Introduction: The currency rules that are quietly being rewritten

The Argentine peso has depreciated by 200% in a year, and Argentinians are already using USDT to pay salaries. In 2025, Buenos Aires, a designer received a payment from a client in New York: not a bank transfer, not PayPal, but USDT. The entire transaction was completed on the blockchain, arriving in seconds, with fees of less than a cent. If done through traditional bank cross-border remittance, it would take 3 to 5 business days, with fees ranging from 3% to 5%, plus the burden of peso exchange rate fluctuations.

This scene is playing out in the lives of hundreds of millions worldwide: Turkish freelancers using USDC to avoid the collapse of the lira; Nigerian remittance workers sending income back home through stablecoins, with costs significantly lower than traditional channels (the average global remittance cost is about 6.5%, reaching 8.45% in Sub-Saharan Africa, while platforms like Yellow Card can achieve zero or very low fees in the African corridor); Vietnamese small businesses paying suppliers with stablecoins, reducing settlement time from 5–15 business days to seconds.

These phenomena point to one conclusion: stablecoins are evolving from peripheral tools on cryptocurrency exchanges into infrastructure covering the daily financial lives of hundreds of millions of people. They are neither an appendage of Bitcoin nor a speculative instrument, but rather a completely new, programmable, and cross-border form of financial account.

Taking this observation a step further: stablecoins are less like crypto assets and more like the next generation of global bank accounts. Functionally, they cover storage, payment, and yield; in terms of scale, they serve hundreds of millions of people, and their on-chain clearing volume has surpassed Visa and Mastercard combined.

Stablecoins are not only on-chain dollars, but also on-chain banks.

I. Stablecoins Restructure Bank Accounts

1.1 The Four Functions and Deficiencies of Bank Accounts

Before discussing stablecoins, we must first answer a fundamental question: What is the essential function of a bank account?

The functions of money can be summarized in three points: store of value, medium of exchange, and unit of account. A complete bank account, on the other hand, adds the following services to these three functions:

Store of value: Safeguarding wealth in fiat currency, maintaining liquidity and allowing for easy access.

Payment and settlement: the transfer of funds between individuals, businesses, and institutions to complete commercial transactions.

Income generation: Generating additional returns through deposit interest, wealth management products, or loan services.

Credit building: Based on account history, a credit score is generated to support lending and financial services.

However, this system has structural flaws.

Geographical barriers mean that approximately 1.3 billion people worldwide remain "unbanked," excluded from the modern financial system by reasons such as lack of identification documents, living in areas not covered by bank branches, or failing to meet minimum deposit requirements.

The efficiency dilemma is that a standard international bank transfer in the SWIFT network involves three to four nodes: the originating bank, intermediary banks, and the receiving bank. Each node can potentially cause delays and accumulated fees, resulting in an overall arrival time that typically takes 2 to 5 business days, with fees generally ranging from 3% to 8%. Furthermore, global banking system clearinghouses (such as Fedwire at the Federal Reserve and TARGET2 in Europe) are subject to operating hours and cannot operate on holidays.

1.2 Second-level settlement, 24/7 operation: Stablecoins are rewriting banking rules.

Stablecoins implement the three core functions of bank accounts on the blockchain and systematically overcome the aforementioned limitations of traditional banks:

Traditional banks are limited by geography and identity, while stablecoins only require an internet connection and have already covered 150+ countries.

Settlement time has been reduced from 1-5 business days to seconds, making it 100-500 times faster.

Traditional banks are limited by working days and time zones, while stablecoins operate 24/7.

Cross-border transaction fees have been reduced from 3%-8% to less than 0.1%, a decrease of 90%-99%.

Smart contracts enable stablecoins to execute automatically without human intervention.

On-chain public auditability, trust costs approach zero.

No ID or proof of address required; a wallet address is all you need to open an account.

Programmability is particularly crucial. Traditional bank remittances are one-time, static transfers of funds. Stablecoin accounts, through smart contracts, can achieve:

Conditional payment: "Funds are automatically released after the user completes task verification."

Regular automatic transfers: Payroll or subscription deductions that require no manual intervention.

Multi-party atomic settlement: Multiple transactions either succeed simultaneously or are rolled back simultaneously, completely eliminating settlement risk.

Composable Finance: Stablecoin balances can be directly used to access DeFi protocols and automatically earn interest.

The boundaries of programmability continue to expand. Previously, private key management was a barrier for ordinary users. With the advent of account abstraction (ERC-4337), users can log into their wallets using email or social media accounts, eliminating the need to access mnemonic phrases. Intent-based architecture goes even further: users simply declare "I want to pay X to Y," and the solver automatically selects the optimal path, disregarding details like cross-chain and gas fees. Programmable payments are transforming from a developer's tool into a smart payment system accessible to ordinary users.

Programmability is a key dimension that allows stablecoins to surpass bank accounts. A monetary account that can self-execute, automatically clear, and operate according to rules has an intrinsic value far exceeding that of any traditional banking product.

Bank accounts were the financial containers of the 20th century, while stablecoin addresses are the programmable financial nodes of the 21st century.

II. The Three Roles of Stablecoins in the Crypto Economy

If we compare the crypto-financial system to a city, Bitcoin is the city's gold reserves, Ethereum is the city's basic computing infrastructure, and stablecoins are the currency circulating in the city, the lifeblood that allows the entire economic system to function.

2.1 Stablecoins serve as the pricing standard for on-chain economies.

Almost all trading pairs, derivative contracts, and lending products in the crypto market use stablecoins as their pricing standard.

Bitcoin and Ethereum exhibit extremely high price volatility. Ethereum's price plummeted from nearly $4,000 to approximately $900 within a year in 2022, a fluctuation exceeding 75%. Pricing lending products with highly volatile assets makes risk management extremely difficult. In contrast, stablecoins provide a unique on-chain "measure of value," enabling option pricing, liquidation threshold setting, and margin calculation.

Taking the DeFi lending protocol Aave as an example, over 65% of its total value locked (TVL) of collateral and over 75% of its lending demand are in the form of stablecoins. Without stablecoins, DeFi lending would be virtually impossible to operate.

2.2 Stablecoins account for 70% of on-chain transfers and are the main on-chain payment channel.

In decentralized exchanges (DEXs), stablecoin pairs (such as USDC/USDT and USDC/DAI) typically account for 40% to 60% of the total trading volume. This is because when users adjust their asset allocation, they usually need to convert their holdings into stablecoins before proceeding with further operations, making stablecoins the most frequently used "intermediate currency" in the crypto economy.

In the cross-chain ecosystem, stablecoins hold a more central position. A significant amount of fund flows between multiple chains, including Ethereum, BNB Chain, Polygon, Solana, and Arbitrum, are facilitated through stablecoin bridging. From 2024 to 2025, the volume of stablecoin cross-chain bridging transactions continued to grow, with protocols such as Circle CCTP and LayerZero processing billions of dollars in cross-chain transfers monthly. Circle CCTP (Cross-Chain Transfer Protocol) allows USDC to be burned on the source chain and minted on the target chain, achieving native cross-chain functionality without the need for a third-party bridge; full-chain interoperability protocols like LayerZero enable stablecoins to flow uniformly across multiple chains, reducing liquidity fragmentation. These solutions directly impact the usability of stablecoins: users no longer need to hold USDC on each chain separately, and the latency and slippage of cross-chain transfers are significantly reduced.

Key data: Stablecoins account for over 70% of total on-chain transactions, far exceeding Bitcoin's 15% and Ethereum's 8%. Stablecoins have become the largest payment medium in the on-chain economic system.

2.3 Stablecoins are the core pillar of DeFi liquidity.

In the realm of yield strategies, stablecoins are the most core productive assets. Stablecoin holders can deposit them into protocols such as Compound, Aave, and Curve to earn annualized returns of approximately 3% to 15%, without bearing exchange rate risk.

This characteristic elevates stablecoins beyond ordinary "stores of value" to become "productive financial assets": maintaining value stability while actively generating returns. Similar to the logic of traditional bank savings, but implemented within a globally open and permissionless framework, holders can obtain on-chain returns without bearing exchange rate risk.

MakerDAO is a prime example. This decentralized stablecoin protocol maintains a supply of approximately $8.5 billion in DAI and allocates its reserves to real-world assets such as U.S. Treasury bonds, creating an "on-chain central bank" style balance sheet management.

Bitcoin is digital gold, Ethereum is a global computer, and stablecoins are the on-chain monetary system itself.

The inclusion of storage, payment, and yield functions makes stablecoins functionally equivalent to bank accounts.

III. Four types of stablecoin pegs and the triple trust model

Stablecoins do not have a single technological architecture, but rather represent humanity's diverse explorations of "how to create trustworthy currency in the digital world." Behind each different design lies a different monetary philosophy and trust assumption.

Fiat-backed cryptocurrencies (USDT, USDC): 1:1 fiat currency reserves, trust comes from centralized institutions, high stability and strong liquidity, but face centralization risks and regulatory pressure.

Algorithmic (UST collapsed, Frax hybrid): Algorithmic/hybrid regulation, trust comes from code and mechanisms, pursuing decentralization, but there is a risk of mechanism failure.

Real asset-backed RWA (USDM, sFRAX): pegged to government bonds/real assets, trust comes from asset value, offering both returns and inflation protection, but with liquidity risks.

Precious metals (PAXG, DGX): Physical gold reserves, trusted assets based on global consensus, value independent of national credit, and relatively limited liquidity.

3.1 USDT and USDC account for 86% of the market capitalization, with fiat currency-backed securities being the mainstream.

USDT (Tether) and USDC (Circle) are currently the dominant players in the stablecoin market, with a combined market capitalization exceeding $260 billion, accounting for approximately 86% of the total stablecoin market capitalization. USDT holds about 60% of the market share, and USDC about 25%. Whoever controls the on-chain unit of account controls the on-chain economy; the dominance of USD-denominated stablecoins means that the US dollar has effectively become the "on-chain reserve currency."

Their operating logic is straightforward: for every USDT or USDC issued, the issuer must hold an equivalent amount of US dollars (or dollar equivalents such as short-term treasury bonds) in a bank account as reserves. Users' trust in stablecoins ultimately stems from their trust in the issuing institution, believing that Tether or Circle truly holds sufficient reserves and can fully redeem users when they redeem their coins.

In-depth case analysis: The regulatory game of Tether (USDT).

Tether was once the most opaque entity in the crypto market. In 2021, the New York Attorney General's office reached a settlement with Tether, which paid an $18.5 million fine and admitted to misappropriating reserve assets to cover losses at the Bitfinex exchange.

Subsequently, Tether significantly improved reserve transparency, transferring a large portion of its reserves from commercial paper to U.S. Treasury securities and establishing a quarterly reserve certification mechanism. However, controversy persists: Tether's certifications are issued by accounting firms such as BDO, rather than undergoing a comprehensive audit by the "Big Four," leading some market participants to have doubts about the integrity and redeemability of its reserves. Regulatory requirements from multiple U.S. states and compliance requirements under the EU's MiCA also constrain Tether's operations.

Ironically, it was precisely these crises and doubts that made Tether stronger: it strengthened reserve management and became a major buyer in the US Treasury market (its holdings at one point surpassed those of many sovereign nations). USDT remains the world's most traded cryptocurrency, with a daily trading volume exceeding $60 billion, surpassing Bitcoin.

3.2 Survivors of Algorithmic Stablecoins After Luna's Collapse

Algorithmic stablecoins have the most radical design philosophy: replacing central institutions with code and economic incentives to automatically maintain price stability. This is the ultimate experiment in whether "currency can be completely trustless."

In May 2022, the Terra/Luna ecosystem collapsed, marking the most disastrous failure in the field of algorithmic stablecoins to date. UST (TerraUSD) plummeted from $1 to zero in just one week, resulting in the loss of approximately $60 billion in market capitalization and triggering a "Black May" for the entire crypto market.

However, this failure did not end the exploration of algorithmic stablecoins. Frax Finance's hybrid mechanism (partial collateral + partial algorithm) demonstrated stronger stability after the Luna crash and has introduced real-world asset (RWA) backing, forming a "layered trust" architecture. Liquity's LUSD, on the other hand, uses an over-collateralized ETH plus liquidation mechanism, making it a collateralized rather than purely algorithmic type, and it remained pegged during the 2022 stress test.

Market Lessons:

The failure of algorithmic stablecoins offers an important lesson: the stability of a currency cannot be guaranteed solely by mathematics; it also requires the backing of real assets or trusted institutions as a last line of defense. Purely algorithmic stablecoins (without real asset backing) have been condemned by the market; future "decentralized stablecoins" can only be hybrid types.

3.3 RWA Track: Tokenization of Government Bonds and Interest-Bearing Stablecoins

Real World Asset (RWA) stablecoins are currently the most popular sector among institutions. The core logic is to digitize high-quality assets in the real world (US Treasury bonds, corporate bonds, real estate, commodities) and form "yield stablecoins" that can be traded on the blockchain.

MakerDAO is a pioneer in the RWA (Real-World Asset) sector. It holds approximately $1 billion in RWA, primarily in short-term U.S. Treasury bonds, providing real-world asset backing for DAI's stability and allowing DAI holders to indirectly benefit from Treasury yields.

Mainstream RWA products differ in their mechanisms.

Ondo OUSG is pegged to a short-term Treasury bond ETF, with redemption on a T+1 basis and returns reflected through token rebase; BlackRock BUIDL is pegged to a US dollar institutional money market fund, tokenized by Securitize, with daily compounding returns, and redemption completed through on-chain burning and off-chain redemption.

Franklin Templeton BENJI is pegged to the FOBXX money market fund, with a mechanism similar to BUIDL. The three funds each have their own strengths in terms of redemption timeliness, on-chain availability, and minimum investment amount, catering to the needs of different institutions and individuals.

Ondo USDY is even more straightforward: holding USDY is equivalent to holding the yield rights to short-term U.S. Treasury bonds, with interest accruing automatically daily. The APY is approximately 5% to 5.5% (linked to the Federal Reserve's benchmark interest rate), providing real returns while maintaining price stability.

3.4 Gold Stablecoins: On-chain Liquidity and Fragmentation

Precious metal stablecoins can be described as a "return to history": digitizing gold, the most widely recognized store of value for thousands of years, and giving it instant liquidity on the blockchain.

Paxos Gold (PAXG) is currently the largest gold stablecoin, with each token representing one ounce of physical gold stored in a London vault. Users who hold PAXG essentially own the gold, and it can be traded globally at any time without the need for physical transport or access to commodity exchanges.

The deeper significance of precious metal stablecoins lies in breaking the "liquidity curse" of gold. The dilemmas of traditional gold investment are: poor liquidity (large transactions require brokers), cumbersome delivery (physical gold requires transportation and storage), and poor divisibility (it's impossible to buy even 0.001 ounces of gold). Blockchain technology enables gold to achieve near-perfect divisibility and liquidity, allowing users to hold $1 worth of PAXG and trade it anytime, anywhere.

The emergence of precious metal stablecoins is the most profound tribute that blockchain pays to the history of human currency, reviving the gold standard, which had been dead for decades, in a completely new form in the digital world.

3.5 A Triple Trust Model of Institutions, Assets, and Algorithms

To understand the significance of stablecoins, we must first answer a more fundamental question: How is trust in currency generated?

The human monetary system has gone through three eras of trust:

The Age of Trust in Material Goods (3000 BC - 1971): The value of money derives from its physical properties: the scarcity and chemical stability of gold, and the malleability and industrial value of silver. This trust is embedded within the material itself, requiring no institutional endorsement.

The era of institutional trust (from the collapse of the Bretton Woods system in 1971 to the present): Currency has decoupled from gold and is instead anchored to the credit backing of nations. The value of the US dollar derives from the promise that the US government will repay its debts with it. This trust is highly dependent on political stability and economic strength.

The era of algorithmic trust (from the birth of Bitcoin in 2008 to the present): The value of currency comes from the verifiability of its code and the immutability of its rules. The foundation of trust in Bitcoin is not a promise from any government, but rather the belief that "mathematics does not lie, and algorithms do not corrupt."

Stablecoins simultaneously embody three trust models.

Institutional trust-based trusts (such as USDC and USDT) rely on the credit and compliance of the issuing institution, are highly stable and easy to regulate, but have single points of failure and centralization risks.

Asset-based trust products (such as PAXG and USDM) are anchored to the intrinsic value of real-world assets and are resistant to political risks, but are affected by asset price fluctuations.

Algorithm-based trust systems (such as DAI and FRAX) rely on the verifiability of code rules and are completely decentralized, but their mechanism design is complex and their fault tolerance is small.

The three models are intertwined in reality. Although DAI is called a decentralized stablecoin, its reserves already contain a large amount of USDC (institutional trust) and RWA (asset trust); USDC, although centrally issued, runs on Ethereum (algorithmic trust), and its reserves can be verified through on-chain audits (asset trust).

The most competitive stablecoins are often an organic combination of three trust models. A single source of trust is both a source of efficiency and a source of vulnerability.

3.6 The Game Between Private Currency and National Sovereignty

The rise of stablecoins is challenging a previously unquestioned assumption: that currency must be issued by a state monopoly.

In the framework of modern economics, monetary sovereignty is a core component of national sovereignty. Controlling the money supply means controlling inflation, unemployment, credit expansion, and even political cycles. Historically, every large-scale circulation of private currency has been suppressed by the state in some way: the United States banned private ownership of gold in 1934, and Facebook's Libra project failed under regulatory pressure in 2019.

However, the decentralized nature of stablecoins makes them difficult to suppress simply. USDT, without being backed by any single country, has become the most widely used "everyday dollar alternative" in dozens of countries worldwide. This is a new type of monetary phenomenon: a global currency issued by private institutions, circulating outside sovereign borders, and spontaneously adopted by hundreds of millions of people.

Stablecoins have reopened an age-old question: Who should create money? The state, the market, or an algorithm?

The coexistence of institutional, asset, and algorithmic trust models reflects the diversification of "global banking accounts".

IV. Where does the global demand for stablecoins come from?

The rise of stablecoins is neither a result of top-level design, regulatory impetus, nor simply a product of geek entertainment. Hundreds of millions of ordinary users worldwide, facing real pain points, have voted with their feet to make their choice. Remittances are the "Trojan horse" that has propelled stablecoins into the mainstream: when hundreds of millions of households use stablecoins to receive salaries and remittances, any regulatory ban will face enforcement difficulties—you cannot prevent people from receiving a payment.

4.1 Stablecoins are a survival tool when the local currency collapses.

On the menu of a Buenos Aires café, sandwich prices are rewritten weekly. The owner accepts pesos, but keeps the dollars in mind; when a customer pays with USDT, he immediately pulls out his phone to check the exchange rate before agreeing to the transaction. This scene is playing out repeatedly in Venezuela, Argentina, Zimbabwe, Turkey, and Lebanon: local currencies depreciate sharply in a short period, rapidly eroding residents' wealth. Stablecoins (mainly USDT) are not for speculation, but for survival. Local residents use them to protect their wealth; merchants use them to hedge against depreciating local currency prices; and cross-border workers use them to safely transfer income abroad.

Case Study: Argentina's Peso Crisis and USDT Transformation

In 2023, Argentina's inflation rate exceeded 200%, and the "blue dollar" exchange rate—between the official and black market rates of the peso and the US dollar—once exceeded 100%. For ordinary Argentinians, holding pesos meant a rapid devaluation of their wealth. Foreign exchange controls were extremely strict; ordinary residents could only purchase $200 per month at the official exchange rate, far from sufficient to cope with inflation.

As a result, USDT has become Argentina's "shadow dollar": merchants accept USDT quotes, real estate transactions are denominated in USDT, and even a portion of wages are paid in USDT. Chainalysis data shows that Argentina was one of the fastest-growing countries in terms of stablecoin acceptance globally in 2023.

Argentinians' choice of USDT follows a clear logic: official foreign exchange controls limit monthly foreign exchange purchases to $200, failing to hedge against inflation; while the black market "blue dollar" offers access to more dollars, its exchange rate is highly volatile and counterparty risk is high. USDT bypasses banking regulations through local exchanges (Lemon, Buenbit) and P2P channels, and on-chain transfers are verifiable and cannot be frozen. Once merchants begin accepting USDT quotes, network effects encourage more people to hold and use it, creating a positive cycle.

After Millais took office in December 2023, Argentina initiated discussions on dollarization, including plans to close the central bank and adopt the US dollar as legal tender. Before official dollarization was implemented, USDT had already become a de facto alternative to the US dollar: some companies used USDT to pay salaries, and real estate transactions were settled in USDT to circumvent foreign exchange controls.

4.2 Remittance costs have dropped from 8% to less than 0.1%, with stablecoins rewriting the rules.

In a market on the outskirts of Lagos, a vegetable vendor receives monthly remittances from her brother in London. Previously, the money went through Western Union, incurring a £12 fee and a four-day processing time; she had to take time off work to collect it in the city, adding to her travel expenses. Last week, her brother switched to Yellow Card: she scanned a QR code with her phone at a small shop next to the market, and the naira arrived in her account 10 minutes later, with a fee of less than $1. She didn't know anything about blockchain; she only knew the money had arrived.

Data confirms this trend. Global cross-border remittances exceed $800 billion annually, with a large portion flowing to developing countries. The Philippines, Mexico, Nigeria, and India are the world's largest remittance recipients, where traditional remittance fees typically range from 5% to 10%. Data shows that traditional remittance costs along the UK-Nigeria corridor are approximately 5% to 8%, requiring $50 to $80 in fees for a $1,000 remittance, and taking 3 to 5 business days. Through stablecoins and platforms like Yellow Card and Conduit, the same remittance can be completed in under 10 minutes with fees less than $1.

Yellow Card's mechanism is not complex: remitters purchase USDT in the UK using British pounds and send the USDT to the recipient's wallet in Nigeria via on-chain transfer; the recipient can then exchange the USDT for Naira cash through Yellow Card's offline agents or app. Traditional remittances involve four steps: the originating bank, SWIFT, an intermediary bank, and the receiving bank, each incurring fees and delays; stablecoin remittances break down "USD → Naira" into "USD → USDT (on-chain) → Naira," significantly reducing intermediate steps. The Central Bank of Nigeria banned banks from providing services to crypto businesses in 2021, and further deregulated the ban in 2023; while the regulatory stance on stablecoins remains unclear, their adoption by the public has already reached a considerable scale.

If the average cost of global remittances falls to below 3% of the UN Sustainable Development Goals, it will save workers in developing countries more than $40 billion annually. Stablecoins are by far the most promising technological path to achieving this goal. This is not an experiment by geeks, but a market choice made by hundreds of millions of people.

4.3 Receiving global payments from a single wallet address

A freelancer in Southeast Asia just received the final payment from a client in New York. The money arrived in 10 seconds with a fee of less than a dollar; if he had used PayPal, it would have taken 3 days and the platform would have taken a 5% cut. He had never met the client and didn't need their bank account information, only a wallet address. The global digital economy has created hundreds of millions of freelancers, remote workers, and digital creators, and the difficulty of receiving cross-border payments is a common pain point for them. PayPal is unavailable or has extremely high fees in many countries, international bank transfers are cumbersome and expensive, and cash payments are simply not feasible in digital service scenarios.

Stablecoins offer an ideal solution for this group: a single crypto wallet address can receive global payments with extremely low fees and instant arrival. Platforms such as Deel and Bitwage have commercialized stablecoin payroll payments, serving hundreds of thousands of freelancers worldwide. Freelancers no longer need to rely on PayPal or local banks; employers, on the other hand, reduce cross-border payroll costs and speed up settlements.

The rise of stablecoins is a pure example of market democracy; users voted with their feet, choosing a faster, cheaper, and more open monetary system.

This bottom-up adoption is the most powerful market validation of "global banking accounts".

V. Size and Trends of the Global Stablecoin Market

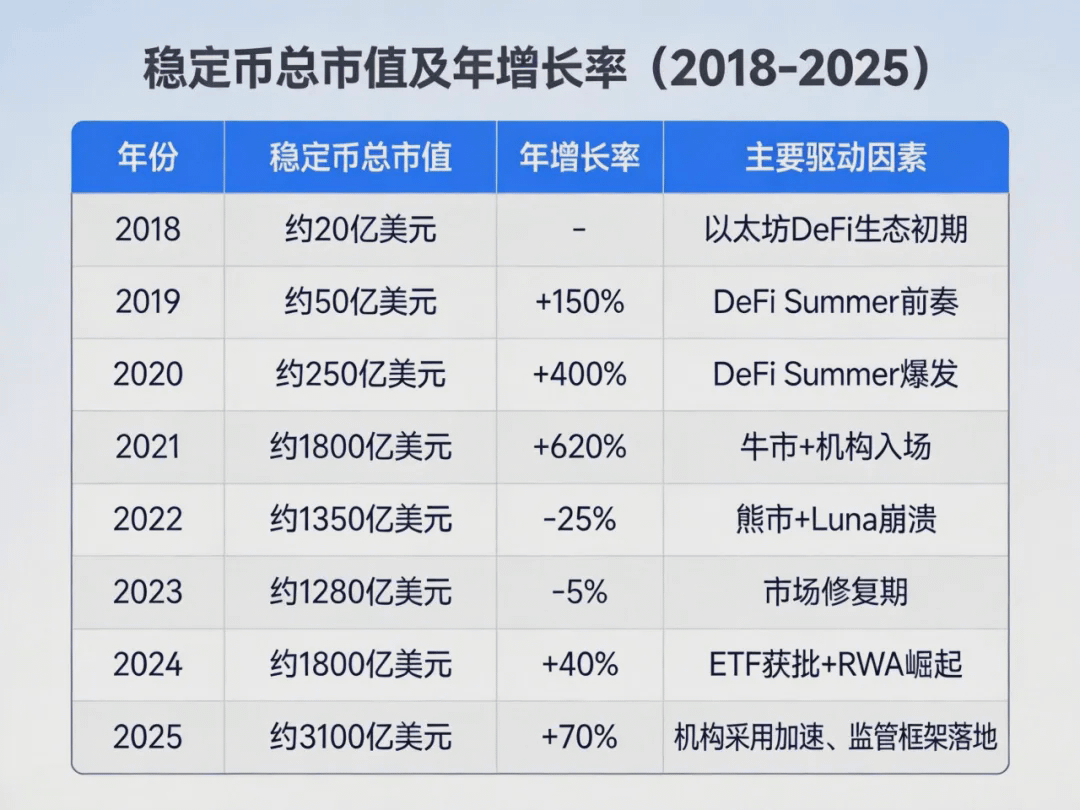

Stablecoins have a growth curve that is rarely matched in crypto history. From a market capitalization of less than $2 billion in 2018 to more than $310 billion by the end of 2025, they have grown more than 150 times in seven years.

5.1 $35 Trillion in On-Chain Settlement: Stablecoins Surpass Visa

The annual on-chain transaction volume of stablecoins is approximately $35 trillion, surpassing the combined volume of Visa and Mastercard—a point often overlooked. It's important to note that stablecoin data refers to on-chain transaction volume, including CEX deposits and withdrawals, cross-chain bridging, and DeFi fund flows, which doesn't entirely align with Visa's retail payment transaction volume; however, its scale has reached the level of mainstream payment infrastructure. Visa took 60 years to build this scale, while stablecoins achieved it in less than 10 years. The underlying reason is that on-chain transactions operate 24/7, without intermediaries or SWIFT, making the marginal cost of scaling far lower than that of traditional card organizations.

5.2 BlackRock, PayPal, and Stripe enter the market, accelerating institutionalization.

On the day BlackRock's BUIDL went live, Wall Street cash managers could allocate US Treasury yields on-chain for the first time. They didn't need to understand smart contracts; they could simply buy BUIDL like they would a money market fund. Upon redemption, the assets were destroyed on-chain, and the funds returned to their bank accounts. The boundary between traditional finance and on-chain assets was officially broken down at that moment.

In 2025, the institutionalization of stablecoins will accelerate significantly:

BlackRock launched the BUIDL fund, tokenizing US Treasury bonds, and its size has exceeded $2 billion, making it one of the world's largest on-chain RWA money market funds. The BUIDL mechanism works as follows: investors purchase BUIDL tokens on-chain, indirectly holding shares in the BlackRock USD Institutional Money Market Fund; the fund's assets consist of short-term US Treasury bonds, repurchase agreements, and cash, with daily returns automatically compounded and reflected in the token's value. Upon redemption, investors burn BUIDL on-chain, and Securitize off-chain transfers the corresponding USD to the investor's bank account. This "on-chain holding, off-chain redemption" model allows traditional institutional funds to enter on-chain yield products in a compliant manner. BUIDL has expanded to seven chains, including Ethereum, Solana, and Polygon.

PayPal's launch of PYUSD, combining its 200 million user base with a stablecoin, marks a significant step towards stablecoin adoption by major payment giants.

Stripe reopened its cryptocurrency payment functionality and acquired stablecoin infrastructure company Bridge, completing the largest acquisition in crypto history for $1.1 billion.

Visa and Mastercard expand stablecoin settlement pilot program, adding USDC to merchant settlement options.

Trend judgment:

The entry of institutions marks the formal transition of stablecoins from "experiments in the crypto world" to "mainstream financial infrastructure".

Institutional investors are able to legally allocate on-chain yield products; traditional finance gains access to digital transformation; and the entry of PayPal and Stripe has made stablecoin payments the "default option" for ordinary users.

The scale and adoption data show that "global banking" is no longer a concept, but a reality that is happening.

VI. Regulatory Game and Institutionalization of Stablecoins

Disruptive financial innovations always attract regulation. For stablecoins, regulation is both a challenge and an inevitable step towards mainstream adoption.

6.1 Differentiated Regulatory Paths: Cautious Opening Up, Proactive Embrace, and Alternative Routes

Major economies around the world are responding to the rise of stablecoins in different ways:

6.2 Rising compliance costs accelerate institutional entry

Regulation has two sides to the stablecoin market: it increases compliance costs and narrows the space for innovation, but it also provides legal certainty for institutional entry, which may attract larger-scale funds.

Taking the EU's MiCA as an example: Circle obtained one of the first EMT licenses in the EU, which clarified USDC's compliance status in the European market. This gave traditional European banks and payment institutions a legal basis to access USDC for the first time, promoting the rapid expansion of USDC in the European market.

The core controversy surrounding stablecoin regulation lies in whether to incorporate it into the existing monetary regulatory framework (bank regulation) or to legislate it as a completely new asset class. Different choices will profoundly impact its development. Once the regulatory framework is in place, compliant companies can legally access the market; users will receive clearer protection of their rights; and innovators will need to find a balance between compliance and innovation.

Key Trend: Regardless of the differences in regulatory approaches across countries, a consensus is emerging: stablecoins will be regulated, not banned. Regulation will not eliminate stablecoins; it will only accelerate their institutionalization, ultimately leading to a coexistence of "compliant" and "gray" markets. The former will serve mainstream financial users, while the latter will continue to operate in areas not covered by regulation, with both coexisting in the long term.

6.3 Criticism of BIS, USDC's de-pegging, and MiCA's delisting of USDT

The cautious criticism of stablecoins by international regulators is also noteworthy. Understanding these concerns helps in a more comprehensive assessment of the limitations and potential of stablecoins as a "global banking account."

The BIS's criticism of "singleness of money": In its 2023 Bulletin 73, the Bank for International Settlements (BIS) pointed out that private currencies circulating as "digital bearer instruments," such as stablecoins, may violate the principle of "singleness of money," which states that there should be no exchange rate fluctuations between different forms of currency. The BIS noted that stablecoins deviated from the $1 mark in the FTX crash and the Silicon Valley Bank incident, and this "near-singleness" could be amplified into systemic frictions during periods of stress. The BIS advocated replacing stablecoins with "tokenized deposits" settled in central bank currency to maintain monetary singleness.

The CPMI's "Same Business, Same Risk, Same Regulation" principle: In 2022, the Committee on International Payments and Market Infrastructures (CPMI) and IOSCO issued guidelines requiring systemically important stablecoin arrangements to comply with the Financial Market Infrastructures Principles (PFMI), namely "Same Business, Same Risk, Same Regulation." This means that if stablecoins assume payment and settlement functions, they will face regulatory standards comparable to those of banks and payment institutions.

USDC's de-pegging with Silicon Valley Bank: In March 2023, Silicon Valley Bank (SVB) collapsed, and Circle held approximately $3.3 billion in USDC reserves held there. Following the news, USDC plummeted to approximately $0.88 within hours, marking its most severe de-pegging in history. Although the US government announced full protection for depositors within 48 hours and USDC quickly returned to its peg, this event exposed the "single point of failure" risk of fiat-backed stablecoins: the collapse of a reserve bank can directly impact the redemption capacity of stablecoins.

The actual impact of MiCA on market structure: After the full implementation of the EU MiCA regulations, exchanges such as Binance and Kraken delisted USDT in the EU region due to compliance considerations, retaining only stablecoins with EMT licenses such as USDC and EUROe. The reason for the delisting was that Tether, the issuer of USDT, had not applied for an EMT license in the EU. If exchanges continued to provide USDT trading to EU users, it would violate MiCA's restrictions on "unauthorized stablecoins." After the delisting, the market share of licensed stablecoins such as USDC and EUROe in the EU region increased, and Circle gained a first-mover advantage; some users continued to use USDT through VPNs or non-EU entities, creating regulatory arbitrage. This signifies that regulation has begun to substantially reshape the stablecoin market landscape, rather than merely remaining at the principle level.

These criticisms and incidents are valid and expose the true vulnerabilities of stablecoins: single points of failure, centralized reserves, and regulatory arbitrage. However, historical experience shows that regulation typically does not stifle innovation but rather accelerates its differentiation—compliant and gray areas coexist, with the former becoming mainstream and the latter continuing in the cracks. The implementation of the regulatory framework will determine whether stablecoins can upgrade from "usable" to "trustworthy" global accounts.

VII. Stablecoins and the Web3 Financial System

Stablecoins are the monetary foundation of the Web3 financial system, which aims to build a new type of financial infrastructure that is globally open, permissionless, and highly transparent.

7.1 The 1.3 billion unbanked individuals may first have stablecoin wallets.

In a small town in East Africa, a man who had never been to a bank had a smartphone and an M-Pesa account, which he used for daily payments and transfers. Last year, someone told him he could exchange his M-Pesa balance for USDC and deposit it into an on-chain interest-bearing protocol, where it would automatically increase in value daily. He tried it, and watching the numbers change as the money arrived, he felt for the first time that he had some connection to "global interest rates." He may never have a traditional bank account; this phone is his first "global bank account."

World Bank data shows that approximately 1.3 billion adults worldwide still lack bank accounts, primarily located in sub-Saharan Africa, South Asia, Southeast Asia, and Latin America. The direct consequences of being unbanked include: inability to obtain loans, save money, and participate in formal economic activities.

Stablecoins offer these 1.3 billion people a direct path to bypass the traditional banking system: all they need is a smartphone and an internet connection to have a "global bank account" that can receive payments, store value, and conduct cross-border transactions.

Take Kenya as an example: the success of M-Pesa has proven that mobile payments can extend financial services to populations inaccessible to traditional banks. Web3 finance, built on stablecoins and DeFi, further extends this concept: M-Pesa solved the payment problem for the unbanked, but funds remained in local currency and couldn't easily participate in global assets. The extension of stablecoins + DeFi lies in this: users can exchange their M-Pesa balance for USDC, deposit it into interest-bearing protocols on Stellar or Solana to earn yields linked to US Treasury bonds, and then exchange it back to their local currency when needed. This essentially provides the unbanked with an entry point to a "global savings account": payments, savings (risk-free returns), lending (asset-backed, no credit score required), and investment (participation in global asset markets).

7.2 DeFi Lego: Composable Finance on Stablecoins

Decentralized finance (DeFi) is built on stablecoins and uses smart contracts to replace financial intermediaries, enabling traditional financial functions such as lending, trading, derivatives, and insurance, and is open to anyone in the world.

The most unique aspect of DeFi lies in its "Lego brick" composability: different protocols can be seamlessly combined to create composite products that traditional finance cannot achieve. For example, a user can deposit USDC into Aave to earn interest, use that position as collateral to borrow ETH, and then deposit it into Lido to earn staking rewards. These three layers of returns are stacked, all without human intervention. Individual users can participate in lending and earning rewards without a bank; developers gain composable financial infrastructure upon which they can build new products.

Key data: In 2025, the total value locked (TVL) in DeFi peaked at over $230 billion, with stablecoins accounting for approximately 45% of that. This means that over $100 billion in stablecoins are generating yields and liquidity 24/7 in DeFi protocols.

7.3 Stellar and Solana become the main battleground for stablecoin payments

The core pain point of traditional cross-border payments lies in the inefficiency of the SWIFT network. While SWIFT is secure, each cross-border payment needs to go through multiple intermediary banks, and each node may introduce delays, fees, and error risks.

Stablecoin peer-to-peer payments have completely restructured this architecture: sender → on-chain transmission → receiver, without the need for intermediate nodes, and stablecoin transfers between any two wallet addresses globally are "frictionless".

The Stellar network and the Solana blockchain have become the main infrastructure for stablecoin payments. Stellar processes more than 100 million stablecoin transactions annually, primarily serving remittance and payment scenarios in South America and Africa; Solana, with its extremely low fees (less than $0.0001 per transaction) and extremely high throughput (thousands of transactions per second), is becoming the preferred public blockchain for stablecoin payments.

Stablecoins have enabled finance to achieve true globalization for the first time, not just for the wealthy, but for everyone.

For the first time, 1.3 billion unbanked people may have access to a usable global financial interface, rather than just a theoretical possibility.

VIII. The Strategic Game Between Stablecoins and Central Bank Digital Currencies

Understanding the future of stablecoins is inseparable from geopolitics: the strategic competition between stablecoins (especially US dollar stablecoins) and central bank digital currencies (CBDCs) has become one of the most important monetary geopolitical narratives of the 21st century.

8.1 Dollar stablecoins unexpectedly extend the dollar's hegemony

In the stablecoin ecosystem that has emerged in the crypto market, US dollar stablecoins (USDT, USDC) hold an absolute dominant position, accounting for over 85% of the total market capitalization. This phenomenon has led to an unexpected consequence: stablecoins have become a digital extension of the global influence of the US dollar.

In over 150 countries worldwide, people use dollar-denominated stablecoins for savings, payments, and cross-border transactions, even if residents of these countries have never held physical dollars or had any contact with the US banking system. This influence is transmitted through specific pathways: when the Federal Reserve raises interest rates, the yields of interest-bearing stablecoins rise in tandem, changing the savings returns for global holders (interest rate transmission); USDT and USDC reserves are heavily allocated to US Treasury bonds, and their asset choices directly affect global dollar liquidity (reserve asset transmission). The monetary policies of the US Treasury and the Federal Reserve, through dollar-denominated stablecoins, "invisibly" influence the wealth of hundreds of millions of people worldwide.

Dollar stablecoins are essentially a "light asset" extension of dollar hegemony on the blockchain: the US can make global payments and savings pegged to the dollar without having to build bank branches or clearing infrastructure overseas. Traditional dollar internationalization relies on SWIFT, correspondent banks, and offshore dollar markets; stablecoins compress this process into a single issuer, a public blockchain, and hundreds of millions of wallet addresses.

A report by the Congressional Research Service points out that the global expansion of dollar stablecoins is the most important new channel for the internationalization of the dollar over the past decade, and its influence has even surpassed the overseas expansion of traditional financial institutions.

8.2 The Competitive Logic Between Central Bank Digital Currencies and Stablecoins

China's strategic logic in advancing the digital yuan is a strategic response to the global expansion of US dollar stablecoins. The goal of the e-CNY is to establish a China-led digital payment network without relying on US dollar stablecoin infrastructure.

However, there are fundamental architectural differences between e-CNY and stablecoins: e-CNY is a centralized, sovereign digital currency, with all transaction records controlled by the People's Bank of China; while stablecoins (especially decentralized stablecoins) operate on global public blockchains and are not controlled by any single sovereign.

This difference dictates that the two are suited for different scenarios: e-CNY is suitable for the digital transformation of domestic payments; stablecoins excel in supranational scenarios such as cross-border payments, DeFi, and anonymous transactions. Domestic users use e-CNY to obtain sovereign backing; cross-border users and overseas enterprises still prefer USD stablecoins for international settlement. e-CNY and USD stablecoins will not directly compete in the short term: the former's main battlefield is domestic payments, while the latter is cross-border; each guards its own territory, and direct competition has not yet begun.

8.3 The Formation of a Multipolar Monetary Order

The current stablecoin market landscape foreshadows the formation of a multipolar monetary order: no longer dominated by a single currency, but rather with USD stablecoins, EUR stablecoins, gold stablecoins, and CBDCs from various countries competing and coexisting in different scenarios.

This diversification is not a fragmentation of the monetary system, but rather a layered specialization: users can choose the most suitable currency form according to their usage scenarios, using USDT for cross-border payments, DAI for DeFi yield strategies, PAXG for value storage, and their local CBDC for domestic consumption.

The future monetary system will be a multi-layered monetary network composed of stablecoins, CBDCs, and traditional currencies, much like the layered architecture of internet protocols. Each layer will serve a different purpose and together support the global digital economy.

The interplay between US dollar stablecoins and central bank digital currencies will reshape the geopolitical landscape of the "global banking account."

IX. Future Outlook: The Birth of Global Bank Accounts

Monetary history is at a rare turning point. Over the next 5 to 10 years, the following trends will profoundly reshape the global financial system.

9.1 Stablecoins are experiencing the "Internet era"

In the early 1990s, the internet was seen by most as a geek toy and a laboratory for a select few. By the early 2000s, it had begun to reshape business models; by the 2010s, it had completely transformed media, retail, and social networking; and today, it is an indispensable infrastructure for the economy.

Stablecoins are experiencing a similar "internet moment": from experimentation in the geek community to a necessity in emerging markets, to accelerated institutional adoption, and finally to the establishment of regulatory frameworks. Stablecoins will grow into the infrastructure of global finance, rather than a peripheral supplement.

9.2 Interest-bearing stablecoins are becoming the next generation of savings accounts.

"Interest-bearing stablecoins" are one of the most important innovative directions in the current stablecoin market. These stablecoins maintain a 1:1 peg to the US dollar while investing reserve assets in US Treasury bonds or other low-risk assets, and automatically distribute the returns to holders.

Take Ondo's USDY as an example: holders automatically accumulate approximately 5% annualized government bond yield daily, requiring no action. For the first time, users in developing countries can obtain the same savings returns as US investors without relying on local banks. Emerging market residents gain a prototype of a "global savings account"; institutions gain a compliant tool for on-chain cash management. Interest-bearing stablecoins are likely to reshape the savings logic of emerging markets, becoming one of the most important monetary experiments of the 2020s.

Prediction: By 2030, the market capitalization of interest-bearing stablecoins may exceed $500 billion, becoming the world's largest cross-border savings instrument and providing hundreds of millions of residents in emerging markets with low-risk returns previously only available to institutional investors.

9.3 AI needs currency, and stablecoins are a natural choice for the AI economy.

The narrative that AI agents need to autonomously conduct financial transactions (pay for services, receive income, and manage funds) is emerging, making stablecoins the natural currency of the AI economy.

Imagine an autonomous AI agent that can automatically pay cloud computing services using USDC, receive user fees, deposit idle funds into DeFi protocols to earn returns, and automatically redeem them when needed. The entire process requires no human intervention, no bank account, and no human endorsement, because AI has no legal entity status and cannot open a bank account, but it can have a crypto wallet.

This scenario is not science fiction. Coinbase has already launched a wallet product specifically for AI agents, and multiple AI startups are building stablecoin infrastructure for the "AI economy." Once the AI economy scales up, stablecoins may become the sole form of currency for its operation.

AI needs currency, but AI cannot open bank accounts. Stablecoins are the first type of currency that AI can use autonomously.

Diversified anchoring, CBDC specialization, and the AI economy represent the next stage of the "global banking account." Whether these visions can be realized depends on the finalization of the regulatory framework, improved reserve transparency, and the continuous management of de-anchoring risks.

Conclusion

Returning to the Argentine designer mentioned at the beginning of the article, he wasn't conducting encryption experiments or speculating, nor was he driven by technological passion. He was simply using the most rational approach to solve a real problem: how to securely, quickly, and cost-effectively complete an international transaction in an environment of peso collapse.

His choice is the choice that hundreds of millions of people around the world are making. This is not a revolution, not a subversion, but a quiet and irreversible market evolution.

The true significance of stablecoins lies not in technological innovation itself, but in the fact that, for the first time, every person on Earth, whether in Buenos Aires or Lagos, whether freelancer or assembly line worker, has the opportunity to have a globally usable, instant-settlement, programmable, and yield-generating bank account—a global financial gateway that requires no institutional permission.

Stablecoins are not a replacement for banks, but rather a reinterpretation of the question of "who can open a bank account".

Looking to the future, we must also acknowledge the risks and uncertainties. Whether stablecoin issuers can meet large-scale redemption demands under extreme liquidity pressure remains to be fully tested; the reserves of USDT and USDC are highly concentrated in a few banks and government bonds, and the collapse of a single institution could trigger a chain reaction; regulatory paths differ significantly across countries, and issues of applicable law and regulatory arbitrage during cross-border flows remain unresolved. Acknowledging these uncertainties does not negate the potential of stablecoins, but rather makes our conclusions more balanced.

This is a world in the making. And it is not born with a declaration, but through the silent accumulation of every stablecoin transaction.

Readers may pay attention to the regulatory progress of stablecoins in various countries, distinguish between compliant and gray market products, and pay attention to the transparency of issuer reserves; the above does not constitute investment advice.

--end--

In-depth column · 2026

Data source for this article

Reports: TRM Labs (Stablecoin Scale Report) 2026; Chainalysis (Cryptocurrency Geography Report 2025) (Crypto Report 2025); CCData (Stablecoin & CBDC Report) December 2025; World Bank (Remittance Prices Global Database), Remittance Prices Worldwide; Visa Research

Data: DeFiLlama, CoinGecko, rwa.xyz

Regulatory bodies: BIS Bulletin No. 73, CPMI-IOSCO (Guidelines on Stablecoin Arrangements) 2022

Market capitalization, TVL, and liquidation volume are for 2025; the $35 trillion on-chain liquidation volume is based on TRM Labs' 2026 report. Please refer to the latest reports from each institution for specific figures.