The Strait of Hormuz is practically blockaded, and the global energy market is being pushed towards what could be the most severe energy crisis since the 1970s!

On Monday, oil prices surged dramatically at the opening.

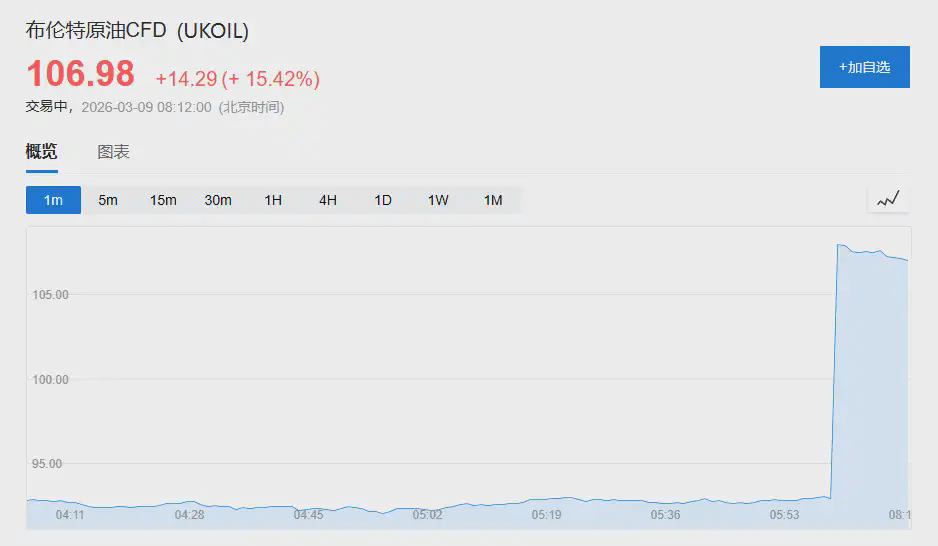

WTI crude oil futures once surged by 22%, breaking through the $110 mark; Brent crude oil futures also rose by 20%, reaching $111.04 per barrel. The gains have since moderated.

Meanwhile, due to the obstruction of crude oil exports and the rapid exhaustion of storage space, more and more major oil-producing countries in the Middle East are forced to announce production cuts.

According to previous mentions by Wall Street Journal, the wave of production cuts in the Gulf region is spreading rapidly.

Kuwait has officially declared force majeure and significantly cut production; the UAE has also started to adjust offshore production levels to relieve storage pressure.

Goldman Sachs directly "overturned" previous optimistic judgments, warning that the actual decline in flow through the Strait of Hormuz is far greater than expected. If this cannot be restored in the coming days, the upward risks for oil prices will significantly expand.

More critically, the intensity of this crisis has far exceeded initial judgments from all parties.

At the beginning of the attacks by Israel and the U.S., officials from Gulf countries generally believed that the situation would remain controllable and limited as in previous conflicts.

But this time, it is compounded by a new variable that has never appeared in history:

Qatar has become the world's largest liquefied natural gas exporter.

When its core facilities shut down, nearly 20% of global LNG supply is suddenly cut off. The energy shock thus rapidly spreads from the oil market to the gas market.

The result is: natural gas prices in Europe and Asia surged simultaneously.

Next, various sectors from Chinese chemical manufacturing to the Asian power industry may face a series of chain reactions.

The Hormuz crisis exceeded everyone's expectations.

The speed at which the crisis escalated caught the market off guard, largely due to initial misjudgments from all parties.

According to the Wall Street Journal, a few weeks before the attacks by Israel and the U.S., Gulf oil-producing country officials received assurances from the U.S. side that even if retaliatory actions occurred, the targets would only be U.S. military bases.

In other words, Iran will not attack the energy facilities of Gulf countries nor will it attempt to blockade the Strait of Hormuz.

After all, during the 12-day bombing by Israel and the U.S. against Iran last June, the Strait of Hormuz remained open at all times.

Therefore, when the attack actually happened, most officials were still optimistic.

It is reported that some officials even forwarded memes of Mr. Bean giving the middle finger in chat groups, comparing Iran's possible retaliatory actions to this clumsy comedic character.

OPEC held a meeting on the first Sunday after the attack, focusing on whether to increase production, with almost no serious discussion on the situation in Iran.

Until the situation rapidly spiraled out of control.

A senior Saudi official later admitted:

"We really did not expect Iran to strike at the entire Gulf, completely throwing our relationship aside."

Subsequently, a recording of a suspected Iranian naval officer notifying ships not to enter the Strait of Hormuz was quickly circulated in industry WhatsApp groups.

The flow of tankers plummeted, and market sentiment immediately turned to panic.

Storage tanks are in urgent condition, and the production cut wave is spreading.

The Strait of Hormuz is nearly blocked, quickly triggering a chain reaction among Middle Eastern oil-producing countries.

The core reason is simple: the storage capacity is running out.

Iraq was the first to be forced to cut production due to storage tanks nearing saturation, with production reductions exceeding two-thirds.

Subsequently, Kuwait Oil Company officially declared force majeure.

According to Bloomberg, citing informed sources, Kuwait's production cut has expanded from about 100,000 barrels per day on Saturday to nearly 300,000 barrels per day, and it will continue to adjust based on storage levels and the situation in the Strait.

In January of this year, Kuwait's daily production was about 2.57 million barrels, and the only export route is the Strait of Hormuz. Once the Strait remains blocked for a prolonged period, its storage capacity could be exhausted in a matter of weeks or even days.

Abu Dhabi National Oil Company (Adnoc) also announced on Saturday that it is "adjusting offshore production levels to meet storage demands."

As OPEC's third largest oil producer, the UAE's daily production in January exceeded 3.5 million barrels.

Although Adnoc operates a pipeline to Fujairah port with a daily capacity of about 1.5 million barrels, which can bypass the Strait of Hormuz to maintain partial exports, this route cannot fully replace the transport capacity of the Strait.

Morgan Stanley estimates that if the Strait is not reopened by this Friday:

· The region's daily production decline may exceed 4 million barrels.

· By the end of March, the reduction could approach 9 million barrels.

This is equivalent to nearly one-tenth of global demand.

Saudi Arabia has begun rerouting some crude oil exports to the Red Sea port of Yanbu.

However, Goldman Sachs tracking data shows that the net redirection flow through pipelines and alternative ports has only increased by about 900,000 barrels per day in the past four days, far below the theoretical limit of 3.6 million barrels per day.

Additionally, the attack on the Fujairah storage facilities and the shortage of marine fuel have further compressed alternative export capabilities.

Qatar LNG Shutdown: The "New Variable" of the Crisis.

Unlike any previous energy conflict in the Middle East:

Qatar has become the world's largest LNG exporter.

This dependency formed over the past 20 years has been thoroughly amplified in this crisis.

After the Iranian drone attack on Qatar's Ras Laffan gas complex, Qatar Energy Company announced on March 2 that it would stop LNG production at the facility and declared force majeure.

Ras Laffan has an annual capacity of 77 million tons, accounting for about 20% of global LNG supply.

HSBC Global Investment Research pointed out that the facility's shutdown is not only due to the blockage of the Strait.

Due to the inability to transport goods, on-site storage capacity is only about 1 million tons, less than five days of normal loading capacity. In other words, Qatar Energy Company has no choice but to halt production.

The market response was very direct.

European benchmark natural gas prices (TTF) surged by about 70% over two trading days; Asian spot LNG prices (JKM) rose by about 50%.

Both have set new highs in nearly three years.

LNG tankers have even engaged in a "scramble for goods" on the high seas.

A LNG ship named Clean Mistral suddenly turned 90 degrees towards Asia while en route to Spain, followed by several other ships making similar adjustments.

What’s more troublesome is that restarting also requires time.

Reuters cites industry estimates:

· Restarting Ras Laffan itself requires about two weeks.

· It will take another two weeks to return to full production.

HSBC estimates:

· A shutdown of 1 month will result in a loss of about 6.8 million tons of LNG.

· The loss from a shutdown of 3 months is about 20.5 million tons.

Considering that Trump previously indicated that the war with Iran is expected to last four to five weeks, the supply loss in the market's mainstream scenario is already close to 8 million tons.

The problem is that the global LNG market has almost no backup capacity.

Although the U.S. is the world's largest LNG exporter, its backup capacity is estimated to be only about 5%; Norway has stated that its natural gas production is nearing full capacity; Australia's backup capacity is similarly limited.

Goldman Sachs 'tore up the report': the upward risk for oil prices is expanding rapidly.

Goldman Sachs' commodity research team published a report on March 6, nearly publicly overturning previous forecasts.

Goldman Sachs' chief oil strategist Daan Struyven previously set the baseline path as:

· The flow through the Strait of Hormuz is expected to maintain about 15% for the next five days.

· The following two weeks will restore to 70%.

· It will take another two weeks to restore to 100%.

Based on this assumption, Goldman Sachs raised its second quarter average price forecast for Brent to $76, and WTI to $71.

But reality soon shattered these assumptions.

Goldman Sachs' latest estimate:

The flow through the Strait of Hormuz has already decreased by about 90%, which is a reduction of about 18 million barrels per day.

The actual redirected flow through alternative pipelines is only a quarter of the theoretical limit.

At the same time, most shipowners are now choosing to wait and see.

What truly prevents ships from passing is not the freight costs, but the physical safety risks— as long as physical risks exist, ships will not pass through, no matter how high the freight rates.

Goldman Sachs bluntly stated in the report:

If there are no signs of a solution this week, oil prices could likely break through $100 next week.

If the Strait's flow remains low throughout March, oil prices (especially refined oil) could exceed the historical peaks of 2008 and 2022.

The report specifically emphasizes:

The upward risk for oil prices is "rapidly expanding."

Energy historian Daniel Yergin also warned:

In terms of daily oil production, this is the largest supply disruption in global history. If it lasts for several weeks, it will have far-reaching effects on the global economy.

The U.S. is relatively insulated, but the shock is still spreading.

U.S. Energy Secretary Chris Wright stated on Fox News that energy "will soon flow back through" the Strait of Hormuz and believes that the rise in oil prices mainly comes from market concerns about the duration of the conflict.

Trump stated on Air Force One that he was not worried about gasoline prices and expected oil prices to "drop very quickly" after the war ends.

Compared to the 1970s, the U.S. energy structure is indeed more resilient now.

The proportion of the oil and gas industry in GDP is lower, and the U.S. has itself become a major energy exporter.

But the problem is—

Oil prices are globally priced.

The rise in retail prices for gasoline and diesel will still have a real impact on U.S. consumers.

Airline executives have warned that soaring jet fuel prices will squeeze quarterly profits and may drive up ticket prices.

At the same time, some of the U.S. government's response measures also conflict with existing policies.

To mitigate the impact of supply disruptions in the Gulf, the U.S. Treasury has eased certain sanctions on Russian oil to allow countries like India to seek alternative supplies.

This forms a clear contradiction to the previous policies aimed at isolating the Russian oil industry.

According to analysis from HSBC and Morgan Stanley, this energy shock presents distinctly different impacts in Eurasia.

For the Chinese chemical industry, this is somewhat an opportunity.

The surge in European natural gas prices has raised production costs for local chemical companies. HSBC Qianhai Securities pointed out that this will bring market share expansion and product premium space for Chinese chemical companies (such as in MDI, TDI, vitamins, etc.).

In Asia, however, the situation is even more severe—

The market is facing a real energy supply shortage.

Morgan Stanley pointed out that about 20% of Asia's electricity and gas industry relies on Middle Eastern LNG, with particularly significant exposure in India, Thailand, and the Philippines.

To cope with fuel shortages and rising costs, some Asian countries have begun to revert to coal power to maintain grid stability.#伊朗新领袖 #特朗普称伊朗战事接近尾声 #国际油价突破100美元 $BTC $ETH