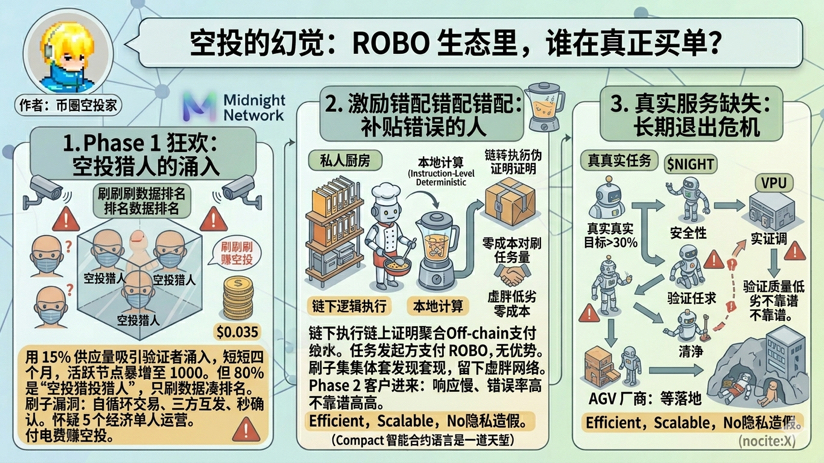

The airdrop design of Fabric Phase 1 is nothing short of genius—attracting global validators with 15% of the supply, in just four months, active VPU nodes surged from less than 500 to 1000. However, when I mingled in the testnet community, I discovered a harsh reality: 80% of the nodes are "airdrop hunters"; they don't care about task quality, don't invest real computing power, and just brush data to rank up.

This raises a fundamental question: what exactly is @Fabric rewarding?

The white paper states that airdrops are allocated based on "on-chain contributions," but the contribution criteria are the task volume and staking time. Bots quickly found a loophole: self-circulating transactions—three validators sending packets to each other, one confirmation per second, task volume skyrocketing, zero cost. In the testnet's 23 sub-economies, 15 are single-operated; I suspect this is the kind of "task brushing" game. Their only costs are electricity (about $2.2 per month) and time, expecting an average airdrop of $175 (based on 15% supply, $0.035 price, covering 30% of nodes estimated).

At the end of Phase 1, these opportunists will cash out collectively, leaving behind a network with inflated task volumes and poor verification quality. When real customers enter Phase 2, they find slow responses, high error rates, and unreliable nodes, and they turn away. Where is the demand for a network that no one uses, $ROBO ?

Ironically, the real robot owners—those vendors who want to use Fabric to solve practical problems—have become outsiders. They need stable and reliable verification services, but the prosperity of Phase 1 cannot mask the void of Phase 2. I asked two AGV vendors, and their exact words were: "Once you launch Phase 2, we will consider integration; now is not the right time."

This means that Fabric is using airdrops to subsidize the wrong people: the opportunists gain short-term benefits and exit in the long term; those who truly need the service watch coldly. It's like using public funds to treat everyone to dinner, while only freeloaders attend, and the main guests are absent.

I calculated a figure: if Phase 2 wants to maintain the number of nodes from Phase 1, it needs to pay validators at least $50/person per month (based on hardware costs and opportunity costs). Assuming 1000 nodes, that's $50,000 per month, or $600,000 per year. If the income generated from the network's real task volume is less than this amount, nodes will inevitably drop out. Currently, the test network's task volume is only growing by 30% per month, and estimating based on 80% low-value data labeling tasks, annual revenue may be less than $200,000—insufficient to pay salaries.

The price of ROBO is currently supported by airdrop expectations rather than real demand. Once the airdrop ends, the price drops from $0.035 to $0.01, and the opportunists have earned enough to exit, while real task providers find that ROBO income cannot cover costs, and they exit too. The network effect has never reached its tipping point, instead falling into a death spiral of "high inflation → sell pressure → price drop → validators exit → network shrinkage."

The Helium network is a cautionary tale: in 2021, Hotspot miners surged, but coverage quality declined. When IoT applications arrived in 2022, they found the network unreliable, leading to customer loss, and the token price fell from $55 to $2. Helium spent two years rebuilding its reputation; will Fabric repeat the same mistakes?

I see three key signals: 1. Within three months after Phase 1 ends, will the number of validators be halved? 2. After Phase 2 launches, will real task volume (non-circular) grow by >20% per month? 3. Will ROBO on-chain transactions shift from airdrop expectations to task fee payments? If the first two are not met, Phase 2 will be a bubble-bursting ceremony.

@Fabric Foundation 's original intention may have been good—to incentivize early participants with tokens. However, misaligned incentives lead to resource misallocation. When airdrop value far exceeds service value, the rational choice is to complete tasks rather than build an ecosystem. This is not the original sin of Web3; it is a common trap of leveraging short-term subsidies for long-term growth. When the subsidies stop, will the ecosystem still exist?

So don't be blinded by airdrops. The future of #ROBO is not in the frenzy of Phase 1, but in the retention rate of Phase 2. If the proportion of real tasks does not exceed 50%, and the top 10 validators' staking proportion falls below 30%, this network is just a meticulously designed Ponzi scheme. Everyone is an actor, and only time will reveal the outcome.