The Fabric white paper describes ROBO as "the water, electricity, and coal of the machine economy," but it never explains where this "water, electricity, and coal" cycle starts and ends.

Assume a typical scenario: A robot completes a quality inspection task and earns 10 ROBO as a reward. It needs to pay 3 ROBO to the verification node (30% fee rate), then it might spend another 2 ROBO to purchase a skill upgrade, leaving 5 $ROBO deposited in the wallet. If these 5 ROBO are not spent, they are dormant assets. If the robot wants to withdraw to fiat currency, it needs to sell ROBO on a CEX — the act of selling itself consumes liquidity: where do the buy orders come from?

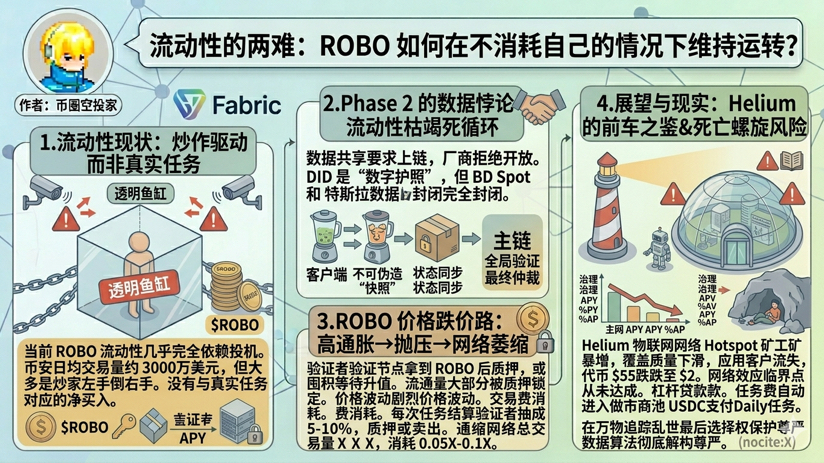

Currently, the liquidity of #ROBO almost entirely depends on speculative trading. After Binance went live, the daily trading volume was about $30 million, but most of this money was just traders passing it back and forth without corresponding net buys related to real tasks. When robot owners sell ROBO for fiat to pay for electricity and hardware loans, there must be new buyers to take over, or the system cannot sustain itself.

The airdrop in Phase 1 created a lot of "pseudo liquidity": validators immediately staked the ROBO they received or hoarded it in anticipation of appreciation, rather than using it genuinely. When the real scenarios of Phase 2 arrive, robot owners will need to frequently pay with ROBO, but a large portion of the circulating supply is locked in staking, leading to insufficient tradable balances and causing severe price volatility, with prices rising when buying and dropping when selling, resulting in unstable actual income.

A deeper contradiction lies in the fact that transaction fees consume ROBO itself. For each task settlement, validators take a cut of 5-10%, which means this portion of ROBO is either staked or sold, removing it from circulation. If the total network transaction volume is X ROBO/month, the net consumption is about 0.05X-0.1X (not considering new staking). This means the total circulating supply of ROBO will slowly deflate unless there is continuous new inflow (new users buying, airdrops, team releases).

I saw a data point: the task volume on the test network increases by 30% monthly, but only 30% of the validator's income comes from task fees, while 70% relies on airdrop expectations. After Phase 1 ends, if airdrops dry up, validators relying solely on task fees will see their income drop by 70%. They will either withdraw their tokens and leave, or significantly raise the fees, which will reduce the net profit for robot owners, creating a vicious cycle.

In comparison to Render Network: rendering clients pay for tasks with fiat, and Renderers receive RNDR (which is redeemable), but RNDR also incurs transaction fee consumption. Render's solution is to continuously attract new rendering demand, bringing in new buyers. The problem with Fabric is that robot task demand is infrequent and irregular, unlike rendering, which has a continuous content production demand, making the source of buyers unstable.

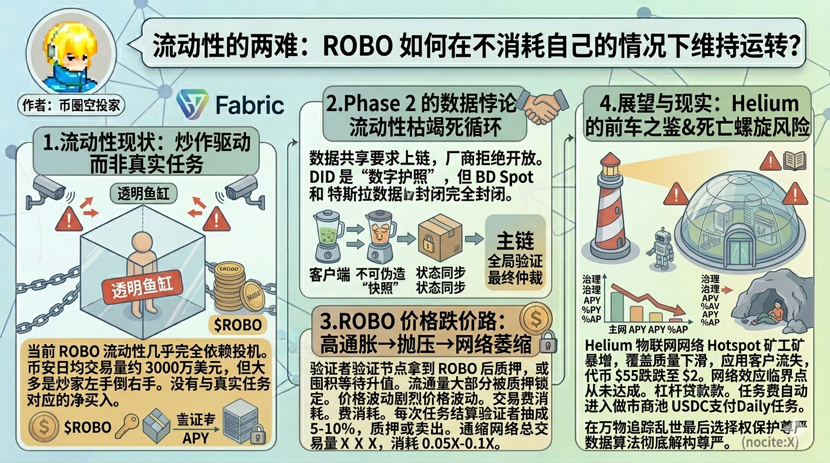

There is also an invisible problem: ROBO is being used as collateral. If robot owners stake ROBO to obtain loans, which are then used to pay for task fees, this creates a leverage cycle. However, ROBO's price is highly volatile, and when the value of collateral declines, it triggers liquidation, leading to more ROBO flooding the market and the price dropping even more—this is a typical DeFi death spiral.

@Fabric Foundation should design a "liquidity cycle" mechanism: for example, a portion of the task fees automatically enters a market maker pool to provide buy-sell depth; or introduce stablecoin settlement options, with ROBO used only as governance and staking tokens, while daily tasks are paid in USDC. But the white paper lacks these designs.

I see three danger signals: 1. Staking accounts for >80% of ROBO's circulating supply 2. Continuous outflow of CEX deposits (withdrawals to cold wallets) 3. ROBO's proportion in task fee payments is <20%. If all three signals appear simultaneously when Phase 2 starts, it indicates that the liquidity structure has failed.

ROBO attempts to play both roles of "store of value" (staking governance) and "medium of exchange" (task payment), but these two roles are inherently in conflict: as a store of value, people are reluctant to spend; as a medium of exchange, it needs to circulate frequently. When consumption (transaction fees, withdrawals) exceeds inflows (new demand, new buyers), liquidity exhaustion is just a matter of time. The prosperity of Phase 1 was bought with airdrop checks, and Phase 2 will test whether there are people willing to continuously pay for the utilities of the machine economy.