Recently, I heard that Binance is holding an OpenClaw & AI Agent event, and coincidentally, someone talked to me about this direction, so I decided to participate. Actually, I've always wanted to create a truly operational quantitative system, rather than a PPT project that 'only draws pictures and tells stories'. This time, I took this opportunity to really dive in. Now my QuantClaw AI has connected to the Binance API and is no longer just at the backtesting stage, but can run the entire strategy process within the system.

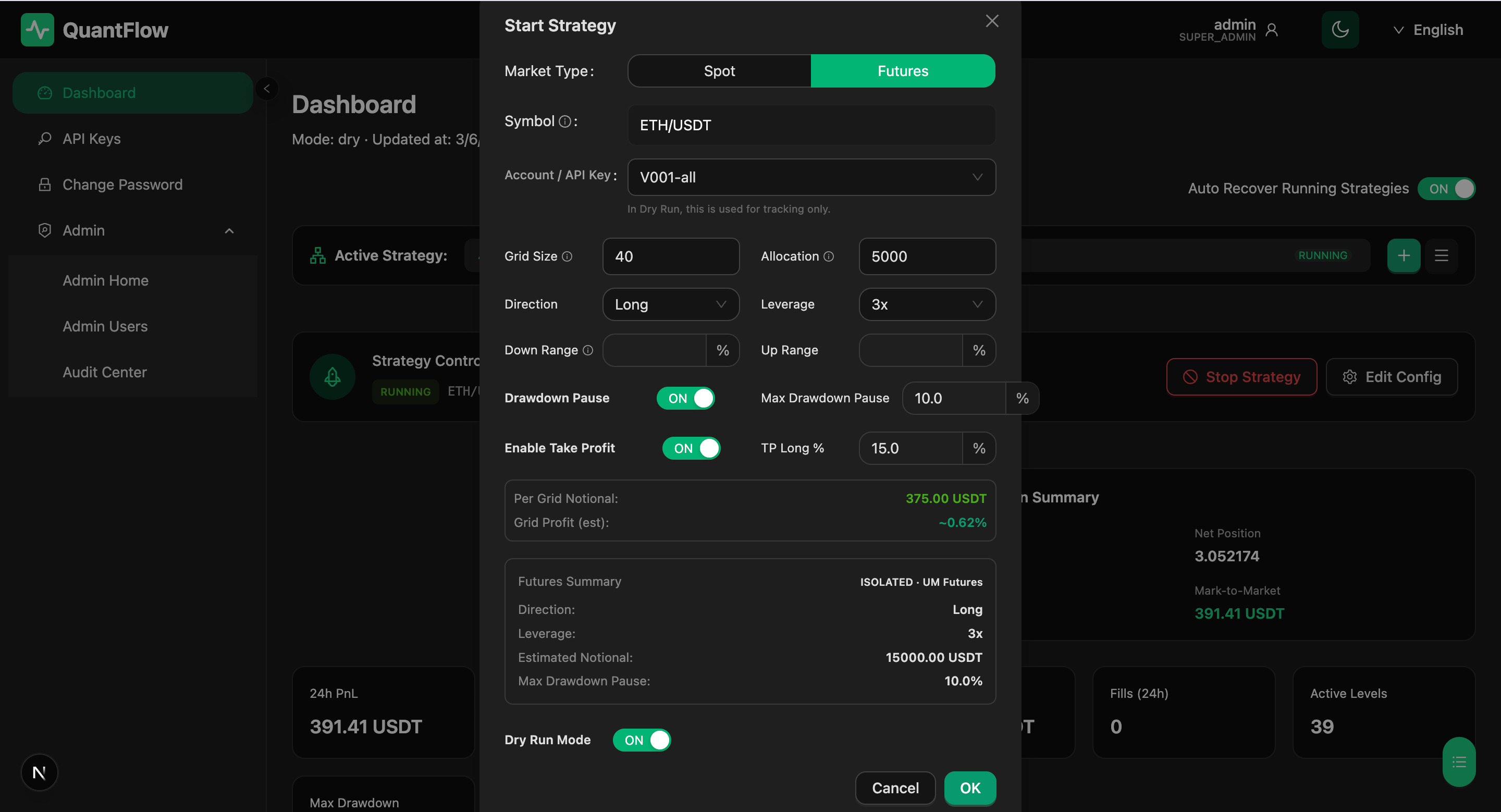

Currently, the two most practical strategies being implemented are: grid spot + grid contract. The spot mainly engages in relatively stable volatility arbitrage, while the contract improves capital efficiency when there is a clear direction or in a fluctuating range. The strategy itself is not complicated, but when actually doing it, I found that quantitative trading is actually a very 'engineering' thing.

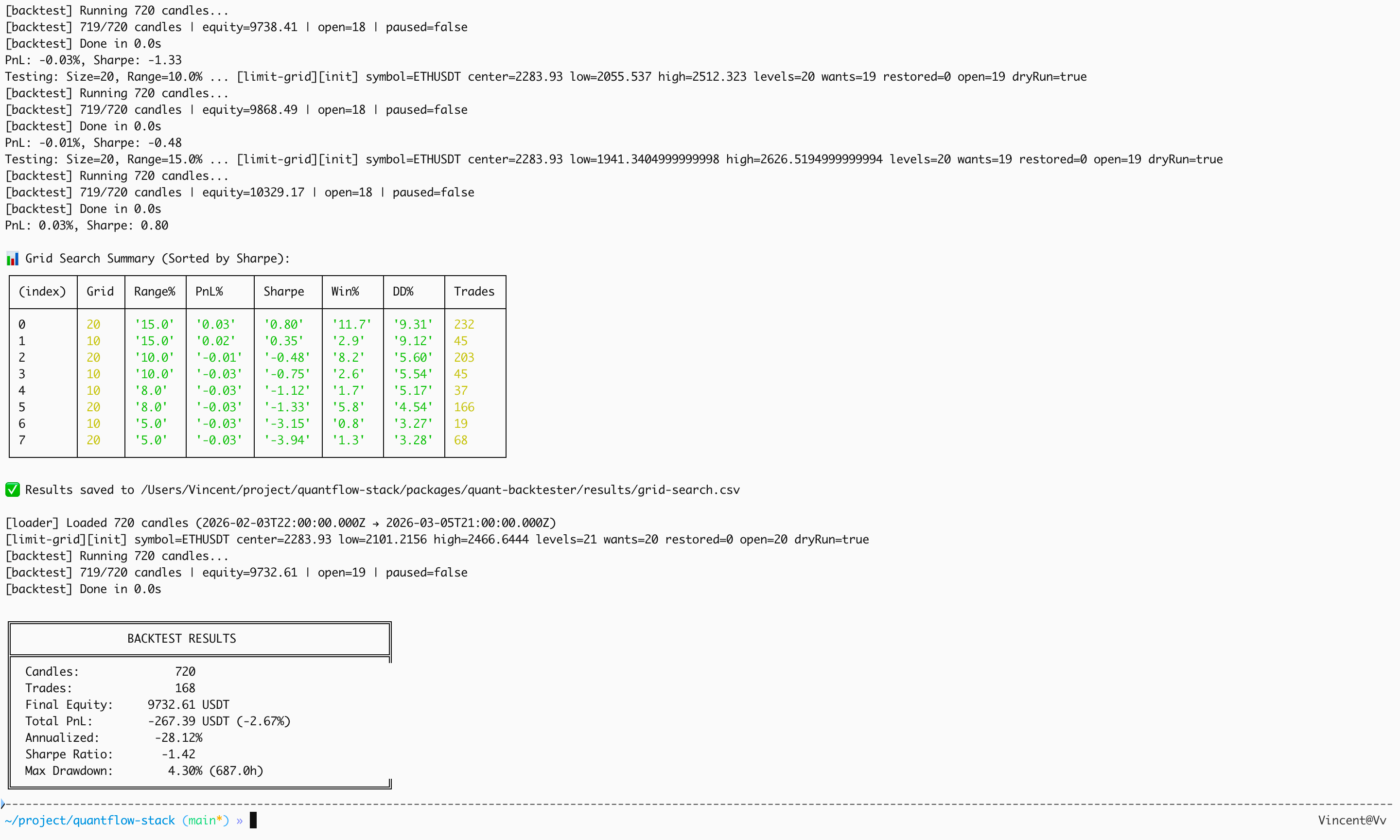

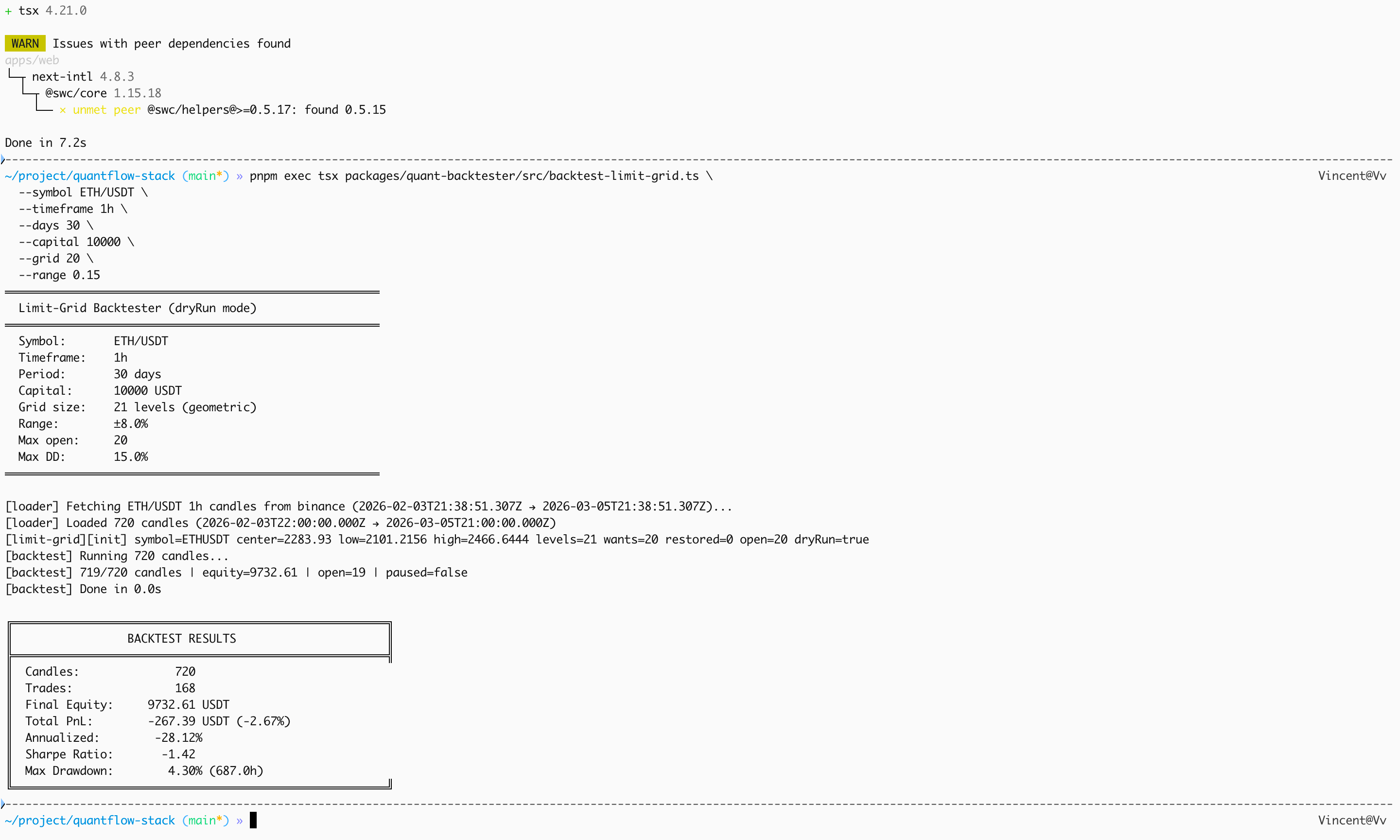

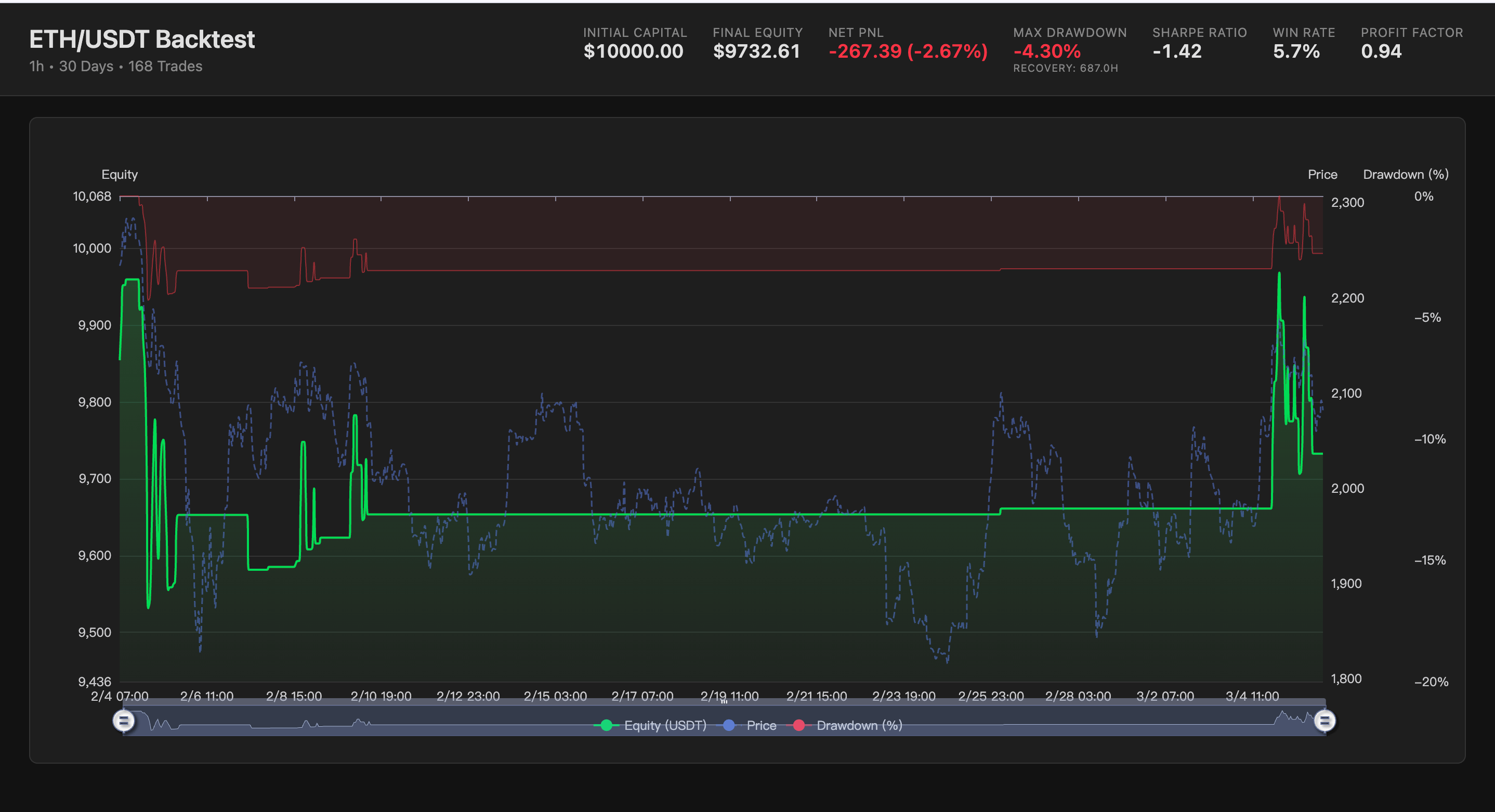

The biggest realization during this time is that quantitative analysis doesn't end with the completion of the strategy; engineering details determine life or death.

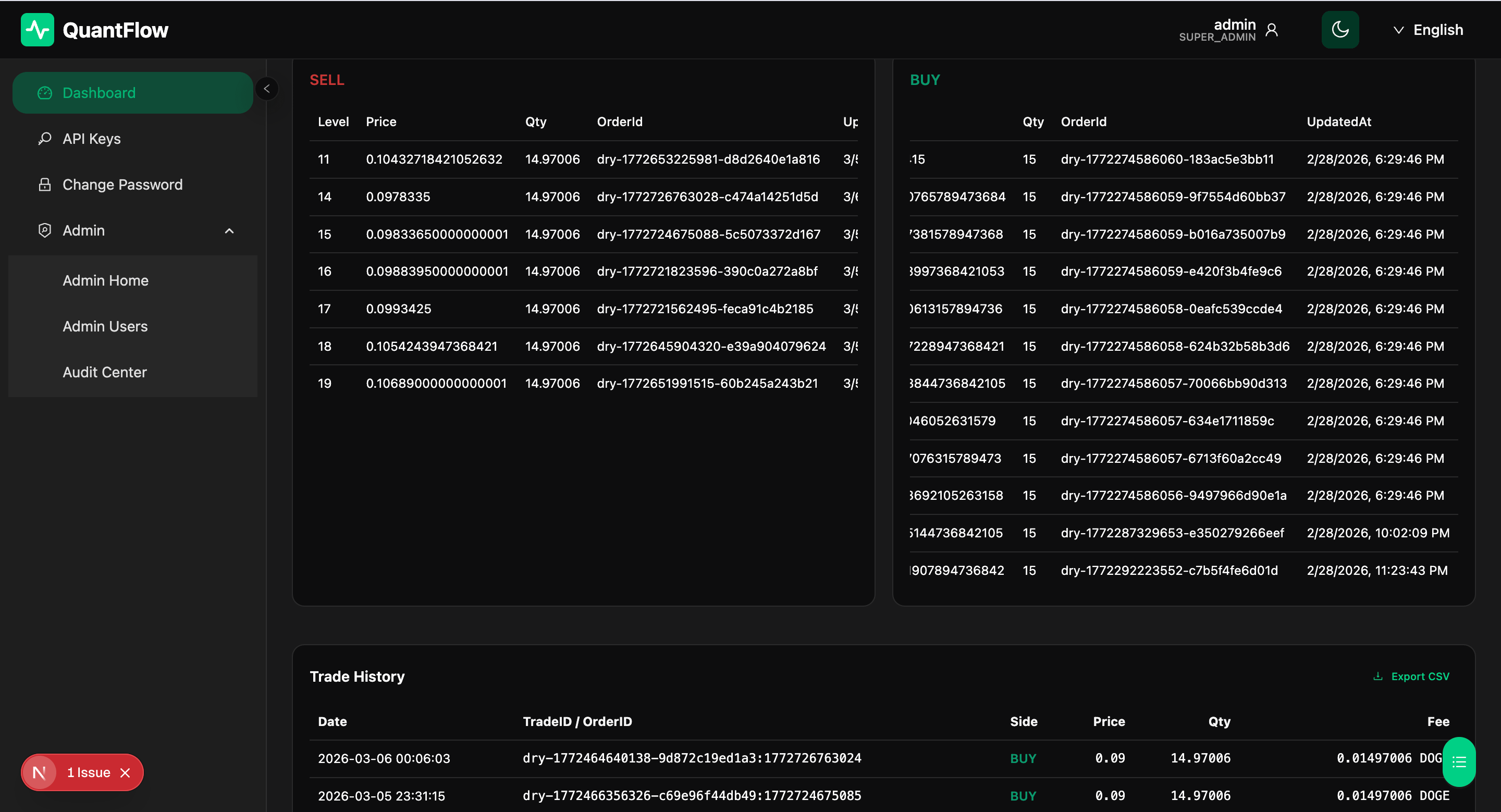

For example, the state recovery after strategy restart, transaction history persistence, abnormal retries, automatic continuation after disconnection, and clearly marking spot/contract, long/short directions on the UI. These things may not seem cool, but they are crucial in real trading; if any link fails, the profit curve could be pierced by a needle.

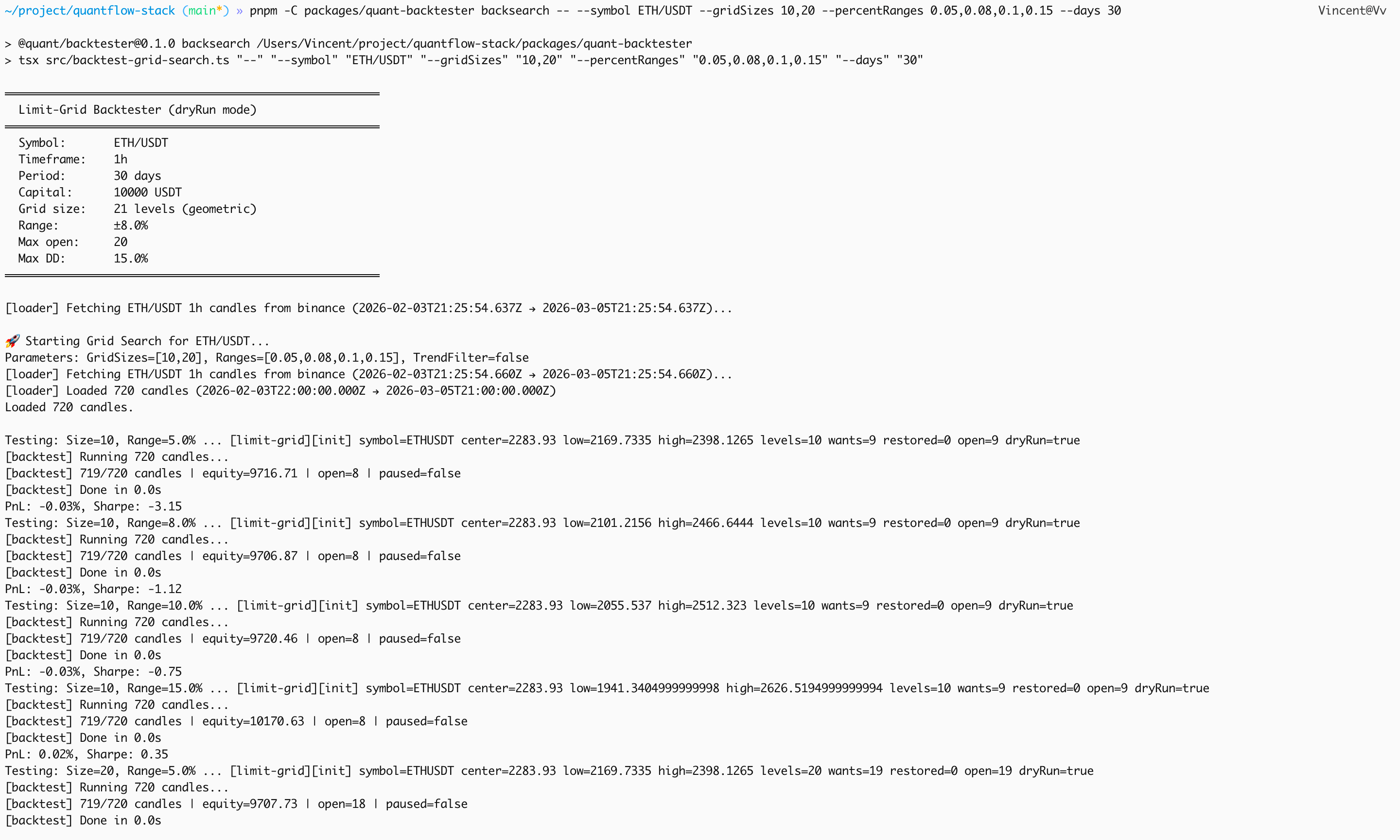

Currently, I mainly focus on several core indicators: Sharpe, PnL, maximum drawdown, and transaction frequency. For me, Sharpe is more like a stability health report rather than a bragging number; PnL is not just about exploding one day, but rather whether it can survive long-term in different market rhythms. Therefore, my strategy is to first validate with small funds, iterate in short cycles, and then gradually scale up, rather than going all in at once.

Next, I also plan to integrate the capabilities of the Little Lobster (OpenClaw Agent) into the system, not just executing strategies, but also hoping it can participate in strategy-assisted decision-making, such as subscribing to market news, observing market sentiment, combining funding rates and volatility structures to provide me with more evidence-based adjustment suggestions.

My goal is actually very down-to-earth; it's not about shouting some slogan like 'dominate the market,' but rather hoping that QuantClaw can become a tool that helps me reduce emotional trading, improve execution discipline, and steadily make profits.

For me, this project is not just a competition entry, but more like turning the idea of 'wanting to do quantitative analysis for a long time' into a real system that iterates every day. I will continue to publicly share progress, and if there are friends who understand trading and engineering, you are welcome to exchange ideas and refine QuantClaw into a truly viable quantitative product for long-term survival in real trading.

Later: plan to integrate Binance's Square API – it can be used to share trading experiences, which feels great.