Instant funding is one of the fastest-growing models in prop trading right now. On the surface, it looks simple: skip the evaluation and start trading immediately with a funded account.

But from a trader’s perspective, the reality is more nuanced.

Here’s how it actually works and what most people underestimate.

Key Takeaways

Instant funding gives you immediate access to a funded account, with no multi-step challenge

You still trade under strict rules: drawdown limits, payout conditions, and restrictions

Getting access is easier but keeping the account is where most fail

You’re not removing difficulty, you’re shifting it to day one

What Instant Funding Really Means

In traditional prop trading, you typically go through a structured evaluation. That often means hitting profit targets (like 10% and then 5%) while respecting risk limits.

Instant funding removes that phase entirely.

You pay, you get access, and you start trading right away.

But here’s the important part:

You’re being evaluated from your very first trade.

There’s no warm-up phase. No buffer period. If you break the rules, the account is gone, just like that!

How Instant Funding Works in Practice

The process is usually straightforward:

Choose your account size

Pay the upfront fee

Get immediate access

Trade under predefined rules

Sounds simple and it is.

But the real challenge starts once you’re inside.

Let’s take a realistic scenario:

Account size: $10,000

Max drawdown: 5% → $ 500

Two poorly sized trades can wipe that buffer quickly. For example:

Trade 1: - $ 300

Trade 2: -$250

You’re done.

This is why experienced traders don’t focus on account size first, they focus on the loss buffer.

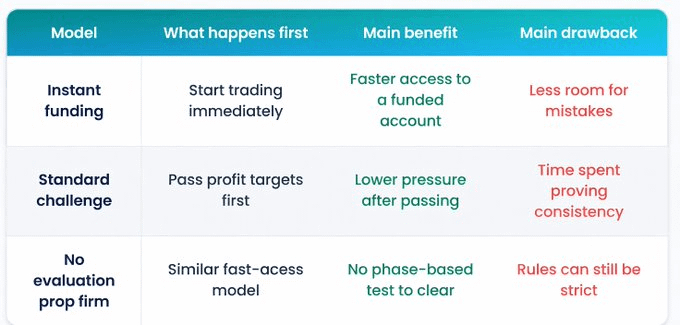

Instant Funding vs Challenge Models

A lot of traders ask whether instant funding is “easier” than a classic challenge.

That’s the wrong question.

The real difference is where the pressure sits.

Challenge model → pressure comes before funding

Instant funding → pressure starts immediately

Some traders prefer proving consistency first. Others prefer jumping straight into live conditions.

It’s mostly psychological.

There’s also the “no evaluation” model, which looks similar on the surface, but still comes with strict internal rules.

Instant Funding vs Challenge

Bottom line:

Every model has constraints. They’re just structured differently.

The Rules You Can’t Ignore

One of the biggest misconceptions is that instant funding comes with fewer restrictions.

In reality, risk controls are often just as strict—if not stricter.

The key rules usually include:

Maximum drawdown (static or trailing)

Daily loss limits

Payout conditions

Strategy restrictions (news trading, arbitrage, etc.)

Consistency requirements

Example:

$25,000 account

4% max drawdown → $1,000 total loss limit

If you risk 2% per trade, two losses can push you dangerously close to the limit.

This is where many traders fail not because of strategy, but because of sizing.

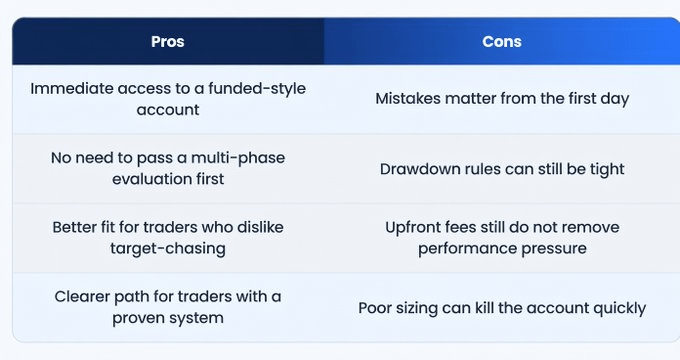

Pros and Cons of Instant Funded Accounts

Instant funding solves one problem very well: time.

You don’t need to spend weeks or months passing a challenge.

But it introduces a different kind of pressure.

Advantages:

Immediate access to a funded-style account

No need to pass multi-phase evaluations

Good fit for traders with a proven system

No target-chasing pressure

Limitations:

Mistakes are punished immediately

Tight drawdown rules leave little room for error

Upfront cost doesn’t remove performance pressure

Poor risk management can end the account quickly

👇Here’s how it actually compares in practice:

The key difference comes down to one thing: where the pressure sits. And that single factor changes how most traders perform.

How to Compare Instant Funding Prop Firms

If you’re evaluating different prop firms, don’t start with the price.

Start with survivability.

A cheaper account with aggressive rules can cost you more in the long run than a slightly more expensive one with realistic conditions.

Here’s what I personally look at first:

Drawdown type (static vs trailing)

Payout structure and frequency

Consistency rules

Strategy restrictions

Scaling potential

For example, a trailing drawdown can behave very differently from a fixed one it can tighten your margin over time if you’re not careful.

Some traders prefer platforms that align better with their execution style. I personally pay close attention to how flexible the risk model is before committing to any account.

🔽 Platforms & Discount

Some prop firms are structured differently, and Mubite is one of the platforms that stands out in the instant funding space.

From a user perspective, the setup feels very crypto-native and smooth to navigate, especially compared to more traditional models. The access to a wide range of trading pairs also gives more flexibility depending on your strategy.

That said, the platform itself is never the edge - risk management is.

If you're exploring options, some platforms occasionally offer discounts.

Use code: CRYPTOJOBS (20% off when available)

More details in my bio 💎

Final Thought

Instant funding doesn’t make trading easier.

It simply removes the initial barrier.

The real challenge doesn’t change:

discipline, risk control, and consistency.

If your risk management is solid, the model can work.

If not, the outcome is always the same - the account won’t last.

Source: MUBITE MEDIA