The cold winter wind sweeps through every corner of the crypto market, the trading dust of the first quarter of 2026 has settled, all the noise and traffic bubbles have been stripped away by the chill, and the research report from CoinGlass lays bare the most naked trading data in the industry, along with the most genuine survival cards.

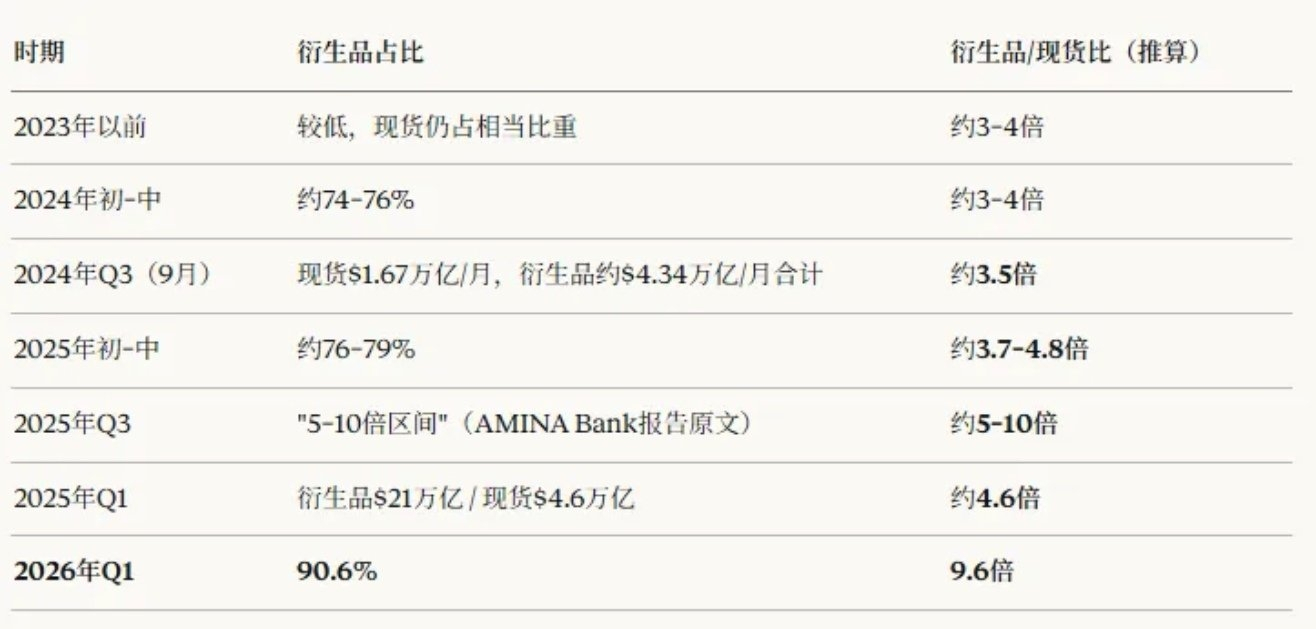

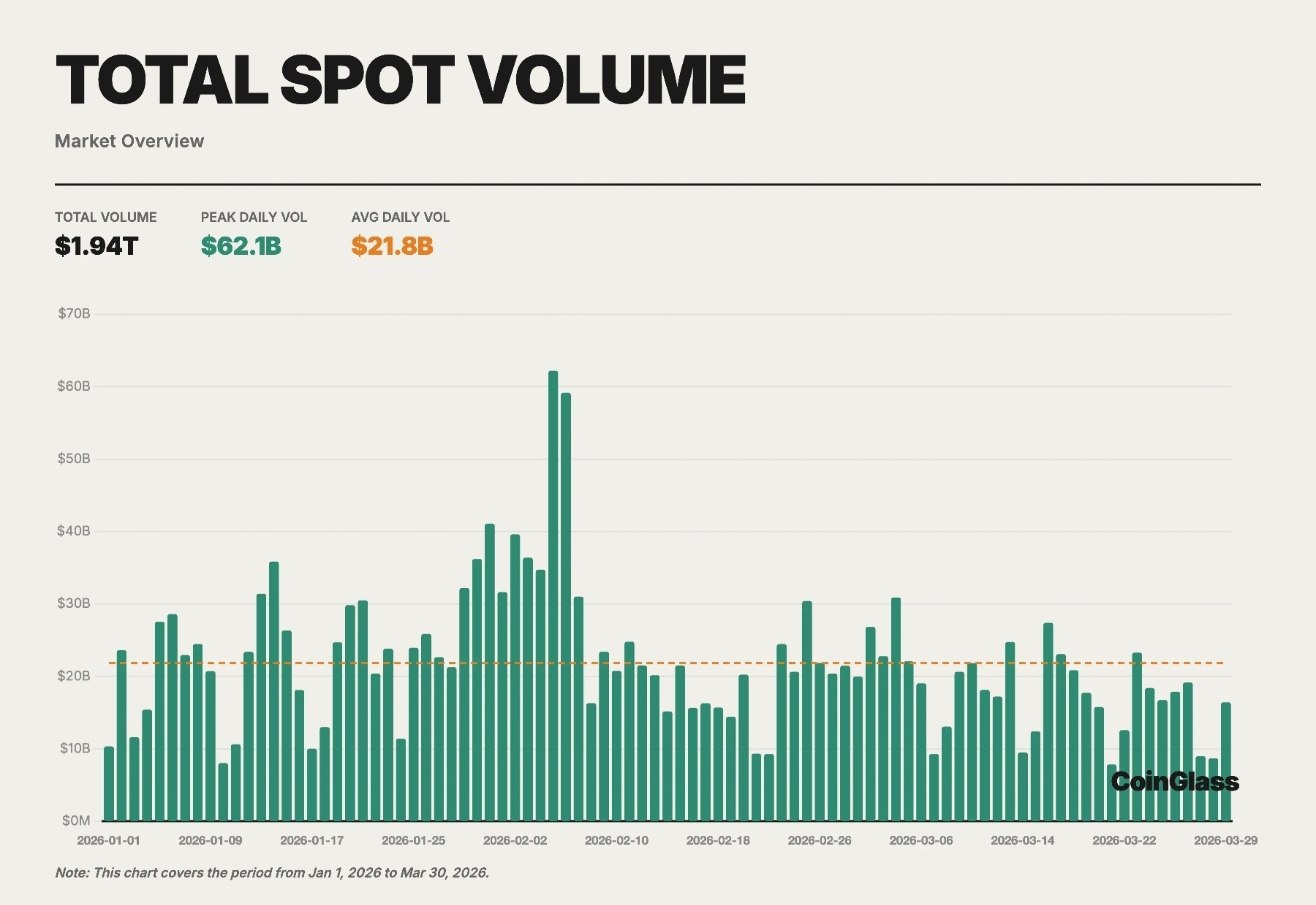

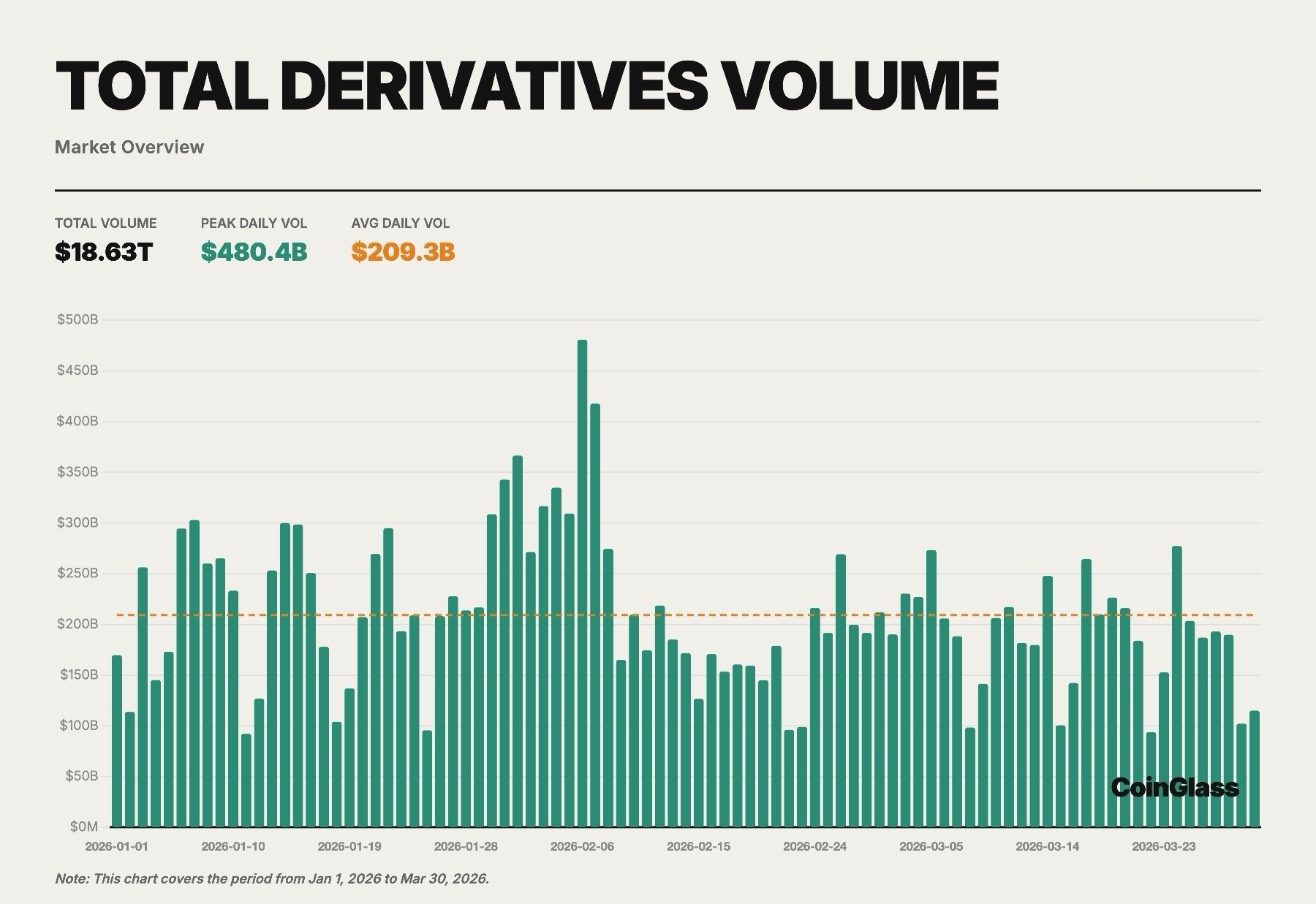

The total trading volume of the entire market in the first quarter is fixed at 20.57 trillion USD. This figure seems enormous, yet it has dropped by 20% compared to the same period in 2025, with an overall market contraction reaching 23%. More thought-provoking than the contraction is the deep distortion of the market trading structure—18.63 trillion USD in derivatives trading corresponds to only 1.94 trillion USD in spot transactions, with a staggering ratio of derivatives to spot reaching 9.6 times. This means that in every 10 yuan traded in the market, less than 1 yuan is actual token trading, with the remaining over 9 yuan all being contracts, perpetuals, and futures speculation. It is worth noting that just a year ago, this ratio was only 4.6.

Those willing to invest real money in spot trading and hold coins long-term have dropped to historically low levels. In the bear market, spot trading has lost its wealth creation effect. Those who remain in the market are mostly using contracts to manage positions, hedge risks, and engage in short-term speculation. This market is no longer an era of comprehensive expansion driven by new funds but rather a stock game operating around leverage, hedging, and short-term trading in a relatively cautious environment.

It is precisely in such a winter that the Matthew effect in the market is amplified to the extreme. The more sluggish the market, the more funds and traders naturally concentrate on platforms with deeper liquidity, stronger execution capabilities, and more stable capital accumulation. The siphoning of liquidity and user assets by top platforms has almost become an irreversible trend.

In CoinGlass's report, Binance has firmly established its position as the absolute leader in the industry with fragmented data. It is the only platform in the entire industry that ranks first in four core dimensions: derivatives trading volume, average positions, order book depth, and user asset accumulation. In the first quarter, its derivatives trading volume was approximately $4.90 trillion, with a market share of about 34.9% under the Top 10 metric, an average position size of approximately $23.9 billion, and user asset accumulation reaching $152.9 billion, accounting for as much as 73.5% of the total user assets in the industry CEX. More notably, during the market's contraction, its market share has instead increased, with spot share rising from 34% to 35.4%, and derivatives share increasing from 33.2% to 35.7%. The depth of liquidity and user asset reserves have created a chasmic gap with the players behind it.

Many people are dazzled by the trading volume of exchanges, forgetting that trading volume can be propped up by short-term activities and market-making strategies. Only the long-term presence of funds truly reflects user stickiness and real trust. This point is never a lie according to on-chain data. Glassnode's on-chain monitoring shows that Binance's USDT reserves increased during the transition between bull and bear markets, rising from a low of $24.6 billion to $43.8 billion. Even though there was a temporary decline in the first quarter of 2026, it quickly returned to an upward trend; BTC reserves have been even more stable, only experiencing a sudden drop once in the past five years during the 2022 FTX crisis, after which they continued to recover, stabilizing above 550,000 coins in the long term.

The reserve assets of exchanges represent the users' real money. Even after experiencing rounds of public opinion storms, users still ultimately cast the most honest trust votes with their own funds.

Beneath the leaders, the market's hierarchical structure has become nearly solidified. OKX firmly holds the second position in the industry, being the closest challenger to Binance among all centralized platforms, especially in the derivatives battlefield, with a derivatives trading volume of $2.19 trillion in the first quarter. Although there is still a significant gap with the leader, it has firmly maintained the second position and is the only player in the industry capable of competing with the leader in BTC and ETH contract depth. Following it, Bybit, Gate, and Bitget rank in the top five, among which Bitget is no longer a player that relies on short-term traffic and single hotspots to stay at the table. Instead, it has completed a critical transition from a growth-type platform to a stable-type platform, securing its footing in the industry's reshuffle.

Players in the mid and tail segments are facing a squeeze from both ends in this winter. The emergence of on-chain derivatives DEXs like HyperliquidX has led many to see on-chain DEXs as zero-sum opponents to top CEXs, believing that one rises as the other falls. However, real market data tells us that even if on-chain derivatives platforms break into the top ten in trading volume, the market share they truly capture is never from top CEXs, but from the market shares of smaller exchanges ranked 5 to 10.

DEXs continuously engage in internal competition in the on-chain world, using innovation and a geek spirit to undermine the survival space of small to medium centralized exchanges. However, the users and funds flowing out of these smaller platforms ultimately still flow continuously toward top CEXs. This is the most authentic ecological logic of the industry: DEXs are responsible for preserving the geek spirit and innovative vitality of the industry, continuously exploring boundaries in niche areas; while top CEXs are responsible for withstanding the impacts of traditional finance on the front lines and absorbing vast amounts of compliant capital. The two have never been mortal enemies but rather form an excellent ecological complement in this industry cycle.

Every time the market cools down, there are always voices claiming that the top platforms are failing. Yet with every real data release, we can see that liquidity is actually concentrating even more deeply towards the leaders. A bear market is never a carnival that disrupts the landscape but a touchstone that washes away the superficial. It strips away all short-term traffic and noise, leaving only the most hardcore survival capabilities—it's not about whose story is told louder, but about who truly possesses the ability to become the market's infrastructure, providing users with the most solid liquidity and the most reliable trust endorsement amidst the cyclical storms.

Winter will eventually pass, but the script of the cycle always writes the same ending: those who endure the bear market can welcome the true strong in the next bull market.#coinglass #BTC行情 #加密 $BTC