On March 24, 2026, the Hong Kong Monetary Authority officially issued the first batch of stablecoin issuer licenses to Sina.com. This day was awaited by the crypto industry for three years. Almost simultaneously, @Sign officials disclosed that the new measures in 2026 include the integration of banking stablecoin middleware, with traditional financial institutions needing compliant channels to connect on-chain liquidity.

The appearance of two signals in the same month may not be a coincidence.

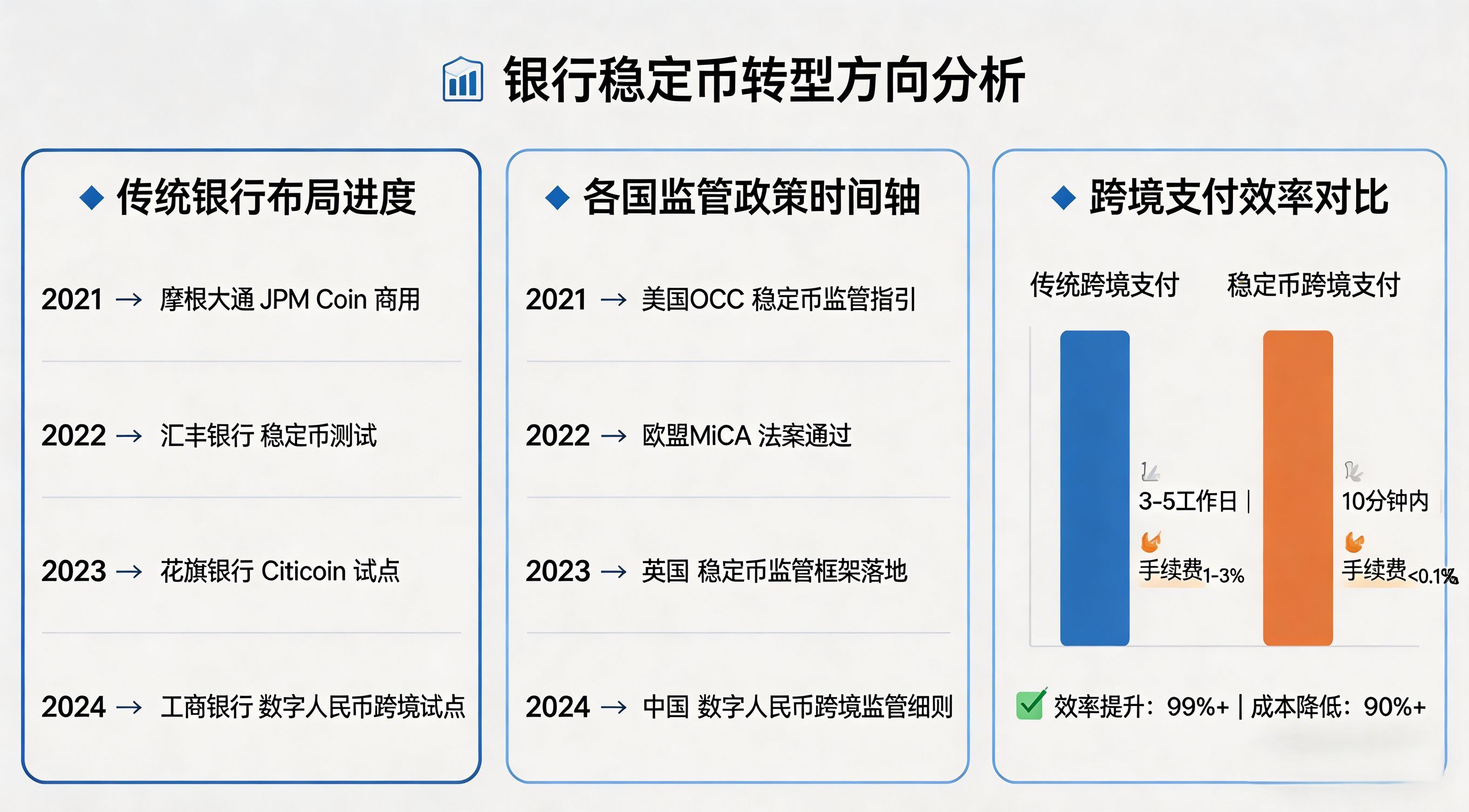

The timeline for banks to enter the market

When will traditional banks issue stablecoins on a large scale? A person involved in the license application revealed that among the first approved institutions, two are a joint venture of licensed banks and technology companies. This means that banks entering the market is not a question of 'whether' but 'how' to connect.

@Sign's verification layer perfectly addresses the challenge of "how to connect". Stablecoins issued by banks need to be used across chains, require compliance audits for tracking, and need on-chain certificate verification. This middleware does not require banks to restructure existing systems but adds a verifiable trust layer on top of the existing architecture.

Key window of 2026

Some analysts privately predict that in Q4 2026, 2-3 large commercial banks may announce on-chain integration projects. This pace is faster than the market expects. The United States (GENIUS Act) requires that stablecoin regulations be finalized by July 2026, and a clear regulatory framework is a prerequisite for institutional capital entry.

A compliance officer who participated in bank integration projects revealed that traditional cross-border payment audits typically require 7-14 working days, but this was shortened to less than 48 hours using the Sign verification layer. The cost of manual review has been reduced by about 65%.

Media reports and capital flows

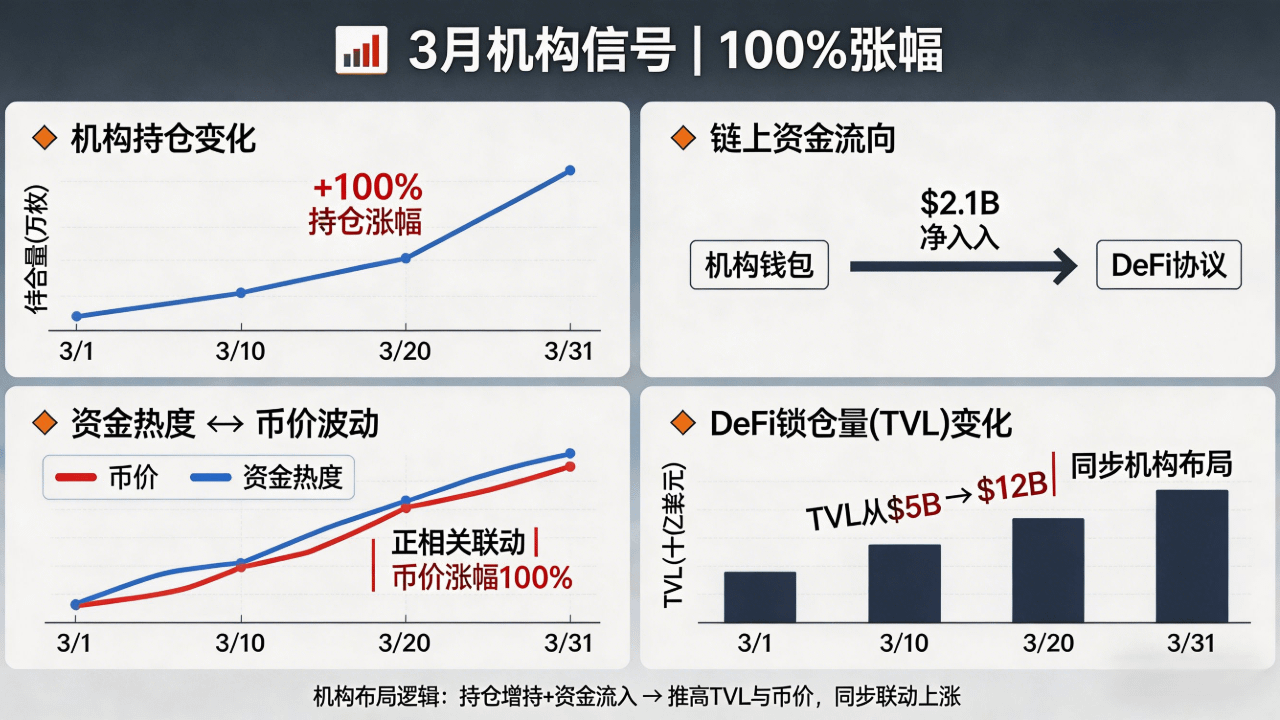

Chainwire reported on March 7 that SIGN surged over 100%, with its role in sovereign digital infrastructure being repriced by the market. Singaporean media reported a significant increase in institutional interest. A market maker revealed that after monitoring the price surge, on-chain transfer volumes noticeably decreased, indicating that early holders are actively reducing selling pressure expectations.

By 2026, the RWA tokenization market will surpass $25 billion, nearly quadrupling compared to a year ago. A clear compliance framework is a prerequisite for institutional capital entry.

Conclusion

The crypto industry has been shouting about "disrupting traditional finance" for so many years, but what is truly accepted are often those infrastructures willing to compromise and bridge. When banks start using on-chain proof, the large-scale entry of traditional finance may truly arrive. Some games never existed on the K-line, but rather in the signed bank contracts.