The cryptocurrency market is adjusting; why did tokenized US Treasuries defy the trend and reach a new high of $4.2 billion? Behind this question lies a trend: funds have not exited but have flowed from volatile assets to income-generating 'digital dollars'.

Stablecoins are transitioning from a settlement tool to an income-generating asset. Holding USDT and USDC no longer means idle funds, but rather, it can earn interest like a bank deposit, often with a higher yield.

So how do stablecoins achieve the transformation from a settlement tool to an income-generating asset?

The dilemma of traditional cash: holding it means losing money.

In most economies, holding cash equates to bearing opportunity costs and inflation erosion.

The annualized rate of interest for demand savings at large U.S. banks generally falls between 1% and 3%. Even in some banks' high-yield savings accounts, it mostly ranges from 4.3% to 4.5%. Deposit rates in China, Europe, Japan, and other regions have long been close to or below inflation rates. The result is: money in banks slowly loses purchasing power.

Additionally, bank wealth management, money market funds, and short-term bond funds often have minimum purchase thresholds and redemption restrictions. Traditional money market funds are mostly T+1 redeemable, with some T+0 (redeemable on the same day) products having limited daily redemption amounts (such as $10,000). For users with small amounts of money or requiring immediate liquidity, there are not many alternative income options.

In this environment, a deeply ingrained notion has formed: cash is meant to be spent, not saved. Holding cash is seen as a 'waiting for consumption' transitional state rather than an appreciating asset. The emergence of stablecoins has changed this situation.

Wealth management revolution: making cash valuable again

Stablecoins have changed this logic: holding them can earn interest, and the returns are often higher than those of banks.

Holding stablecoins like USDT, USDC, etc., allows one to earn income through DeFi protocols and RWA products, with annualized returns generally exceeding those of traditional bank demand deposits, and in some scenarios comparable to or even higher than money market funds and short-term bond funds. Thus, stablecoins evolve from being mere trading mediums to income-generating assets.

From a trading medium to an income asset

The primary use of stablecoins was initially for pricing and payments. On exchanges, over 90% of trading pairs are priced in stablecoins; in settlement scenarios, by 2025, the on-chain trading volume of stablecoins will reach $33.5 trillion, surpassing the combined scale of Visa and Mastercard. However, beyond the settlement function, stablecoins are taking on storage and wealth management roles.

Income comes from three sources: DeFi lending interest, liquidity mining rewards, and interest distributions from RWA products. Users deposit stablecoins, and smart contracts automatically execute strategies without frequent operations.

This form of 'programmable currency' allows holding stablecoins itself to become a form of wealth management. Let’s first look at how interest-earning stablecoins achieve this.

The rise of interest-earning stablecoins

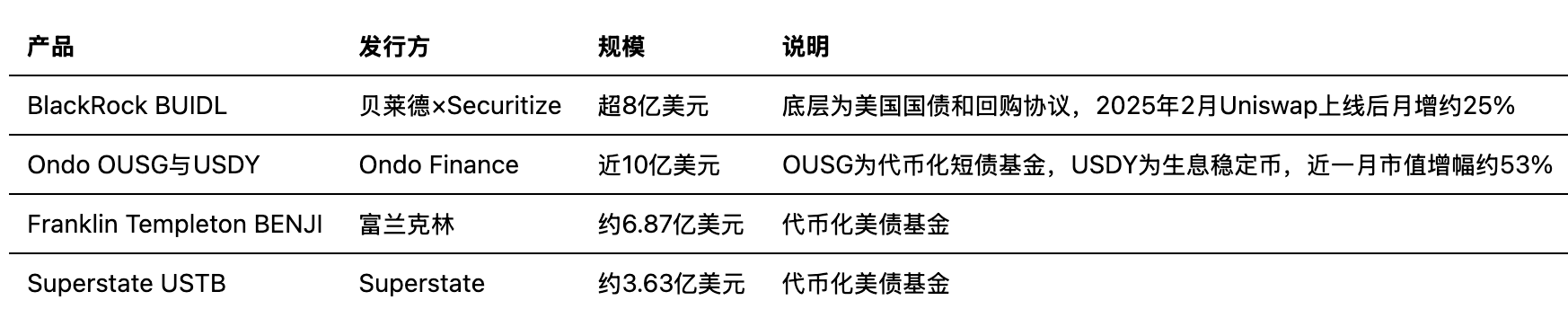

Ondo Finance's USDY (US Dollar Yield) is a typical interest-earning stablecoin, with underlying assets being short-term U.S. Treasury bonds, short-term bond ETFs, or bank demand deposits. According to public information, the annualized yield of USDY is around 4.5% to 5.3%, with daily yield accumulation upon holding.

The collaboration between Circle and Hashnote on USYC and the joint issuance of BUIDL by BlackRock and Securitize essentially also transmit off-chain treasury bond income to on-chain tokens. By 2025, the total scale of interest-earning stablecoins and tokenized treasury bond products will exceed $20 billion.

The market is shifting from 'zero-interest stablecoins' to a 'safe interest' model. Bryan Choe, head of research at rwa.xyz, points out that during crypto market pullbacks, the growth rate of tokenized treasury bonds outpaces that of stablecoins, reflecting that investors are not exiting but are seeking safer, income-generating assets on-chain. This aligns with the 'hedging' logic of funds moving from stocks to treasury bonds in traditional markets.

In addition to off-chain RWA income, on-chain DeFi also provides stable income channels. In other words, your stablecoins can not only earn interest while lying idle but also enjoy on-chain returns.

DeFi ecosystem: where does the 6% annualized, T+0 redemption come from?

6% annualized, T+0 redemption, is the core advantage of stablecoins compared to money market funds. The income of stablecoins is primarily created and distributed by decentralized finance (DeFi) protocols.

Lending protocols: stable interest income

Lending protocols like Aave and Compound allow users to deposit stablecoins to earn interest. Borrowers over-collateralize crypto assets to borrow stablecoins and pay interest; depositors share in this interest income.

According to statistics from platforms like TokenDataView, the average variable interest rate for USDC on Aave in the first half of 2025 is about 6.2% APY, and about 5.8% APY on Compound. After accounting for protocol token rewards, the net annualized yield can reach over 6% to 9%.

Compared to traditional bank savings rates of 1% to 4.5%, DeFi lending has a clear advantage in returns. Risk control relies on over-collateralization: borrowers must provide collateral valued higher than the loan amount, and the liquidation mechanism automatically triggers when the collateral ratio is insufficient, protecting depositors' principal. This is also the foundational mechanism that allows DeFi lending to operate without traditional credit assessments.

Liquidity mining: low volatility returns from stablecoin pools

In decentralized exchanges like Curve, liquidity providers for stablecoin trading pairs (such as USDT/USDC/DAI) can earn a share of transaction fees and protocol rewards. Due to the 1:1 price anchoring between stablecoins, the price difference is minimal, making the 'impermanent loss' (potential losses from price deviations) in such liquidity pools almost negligible, and the returns are relatively predictable.

The annualized returns from stablecoin pools vary with market activity, generally ranging between 5% and 15%.

Income comes from two sources: traders' transaction fees and incentive tokens issued by the protocol (like CRV).

Yield aggregator: automatically finding optimal strategies

Yield aggregators like Yearn Finance automatically allocate funds to protocols such as Aave, Compound, and Curve, seeking the highest yield strategies at any given time, and supporting one-click deposits and withdrawals. Users do not need to research each protocol individually or manually migrate funds to achieve yields close to market optimal stablecoin returns.

These products lower the participation threshold but also introduce protocol risks and smart contract risks.

Choosing mature and well-audited projects remains a prerequisite for participating in DeFi wealth management.

The underlying logic of the income mechanism

Whether it’s lending, liquidity provision, or aggregation, the ultimate source of stablecoin income is: borrowers' interest payments, traders' transaction fees, and incentives issued by protocols to attract liquidity. These values are automatically distributed through smart contracts, forming an on-chain 'money market'.

In simple terms, when you deposit stablecoins, on-chain smart contracts help you earn interest, requiring almost no operation.

RWA: U.S. Treasury bond income on-chain, allowing ordinary people to buy

Besides on-chain earnings, there is another way: bringing real assets like U.S. Treasury bonds onto the chain. RWA (Real World Asset) introduces the income from traditional assets to the blockchain.

In other words, in addition to 'earning interest spreads' on-chain, your stablecoins can also buy off-chain U.S. Treasury bond income. The essence of RWA is to bring the interest of traditional assets like U.S. Treasury bonds and commercial papers onto the chain and distribute it to token holders.

What is RWA

RWA refers to the tokenization of traditional financial assets, making them tradable, holdable, and income-generating on the blockchain. Typical assets include U.S. Treasury bonds, corporate commercial papers, real estate income rights, and commodities.

Once tokenized, these assets can be transferred on-chain 24/7, can be split into smaller units, and can also be used in combination with DeFi protocols.

For stablecoin holders, RWA provides another path for income: holding tokens linked to traditional assets like U.S. Treasury bonds to earn interest income similar to off-chain.

Tokenized U.S. Treasury bonds: the current main battlefield of RWA

U.S. Treasury bonds have a high credit rating and good liquidity, making them the most mature category within RWA. According to data from rwa.xyz, the total market value of tokenized U.S. Treasury bonds will exceed $4.2 billion by March 2025, setting a new historical record.

When the crypto market experiences a pullback, funds shift from volatile assets to tokenized U.S. Treasury bonds, forming an on-chain 'hedging' behavior.

Bryan Choe's comparison shows that during bull markets, the growth rate of stablecoins surpasses that of tokenized treasury bonds, while in bear markets, the growth rate of tokenized treasury bonds surpasses that of stablecoins, confirming the trend of investors rotating assets on-chain.

RWA is the path that injects income into stablecoins

Stablecoin issuers can invest part of their reserves in U.S. Treasury bonds, commercial papers, and other RWAs, then distribute the income to stablecoin holders. For example, issuers holding U.S. Treasury bonds earn about 4% to 5% annualized returns and design mechanisms to pass part of the income to token holders, upgrading stablecoins from 'digital dollars' to 'income-generating dollars.'

Products like Ondo USDY, Circle USYC, etc., bind treasury bond income with stablecoin holding, providing users with an interest-earning experience of 6% annualized, T+0 (redeemable on the same day). Traditional money market funds are mostly T+1 redeemable, and some T+0 products have limit restrictions; on-chain interest-earning stablecoins can achieve instant exchange and transfer, offering liquidity advantages.

In simple terms, what you are buying is not a traditional fund, but a form of on-chain 'interest-earning cash' that can be used and withdrawn at any time.

The scale and expectations of the RWA market

Reports from Binance Research indicate that the RWA market size grew by over 260% in the first half of 2025 compared to the beginning of the year, increasing from about $8.6 billion to nearly $30 billion. Citibank forecasts that by 2030, the RWA market size may reach $2 trillion to $16 trillion. The entry of traditional institutions like BlackRock, Goldman Sachs, and Blackstone has accelerated the process of asset tokenization and compliance.

In simple terms, off-chain assets are being massively 'brought on-chain', allowing ordinary people to use stablecoins to buy U.S. Treasury bond income.

DeFi combined with RWA, plus the stablecoins themselves, has created a complete on-chain dollar ecosystem.

Digital dollar economic system: the 'second heart' of the dollar is already beating

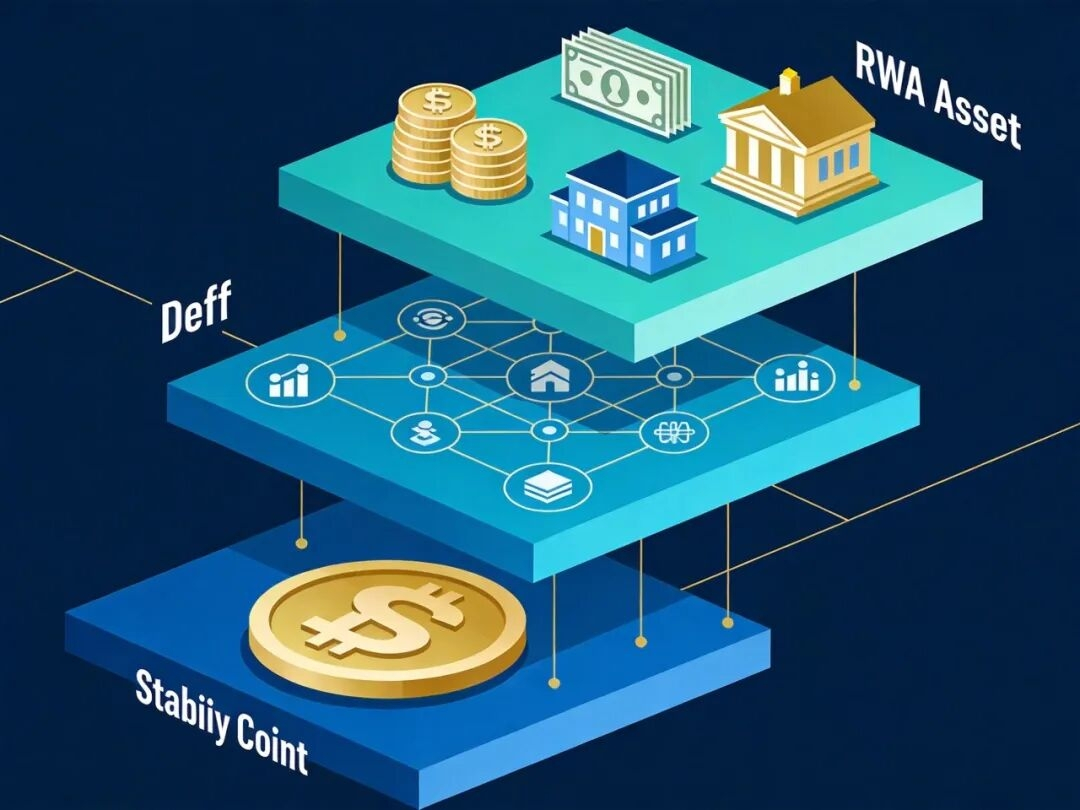

The combination of stablecoins, DeFi, and RWA has already formed an on-chain dollar ecosystem that does not rely on traditional bank accounts for participation.

Three-layer structure

Stablecoins: the base currency layer. USDT, USDC, etc. provide on-chain dollar pricing and settlement units.

DeFi: the financial services layer. Lending, trading, aggregation, and other protocols provide income and liquidity.

RWA: the asset income layer. Connecting traditional income-generating assets like U.S. Treasury bonds and commercial papers to the blockchain.

The three layers combined form a 'digital dollar economic system' that can participate without relying on traditional bank accounts. Users can deposit and withdraw funds, earn returns, and make payments through wallets, without needing to open accounts offline, unrestricted by business hours, and theoretically without national boundaries.

Two systems running in parallel

This system does not replace traditional banks but runs in parallel with them. The traditional banking system remains the first pillar of dollar credit, undertaking core functions such as deposits, loans, and settlements. Stablecoins and the DeFi network constitute a 'second heart': providing another channel for dollar liquidity and appreciation outside the traditional system.

The foundation of both is dollar credit. The value of stablecoins is ultimately still anchored to the dollar, and the income from RWA also comes from dollar-denominated treasury bonds and bonds. Therefore, the digital dollar economic system is an extension of the digitization and networking of the dollar, rather than an independent system detached from the dollar.

The significance of stablecoin wealth management

The wealth management revolution brought by stablecoins is essentially an update of monetary concepts. Cash is no longer defaulted as a 'zero yield, waiting for consumption' transitional state but can participate in earning interest and appreciation as an asset. This shift has already happened on-chain and is accelerating with the expansion of RWA scale and the clarification of regulatory frameworks.

Conclusion

Stablecoins have made 'cash' valuable again. Through DeFi protocols and RWA products, holding stablecoins can yield higher returns than traditional bank deposits while maintaining payment and transfer capabilities.

Stablecoins are no longer just simple payment tools but financial accounts that earn income, are programmable, and without borders; this is not a replication of traditional finance but a new structure formed under market selection and technological drive. The digital dollar economic system constituted by stablecoins, DeFi, and RWA is becoming an indispensable part of the dollar ecosystem and may also become a new choice for ordinary people in cash wealth management in the future.

In the future, your wallet may also hold an interest-earning stablecoin that can be deposited and withdrawn at any time; would you give it a try?