According to Reuters, with the mediation of Pakistan, the United States and Iran reached a two-week ceasefire agreement, temporarily halting a conflict that had already lasted six weeks. Both sides agreed to suspend attacks and to restore navigation through the Strait of Hormuz, under certain conditions. The agreement also received partial support from Israel, another country involved in the conflict.

According to Reuters, with the mediation of Pakistan, the United States and Iran reached a two-week ceasefire agreement, temporarily halting a conflict that had already lasted six weeks. Both sides agreed to suspend attacks and to restore navigation through the Strait of Hormuz, under certain conditions. The agreement also received partial support from Israel, another country involved in the conflict.

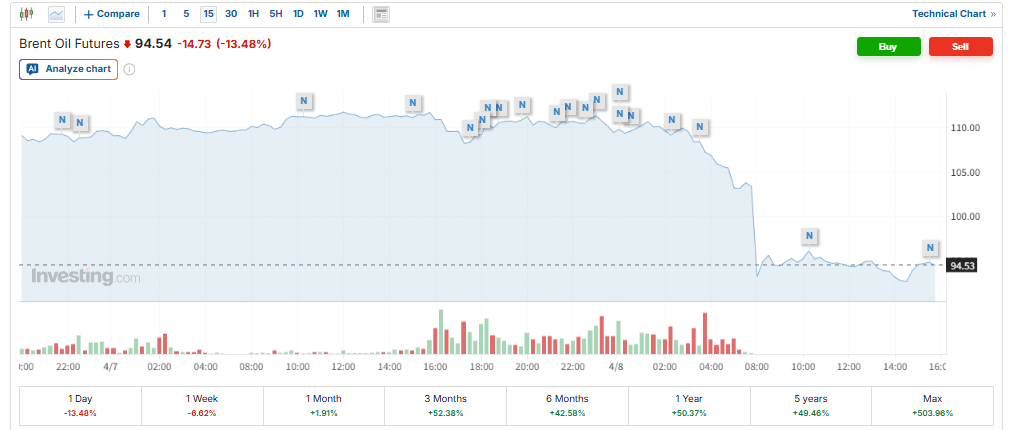

After the ceasefire, markets reacted strongly: Brent oil fell nearly 20% in a single day, while Asian stocks, gold, and cryptocurrency markets saw a broad recovery.

However, a ceasefire is not the same as peace. In subsequent negotiations, Iran proposed ten conditions as a basis for talks, including the central issue of the conflict: permission for uranium enrichment activities. This suggests that negotiations will be extremely challenging. The two-week ceasefire seems more like a "trust test," serving as a starting point for future agreements.

1. Divergent Conditions: Ceasefire as a Temporary Measure, Not as a Solution

Specifically, the ten conditions proposed by Iran include:

• Resumption of energy exports: easing or lifting restrictions on oil exports.

• Sanctions relief: particularly on financial and settlement systems.

• Unfreezing of assets: release of frozen funds abroad.

• Control over the Strait of Hormuz: maintaining influence or toll rights over the passage.

• Security guarantees: preventing future direct attacks by the US or its allies.

• Nuclear sovereignty: rejecting the total abandonment of nuclear capabilities.

• Regional influence: maintaining its strategic presence in the Middle East.

• Ceasefire is not definitive: rejecting temporary ceasefires as substitutes for long-term agreements.

• Equal negotiation framework: refusal of unilateral conditions.

• Long-term negotiation pathway: demanding a transition to prolonged negotiations.

Although President Donald Trump described these claims as a "viable basis for negotiation," many of them affect fundamental US interests, such as nuclear sovereignty and regional influence. Iran's priorities, in turn, focus on energy and sanctions relief. There is little convergence between the two sides that can be reconciled in the short term.

However, Israel has not fully adhered to the ceasefire. Prime Minister Benjamin Netanyahu stated that the ceasefire "does not include Lebanon" and continued attacks even after it took effect. Under these conditions, the ceasefire does not represent a resolution, but rather a temporary pause.

A more reasonable interpretation is that both sides need time to make the conflict more manageable: the US needs to deal with internal political pressure or prepare for new military actions, while Iran needs time to reorganize its administrative and operational capacity amid ongoing attacks.

In this context, two possible paths may emerge:

Scenario 1: Breach of the Ceasefire

If either side launches new attacks within two weeks — whether by miscalculation or strategic escalation — the conflict could quickly escalate again. Markets would readjust extreme risk prices, energy prices could rise again, and risk assets would face new pressure.

Scenario 2: Extension of the Ceasefire

If both sides expand the current framework and move towards deeper negotiations, the intensity of the conflict will significantly decrease. As long as tensions remain unresolved, markets will gradually shift from "war prices" to "negotiation prices."

Underlying issues remain unresolved, but the risk of losing control has been temporarily suppressed — enough to stabilize markets in the short term.

2. The US wins on the oil price issue.

Upon further analysis, the actual outcome of this conflict is not fully reflected in its declared objectives.

The US publicly emphasizes the need to contain Iran's nuclear capabilities, but this goal cannot be verified in the short term. What has substantially changed is the energy price structure.

Although global oil prices have retreated nearly 20% from their peak, to about $90, they remain significantly above the pre-war level of $70 — and, crucially, above the average breakeven cost of shale production in the US (approximately $60 to $70). This implies that Middle Eastern oil no longer has a clear price advantage over US production. At the same time, uncertainty in supply from the region has amplified. The US, which has ceased to be merely an energy importer, has become one of the beneficiaries of rising oil prices. This structural shift has developed over the last decade but has been significantly reinforced by the conflict.

This implies that Middle Eastern oil no longer has a clear price advantage over US production. At the same time, uncertainty in supply from the region has amplified. The US, which has ceased to be merely an energy importer, has become one of the beneficiaries of rising oil prices. This structural shift has developed over the last decade but has been significantly reinforced by the conflict.

Cost advantages in energy directly influence production decisions. The US has promoted the relocation of industrial production, and energy prices are a key variable. In a scenario of high but relatively stable oil prices, the US gains a more significant cost advantage compared to energy-dependent economies.

However, as the correlation between gold and the dollar weakens, the conflict has reinforced the dollar's role in energy pricing. This redirected demand for dollars back to the energy system, temporarily slowing the erosion of dollar dominance.

In this sense, the true “outcome” of the conflict may not be in military terms, but rather in structural and price changes.

3. The Era of Inflation and the Instrumentalization of Natural Resources

If gains are reflected in energy prices, costs will first be reflected in inflation.

The rise in energy prices directly transmits to the transportation, manufacturing, and consumption sectors. Although this transmission occurs with some lag, the path is clear. The next US CPI report will serve as the first important window to observe the indirect effects of the conflict.

With negotiations underway, the Federal Reserve is expected to maintain some flexibility between its two mandates: employment and inflation. It may keep interest rates unchanged in the short term, temporarily ignoring inflationary pressures driven by the energy sector. However, if inflation surprises positively, the Fed will face tougher policy choices.

At the same time, the fact that this conflict has ended in negotiations highlights the deterrent power of "resource instrumentalization." Iran used its control over the Strait of Hormuz to force concessions from the US, a dynamic that could become a recurring risk in future geopolitical conflicts.

From ports and shipping routes to mineral resources and energy centers — and even undersea cables and pipelines — there are many bottlenecks worldwide similar to the Strait of Hormuz. Even without a total blockade, the mere presence of risk is enough to increase transportation costs.

From a regional perspective, competition among major powers for resources is likely to intensify in Asia, Africa, and Latin America. In terms of political risk in resource-producing regions, the Americas and the Middle East top the list, followed by Australia and Europe, while Africa — emerging as a crucial battleground — may present a significant increase in political risk in the future.

This trend is likely to become increasingly evident in global supply chains and trading systems in the future.