High-demand assets can achieve continuous settlement, collateralization, and network effects. The programmability of the dollar and bonds reduces financial friction, and trillions of dollars have already been flowing within it.

Author's viewpoint: Ripio founder and CEO Sebastián Serrano

For most of the past decade, the crypto industry has been trying to tokenize niche assets to reshape finance. Although this idea is quite creative, it largely overlooks the core economic logic that truly creates value through tokenization.

In the early stages of blockchain adoption, the most effective applications of tokenization were not at the economic margins, but at its center. The industry's initial intuition—to tokenize illiquid assets—was a misjudgment. The most successful attempts at tokenization involved the most liquid assets in the world, specifically the US dollar in the form of stablecoins.

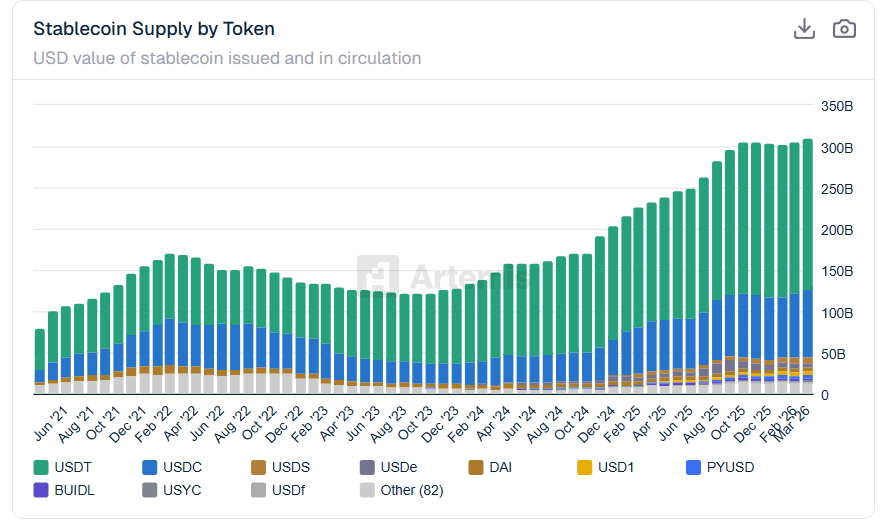

The supply of stablecoins continues to rise. Source: Artemis

The supply of stablecoins continues to rise. Source: Artemis

Today, companies are piloting tokenized versions of treasury bills, smaller currencies, and an increasing number of stocks as other highly liquid assets. This is not a coincidence. Tokenization is most powerful when applied to assets that already have huge demand and possess standardized legal and financial frameworks. Liquidity is the prerequisite for tokenization to transition from a novel concept to infrastructure.

Tokenization of the assets people truly want

Tokenization should start with assets that already have high demand. Currencies, sovereign debt, and major financial instruments are the foundational layer of the global economy. Governments, businesses, and individuals use them every day. Tokenizing these assets does not create demand from scratch, but upgrades the track on which trillions of dollars have already flowed.

A look back at modern history shows that electricity was clearly not initially used to power fancy artistic installations, but factories. The same is true for blockchain. They can only realize their potential when tokenizing currencies and core financial primitives, not marginal assets.

Stablecoins have achieved success. They directly correspond to existing and large-scale application scenarios. Stablecoins can transfer US dollars globally quickly and at low cost. Tokenized government bonds are also gaining attention for the same reason. They represent real high-demand assets that institutions already hold on a large scale.

Tokenization creates the most value in areas where friction is high and costs are substantial. Bonds circulate trillions of dollars annually, but the efficiency is not high. Tokenization can compress settlement cycles from days to minutes. Tokenization also allows assets and cash to flow in real time without relying on intermediaries. This changes the cost structure and risk profile of financial operations.

Network effects will only emerge around highly demanded assets such as currencies and sovereign debt. Once tokenized, interoperability can be achieved immediately. Everyone can build around the same unit of account. This is also why stablecoins have become a pillar of on-chain finance.

NFTs and highly customized RWAs are exactly the opposite. They are inherently fragmented by design. Each asset is unique, legally ambiguous, and difficult to standardize. This prevents them from becoming a shared economic layer. They may have cultural or speculative value, but cannot support widespread financial network effects.

Market effects of tokenizing liquid assets

Adding programmability to illiquid assets can enable ownership fragmentation or automate certain workflows. But this does not unlock new forms of economic synergy. The asset still trades infrequently and still lacks depth in the market.

For liquid assets, tokenization can unlock entirely new financial behaviors. Continuous settlement, streaming payments, automated collateral management. These are just some of the new changes that tokenization can bring.

There are other considerations. Can a certain tokenized asset be used as collateral? This is an important question, and the answer largely depends on liquidity. After all, liquid assets can be safely integrated into automated systems as collateral. Their valuations are transparent and can be updated in real time.

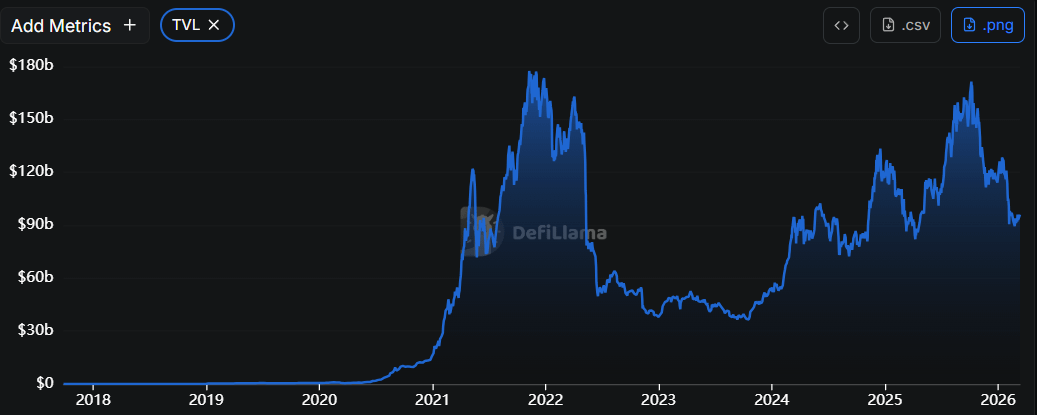

Approximately $96 billion of liquid assets are locked and used in various DeFi protocols. Source: DefiLlama

Approximately $96 billion of liquid assets are locked and used in various DeFi protocols. Source: DefiLlama

However, trading illiquid assets is sporadic, valuations are subjective, and the bid-ask spreads are typically large. Their characteristics make them difficult to use as collateral. Tokenization does not solve this problem. This will reduce market demand for the asset.

For liquid assets, capital efficiency will also significantly improve. Tokenized liquid instruments can potentially be re-staked, proportionally deployed, and programmatically allocated in real time. Capital moves faster within the system. But tokenization does not bring a sustainable market for illiquid assets.

Reducing risk through clarity

US dollars, government bonds, and large corporate debts have mature legal standing, issuer responsibilities, and regulatory frameworks. Tokenization can be embedded within existing financial legal systems, making it much easier for institutions to adopt.

NFTs are more challenging. Issues surrounding ownership, custody, enforceability, and investor protection may overshadow the technological advantages. In practice, these uncertainties increase risk rather than decrease it. It is a natural choice for large institutional tokenization projects to prioritize liquid assets.

The future of tokenization will be defined by assets that are economically central. Clearly, the early attempts at NFTs in the crypto industry were necessary and understandable. NFTs are difficult to achieve long-term success because they focus on the wrong type of assets.

Stablecoins have proven this by upgrading the world's most liquid assets. Tokenizing government bonds and stocks is the logical next step. This is the path for blockchain to evolve from experimental technology to foundational financial infrastructure.