From assets to market capitalization, from cash flow to liquidity control

Table of contents

First, this is the world's most mature "energy data asset repository".

II. The "Old Well Era" Arrives: A Structural Shift in Supply Logic

Third, supply is stagnant, but the asset pool is extremely large.

Fourth, the real opportunity lies not in oil prices, but in "asset mismatch profit-taking".

V. The Overlooked Trillion-Dollar Sector: Oil and Gas Well US SPACs + RWA (Asset Securitization)

VI. Why now? Because the time window has opened.

VII. Final Conclusion: An Underestimated Restructuring of Energy Capital

VIII. Core Definitions

IX. Underlying Assets: A "Real Money-Making" Cash Flow Engine

10. Overall Revenue Structure (Core)

11. Why is it naturally suited for capital operations?

12. From "Financing Model" to "Market Value Machine"

Thirteen, Six-Tier Capital Operation System (Full-Path Integration)

XIV. Ultimate Closed Loop (Core Model)

XV. Upgrading Core Cognition

XVI. What the Alliance Really Needs to Do

17. The ultimate expression in one sentence

18. Ultimate Understanding (Most Crucial)

Nineteen, the most ruthless cognition

20. Final Conclusion

—From assets to market capitalization, from cash flow to liquidity control

* The underlying assets are actually profitable (high profits and stable cash flow).

Capital structure can amplify (financing capabilities).

* The secondary market allows for market capitalization control.

Initiator: Chainlink Group (Canada)

Why Canada?

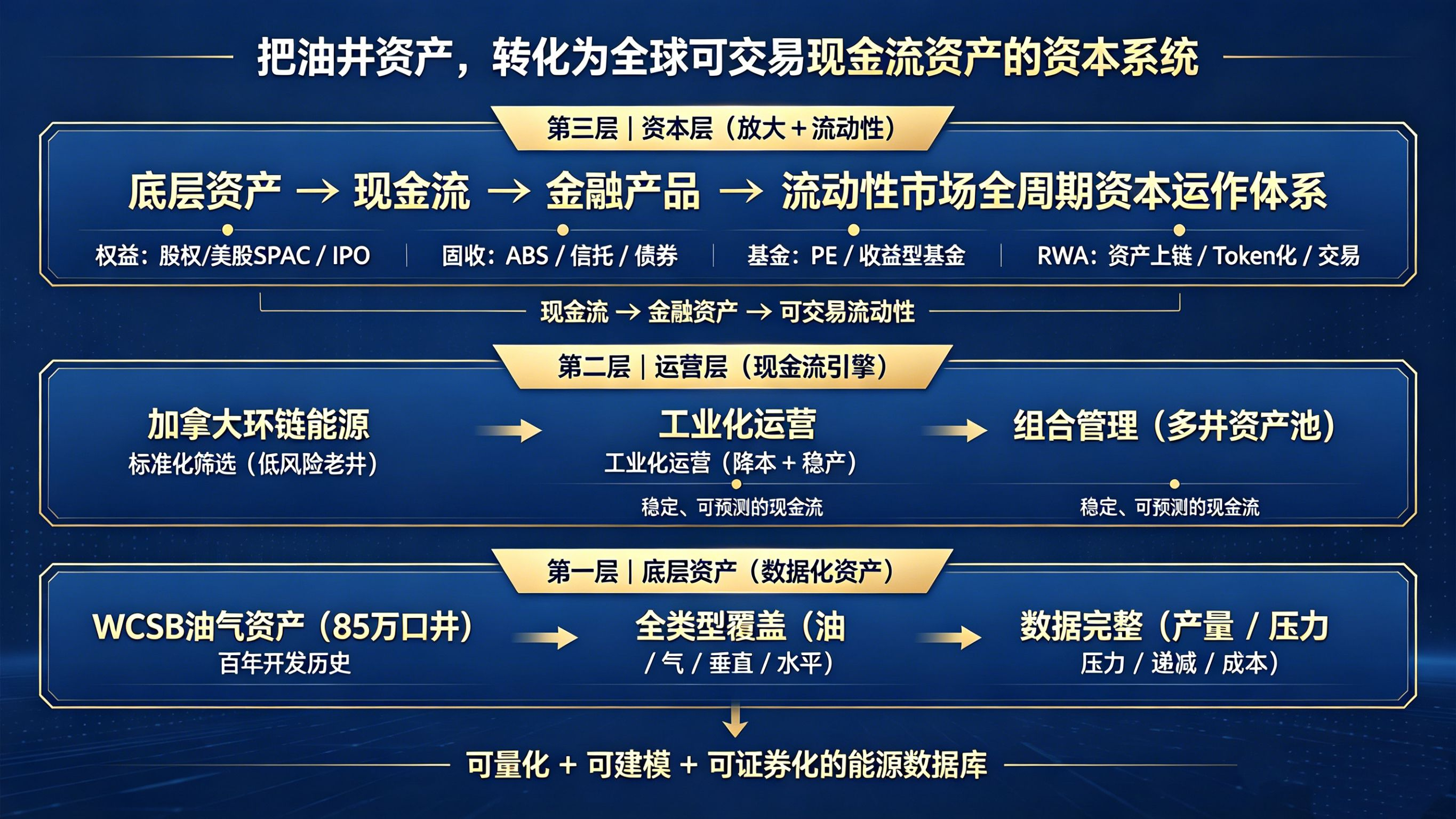

In the Western Canadian Sedimentary Basin (WCSB), more than 850,000 oil and gas wells have been drilled since 1901 (Canadian Association of Petroleum Producers, 2025).

The significance of this number lies not in its "scale," but in its "structure." It releases three key signals that can be capitalized:

First, this is the world's most mature "energy data asset repository".

* Over a century of continuous development cycle

* Covers all types of oil wells / gas wells / vertical wells / horizontal wells

* Highly comprehensive core parameters such as production, pressure, decline curve, and cost.

👉 Fundamental Restructuring:

What's stored here isn't resources, but a globally rare, quantifiable database of oil and gas assets.

Further deduction:

* Can perform standardized modeling (Decline Curve / Cash Flow)

* Risk stratification (well-level asset rating) is possible.

* Enables batch financial processing (asset pool packaging)

Conclusion: The WCSB oilfield serves as "energy data infrastructure".

II. The Arrival of the "Old Well Era": A Structural Shift in Supply Logic

Among 850,000 wells:

* Active producing wells: Only tens of thousands

* Inefficient/Idle wells: Hundreds of thousands of wells

* Orphan Wells: Continuously accumulating

👉 This is not a resource issue, but a typical capital misallocation problem:

Large oil companies exit low-margin assets

* Operating costs are mismatched with organizational efficiency

* Small-scale assets lack financial instruments to support them.

Key changes:

Canada has moved from the "resource expansion phase" to...

"Stock Optimization Cycle"

Third, the supply side is stagnant, but the asset pool is extremely large.

* Annual new drilling: Approximately 5,000–7,000 wells

* The growth rate of the total number of wells is slowing down.

* The existing well stock is extremely large.

👉 Entering the typical structure:

Existing asset size ≤ Incremental development capacity

what does that mean?

Future production will no longer depend on "how many new wells are discovered".

* Rather, it depends on "how to restructure, optimize, and refinance the old wells".

Fourth, the real opportunity lies not in oil prices, but in "asset mismatch profit-taking".

A common market misconception: equating oil and gas investment with oil price beta.

But in Canada, alpha comes from structural mismatches:

1) Old Well Assets, which are systematically undervalued

* Still has stable production

* Positive cash flow

* Defined as "non-core" by large companies

👉 Result: Bulk divestiture / Discounted sale / Clearance sale

2) The "passive exit" wave of global energy giants

Driving factors:

* ESG pressure

* Balance sheet contraction

* Strategic shift to a low-carbon narrative

👉 Direct consequences:

High-quality cash flow assets were liquidated at non-market prices.

3) Regulation + Data Transparency: The Underlying Prerequisites for Financialization

Key institutions:

* Alberta Energy Regulator

* Canadian Association of Petroleum Producers

Core features:

* Strong oversight of production data (directly linked to tax revenue)

* Single well full life cycle traceability

* Engineering and financial data are highly standardized

👉 This leads to a crucial result:

Energy assets have for the first time demonstrated verifiability as "quasi-debt assets".

V. The overlooked trillion-dollar sector: Oil and gas well RWA (asset securitization)

If we reconstruct the single-well model using financial terminology:

* Initial investment: Approximately US$500,000

* Daily production: 35–80 barrels

* Lifecycle: 5–15 years

* Decline rate: 15%–25%

👉 Corresponding financial attributes:

* Predictable cash flow

* Modelable IRR

* Asset stratification and packaging are possible.

VI. Why now: The time window has opened.

Triple variable superposition:

1) Long-term contraction in supply

Global capital expenditure underutilization

* New oilfield development declines

Rising geopolitical risks

2) Demand remains rigid.

Oil remains the core energy source

* Demand for natural gas (especially LNG) continues to grow.

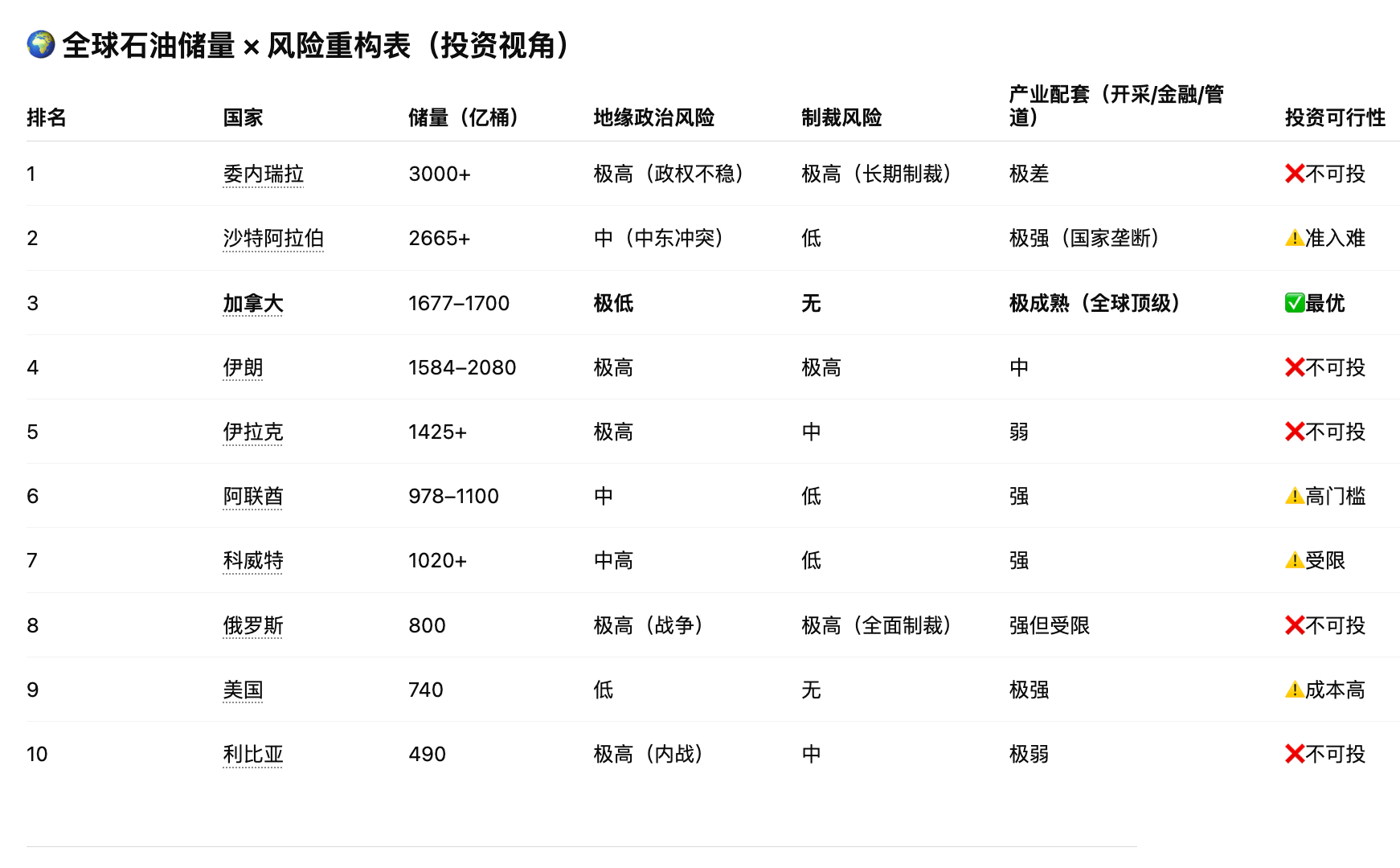

3) Canada's "Asset Reassessment"

Compared to the Middle East, Africa, and Latin America:

Canada has:

Political stability

Mature legal system

Strong intellectual property protection

High data transparency

👉 Essential positioning:

"Anchors of safe assets" in the global energy system

VII. Final Conclusion: An Underestimated Restructuring of Energy Capital

The 850,000 wells are not a historical burden, but rather:

The world's largest pool of reconfigurable and financializable energy assets

The core variable for the future is not:

* New oil field discovery

* Single-point technological breakthrough

But it lies in:

The ability to rewrite financial structures (structuring + securitization + blockchain)

The most crucial sentence

The next energy bull market won't just be about rising oil prices—

Rather, it is a systemic repricing of oil and gas assets.

8. Core Definition (First, break through the cognitive barriers)

We are not doing energy projects, but building a:

An energy capital amplification system with modelable cash flow, multi-tiered financing, market capitalization management, and on-chain liquidity.

IX. Underlying Assets: A "Real Money-Making" Cash Flow Engine

A one-sentence summary (for all investors)

This is an energy cash flow system that can be modeled, predicted, divided, securitized, and put on-chain.

1️⃣ Oil assets (core of cash flow)

▶ Standard model for a single well

* Single well investment: Approximately US$500,000

* Daily production: 35–80 barrels

* Decline rate: Approximately 20%/year

* Lifecycle: 5–10 years

▶ Revenue and Profit (Core Data)

Assumptions: Oil price $60 / $70 / $80, cost $30

Daily profit:

* 35 barrels: $1,050 – $1,750

* 80 barrels: $2,400 – $4,000

▶ Annual profit:

* Approximately $380,000 – $1,460,000

▶ Payback period:

6–12 months

▶ Lifecycle cash flow:

Cumulative total for a single well over 5 years: US$1.5 million – US$4 million

▶ Essence:

A standardized asset unit characterized by "rapid recovery + long-tail cash flow + replicability".

2️⃣ Natural Gas → Electricity (Profit Stabilizer)

* Power generation cost: approximately RMB 0.1 per kilowatt-hour (≈ USD 0.014)

▶ Profit Model:

* Price: 0.05–0.07 USD

Gross profit: USD 0.036 – 0.056/kWh

👉 Gross profit margin: 70%+

▶ Essence:

Low-cost electricity = global energy arbitrage + the underlying moat of computing power competition

3️⃣ Agricultural electricity / biogas (stable income layer)

* Cost: Approximately 0.2 yuan/kWh (≈0.028 USD)

▶ Features:

* Policy subsidies

* Stable returns

* ESG Bonus

▶ Essence:

Low-volatility cash flow + policy-driven competitive advantage assets

4️⃣ Computing power (profit amplifier)

▶ Logic:

Low-cost electricity → transformed into:

* BTC hashrate revenue

* AI computing power leasing

▶ Essence:

Upgrade energy cash flow to "digital asset cash flow + highly elastic returns".

10. Overall Revenue Structure (Core)

Three layers of profit stacking:

① Resource layer (oil/natural gas)

👉 Stable cash flow + quick return on investment

② Energy layer (electricity)

👉 High profit margin + counter-cyclical

③ Digital Layer (Computing Power / Token)

👉 High elasticity + liquidity premium

▶ Final Result:

A composite asset system that simultaneously possesses "certainty + growth potential + liquidity".

11. Why is it naturally suited for capital operations?

Because it possesses four financial attributes simultaneously:

* ✔ Predictable (clear decline curve)

* ✔ Standardizable (unified single-well model)

* ✔ Securitizable (ABS / Fund)

* ✔ Can be on-chain (RWA / Token)

12. From "Financing Model" to "Market Value Machine"

Traditional logic:

Assets → Financing → Holding

Our logic:

Assets → Financing → Listing/On-chain → Market Value Management → Refinancing → Cyclical Amplification

Thirteen, Six-Tier Capital Operation System (Full-Path Integration)

First level: Asset acquisition

* Oil wells / Electricity / Computing power / Biogas

👉 Acquire: Control over the underlying cash flow

Second tier: Primary market financing

* Equity Investment

* GP/LP Fund

* Merger and Acquisition Fund

* Industrial Capital

👉 Completion: Funding Inflow + Asset Integration

Third layer: Debt and structured financing

* ABS

Corporate bonds / Project bonds

* Convertible bonds

* Trust Structure

* Layering of Profit Rights

👉 Completed: Low-cost cash flow amplification

Fourth level: Capital market (listed companies)

US SPACs

IPO / Backdoor Listing

Mergers and acquisitions

+ Core Enhancements:

* ✔ Stock Private Placement (PIPE)

* ✔ Publicly offered products / REITs-like products

👉 Completed:

Assets → Equityization → Inclusion in Valuation System

Layer 5: On-Chain Finance (RWA)

* Released by RWA

* Profit Rights Token

DeFi Collateralized Financing

Stablecoin yield products

👉 Completed:

Global liquidity access

Sixth Layer: Secondary Market and Market Value Management (Core Profit Layer)

▶ Core Objective:

* Stabilize stock price

* Increase valuation multiple

* Controlling fluctuations

* Service refinancing

▶ Three major trading tools:

1️⃣ Market making and liquidity control

Market Maker

* Deep Management

* Transaction guidance

2️⃣ Private Placement + Secondary Market Linkage

* Low-level locking of shares

* Secondary upward movement

* Price difference

3️⃣ Institutional + Transaction Fund Collaboration

* Stable valuation for long-term funds

* Hedge funds provide liquidity

▶ Five types of capital structures (key)

▶ Token Secondary Market

* CEX / DEX

* Liquidity pool

* Staking Incentives

👉 Essence:

Make global retail investors a source of liquidity

▶ Core objective in one sentence:

It's not about raising prices, but about creating conditions for the next round of financing.

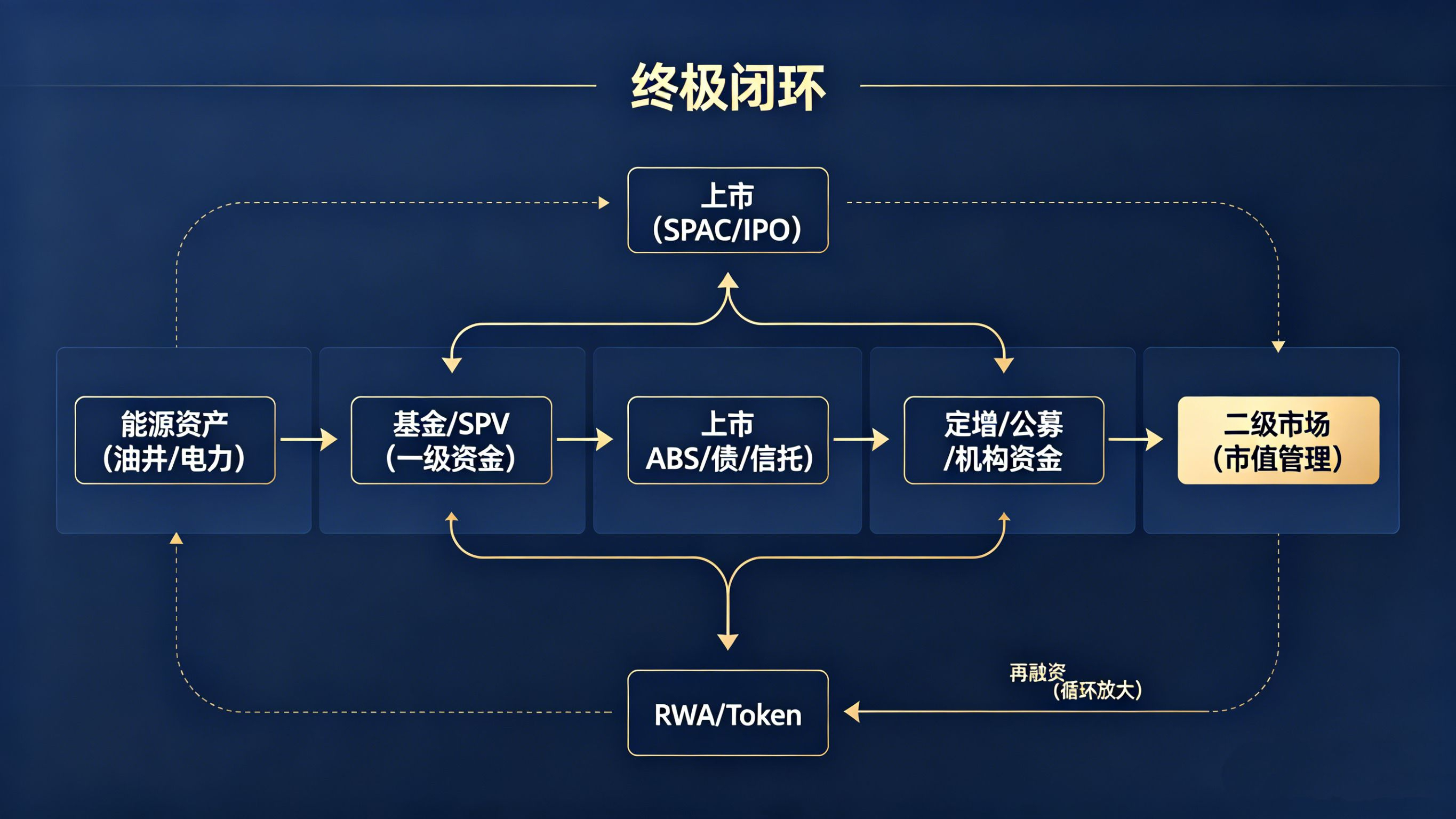

XIV. The Ultimate Closed Loop (Core Model)

Energy assets (oil wells/electricity)

↓

Fund / SPV (Level 1 Fund)

↓

ABS / Debt / Trust

↓

Listing (SPAC / IPO)

↓

Private placement / public offering / institutional funds

↓

Secondary market (market capitalization management)

↓

RWA / Token

↓

Refinancing (revolving amplification)

XV. Upgrading Core Cognition

Traditional companies:

Going public = the end point

us:

Going public = the start of a financing cycle

XVI. What the Alliance Really Needs to Do

We're not looking for investors, we're building a team:

"A Puzzle of Global Financing Capabilities"

Each member will acquire one additional skill:

17. The ultimate expression in one sentence

We are not just financing a single project, but building an energy finance machine that can be repeatedly financed and scaled up.

To build a capital synergy network for energy assets across primary markets, secondary markets, and on-chain markets.

Three layers operating simultaneously:

* Primary Market: Fundraising

* Secondary Market: Magnification

* On-chain Markets: Diffusion

18. Ultimate Understanding (Most Crucial)

We are not just investing in energy assets, but controlling a cash flow system that can be repeatedly securitized, blockchainized, and continuously amplified through market capitalization management.

Nineteen, the most ruthless cognition

What's truly valuable isn't just the oil well, but rather:

Someone who can turn the cash flow from a well into debt, equity, and tokens, and raise funds more than three times.

20. Final Conclusion

The most profitable thing in the future will not be owning assets, but rather:

Control the pricing power, liquidity, and financing pace of assets.

The following are the cooperative business opportunities in Canadian oil and gas exploration: