Polymarket has recently officially announced the launch of its native stablecoin PolyUSD, extending its income structure and asset system to its own liquidity medium. Although PolyUSD has not officially launched yet, Predict.fun has already triggered a seismic shift in the industry due to its 'dynamic patch' for the event judgment rules.

In response to the news that Polymarket is about to launch PolyUSD, Predict.fun has supplemented information on the following two markets:

Will Polymarket launch a token by [Date]? (Will Polymarket issue a token by a specific date?)

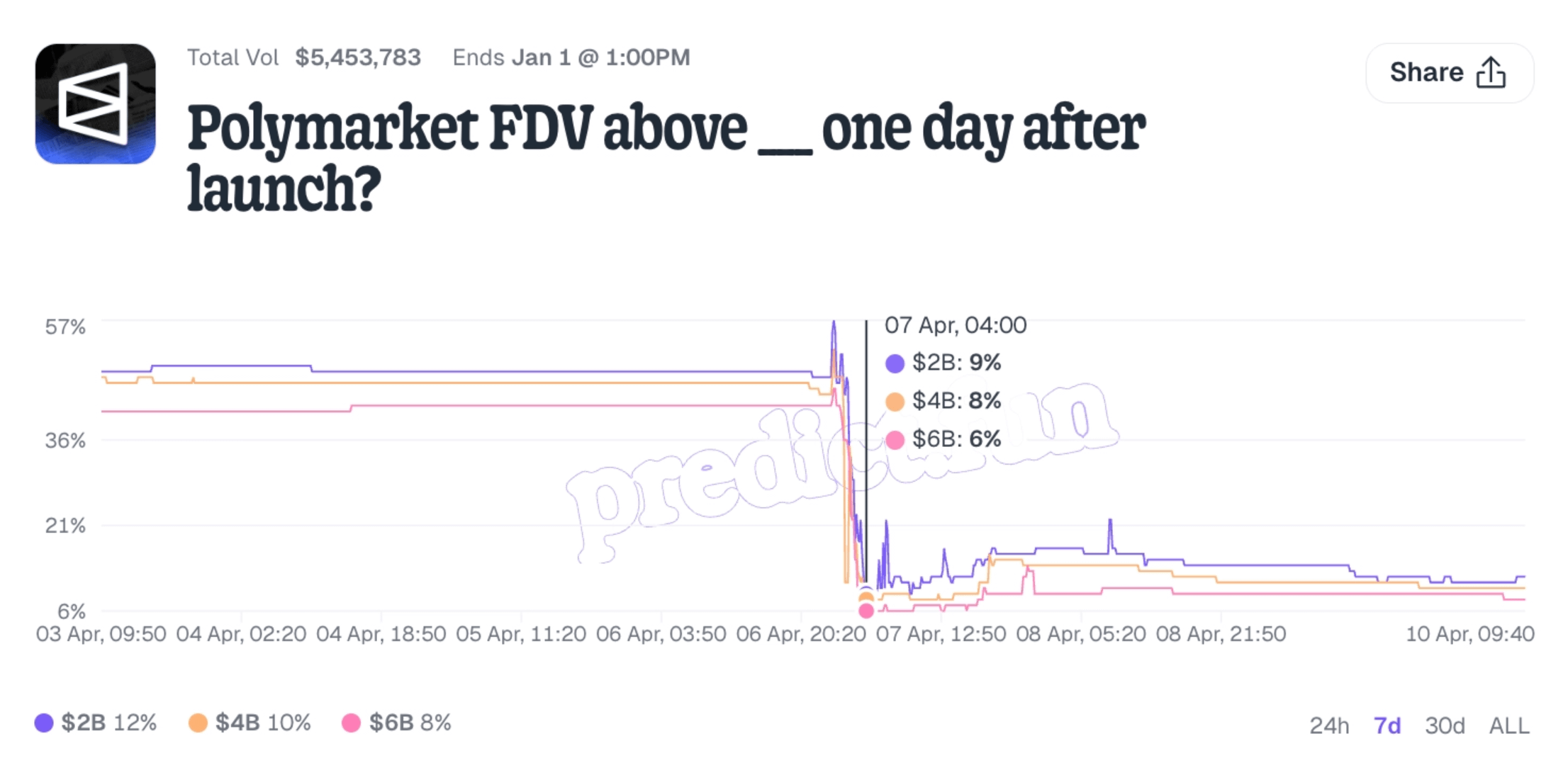

Polymarket FDV above [Amount] one day after launch? (Will the FDV on the first day of token issuance exceed the specified amount?)

Predict.fun explicitly states in the "Additional Information" section of the above market that PolyUSD can also be counted within the scope of "Token" determination. This logical correction directly rewrites traders' universal expectations regarding "Governance Token," leading to a dramatic fluctuation in the probability chart, and Predict.fun has thus fallen into a severe trust crisis of "determination manipulation."

I. From the title to determination, how Predict.fun led the problem astray

In prediction markets, the "interpretation rights" of the rules often determine success or failure more than the "predictions themselves." By deconstructing Predict.fun's original determination standards and its subsequent supplementary "patches," we can clearly see an evolution from semantic consensus to logical traps.

1. Original contract: the "implicit consensus" between title and rules

Before additional information was provided, the corresponding logic between the market title and the determination criteria is as follows:

Market Title: Polymarket FDV above ___ one day after launch?

Original standard key points:

Determination target: "Polymarket's token"

Calculation formula: FDV = Total Token Supply × Token Price (Total Supply × Price)

Asset requirements: must be publicly tradable, fungible tokens (such as ERC-20)

The most critical word in the title is not token, but FDV. Once it enters the FDV context, it naturally corresponds to the market narrative chain of "issuance—pricing—valuation"; at this time, it is discussing: where the valuation of the token with true issuance significance on Polymarket will fall one day after its launch. In the cryptocurrency market, only assets with premium space and price discovery functions will use "FDV" to measure their market valuation.

This is also why, when the vast majority of users see this title, they will first think of platform tokens, governance tokens, core tokens, and similar objects, rather than a purely collateral or settlement tool asset.

In other words, between the title and the original rules, there was originally an implicit consensus:

This discussion concerns Polymarket's "token valuation" rather than "what qualifying assets Polymarket will issue first."

2. Rule loopholes: the "backdoor" that was left behind

Of course, the original rules are not airtight. Its biggest loophole is that it mentions "Polymarket's token" but fails to precisely narrow its definition.

It does not clearly state that this token must be a "governance token" or a "core platform coin." This leaves a problem of "overly broad definition": as long as someone is willing to expand literally in the future, any asset issued by the official that meets the ERC-20 standard has the space to be reinterpreted.

Yet, even so, the loophole in the original rules resembles "the boundaries were not clearly defined," rather than "the object has been rewritten." From a semantic habit perspective, the term FDV itself is meant to measure the project's ceiling, not to count the issuance of a stablecoin.

3. The additional information became a logical replacement

The real turning point appeared in the later "Additional Information." The most critical change was:

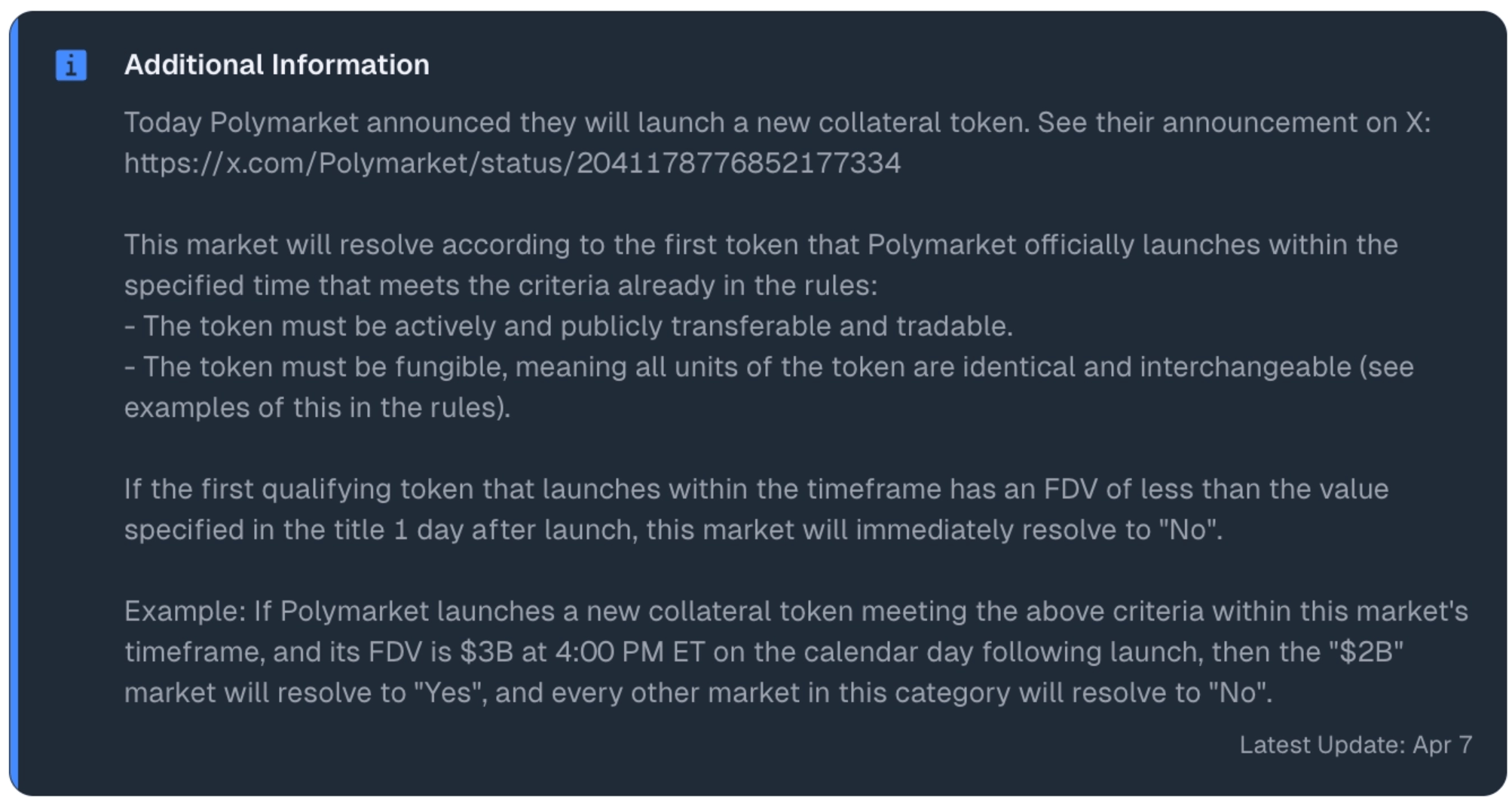

"This market will determine based on the first token that meets the conditions officially launched by Polymarket within the specified time."

This sentence seems to supplement details, but in fact, it completes a covert logical replacement. It transforms the originally market-meaningful term "Polymarket's token," which defaults to core assets, into a purely procedural and selective expression: "the first qualifying asset."

The former emphasizes "who it is": anchoring the narrative of brand and platform valuation.

The latter emphasizes "who came first": As long as the formal technical parameters are met, whoever rushes ahead is the determination target.

II. Similar markets, different anchors: Predict.fun's double standards in determination

The pillar of the platform's credibility lies in the consistency of rule execution.

By comparing the determination rules of Polymarket and Metamask on the Predict.fun platform, it can be found that under the completely same title framework and rule description, Predict.fun is executing two entirely different logics.

1. Logical division under the mirrored title

First, let's look at the titles of these two markets:

Polymarket: "Polymarket FDV above ___ one day after launch?"

Metamask: "Metamask FDV above ___ one day after launch?"

The title structure is completely consistent, all pointing to the fully diluted valuation (FDV) of project assets. This mirrored expression should correspond to a standardized determination protocol.

2. Deconstruction of the Resolution Determination Framework

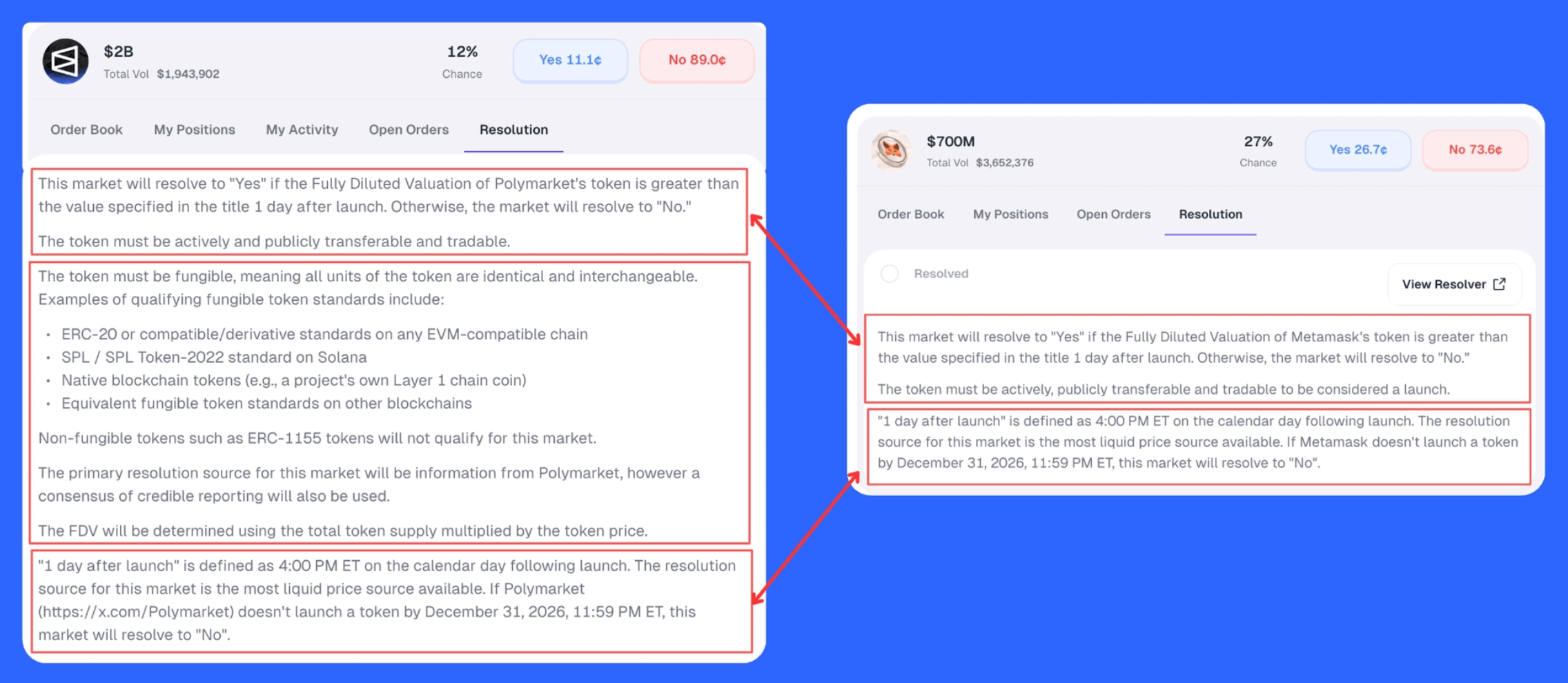

Through the comparison chart below, one can visually see the similarities and differences of the two markets in terms of Resolution (determination logic):

In the description of Resolution, Predict.fun adopts a "three-part" structure (as shown in the red box in the image):

First box (object definition): Clearly defines the determination target as "X's token."

Second box (technical parameters): Specifies that tokens must meet "fungible" and related contract standards.

Third box (settlement details): Defines the settlement time and data sources.

In the case of Polymarket, Predict.fun forcefully declares through the "Additional Information" that PolyUSD meets the criteria. This effectively elevates the technical parameters of the "second box" to the height of a unique core standard, thereby overriding the semantics of "Token" as the core asset of the platform in the "first box."

The conditions in the original rules—such as fungible, transferable, tradable token standards—are essentially just necessary conditions, not sufficient conditions.

They can only indicate that a certain token meets the minimum threshold for discussion, but cannot inversely imply: this token is the X's token mentioned in the title.

In other words,

"Meeting the threshold" does not equal "locking the target."

3. "$mUSD Paradox": The ultimate proof of double standards

The core evidence exposing Predict.fun's double standards lies in the $mUSD issued by Metamask.

Metamask launched its stablecoin $mUSD as early as last year. If we follow the logic set by Predict.fun for Polymarket—"as long as it is an officially issued token that meets the criteria for fungible transfer (including stablecoins), it counts"—then this FDV market should have settled using the $mUSD data from the very first second it went live.

The key contradiction lies in that the launch time of Metamask's prediction market is later than the issuance time of $mUSD. This means:

If the official believes that "Token = any fungible token (including stablecoins)," then this market should have determined settlement in the first second it went live.

Since this market is still trading normally and has not anchored $mUSD, it sufficiently illustrates that Predict.fun's officials do not consider "Token" to be judged as a stablecoin when formulating rules.

Predict.fun's approach in the Polymarket incident completely overturned the default criteria it demonstrated on the Metamask market. This "selective interpretation" proves that the platform is not maintaining the rules but is logically customizing them for specific events. This inconsistency in execution is the root of the skepticism.

When the rules cannot constrain determination, the market will lose to interpretation.

Credibility and liquidity are the core of operating in the prediction market. Rules can be complex, explanations can exist, but the premise is that anchors cannot drift, and standards cannot change abruptly. Once the semantics of the title, the determination target, and the additional information begin to disconnect, the platform consumes not only the patience of users in a particular dispute but also the fundamental trust of the entire market in "fair settlement."

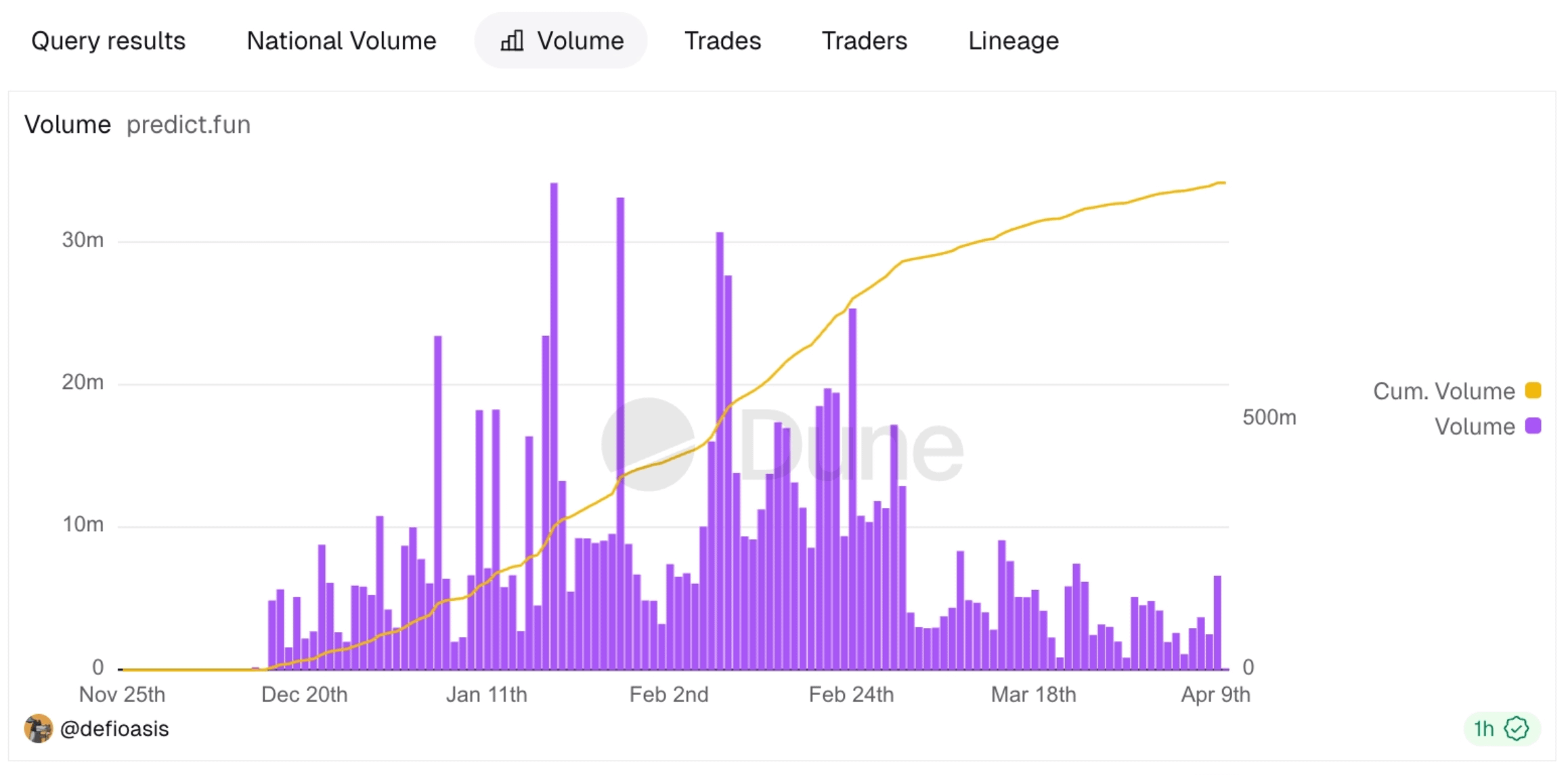

As an early project that received substantial investment from YZI Labs and continued to receive additional funding thereafter, Predict.fun has already stood at the pinnacle of the industry in terms of resources and endorsements. Around March 31, 2026, Binance began gradually pushing the prediction market feature to tens of millions of users through its news flow and Square community; until April 9, this feature was officially fully launched. This means that Predict.fun has completely integrated into Binance's traffic pool and credit distribution system from being an independently operating protocol.

However, looking at the transaction volume trends, since March 31, the integration of the Binance channel has not pulled it back onto a clear growth curve.

Channels can amplify products but cannot save rules that have lost their boundaries; endorsements can bring the first click but cannot replace long-term trust. When a platform continues to consume users' confidence in the consistency of judgments, even the strongest distribution capabilities appear to merely delay the manifestation of problems rather than solving the problems themselves. In other words, endorsements cannot save rules, and traffic cannot save trust.

The collapse of this logical structure is causing Predict.fun to fall into a hidden trust contraction.