Editor's note: While the market is still accustomed to summarizing the world of stablecoins with 'total supply', a set of more granular data is revealing another layer of reality. A single supply figure can only answer 'how much', but cannot explain 'who holds it', 'how it flows', or 'why it stays'. When we observe the supply scale, concentration of holdings, on-chain circulation speed, and classification of specific activities on the same map, what we see is no longer a static stock, but a dynamic structure of how capital migrates, settles, leverages, and reprices on the chain.

This perspective is important because it may correct our intuitive judgments about the past year. The downturn in the crypto market contrasts sharply with the strong performance of US stocks, and the panic amplified by whale sell-offs and price pullbacks can easily lead one to believe that capital is fleeing the crypto world. However, the on-chain data presented in this article, as well as the signals released in recent Circle financial reports, tell a different story: capital may not have disappeared; it may just be temporarily withdrawing from high-volatility risky assets. At least the on-chain data proves that it is entering incentive-driven activities rather than trading demand.

Everyone quotes that supply number. It appears in every report, every earnings call, and every policy hearing. But aside from the 'circulating supply exceeding 300 billion USD', how much do we really know about stablecoins?

Who is holding them? How high is the concentration of holdings? How fast do they circulate, and which chains are they mainly active on? What are they actually used for—are they for DeFi liquidity, payment tools, or merely 'cash equivalents' for parked funds?

Meta just announced plans to integrate third-party stablecoin payments on its platform; the OCC (Office of the Comptroller of the Currency) approved a national trust bank license for stablecoins; Payoneer announced stablecoin functionality for 2 million businesses; Anchorage Digital launched compliant stablecoin services for non-US banks. Institutions and regulators are accelerating their entry, and the answers they need are clearly not just a supply number.

We used the latest stablecoin dataset released by Dune—developed in collaboration with Steakhouse Financial—to answer some of these questions. Here are the findings revealed by the data.

Supply Panorama

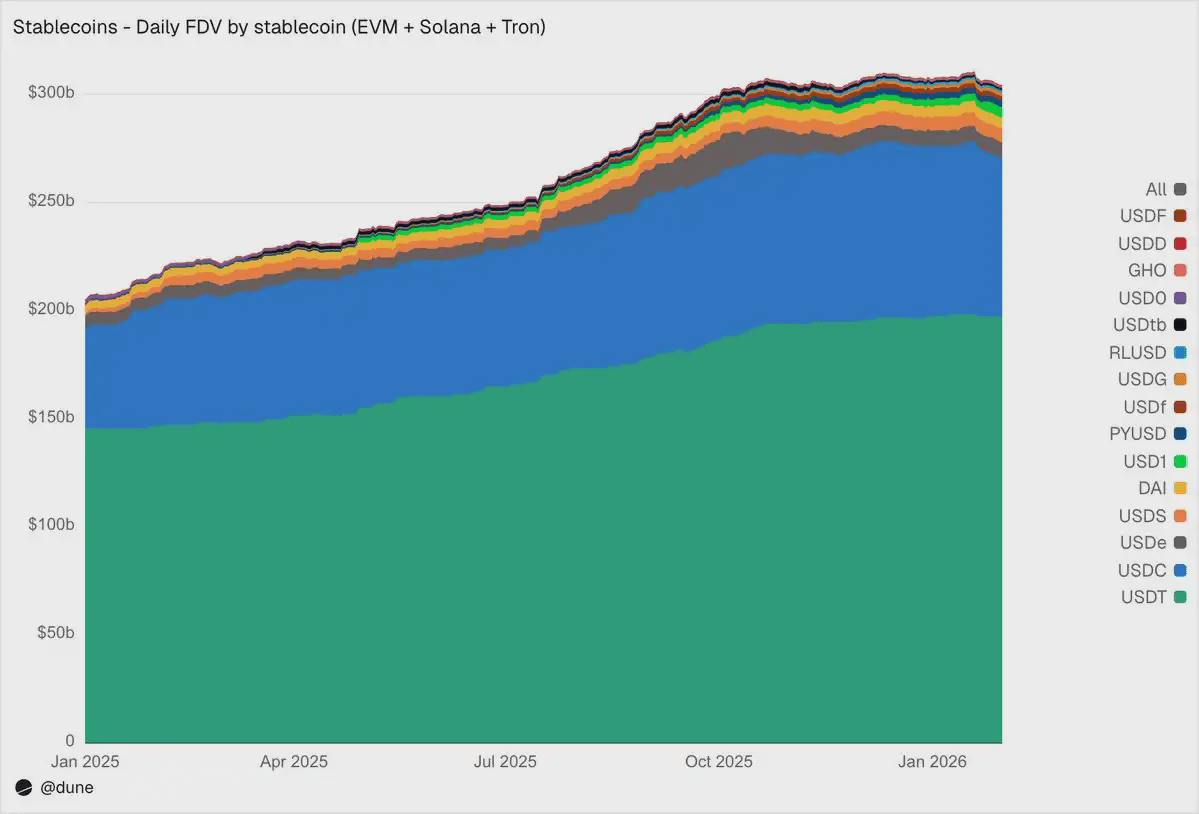

As of January 2026, the 15 largest stablecoins in the EVM, Solana, and Tron ecosystems have a fully diluted supply of 304 billion USD, a year-on-year increase of 49%. Tether's USDT (197 billion USD) and Circle's USDC (73 billion USD) still occupy 89% of the market share.

From the perspective of chain distribution, Ethereum carries 176 billion USD (58%), Tron 84 billion USD (28%), Solana 15 billion USD (5%), and BNB Chain 13 billion USD (4%). Even as the total supply nearly doubled, this on-chain distribution structure has seen little significant change over the past year.

But beneath the two largest stablecoins, 2025 will be a year for challengers to rise. USDS (Sky/MakerDAO) grew 376% to 6.3 billion USD; PYUSD (PayPal) grew 753% to 2.8 billion USD; RLUSD (Ripple) surged from 58 million USD to 1.1 billion USD, an increase of 1803%; USDG expanded 52 times; USD1 grew from zero to 5.1 billion USD.

Of course, not all challengers are heading in the same direction. USD0 dropped 66%; Ethena's USDe nearly tripled at its peak in October, ultimately rising 23% over the year. Even so, the competitive layer beneath USDT and USDC is significantly increasing in the number of competitors.

Who is holding them?

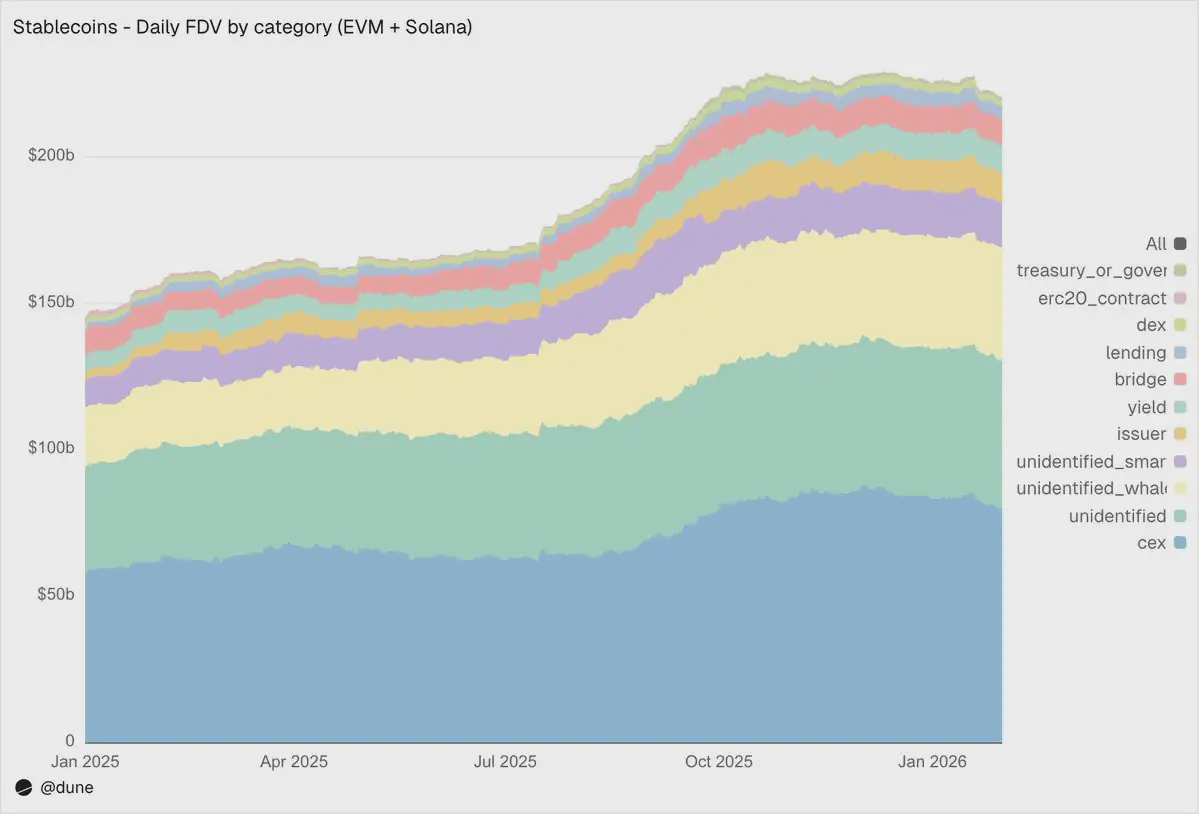

Most stablecoin datasets can only tell you the total supply. However, since our dataset tracks balances at the wallet level and incorporates address labeling, we can answer a more critical question: Who is holding these stablecoins?

In the EVM and Solana ecosystems, centralized exchanges are currently the largest recognized category, holding a scale of 80 billion USD, up from 58 billion USD a year ago. Stablecoins remain the primary infrastructure for trading and settlement.

Whale wallets hold 39 billion USD; the holdings of yield protocols have nearly doubled to 9.3 billion USD, reflecting the growth of on-chain yield strategies; issuer addresses—including treasuries and mint/burn contracts—have surged from 2.2 billion USD to 10.2 billion USD, a growth of 4.6 times, directly reflecting the scale of new supply entering the market.

Regarding label quality: only 23% of the supply is in completely unrecognized addresses. For on-chain data, this is a relatively high recognition rate—and crucial for understanding where the risks of stablecoins are actually distributed.

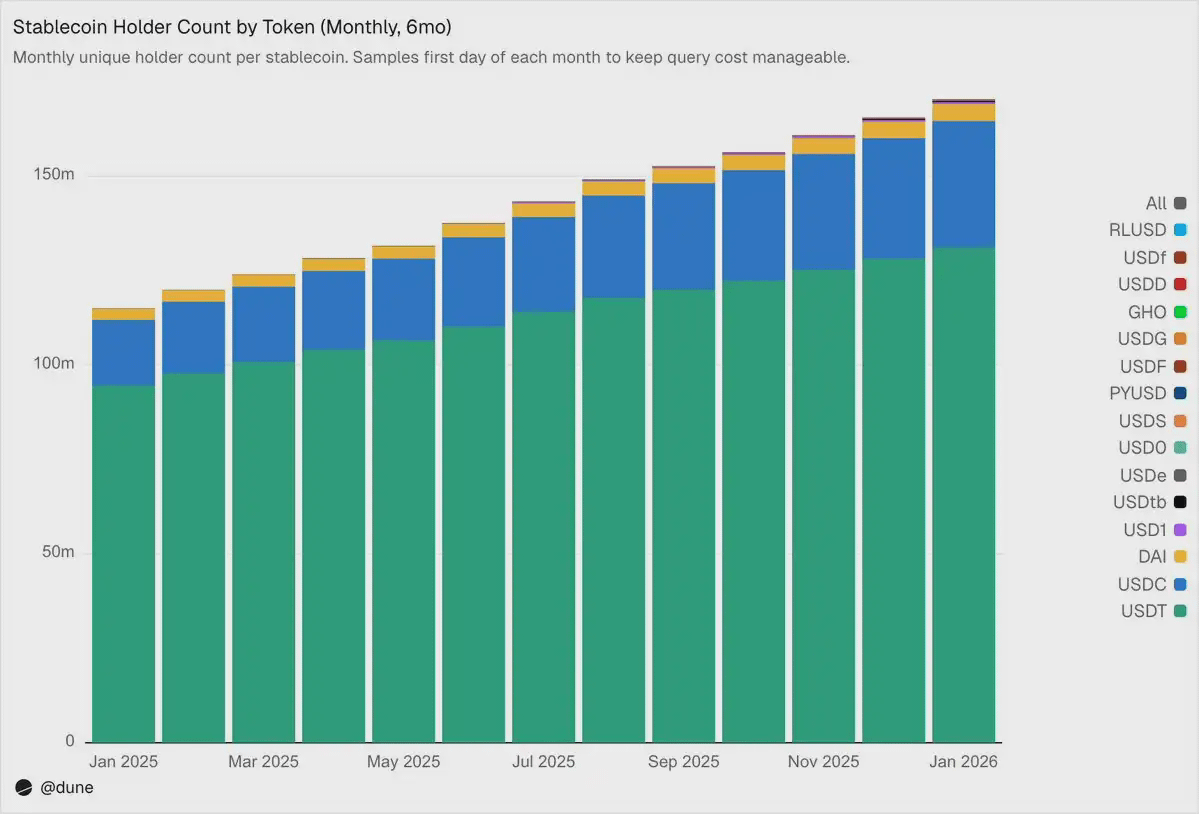

172 million holders, but with extremely high concentration.

As of February 2026, there are 172 million unique addresses holding at least one of these 15 stablecoins. USDT accounts for 136 million, USDC for 36 million, and DAI for 4.7 million. The distribution of these three stablecoins is very broad: the top 10 wallets hold only 23%-26% of the supply, with an HHI (Herfindahl-Hirschman Index, where 0 represents complete dispersion and 1 represents a single holder) of less than 0.03.

In contrast, other stablecoins show a completely different picture. The top 10 wallets often hold 60% to 99% of the supply. For example, USDS has a circulating supply of 6.9 billion USD, but 90% is concentrated in 10 wallets (HHI of 0.48). USDF has an even higher concentration, with the top 10 addresses holding 99% of the supply (HHI of 0.54). As for USD0, it approaches extremes: also 99% concentrated in the top 10 wallets, but with an HHI of 0.84, meaning even within this top ten, the supply is primarily dominated by one or two addresses.

This does not mean that these stablecoins themselves have defects—some projects were launched recently, and some were designed with institutional clients in mind from the start. But it does mean that their 'supply' numbers cannot be interpreted in the same way as USDT or USDC. Concentration of holdings can directly affect de-pegging risks, liquidity depth, and whether the so-called 'supply scale' truly represents real organic demand or merely reflects the allocation behavior of a few large holders. Only when you have the balance data of each holder, rather than relying solely on the aggregated supply derived from mint/burn events, can you perform such analysis.

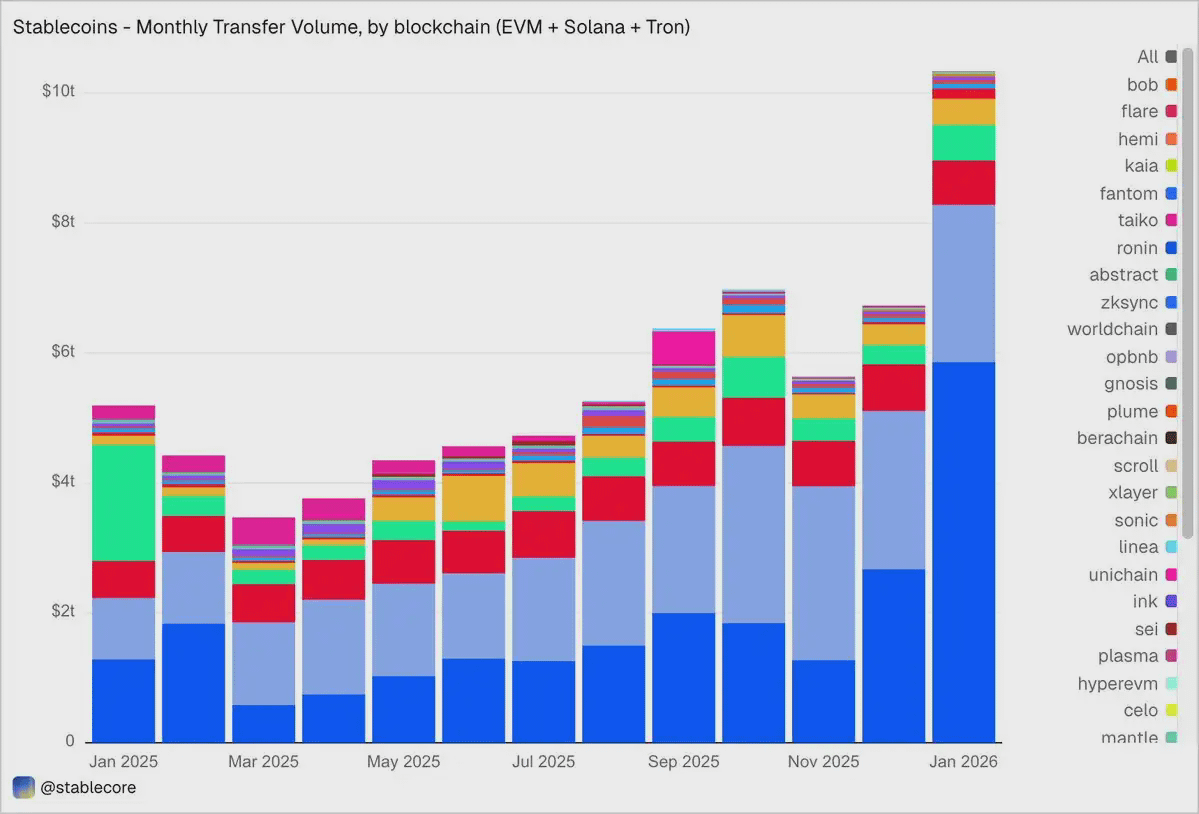

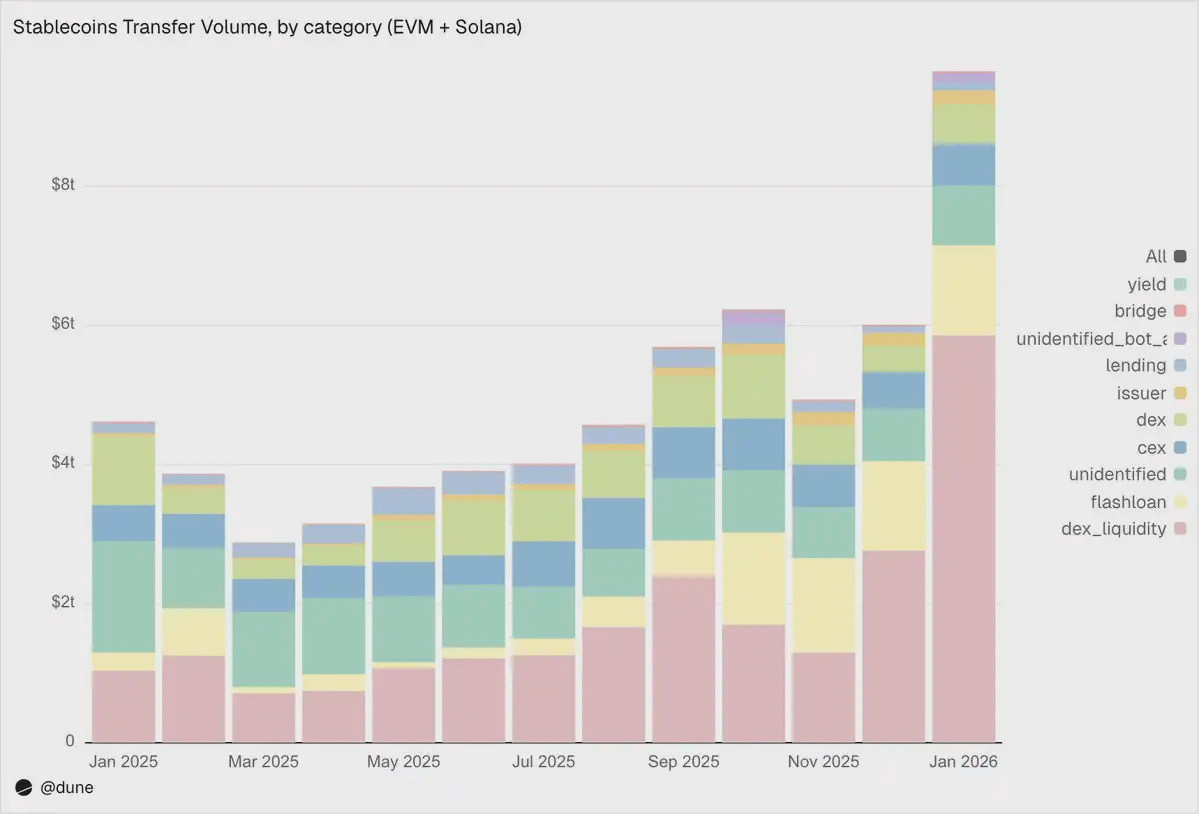

January 2026: Transfer volume 10.3 trillion USD

In January 2026, the total transfer volume of stablecoins within the EVM, Solana, and TRON ecosystems reached 10.3 trillion USD, more than double that of January 2025.

The on-chain distribution and supply structure form a stark contrast: Base leads with 5.9 trillion USD, despite its supply being only 4.4 billion USD; Ethereum follows with 2.4 trillion USD; Tron with 682 billion USD; Solana with 544 billion USD; BNB Chain with 406 billion USD.

By token, USDC dominates with 8.3 trillion USD—almost 5 times that of USDT (1.7 trillion USD)—despite its supply being only about 1/2.7 of the latter. USDC clearly circulates faster and more frequently. DAI stands at 138 billion USD, USDS at 92 billion USD, and USD1 at 43 billion USD.

It should be emphasized that this data is deliberately kept objectively neutral. The dataset was not pre-filtered based on any fixed criteria for 'real' economic activity, so the total may include flows generated by arbitrage, bots, internal routing, and other automated behaviors. We did not hard-code judgments into the data but provided an objective perspective, allowing users to choose their own filtering methods—whether it be excluding bot trading, identifying organic usage, or defining more realistic trading activity metrics.

What exactly are stablecoins doing?

This is precisely where the granularity advantage of the dataset lies. Transfers are not simply labeled as 'amounts' but categorized into different activity types based on on-chain triggering mechanisms. This means we not only know '1 trillion USD has flowed', but also 'why the flow occurred'.

1. Market Infrastructure (DEX Trading and Liquidity)

· DEX Liquidity Provision and Withdrawal: 5.9 trillion USD—the largest application scenario, reflecting the role of stablecoins as base assets for on-chain market makers.

· DEX Swap: 376 billion USD—direct trading activity on automated market makers.

The combined data indicates that stablecoins are primarily used as collateral and liquidity infrastructure for trading. Interestingly, trading volume is more concentrated in incentive-driven liquidity mining and active capital optimization activities, rather than purely trading demand.

2. Leverage and Capital Efficiency (Lending + Flash Loans)

· Flash Loans (Borrowing and Repaying): 1.3 trillion USD—automated arbitrage and liquidation cycles.

· Lending Activities (Deposits, Borrowing, Repayment, Withdrawals): 137 billion USD—representing on-chain short-term capital efficiency and structured credit layers.

3. In-and-out Channels (CEX and Cross-chain Bridges)

· CEX Liquidity—Deposits (224 billion USD), Withdrawals (224 billion USD), Internal Transfers (151 billion USD): totaling 599 billion USD.

· Cross-chain Bridge Access: 28 billion USD—showing the function of stablecoins as settlement channels between cross-chain and centralized platforms.

4. Issuer Layer (Monetary Operations)

· Issuer Operations—Minting (28 billion USD), Burning (20 billion USD), Peg Rebalancing (23 billion USD), and other operations: totaling 106 billion USD, nearly 5 times the 42 billion USD a year ago.

5. Yield Protocol

· Yield protocol activity: 2.7 billion USD—small in scale, but significant in structured strategies and on-chain asset management.

Overall, 90% of transfer volume flows through recognized activity categories, providing a fine view across all layers of the on-chain stack.

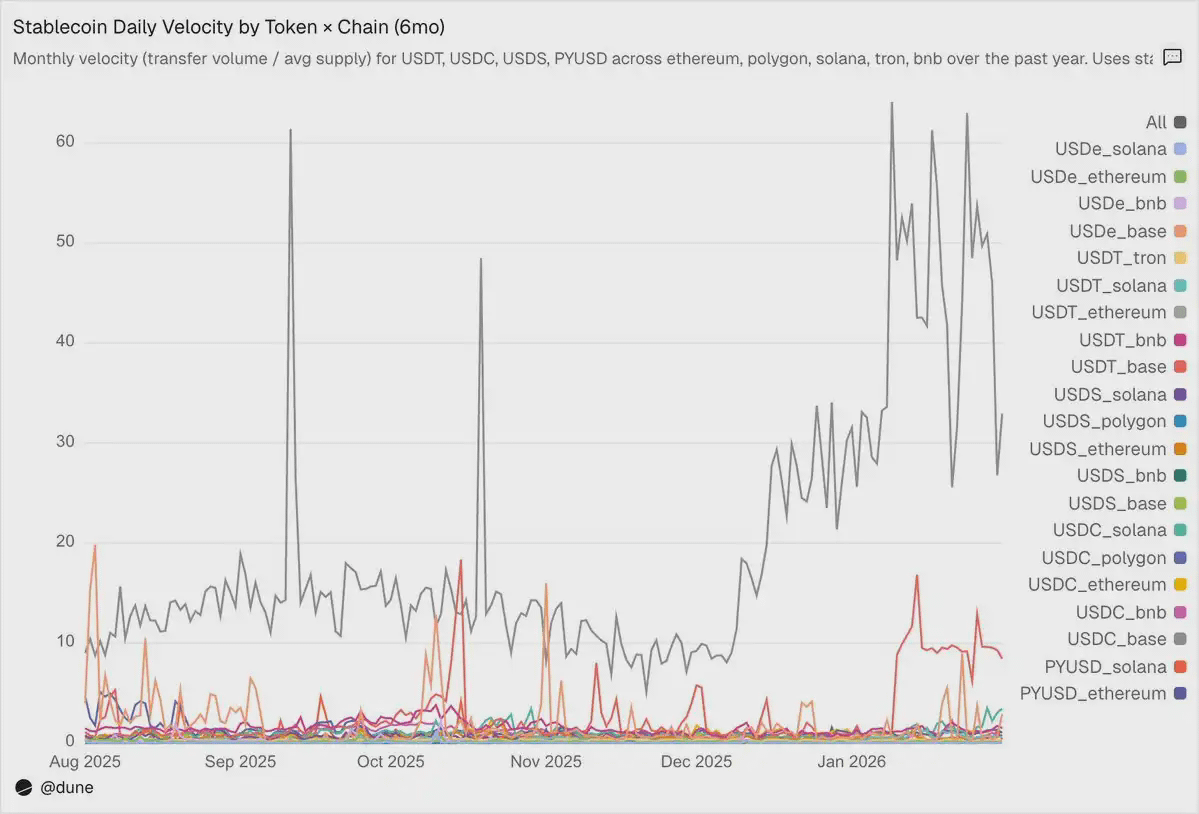

Velocity: The same token, different worlds

Daily circulation speed (trading volume divided by supply) may be the most overlooked metric in stablecoin analysis. It reveals whether stablecoins are actively used as a medium of exchange or merely held.

Among the tokens we analyzed, USDC and USDT stand out again, but exhibit different characteristics.

USDC circulates fastest on L2 and Solana. On Base, USDC's average circulation speed reaches 14 times—an astonishing figure driven by high-frequency DeFi activities; on Solana and Polygon, it's about 1 time; on Ethereum, it also reaches 0.9 times, with nearly the entire supply circulating almost daily.

USDT is the fastest on BNB Chain and Tron. It reaches 1.4 times on BNB Chain, reflecting active trading; on Tron, it is 0.3 times, with lower trading volume but unusually stable trading volume, consistent with its role as a main channel for cross-border payments. On Ethereum, USDT is only 0.2 times, with over 100 billion USD of supply mostly idle.

USDe and USDS are slower, but intentionally so. USDe has an average circulation speed of only 0.09 times on Ethereum; USDS is 0.5 times. Both are yield-bearing stablecoins: USDe is typically staked as sUSDe to capture yield from Ethena’s delta-neutral strategy; USDS is deposited in the Sky savings rate mechanism to earn protocol subsidy returns. Thus, a large portion of the supply remains in savings contracts, lending markets like Aave, or structured yield cycles. Low speed here is not a defect, but a feature—these assets are designed to accumulate yield rather than to circulate frequently.

The differences between chains are often more important than the tokens themselves. For the same PYUSD, the average circulation speed on Solana is 0.6 times, which is four times its speed on Ethereum (0.1 times). The same token exhibits completely different usage patterns in different ecosystems.

Supply and transfer volumes each tell part of the story, while circulation speed connects the two—it reveals whether a stablecoin on a particular chain is an active infrastructure or dormant capital.#稳定币 $BTC $ETH #加密市场反弹