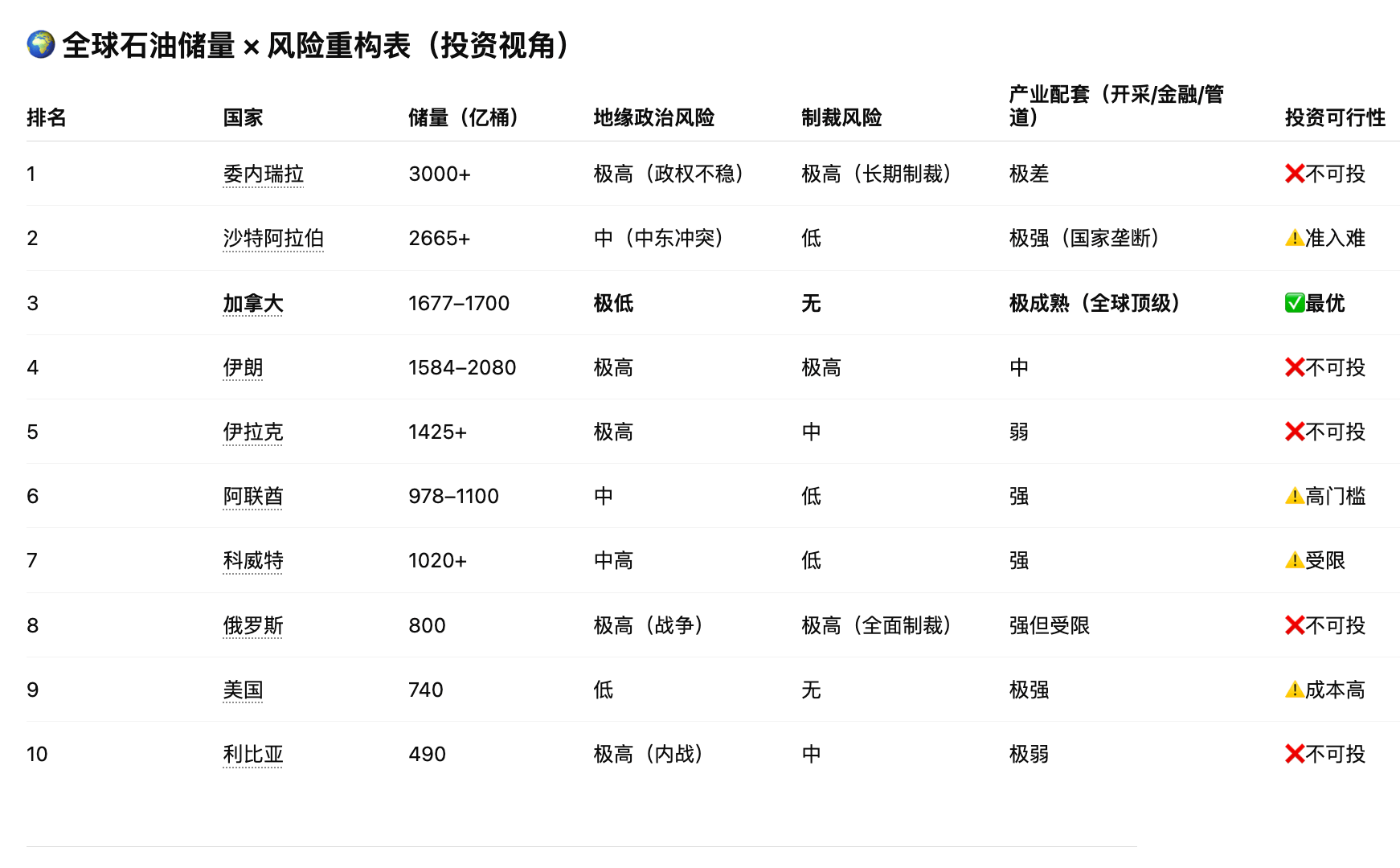

Canada = the "Switzerland" of the energy industry

Table of contents

I. Project Positioning

II. Asset-side engineering (must be made into "auditable cash flow")

III. SPAC Listing Path (Executable Timeline)

IV. Valuation Model (LP Concerns)

V. Market Value Management (must be systematic)

VI. Stock RWA (Core Upgrade Module)

VII. Valuation Restructuring After RWA

8. The Ultimate Capital Closed Loop (This must be shown in the roadshow, as a logic diagram)

9. Risks and Hedging (must be answered in advance)

10. One-sentence conclusion

A complete and executable solution for "Canadian Energy × AI Computing Power × US Stock SPAC × Stock RWA (Tokenization)," unfolded according to the practical logic of investment banking/PE:

Asset modeling → SPAC path → Valuation → Market capitalization management → Post-IPO RWA implementation → Trading and liquidity mechanisms. The focus is on raising funds, passing IPO approval, and continuously increasing valuation.

I. Project Positioning

"A low-cost, energy-driven AI computing infrastructure company + a publicly traded stock RWA issuance platform"

Benchmarking narrative (used to anchor valuation):

* Core Scientific

* Marathon Digital Holdings

II. Asset-side engineering (must be made into "auditable cash flow")

1️⃣ Old oil wells (cash flow base)

Input data (neutral):

* CAPEX: $480K/well

* Production: 50 barrels/day (range 35–80)

* Gas price: $65

* Operating costs: 35–45%

Annualized:

* Income: ≈ $1.18M

* Net cash flow: ≈ $650K–750K

👉 Key Metrics:

Payback period: 8–12 months

* Single-well IRR: 60%–120%

Engineering requirements:

* Third-party reserves report (NI 51-101)

* Historical production curve (Decline Curve)

* Audit reports (can be included in S-4 file)

2️⃣ Natural Gas → Power Generation → Computing Power (Estimation Amplifier)

Electricity costs:

* $0.015–0.025/kWh (lowest range globally)

Transformation:

* 1MW → AI computing power leasing

Annualized model (conservative):

* Revenue: $1.2M/MW

* EBITDA: $600K–800K

👉 Key point:

Transform an "energy company" into an "AI infrastructure company" (and its valuation doubles).

3️⃣ Biogas / Agricultural Electricity (A plus in valuation)

Its purpose is not to make money, but rather:

* ESG rating improved

* Carbon Credits

Policy subsidies stabilize cash flow

👉 Used for:

Increase the probability of institutional funds entering the market (pension funds/ESG funds)

III. SPAC Listing Path (Executable Timeline)

Step 1: Shell preparation (0–3 months)

Choose one of the two paths:

A. Self-built SPAC

* IPO:$100M–200M

* Cost: $8M–12M

B. Acquire an existing SPAC (Recommended)

Lower cost

* Faster turnaround time (3–6 months)

Step 2: PIPE Financing (Critical Lifeline)

Target:

* $50M–150M

* Investor structure:

* Energy Fund

* Web3 Foundation (paving the way for RWA)

Family Office

Step 3: De-SPAC (6–12 months)

document:

* S-4 / F-4

* Audited financial statements (2–3 years)

* Asset Appraisal Report

Step 4: Market Launch Completed

Ticker launched (NASDAQ/NYSE)

👉 Initial valuation of the target:

$500M–$1B

IV. Valuation Model

SOTP (Segmented Valuation)

Oil assets

* 100 wells × $3M

= $300M

Power assets

50MW x $1.2M

= $60M

AI computing power (core premium)

* EBITDA:$25M

* PE: 15x

= $375M

Total valuation

👉 $700M–$900M

Post-IPO goals

Through narrative + fluidity:

👉 $1B–$2B

V. Market Value Management (must be systematic)

Phase 1: Pre-De-SPAC

Release three types of information:

1. Reserves Report (Oil and Gas)

2. Computing power contracts (AI clients)

3. Power Expansion Plan

Phase 2: Initial Public Offering (0–6 months)

Target:

* Stabilize at $10 → Rise to $15–20

means:

* Dividend commitment (8–12%)

* Share buybacks (to support share price)

* Analyst Coverage

Phase 3: Growth Narrative (6–24 months)

I keep talking about three things:

1. Expansion of AI computing power

2. New Energy Access

3. RWA goes live (key catalyst)

VI. Stock RWA (Core Upgrade Module)

This is what sets you apart from 99% of projects.

1️⃣ Structural Design (Compliance Priority)

US stocks (held in custody by a brokerage firm)

↓

SPV Trust (Offshore)

↓

Issuing tokens (representing the right to receive benefits)

↓

On-chain transactions

👉 Essence:

Token ≠ stock itself, but rather represents equity.

2️⃣ Compliance path (must be clearly explained)

US Framework:

* Reg D (Accredited Investor in the United States)

* Reg S (Non-US Investors)

👉 Avoid:

Determined to be an illegal securities issuance

3️⃣ Token design (readily usable)

Parameter recommendations:

* 1 Token = 0.01 pcs

* Anchored to NASDAQ price

* Dividends are automatically distributed.

Function:

* Staking

* Lending (DeFi)

* LP Market Making

4️⃣ Liquidity Design (Key)

question:

US Stocks vs. On-Chain Price Discrepancy

solve:

Market Maker (MM)

Arbitrage mechanism

* NAV anchoring

5️⃣ Revenue Structure (LPs are most concerned about)

Investors receive:

① Stock price rises (stock)

② Dividends (Energy Cash Flow)

③ DeFi Yields (On-Chain)

👉 In short:

Same asset, three sources of income

VII. Valuation Restructuring After RWA

Tradition:

* Energy companies: PE 5–8x

* AI companies: PE 15–20x

After joining RWA:

👉 New Logic:

* Liquidity premium

* DeFi yield premium

Global funds entering

👉 Goal:

PE 20–40x

VIII. The Ultimate Capital Closed Loop

Energy assets (oil/gas/electricity)

↓

Low-cost electricity

↓

AI computing power cash flow

↓

SPAC goes public (gains valuation)

↓

US stock trading (traditional liquidity)

↓

Stock RWA (on-chain)

↓

Global funds are entering (7x24 trading)

↓

refinancing

↓

Acquire more energy assets

↓

Loop Amplification

9. Risks and Hedging (must be answered in advance)

1️⃣ Oil price risk

Hedging: Locking in prices with futures contracts

2️⃣ Fluctuations in AI Demand

* Safety net: Selling electricity (reverting to the utility model)

3️⃣ RWA Regulatory Risks

* Adopt compliant issuance (Reg D/S)

4️⃣ Liquidity Risk

* Market maker + arbitrage mechanism

10. One-sentence conclusion

This is a multi-layered capital amplification system that transforms "underground resources (oil/natural gas)" into "AI cash flow," then completes the pricing through "listing on the US stock market," and finally uses "RWA to split the stock into globally tradable assets."