually pegged to the US dollar? It claims to be 1:1 anchored to the dollar, backed by dollar reserves. However, it is unclear whether it actually has sufficient reserves. In any case, people still tend to believe in it. Isn't this similar to the US dollar during the Bretton Woods system? Back then, the dollar also claimed to be linked to gold, stating that $35 could be exchanged for one ounce of gold. In 1971, Nixon announced the decoupling directly. Why? Because of the dollar's growth, the gold reserves were insufficient. But what does it matter? People continued to use the dollar because there was no better option. The logic behind USDT is the same; although everyone knows that Tether is quite suspicious and that its reserves might not be transparent, do you have a better choice in the cryptocurrency circle? Even if there are other stablecoins, their scale, consensus, and liquidity are far from that of USDT.

The currencies of various countries equal various project tokens, and this stratification is even more interesting. Major currencies like the euro, yen, and pound are like Ethereum, BNB, and SOL, which are large public chain tokens with actual ecosystems, real users, and large numbers of developers, with value supported by fundamentals, although they also fluctuate, they are not likely to suddenly go to zero. In contrast, emerging market currencies like the Turkish lira, Brazilian real, and South African rand are like small to medium project tokens with market caps in the billions or tens of billions, having decent fundamentals, but they are highly volatile and are often severely impacted by market sentiment.

As for Zimbabwean currency and Venezuelan currency, those are typical RUG tokens, where the project party directly flees, the token price goes to zero, and the money in people's hands turns into waste paper. For instance, Zimbabwe's inflation rate reached tens of millions in 2008, ultimately issuing a bill with a face value of 100 trillion, and then the entire currency system collapsed. Isn't this a typical death spiral resulting from the project party issuing unlimited tokens? It's exactly the same logic as the LUNA crash a few years ago.

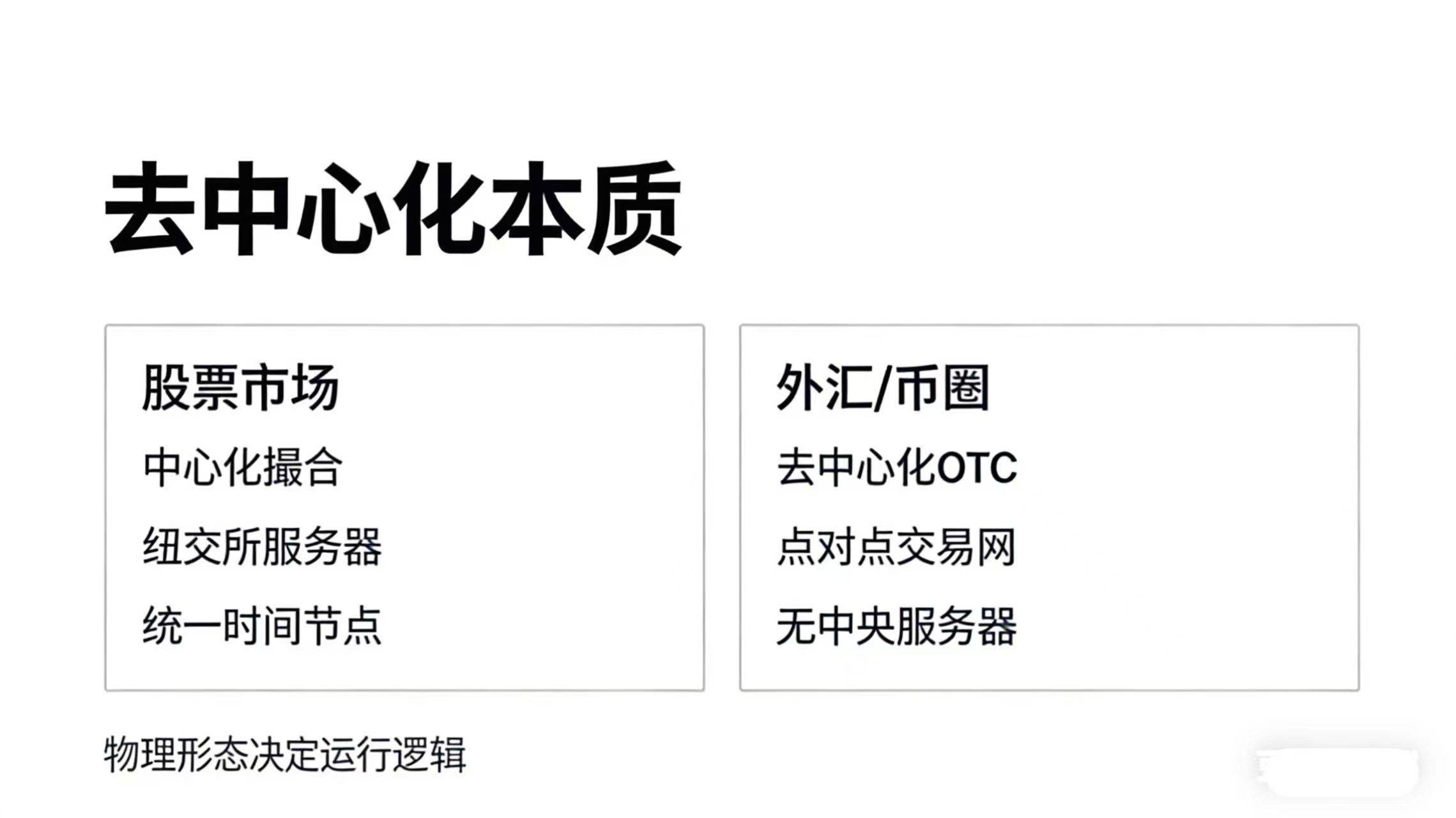

Another point is that the foreign exchange market, like the cryptocurrency circle, is actually a decentralized market. Many people may have thought that the foreign exchange market is like the stock market, with some New York Foreign Exchange Exchange or London Foreign Exchange Exchange. Stock markets have the Shanghai Stock Exchange, Shenzhen Stock Exchange, Nasdaq, and New York Stock Exchange, all of which have physical entities, a central server, and an absolute center, opening and closing at set times. All stock orders ultimately get aggregated into that central server for transaction matching.

However, the foreign exchange market is actually decentralized, and this is similar to the cryptocurrency circle. No exchange can monopolize trading in the cryptocurrency circle, and similarly, no exchange can dominate foreign exchange trading. There may be many exchanges, large OTCs, and C2C merchants trading Bitcoin; the foreign exchange market operates similarly, with thousands of exchanges, banks, investment banks, and brokers globally continuously quoting and transacting with each other.

It is precisely because the foreign exchange market is decentralized that it trades 24/7 like the cryptocurrency circle.

After establishing this framework, we can start to delve into each participant in the market, see what they are playing with, how they are playing, and what the underlying logic is.

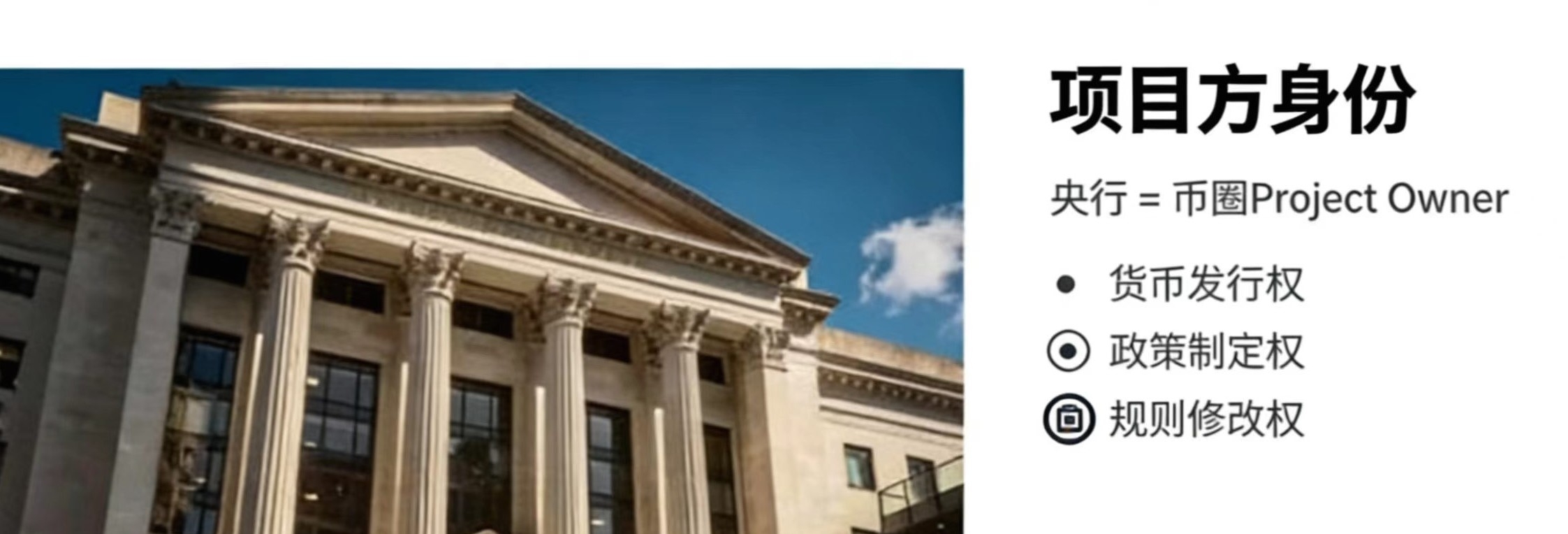

Let's first talk about the governments and central banks that issue currencies; they are the most core players in the entire market. In the foreign exchange market, the roles of governments and central banks are essentially the same as those of project parties in the cryptocurrency circle. Think about it, what can project parties do? They can issue more tokens, buy back tokens, set release rules for tokens, adjust staking yield rates, and decide whether to destroy tokens. Central banks can also print money, absorb liquidity, adjust interest rates, set reserve ratios, and buy and sell foreign exchange reserves. Isn't this the same thing?

But here, there is a very key distinction that needs to be clarified. Many times, project parties in the cryptocurrency circle can do as they please; they can issue more tokens, dump the market, or flee without much consequence because there is basically no regulation and no historical burdens. If they fail, they can just change their name and launch a new project. But traditional central banks at least must maintain appearances, consider their credibility, and think about long-term effects. A country's currency does not just collapse; it is backed by the credit of the entire country and the lives of tens of millions or even hundreds of millions of people. Therefore, central banks are more cautious when making decisions. But note this 'but'; essentially, their power structures are the same—they are both issuers and regulators of currency, both wielding the ultimate weapon of printing money. So when they are truly pushed to the limit or when they genuinely want to achieve a certain goal, they will resort to any means necessary.

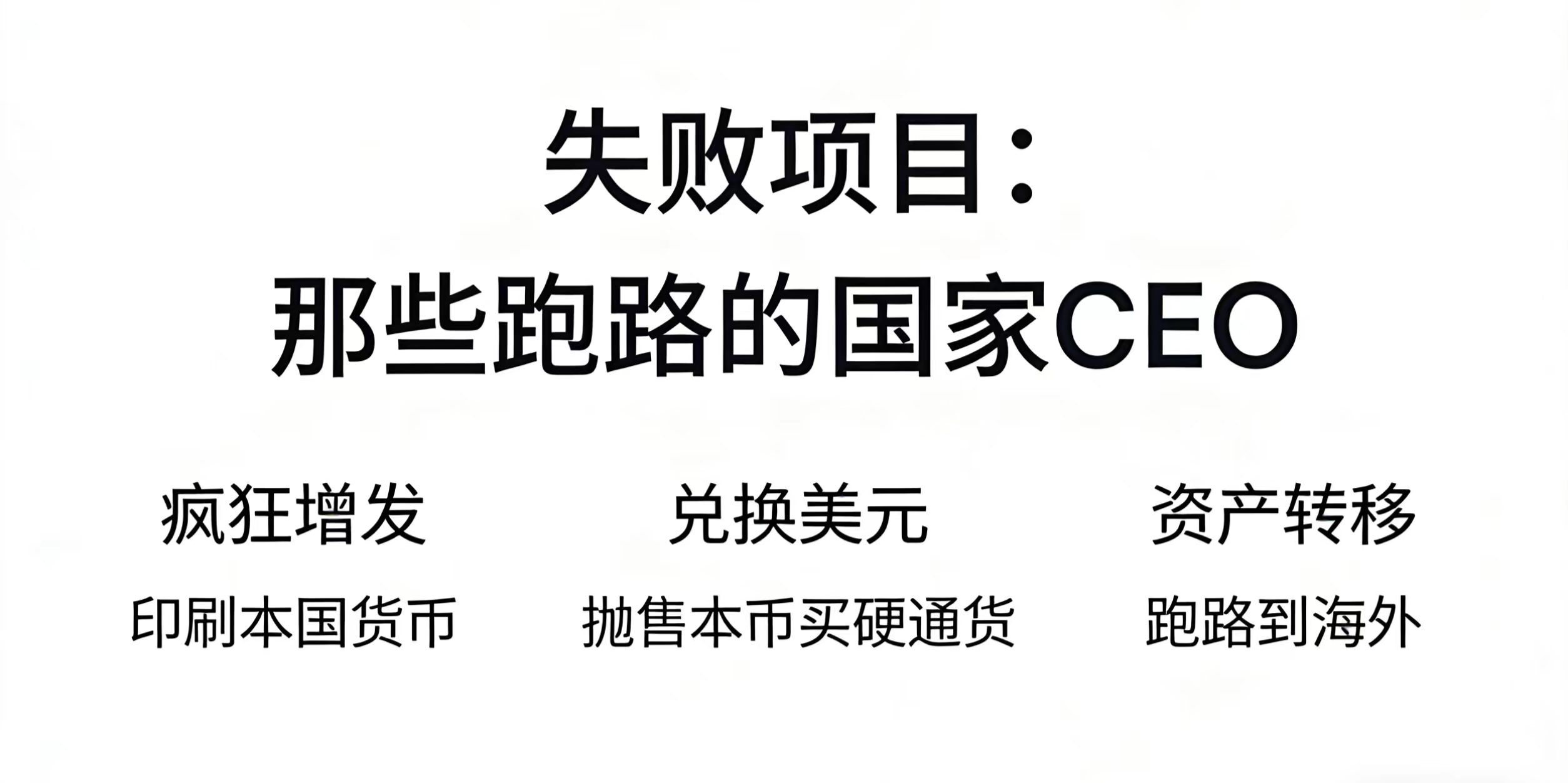

Let’s give a few specific examples. First, Turkey: Erdogan has been a textbook example of a failed project party in recent years. He refuses to raise interest rates, insisting on maintaining low rates, claiming that interest is the root of all evil. What happened? The lira has plummeted, from 8 lira to 1 dollar in 2021, to now over 40 lira to 1 dollar, a decline of nearly 80% in four years. This is a typical case of a project party messing up their ecosystem.

Capital outflows have been curbed, the fiat currency exchange rate has stabilized, and foreign exchange reserves are no longer rapidly declining, but this comes at a cost. Both foreign and domestic confidence has definitely been affected. This has its counterpart in the cryptocurrency circle. Look at those exchanges that impose withdrawal restrictions; in the short term, they can indeed prevent bank runs and price collapses, but in the long run, users will gradually drift away because they no longer trust you, thinking that you might not allow withdrawals at any time. So why should I keep my money with you?

Before FTX collapsed, they first suspended withdrawals, and then everyone knew something was wrong, and then it really happened. Why is Binance the largest exchange in the cryptocurrency circle today? Many whales even dare to keep hundreds of millions of funds in Binance for the long term because it has never imposed widespread, systemic withdrawal restrictions. Foreign exchange controls essentially prevent you from fleeing, locking you in the system; they are effective in the short term, but in the long run, they damage trust and openness. Now let’s talk about market makers; these people are the invisible kings in the foreign exchange market, the true masters of the market. Look at the statistics: the top ten market makers, including JPMorgan, Citibank, Deutsche Bank, Goldman Sachs, UBS, and Barclays, account for over a third of the global foreign exchange trading volume, with daily trading exceeding $2.5 trillion; they are the so-called dealers of the foreign exchange market.

In the cryptocurrency circle, this role is even more obvious and more blatant. Almost every project party of some scale has market makers behind them: Wintermute, Jump Trading, DWF Labs, GSR, Cumberland—all names you would have heard if you are in the cryptocurrency circle. What they do is essentially no different from traditional financial market makers: providing liquidity, taking the bid-ask spread, helping project parties control the market, and sometimes even pulling some tricks.

However, the market makers in the cryptocurrency circle have several significant differences from those in traditional finance.

The first difference is transparency. Although traditional financial market makers have many tricks, at least on the surface, they are relatively regulated, with compliance departments supervising and regulatory agencies monitoring. In the cryptocurrency circle, market makers operate in a black box, and outsiders have no idea what they are doing behind the scenes. In 2014, there was a foreign exchange manipulation case in the foreign exchange circle with a total fine of over $10 billion, where traders referred to themselves in groups as the mafia and bandit club, joining forces to manipulate foreign exchange prices. Such incidents are far too common in the cryptocurrency circle, and it's even more extreme here because regulation is basically zero, allowing these market makers to play many more tricks than in traditional financial markets.

Moreover, let me tell you a secret: the relationship between many market makers in the cryptocurrency circle and project parties, as well as between exchanges, is much deeper than you might imagine. They not only provide liquidity but often are part of the project, or even the project party itself. Imagine a new project wants to issue coins; they find a market maker and say, 'I'll give you some tokens; you help me maintain the coin price stability.' This sounds very normal, right? But in practice, this 'maintaining coin price stability' can be understood in various ways: it can genuinely provide two-sided quotes to make trading more efficient; or it could mean dumping or pumping at critical moments to create the desired price trend. Even worse, some market makers might demand the project party give them very favorable token prices, even free tokens, and then sell them on the market. Isn't that just a disguised way of cashing out in advance? Why would the project party agree? Because they need liquidity and someone to help maintain their coin price at a reasonable level. Moreover, many times market makers will also provide other services for the project party, such as helping them get listed on exchanges and doing market promotion, forming a very complex web of interests.

The second difference is the technological means. Although traditional foreign exchange market makers also use algorithmic trading and high-frequency trading, they are still relatively conventional in comparison. The technological means used by market makers in the cryptocurrency circle are far more advanced and more aggressive. Before FTX collapsed, Alameda Research was one of the largest market makers. How did they play? They provided market-making services to project parties while trading on insider information and could even use customer funds for risk-taking—something that would be unthinkable in traditional foreign exchange markets, but is the norm in the cryptocurrency circle.

Real multinational enterprises with physical businesses in the foreign exchange market are actually the most legitimate participants. They have real cross-border business needs and require hedging against exchange rate risks. Companies like Apple, Microsoft, and Tesla have huge foreign exchange exposures every day, and they must constantly engage in forward contracts and swaps to lock in exchange rate risks.

In the cryptocurrency circle, this corresponds to those projects that are genuinely using blockchain technology, such as those with users, revenue, and cash flow. For example, if you are a blockchain gaming project, your players are on various chains, some paying with ETH, some with BNB, and some with SOL, but you need to pay salaries to the team, pay for servers, and settle with partners, which may all require USD. Thus, you have to do coin-to-coin exchanges and fiat-to-coin exchanges, considering the risk of price fluctuations. Therefore, the foreign exchange risk that a cryptocurrency company has to manage is actually more complex than that of a traditional company, as it needs to handle not only the exchange rate risk between fiat currencies but also the exchange rate risk between cryptocurrencies and the exchange rate risk between fiat and cryptocurrencies. So what can be done? Traditional companies would find investment banks to hedge, sign forward contracts, and swap agreements to lock in future exchange rates. Cryptocurrency companies can do the same, but the problem is that traditional investment banks may not be willing to accept cryptocurrency-related businesses, and even if they do, the quotes can be very expensive.

Moreover, many companies actually have not done well in foreign exchange risk management, especially those that are growing rapidly. They may be doing very well in business, with great technology and products, and fast user growth, but because they have not managed foreign exchange risk well, they end up losing a significant amount in exchange rate fluctuations, even affecting the operation of the entire company. For example, if you are a company primarily settling in ETH. You collected a lot of ETH during a bull market when the ETH price might be $4,000, and you plan to use this ETH to cover your expenses for the next year. However, when the bear market comes, ETH drops to $1,000, and your actual purchasing power shrinks by 75%. If you did not hedge in advance, you would have to swallow that loss, which is the same as what traditional companies experience in the foreign exchange market.

For example, in 2022, the significant appreciation of the US dollar caused many multinational companies to suffer huge foreign exchange losses. Apple lost $1.5 billion in foreign exchange that year, and Google lost $1.8 billion. Of course, they hedged and made back some money in derivatives, but this also shows that foreign exchange risk is very real for businesses. In the cryptocurrency circle, this impact is much more intense, so the effect on businesses is very direct.

Another participant in the foreign exchange market is capital. The businesses we talked about earlier are mainly foreign trade and the commodity market, but the foreign exchange flow within the capital market may be much larger than that of the commodity market. For instance, when an American investor wants to invest in establishing a factory in China, they need to first convert their US dollars into RMB; when a European fund wants to invest in Japanese real estate, they must convert euros into yen. The scale of foreign exchange demand brought about by cross-border investment is astonishing.

Moreover, unlike trade, the demand for foreign exchange in trade is relatively stable, as imports and exports are continuous and planned, but capital flows can be extremely rapid and massive, with hundreds of billions of dollars potentially pouring into or out of a country overnight. Such large-scale capital movements can directly impact the foreign exchange market, leading to sharp fluctuations in exchange rates.

In the cryptocurrency circle, this logic is even more direct and brutal. During the ICO frenzy of 2017, almost all global blockchain projects financed using ETH, regardless of whether they were Chinese, American, or European teams—investors directly sent ETH to you. Why use ETH? Because at that time, ETH was like the international reserve currency of the entire crypto world; everyone recognized it, it had good liquidity, and easy transfers.

But here comes the problem: what do these project parties do after obtaining a large amount of ETH? Their daily expenses are in fiat, needing to pay salaries to the team, rent offices, and do market promotions, all of which require USD, RMB, or euros, so they have to convert ETH into fiat. During the bull market in 2017, this wasn't a big issue; ETH rose from $10 at the beginning of the year to $1,400. Project parties holding ETH were practically winning without effort. Many projects might have raised 10,000 ETH, at the peak price translating to $14 million, and the team felt financially secure, thinking they could spend slowly.

However, when the bear market came in 2018, ETH fell from its peak of $1,400 all the way down to over $80, a decline of more than 90%. Those project parties that did not convert ETH to fiat in time were left dumbfounded. Imagine a project that originally had $14 million on its account, but now only has $800,000 left. Team salaries need to be paid, office rents need to be settled, but there isn't enough money, and many projects died this way. It wasn't that the technology was lacking or the products were poor; it was simply due to poor foreign exchange risk management that they were directly dragged down by the crash of ETH. This is exactly the same as the foreign exchange risk in traditional capital markets.

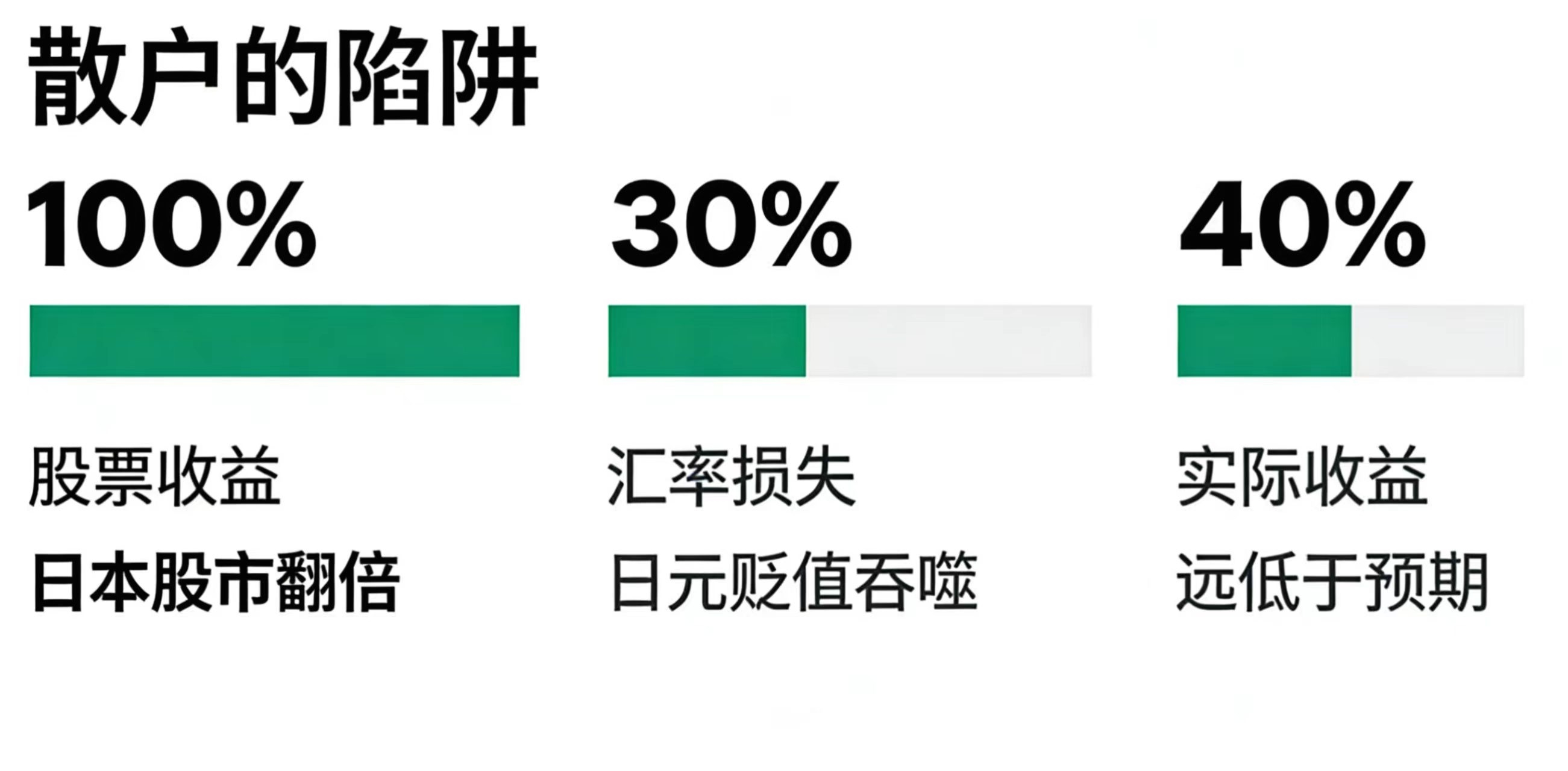

Let's take a real example; Warren Buffett's investment in Japan's five major trading companies illustrates the issue well. In 2020, Buffett announced his investment in Japan's five major trading companies, and by 2023, the increase in these stocks was quite good, with an average increase of doubling. It sounds very profitable, right? But there is a huge problem—foreign exchange risk. Suppose an American investor in 2020 followed Buffett and exchanged dollars for yen to buy these Japanese stocks. At that time, the exchange rate was about 106 yen to 1 dollar, meaning 1 dollar could be exchanged for 106 yen. By 2023, the dollar-yen exchange rate had appreciated to about 150, meaning the yen depreciated by about 30% against the dollar.

Now let’s calculate: your invested Japanese stocks doubled, which looks very good, but when you exchange these yen assets back into dollars, the yen has depreciated by 30%. So what is your actual gain? Suppose you initially invested $1 million and exchanged it for 106 million yen. After the stocks doubled, your yen assets became 212 million yen. But now to exchange back to dollars, at the rate of 150, you can only exchange for about $1.4 million, representing a three-year return of 40%, with most of the gains eaten away by exchange rate risk.

This is why Buffett does not directly exchange dollars for yen to invest; he finances through issuing yen-denominated bonds, effectively borrowing yen to buy Japanese stocks. This operation is truly ingenious: as the yen depreciates, his debt also shrinks, effectively hedging the exchange rate risk.

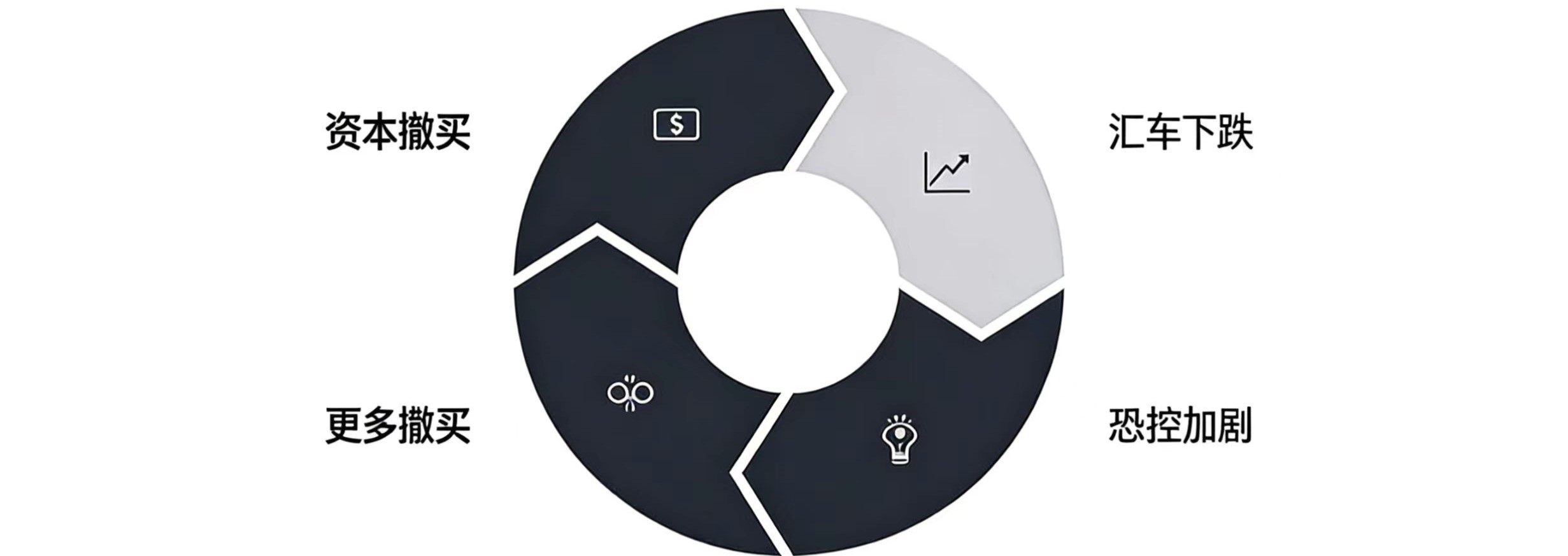

When currency demand declines, exchange rates begin to fall. A decline in exchange rates can trigger more panic selling, as investors worry about further declines and want to exit quickly, creating a death spiral. The Asian financial crisis in 1997 occurred this way, with the Thai baht, Korean won, and Indonesian rupiah plunging by 50% to 70% within just a few months; this was not only because the economic fundamentals of these countries were problematic but also due to the chain reaction caused by panic capital outflows.

The bursting of the ICO bubble in the cryptocurrency circle follows a similar logic. In 2017, a large influx of funds drove up the price of ETH, which attracted more people to participate in ICOs, creating a positive feedback loop. However, by 2018, when people discovered that many ICO projects had no real value and were just air projects, confidence collapsed. Project parties began to sell ETH for cash, and investors started to withdraw, leading to a plummet in ETH prices that forced more project parties to sell, creating a death spiral.

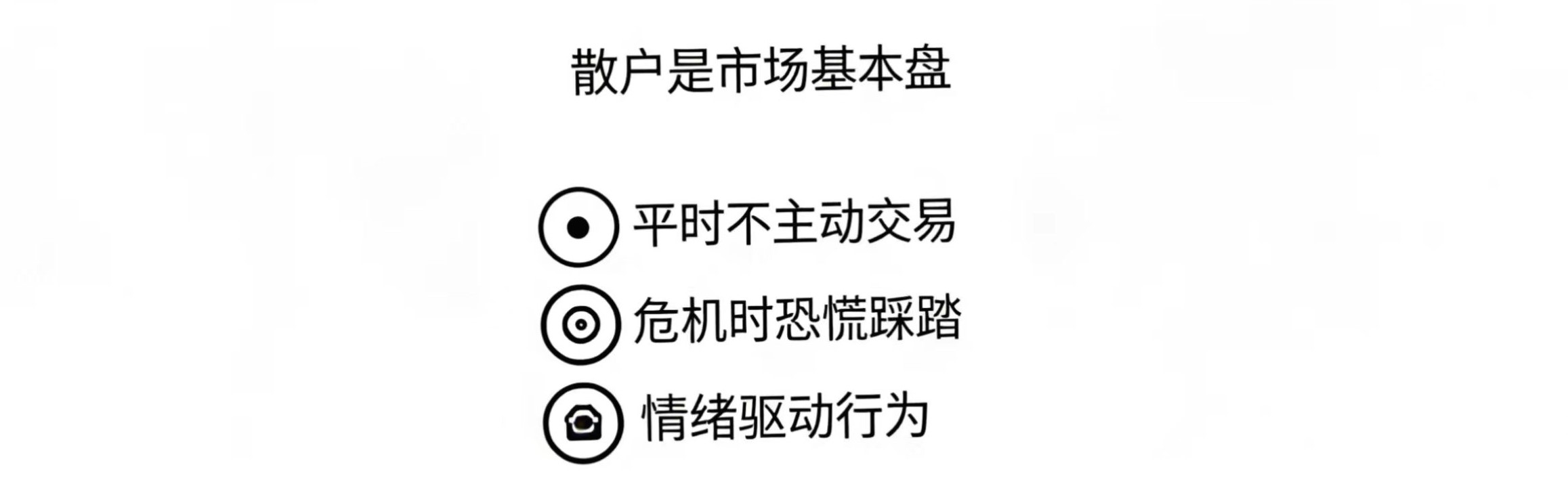

Next, let’s talk about currency holders, who represent the largest basic group of a country's currency, similar to retail investors in the stock market.

In the cryptocurrency circle, due to significant price fluctuations, retail trading is active, while the foreign exchange market fluctuates relatively less, so ordinary holders of currency generally do not trade and only use foreign exchange for travel abroad, studying abroad, or buying some overseas goods. However, during a currency crisis, they often become the dominant force in exchange rate fluctuations, after all, they are the largest holding group. One critical group among them is speculators, who exist in any market and are often the most active group. In the foreign exchange market, Soros is the most famous representative, having targeted the pound and the baht, both classic cases of foreign exchange speculation. Such people are far too many in the cryptocurrency circle, and they play even wilder.

Why do exchange rates go up or down? It's essentially the same as why some coins soar a thousand times while others go to zero. Once you see through the situation of these participants, you will understand that fluctuations are fundamentally caused by the expectations and behaviors of the participants involved. To put it bluntly, whether it's a token issued by a cryptocurrency project party or a fiat currency issued by a government, does it have intrinsic value?

No! Traditional investors often say that people in the cryptocurrency circle are speculating on air; people in the cryptocurrency circle often say that fiat currency is the real air, a government-issued promissory note. Both sides are actually correct.

Observe how the issuing project party operates and builds its ecosystem.

In the cryptocurrency circle, for a project token to have value, the project party must work hard: attract developers to settle in, establish a developer community, encourage everyone to write code and run applications on your chain; you must incubate a flourishing financing ecosystem on-chain, allowing hot money to circulate within your system; you need to unite market makers to maintain good market depth, and not let the price fluctuate wildly; finally, you must instill strong confidence in all token holders, encouraging them to use your tokens across various applications and believe they can make money in your ecosystem. Only by doing these things well can the token price sustain prosperity.

The logic in the foreign exchange market is completely the same. Why is the dollar strong? Because the ecosystem of the American project party is well-managed, with top developers globally—those largest multinational companies, the most excellent entrepreneurs, and capitalists are all there; all the hot money is seeking trading opportunities in the Wall Street ecosystem.

In contrast, those small national currencies that have collapsed often do so because the project parties are not doing their jobs; the most typical case is when project parties rampantly issue tokens to dump the market, giving their project's air tokens to their families to exchange for dollar assets.

In this episode, we will analyze what causes exchange rates to rise and fall, emphasizing the core message: understanding the cryptocurrency circle means understanding the essence of the entire foreign exchange market.