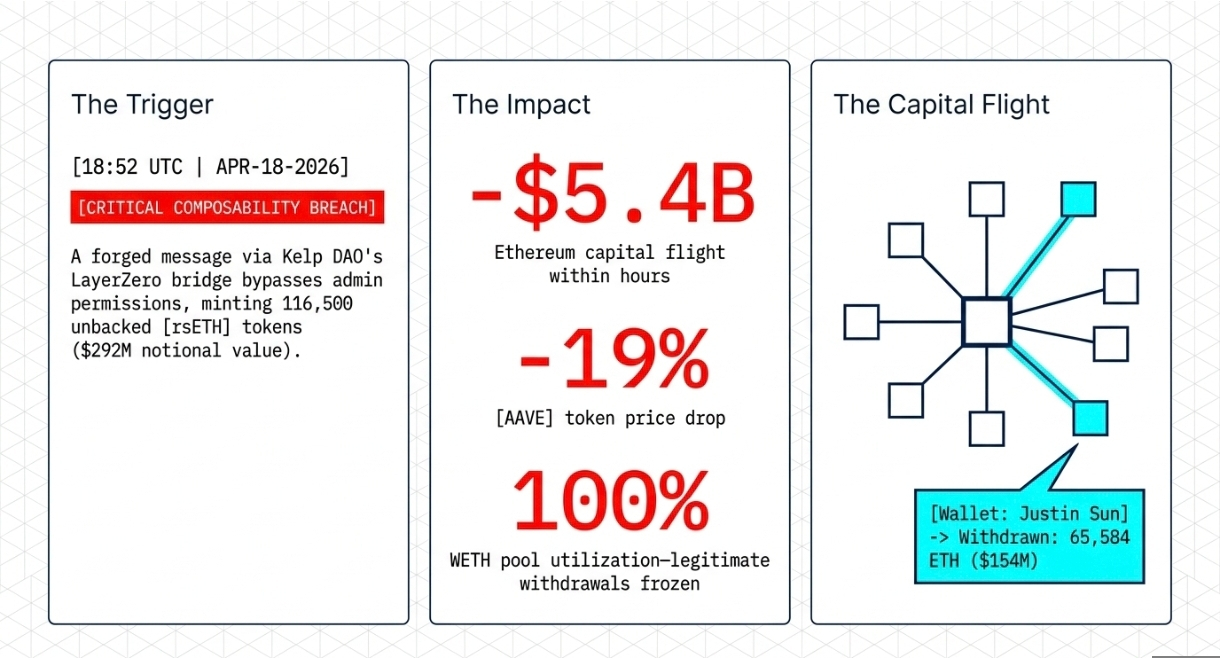

At 18:52 UTC on April 18, 2026, the largest DeFi lending market broke. A single transaction triggered automated alerts across the monitoring systems of the protocol. An attacker had just exploited a vulnerability in the LayerZero cross-chain bridge adapter operated by Kelp DAO.

Security reports confirm the attacker used a forged message to gain unauthorized control over the system. This technical manipulation allowed the attacker to bypass admin-level permissions and mint 116,500 rsETH tokens out of thin air. These forged tokens carried a notional value of roughly $292 million and represented 18 percent of the entire circulating supply of the asset.

Within minutes, the attacker deposited these unbacked tokens into Aave V3 and Aave V4 as collateral. They borrowed real wrapped ether against the fake collateral and completely drained the available funds.

Aave guardians reacted by freezing the rsETH markets to prevent new deposits. Kelp DAO paused its smart contracts. The emergency measures arrived too late. The wrapped ether lending pool hit 100 percent utilization. Users who had deposited ether into Aave to earn interest found they could no longer withdraw their money. Panic spread across social platforms, and onchain activity reflected immediate, massive capital flight.

Real-time reactions exposed the severity of the situation immediately:

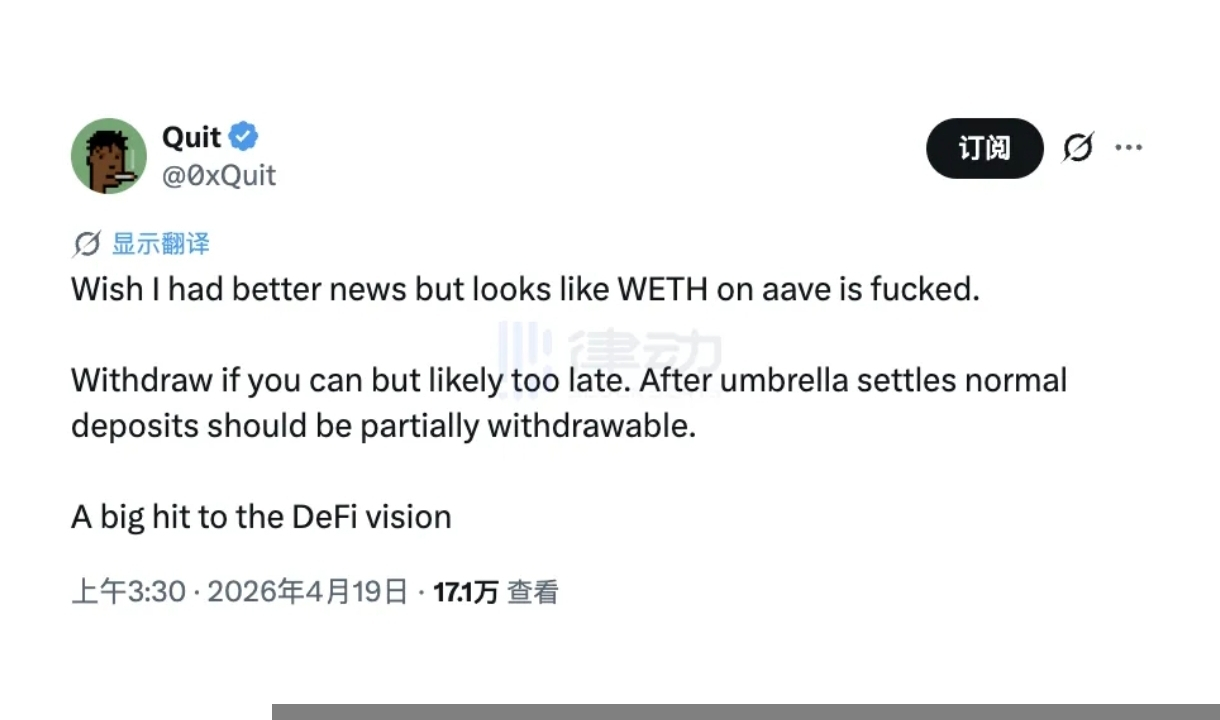

Solidity developer 0xQuit posted on X that wrapped ether on Aave appeared ruined, urging users to withdraw whatever they could before the system locked completely.

Curve Finance founder Michael Egorov observed that Aave was left holding rsETH that could never be sold alongside max-borrowed ETH.

Consensys developer relations head Francesco Andreoli called the situation a case of massive bad debt.

Aave officially announced the freezing of rsETH and wrsETH markets across all deployments to stop the bleeding.

Marc Zeller, founder of the Aave Chan Initiative, took to social media to dismiss the highest bad debt estimates. He stated the event would serve as a real stress test for the Umbrella safety module.

Aave founder Stani Kulechov insisted the smart contracts of the protocol remained completely unharmed and that the problem lay entirely with Kelp DAO.

Both Kulechov and the critics were correct. The core contracts of Aave were never breached. Yet the protocol now carried between $177 million and $280 million in bad debt. A crisis that began outside Aave had become the biggest problem in the history of Aave.

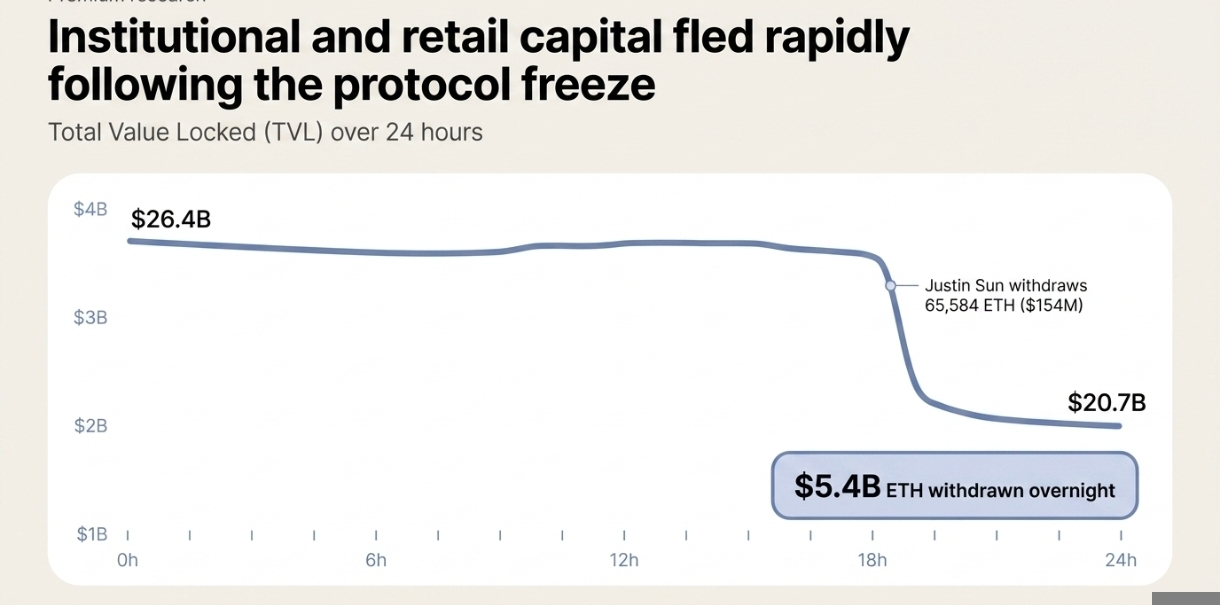

The financial impact spread rapidly. Over $5.4 billion in Ethereum exited the protocol within hours. The total value locked in Aave fell from $26.4 billion to roughly $20.7 billion by the next morning. Large holders rushed for the exits to protect their capital. Blockchain data showed cryptocurrency founder Justin Sun withdrawing 65,584 ether, worth roughly $154 million, in a single transaction. The native AAVE token dropped roughly 19 percent as the market digested the news.

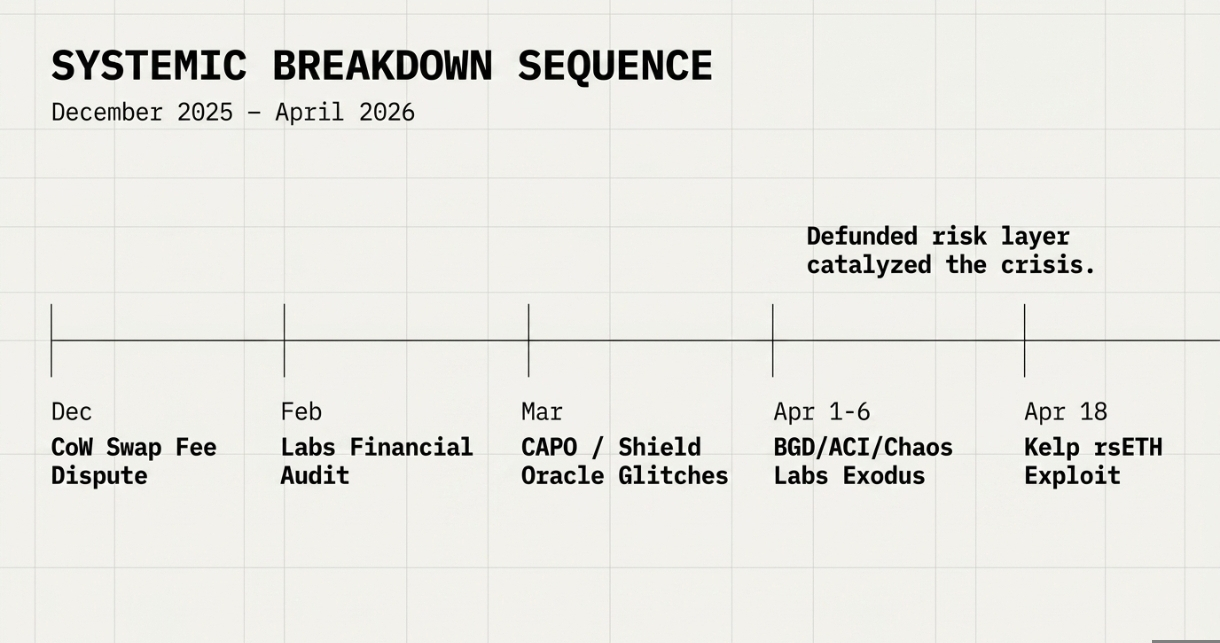

This disaster was never an isolated failure. It was the highly predictable result of multiple systemic breakdowns unfolding between December 2025 and April 2026. A governance war fractured trust between the decentralized autonomous organization and Aave Labs. Three core contributor teams walked away in protest. Risk management capacity degraded severely. Technical glitches signaled growing operational fragility. An external exploit simply hit the exact weakness that a depleted ecosystem was least prepared to handle.

Aave matters because it anchors decentralized finance lending. At its peak, the protocol held over $26 billion in total value locked and had issued more than $1 trillion in cumulative loans. It serves as the largest money market in the digital asset space. When Aave stumbles, the entire sector feels the impact. This report details exactly how Aave stumbled. It begins with a dispute over fees in December 2025 and ends with a frozen ether pool in April 2026.

2. Aave's Golden Era

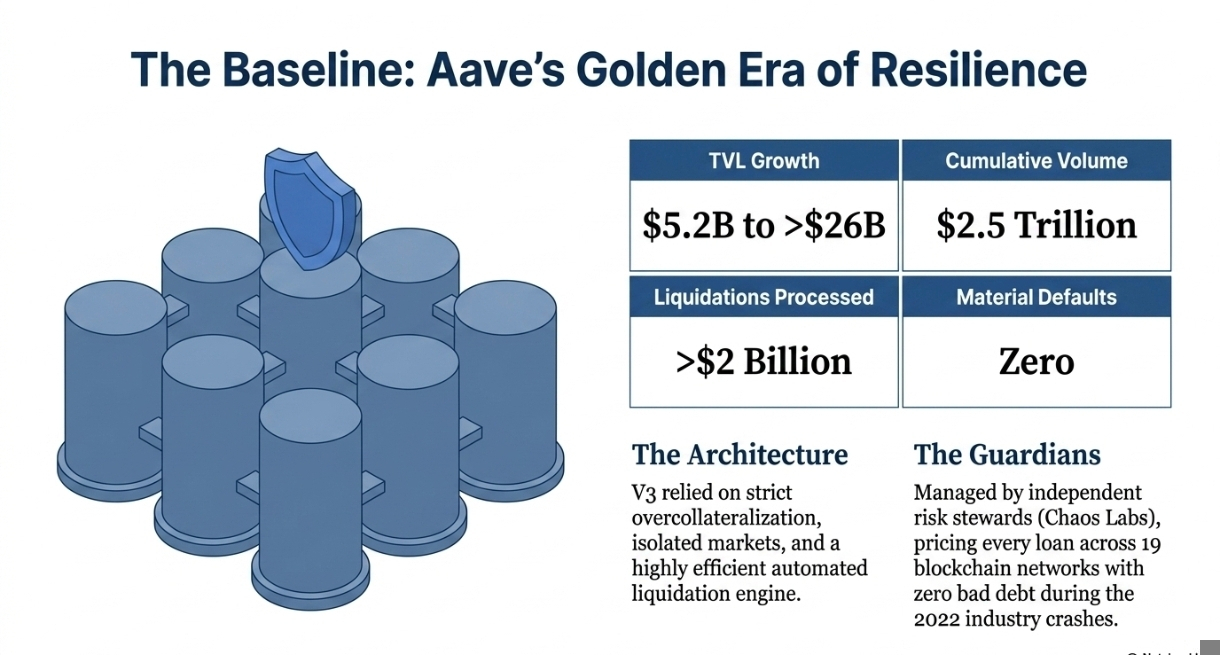

Aave earned its reputation through extreme resilience. During its transition from the V2 architecture to the V3 architecture, the protocol established the industry standard for decentralized risk management. Depositors treated Aave as a foundational layer of yield generation. They viewed its smart contracts as nearly risk-free.

The protocol relied heavily on strict overcollateralization requirements and highly efficient automated liquidation engines. This specific model survived extreme market volatility. Aave maintained near-zero bad debt during the severe industry collapses of 2022. It processed massive liquidation events without leaving the protocol insolvent.

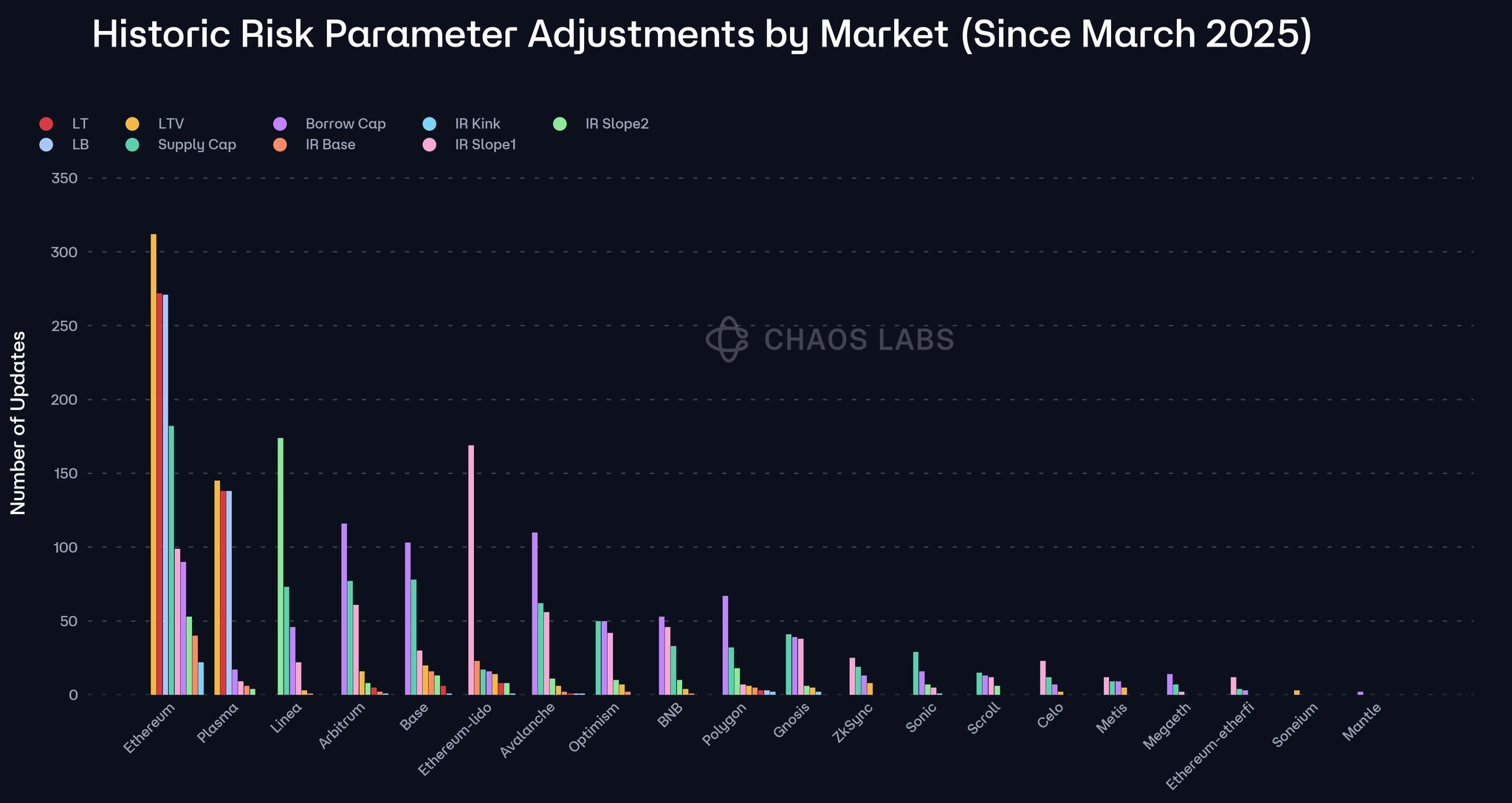

Independent risk managers drove this massive success. Chaos Labs took over the primary risk mandate in November 2022. Their operational record was flawless. They priced every single loan initiated on the platform. They managed risk parameters across hundreds of markets spanning 19 different blockchain networks. Protocol deposits grew from $5.2 billion to over $26 billion during their tenure. They facilitated over $2.5 trillion in cumulative deposit volume. They successfully processed over $2 billion in liquidations without a single material default. The system worked perfectly because it was built on highly conservative assumptions. Borrowers had to post far more collateral than they borrowed. If collateral values dipped, liquidators stepped in quickly.

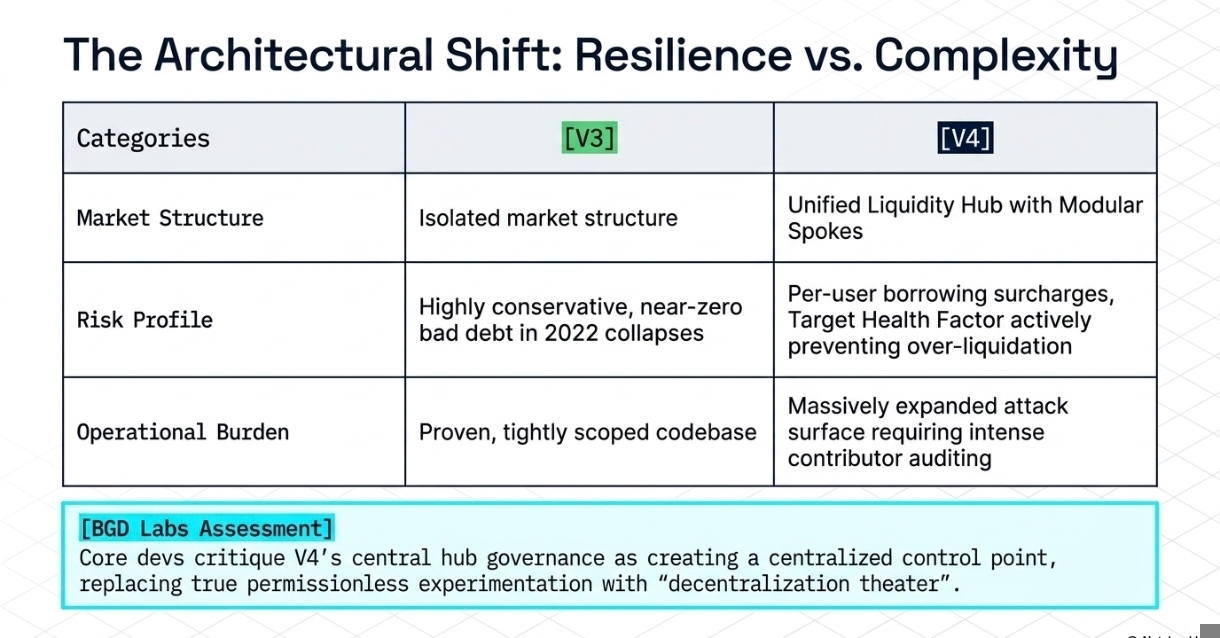

Early cracks appeared with the conceptualization and development of Aave V4. The new architecture introduced a highly complex hub-and-spoke model. This design replaced the isolated market structure of V3.

The V4 architecture introduced several massive changes to the lending environment:

Unified Liquidity Hub: All liquidity routes through a central core rather than sitting in fragmented pools across different chains.

Modular Spokes: User interaction and specific risk limits live in separate spoke modules that connect to the main hub.

Risk Premiums: The system introduces per-user borrowing surcharges tied directly to the quality of their specific collateral.

Target Health Factor Liquidations: Liquidators repay only enough debt to restore a position to a target health level, actively preventing over-liquidation.

The transition created severe organizational friction. The hub-and-spoke model drastically increased the technical complexity of the protocol. It expanded the operational burden on independent contributors who had to audit and secure a much larger surface area. BGD Labs, the core development team for V3, explicitly critiqued the new design. They stated that while V4 was more capital efficient, the central hub governance created a centralized control point. They argued it replaced true permissionless experimentation with decentralization theater.

Tensions surrounding revenue generation, intellectual property, and protocol control began to fracture the relationship between the community and Aave Labs. The relentless pursuit of massive institutional adoption slowly replaced the fundamental commitment to absolute protocol safety. Aave rested its risk management on a fragile foundation of contributor trust. When that foundation cracked, everything built on top of it became vulnerable.

3. The Governance Wars:

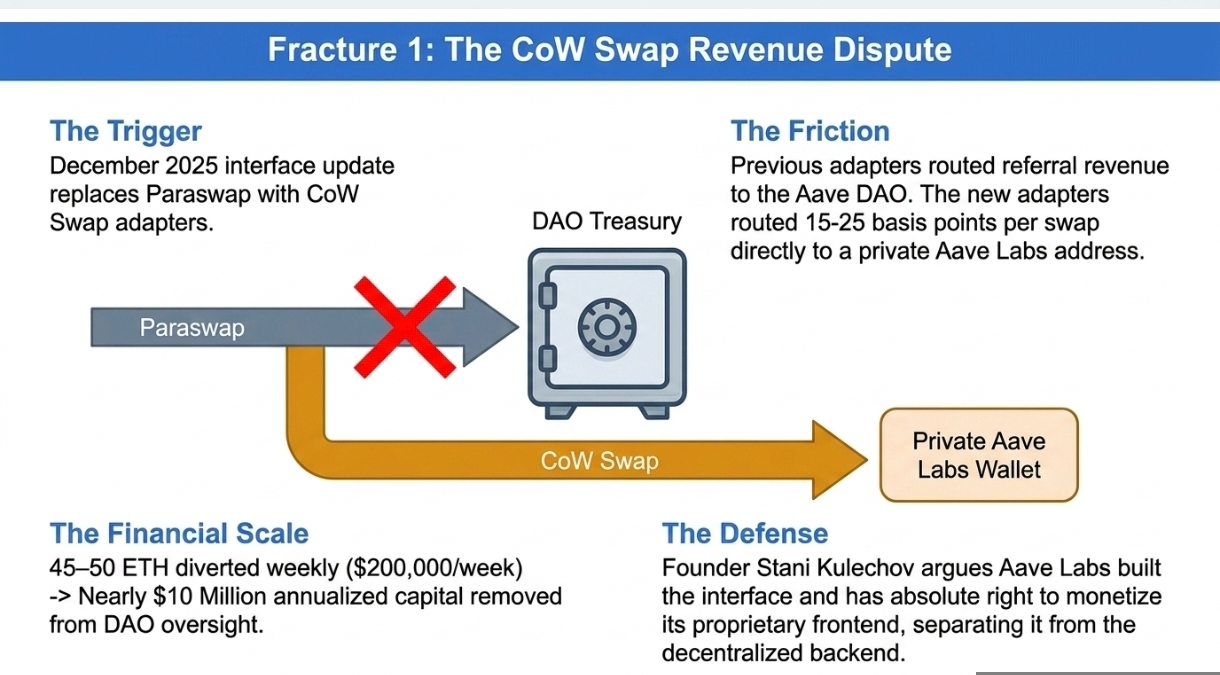

The internal instability began with a highly public dispute over protocol revenue. In December 2025, an interface update triggered a massive political conflict that exposed deep divisions regarding the true ownership of the protocol.

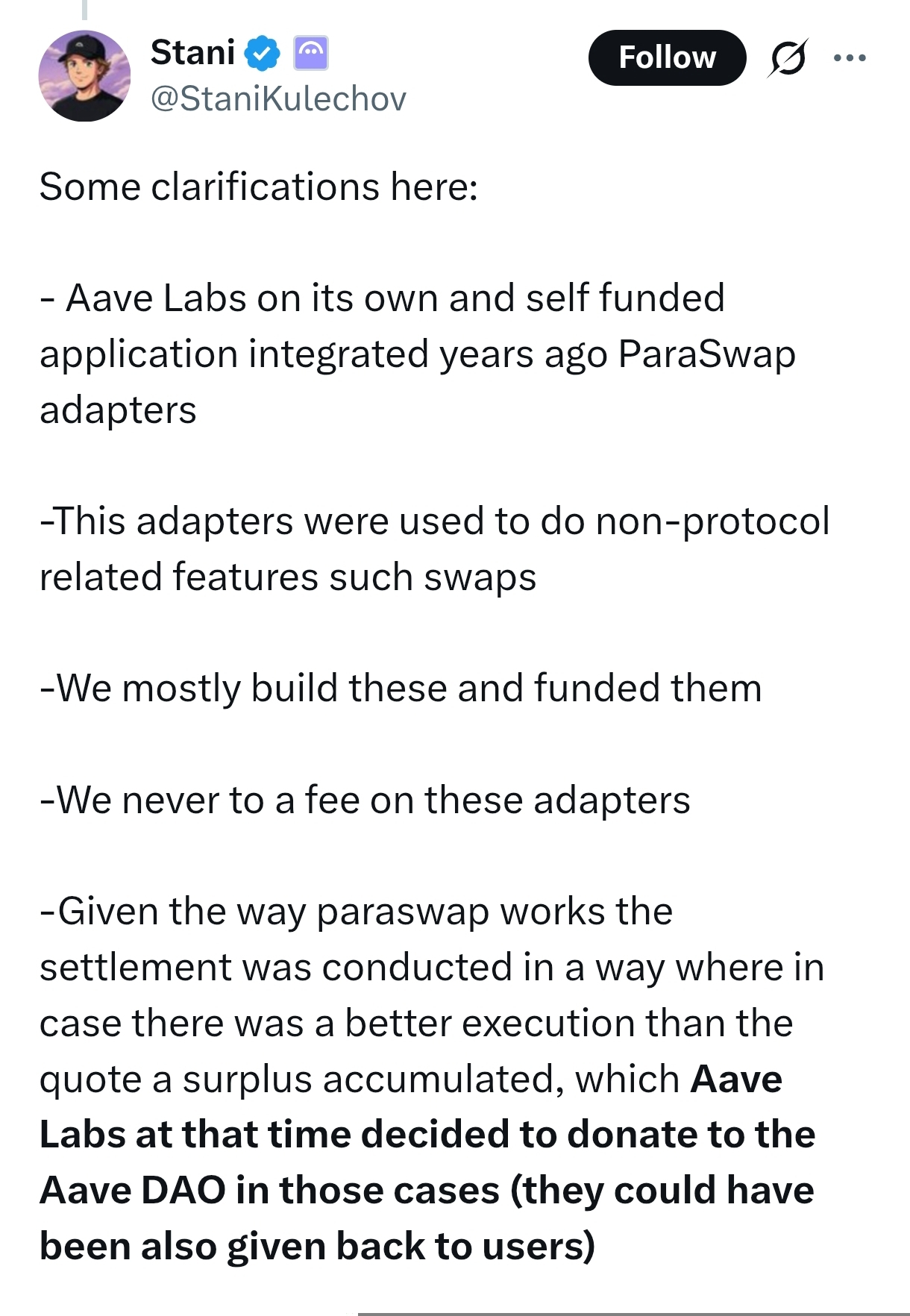

The trigger event involved the integration of CoW Swap. Aave Labs deployed specific software adapters allowing users to swap tokens directly on the aave.com website. This new feature replaced an older, established integration with Paraswap. The previous Paraswap integration included a programmed referral mechanism that directed all generated exchange revenue straight to the Aave DAO treasury.

Community members soon discovered the new CoW Swap implementation operated entirely differently. The new adapters generated swap fees ranging from 15 to 25 basis points per transaction. These fees did not flow to the DAO treasury. They routed directly to a private onchain address controlled entirely by Aave Labs.

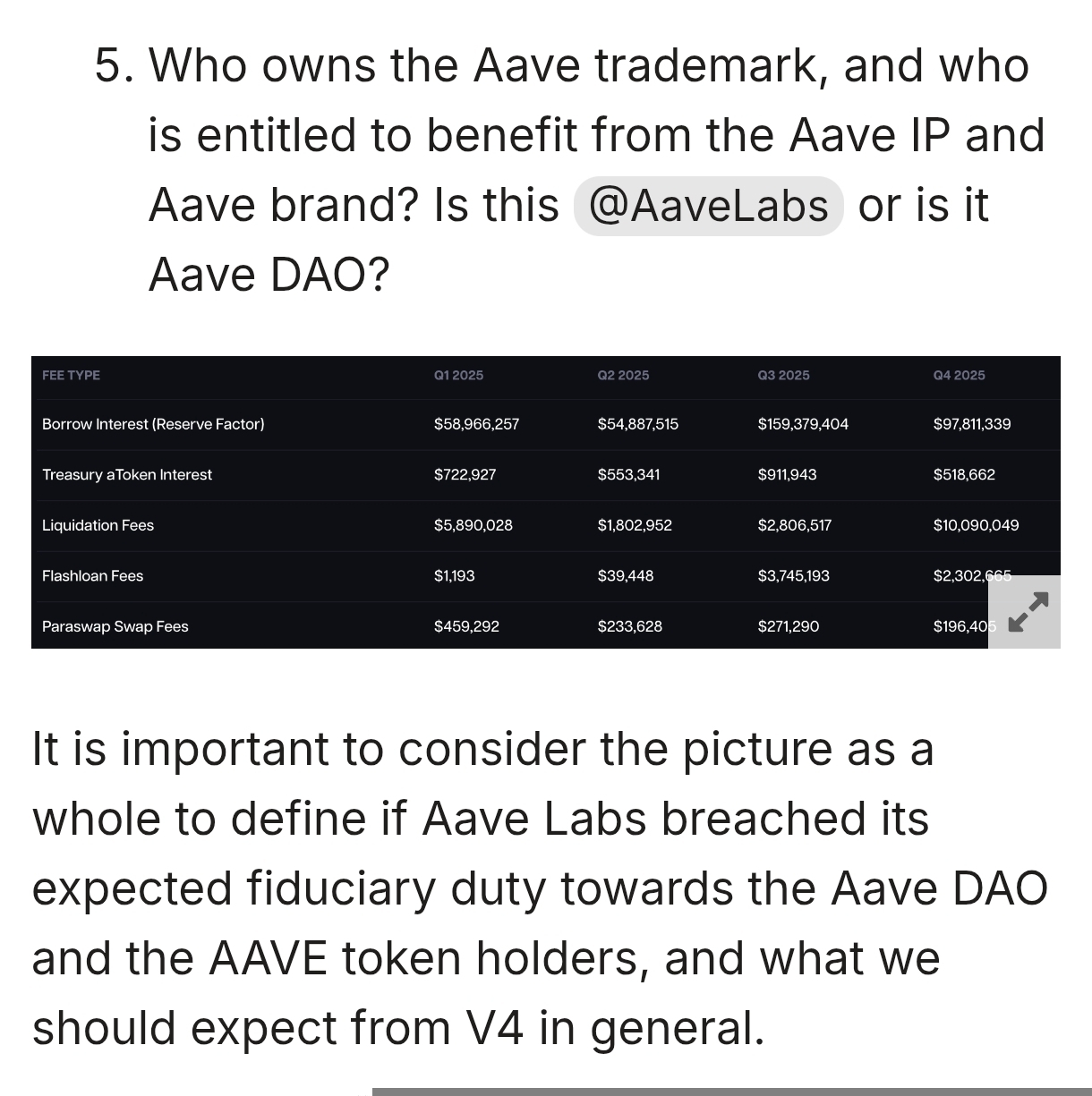

The financial scale was significant. Forum estimates suggested the routing diverted roughly 45 to 50 ether per week on the Ethereum mainnet. This volume equaled approximately $200,000 in weekly revenue. It represented nearly $10 million in annualized capital removed from the DAO treasury.

Aave founder Stani Kulechov vigorously defended the setup. He stated that Aave Labs funded, built, and maintained the frontend interface. He argued the interface was a proprietary product separate from the core decentralized smart contracts governed by the community. He believed Aave Labs had the absolute right to monetize its specific products.

Marc Zeller pushed back immediately. He called the maneuver a stealth privatization of protocol revenue. He labeled the decision a direct attack on the best interests of AAVE token holders. Zeller escalated the conflict on February 25, 2026, by publishing a comprehensive audit of Aave Labs.

The audit detailed that Aave Labs had already received roughly $86 million in total capitalization across the 2017 initial coin offering, venture rounds, direct DAO payments, and the disputed swap fees. Zeller questioned the return on investment for the community. He criticized several standalone initiatives led by Aave Labs. He referred to products like Lens Protocol, GHO v1, and Horizon as a product graveyard. Zeller noted that Horizon, the real-world asset market of the protocol, commanded over $500 million in total value locked but still resulted in a negative 96 percent return on investment. He highlighted that the native stablecoin GHO depegged during its first version and required a complete rebuild by independent teams.

The conflict ultimately centered on voting power. Onchain data showed that Aave Labs and closely associated entities controlled approximately 23 percent of the total AAVE token supply. This massive concentration allowed the development company to dominate governance outcomes. BGD Labs proposed transferring the Aave brand assets to DAO control during the Christmas holiday. Kulechov voted against it, and the proposal failed.

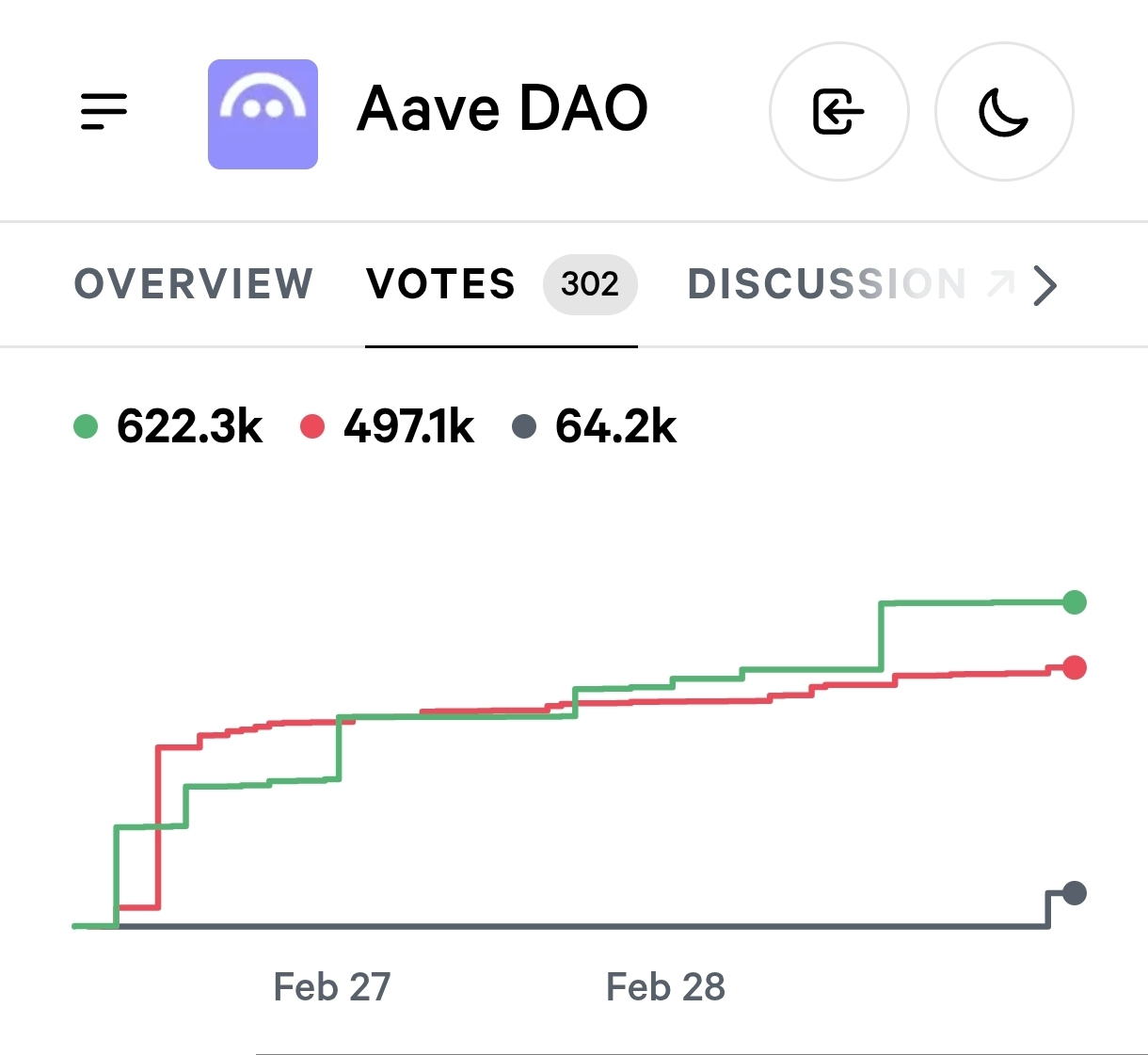

The climax arrived on April 13, 2026. The DAO voted on the "Aave Will Win" proposal. The vote passed with 52.58 percent in favor and 42 percent against.

The approved framework established the following terms:

One hundred percent of gross revenue from Aave-branded products flows directly to the DAO treasury.

Aave Labs receives a $42.5 million stablecoin allocation. This includes $5 million upfront, $20 million streamed over 12 months, and $17.5 million in milestone grants.

Aave Labs receives 75,000 AAVE tokens vesting linearly over four years.

Aave Labs commits to working exclusively on Aave-related products and solidifying V4 as the permanent architecture.

A new Aave Foundation is created to steward the brand assets.

Zeller analyzed the blockchain data immediately after the vote. He identified that 233,000 AAVE votes came directly from three address clusters linked to Aave Labs. He noted that 111,000 AAVE delegated directly from Kulechov voted in favor of the funding. Without these specific votes, the proposal would have failed decisively. The DAO secured a structural revenue victory. The ecosystem lost the trust of its most critical service providers.

4. Chaos Labs' Departure

The governance conflict caused a massive, unprecedented loss of operational capacity. Three major independent service providers announced their departures within weeks of each other. This exodus stripped the protocol of its institutional knowledge right before a major crisis.

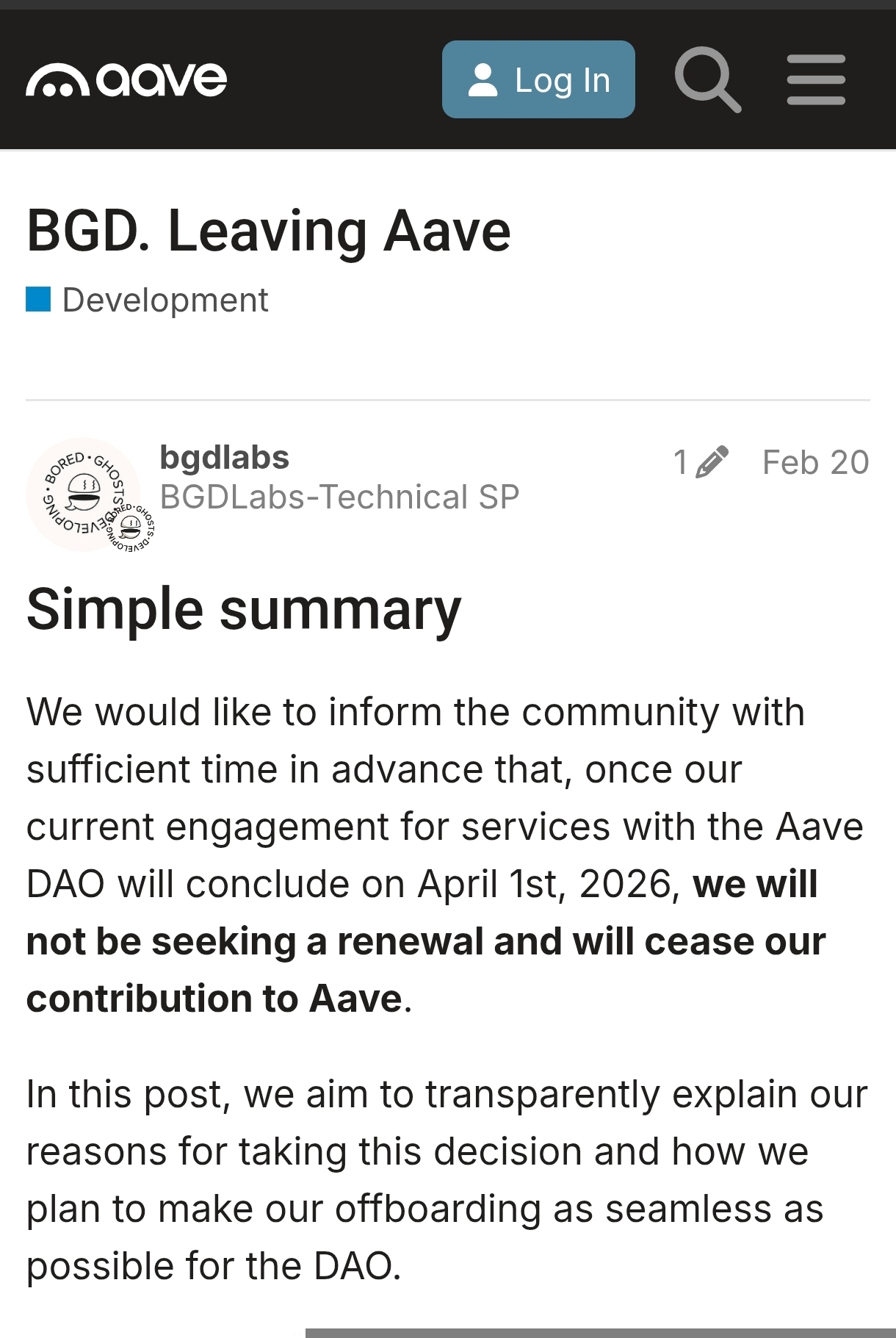

BGD Labs announced their exit first. They served as the primary technical development team responsible for building the massively profitable V3 codebase. They stated they would not seek a contract renewal when their term expired on April 1, 2026. BGD Labs cited profound disagreements about the future direction of the protocol. They experienced aggressive pressure from Aave Labs to focus entirely on the unproven V4 architecture. They felt Aave Labs unfairly criticized the highly stable V3 system to promote V4 features. They described V3 as a solid, future-proof system.

The Aave Chan Initiative followed shortly after. Zeller announced a four-month operational wind-down for the delegate platform. He pointed directly to the unaddressed conditions surrounding the departure of BGD Labs. He characterized the governance environment as a slow-motion coup. Zeller stated there was absolutely no role for an independent service provider when the largest budget recipient held undisclosed voting power and used it to approve their own massive proposals.

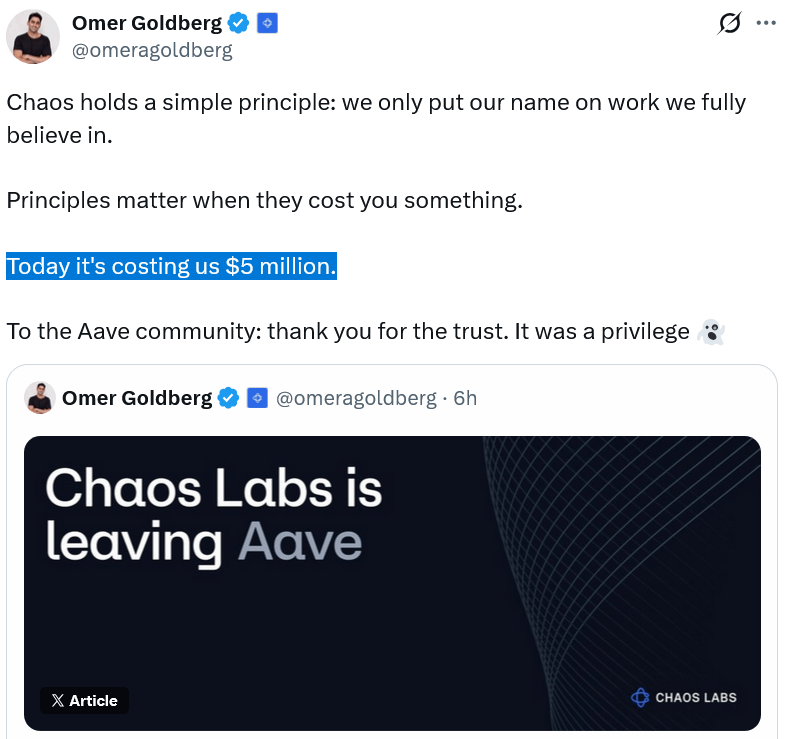

The most severe blow occurred on April 6, 2026. Chaos Labs terminated its primary risk management contract. They rejected an increased $5 million budget offer from Aave Labs. They chose to walk away proactively.

Omer Goldberg, founder of Chaos Labs, explained the departure in a detailed public statement. He cited a fundamental misalignment on exactly how risk should be prioritized and managed at an institutional scale.

The final decision rested on three specific factors:

Increased Workload: The exit of other core contributors materially increased the workload and the operational risk for the remaining service providers.

Expanded Liability: The V4 architecture radically expanded the scope of the risk function. It drastically increased the legal and operational burden. Chaos Labs explicitly stated they did not design the new architecture and would never have designed it that way.

Unsustainable Economics: Chaos Labs operated the Aave engagement at a financial loss for three straight years. Aave generated $142 million in annual revenue. Aave Labs secured a $50 million self-funding package. Chaos Labs received a $5 million offer. Goldberg stated they would still operate with negative margins even with the proposed increase. Traditional banks typically spend 6 to 10 percent of total revenue on risk and compliance. Aave was spending roughly 2 to 3.5 percent.

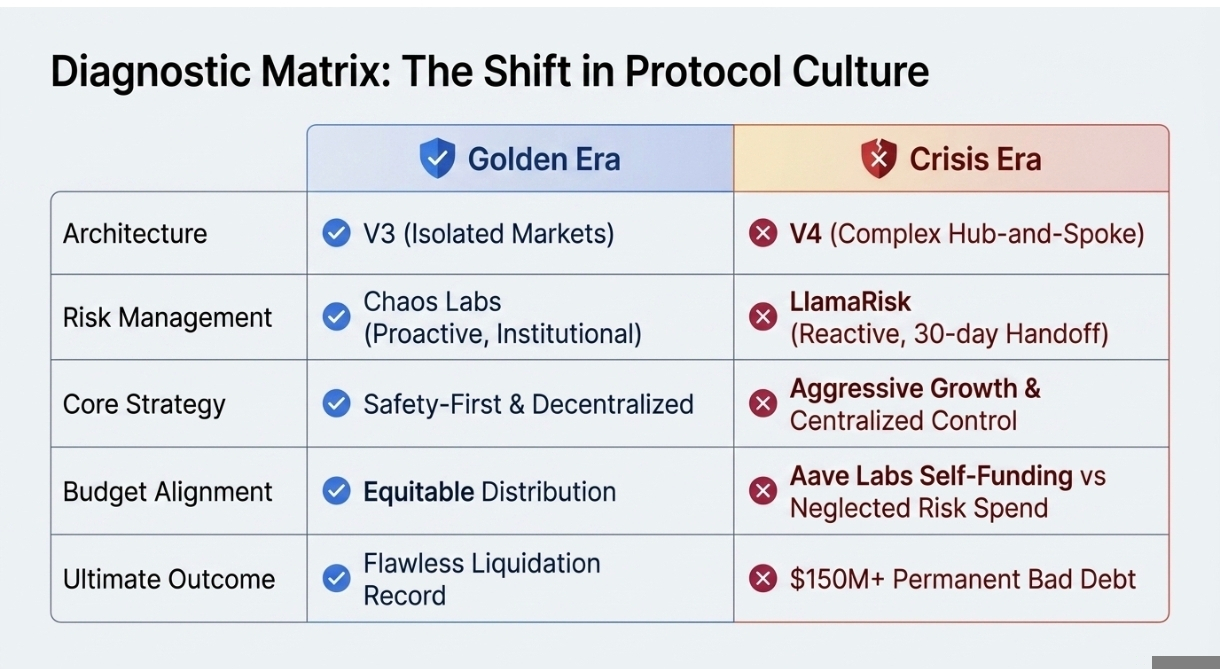

Aave transitioned the risk oversight duties to a secondary provider named LlamaRisk. They planned a standard 30-day handoff process. The protocol lost its most experienced risk analysts. The bespoke modeling infrastructure built by Chaos Labs vanished. This brain drain occurred just twelve days before the rsETH exploit tested the exact boundaries of the platform. Three days after taking over, LlamaRisk submitted a routine adjustment to raise the rsETH supply cap from 480,000 to 530,000 tokens. Nine days after that adjustment, the exploit occurred.

5. Technical Stress Tests:

The technical infrastructure began to fracture alongside the governance layer. Two distinct incidents in March 2026 served as severe warning signals. These glitches exposed massive vulnerabilities in external oracles and interface routing. They demonstrated that operational complexity was creating new failure modes.

5.1 The CAPO Oracle Glitch and Erroneous Liquidations

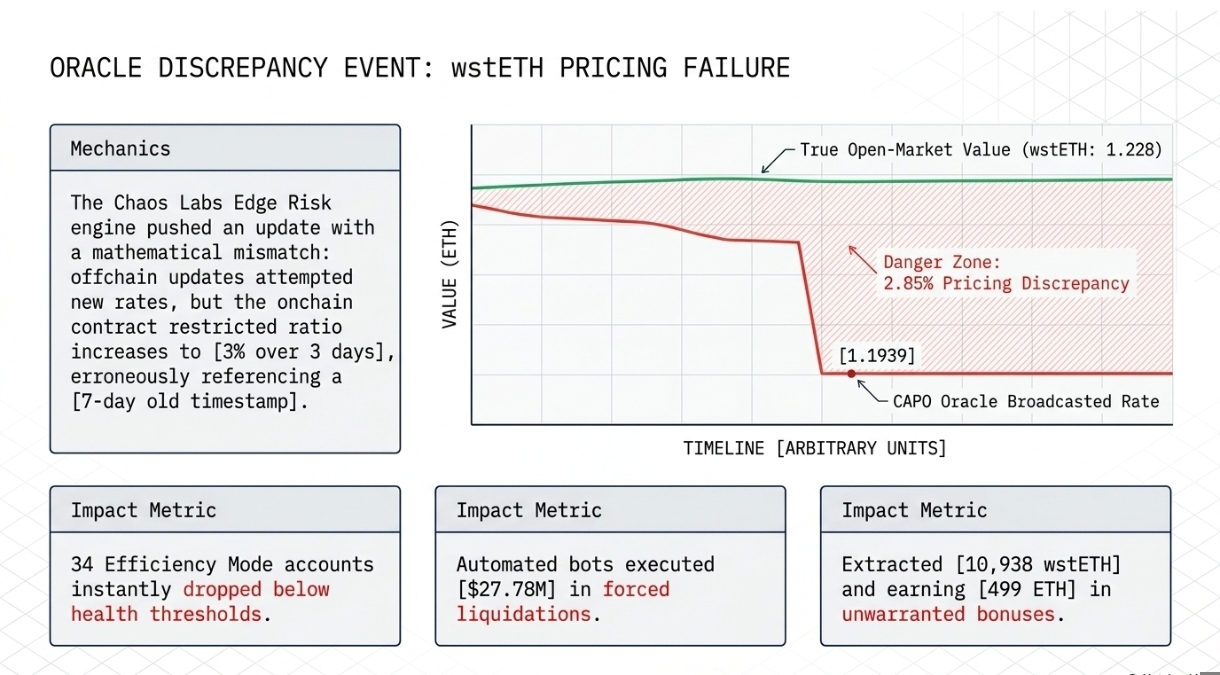

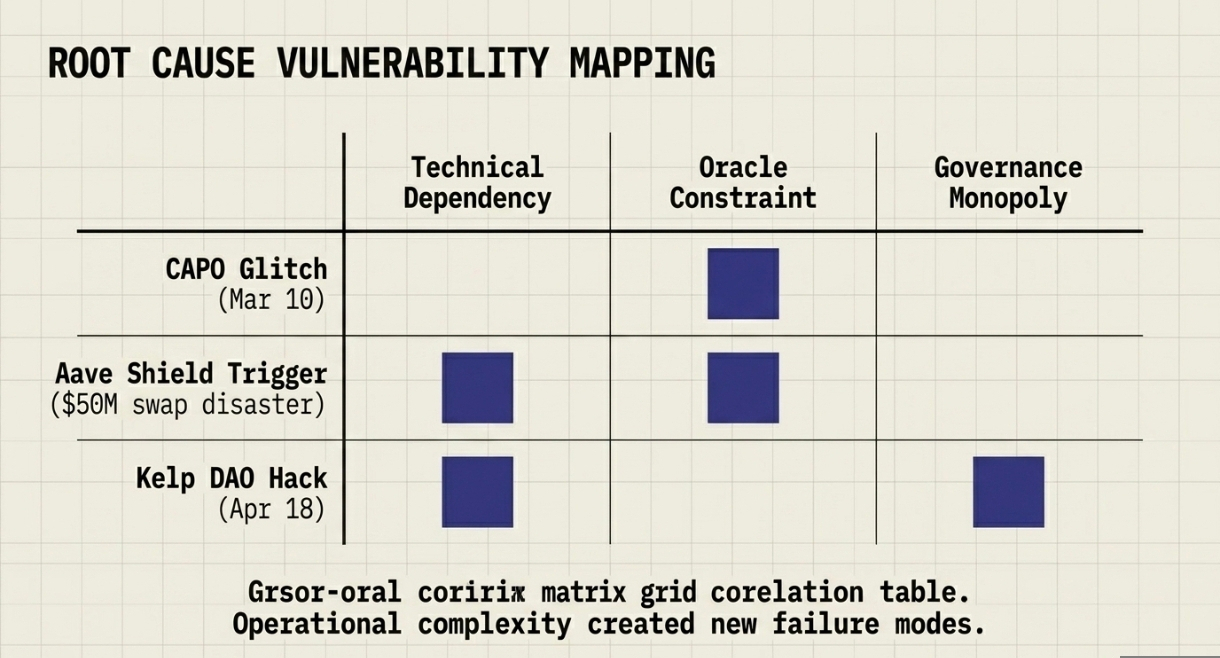

On March 10, 2026, a misconfiguration in the price feed system triggered a massive cascade of unwarranted liquidations. The failure originated entirely within the Collateral Asset Protection Oracle.

CAPO functions as a secondary safety mechanism. It acts as a strict guardrail against extreme market volatility and targeted oracle manipulation attacks. It monitors the market and explicitly caps the allowed price movements for closely related assets. It enforces a strict mathematical limit on how quickly a snapshot ratio can increase over a specific time window.

The Chaos Labs Edge Risk engine pushed a single parameter update on March 10. This update contained a mathematical mismatch between timestamp updates and the strict price ratio limits defined in the CAPO smart contract.

The offchain engine attempted to update the exchange rate. The onchain contract restricted the allowable ratio increase to a maximum of 3 percent over three days. However, the system erroneously continued to update the timestamp to a seven-day old reference point. This contradiction forced the system to calculate an artificially low exchange rate for wrapped staked ether. The oracle broadcasted an exchange rate of 1.1939 wstETH per ETH. The true open market value sat near 1.228.

This 2.85 percent pricing discrepancy devastated highly leveraged borrowers. The undervalued collateral caused 34 Efficiency Mode accounts to instantly slip below their health thresholds. Automated liquidation bots seized the collateral immediately. The bots executed $27.78 million in forced liquidations. They extracted 10,938 wstETH from innocent users. The bots earned approximately 499 ether in total value through liquidation bonuses and the raw pricing discrepancy.

The protocol incurred no bad debt. The smart contracts executed exactly as they were written. The event highlighted a terrifying vulnerability. The lending system depended entirely on incredibly complex oracle logic. A minor configuration error destroyed user portfolios in a single block. Risk stewards manually aligned the snapshot ratio to fix the issue. The DAO committed to full reimbursements using 141 ether in recovered funds supplemented by a maximum of 345 ether from the DAO treasury. The illusion of systemic safety dissolved.

5.2 The $50 Million Large Swap Disaster and Aave Shield

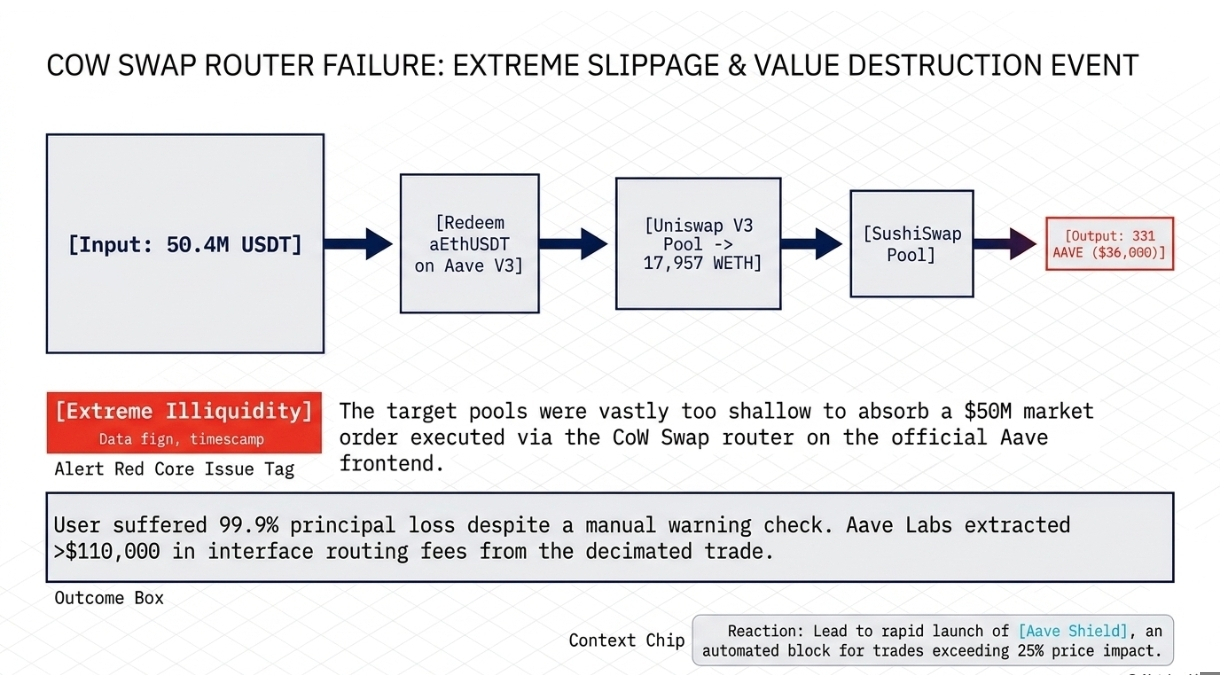

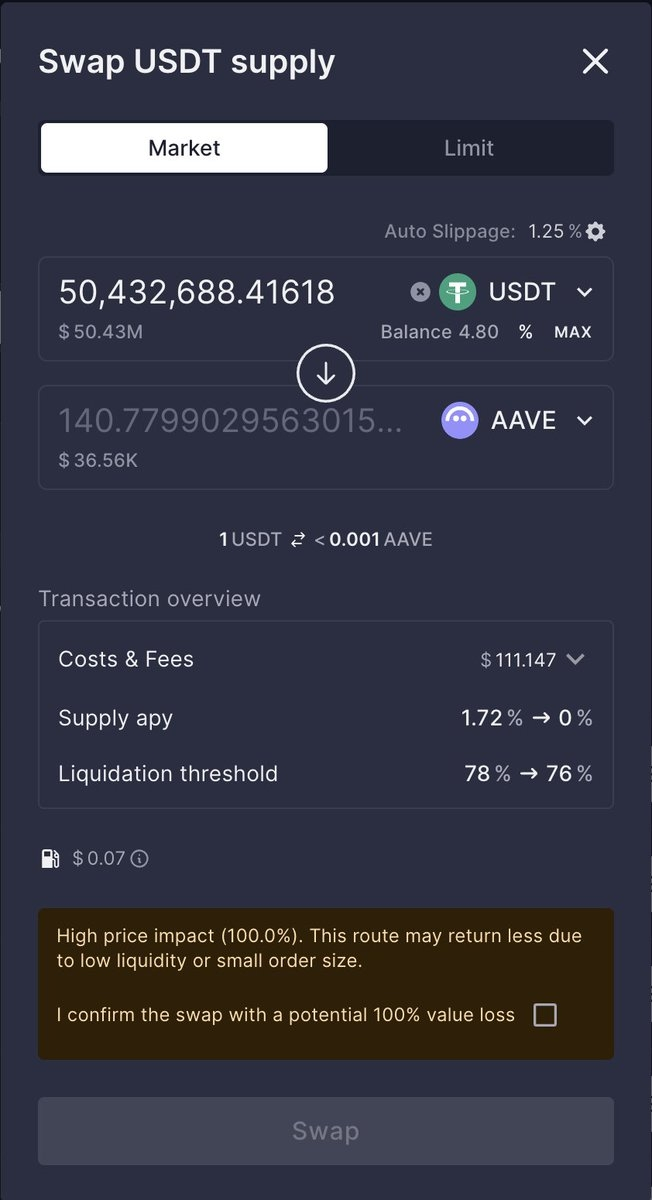

On March 12, 2026, the official protocol interface facilitated a disastrous retail trade. A user attempted to exchange 50.4 million USDT for AAVE tokens. They executed the trade directly through the CoW Swap router integrated into the Aave front end.

The trade broke down completely due to extreme market illiquidity. The complex routing path required the solver contract to redeem aEthUSDT for raw USDT on Aave V3. The solver pushed the funds through a Uniswap V3 pool to acquire roughly 17,957 WETH. Finally, it routed the WETH into a SushiSwap pool to purchase the AAVE tokens. The target liquidity pools were far too shallow to absorb a $50 million market order.

The interface displayed a severe warning. It showed a 99.9 percent price impact. It required the user to manually click a confirmation checkbox accepting a potential total loss. The user manually acknowledged the warning on a mobile device and executed the transaction.

The mathematical outcome was brutal. The $50.4 million converted into exactly 331 AAVE tokens. The trader received approximately $36,000 in value. They suffered a near-total loss of principal. Aave Labs extracted over $110,000 in interface routing fees from the decimated trade.

Developers rapidly launched the Aave Shield feature in response to the massive public backlash. Aave Shield acts as a proactive automated user protection mechanism. It integrates deep into the Aave interface routing system. It automatically blocks any token swap transaction that exhibits a projected price impact exceeding 25 percent. Advanced users must manually navigate to the settings menu to deliberately disable this safety feature before trading.

These incidents occurred during the peak of the governance instability. They happened exactly as the independent risk managers finalized their exit strategies. The glitches demonstrated that the external dependencies and interface logic were becoming highly fragile.

6. The Breaking Point:

The unaddressed vulnerabilities collided violently on April 18, 2026. A highly sophisticated attack utilized cross-chain infrastructure flaws to inflict unprecedented systemic damage upon Aave.

The crisis originated externally with Kelp DAO. Liquid restaking tokens allow users to deposit staked ether to earn native Ethereum yields plus EigenLayer service rewards. The protocol issues a liquid receipt token. For Kelp DAO, this specific token is rsETH. Users trade rsETH on decentralized exchanges. They deposit it into lending protocols like Aave to use as collateral to borrow entirely different assets.

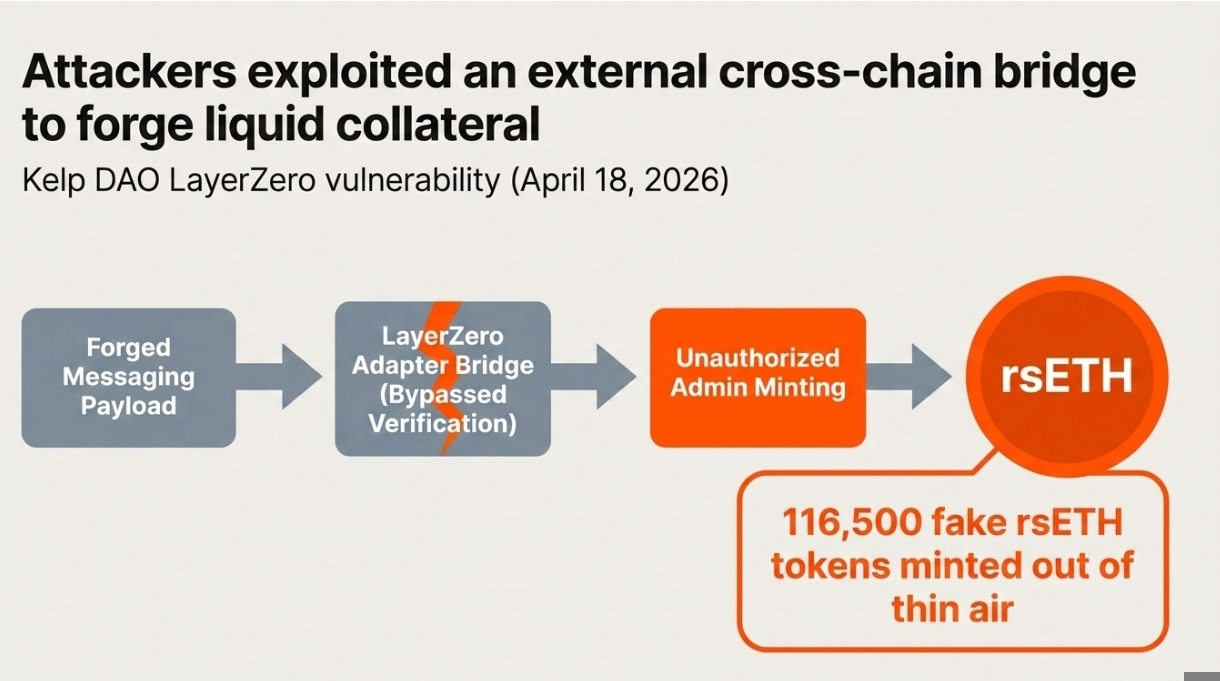

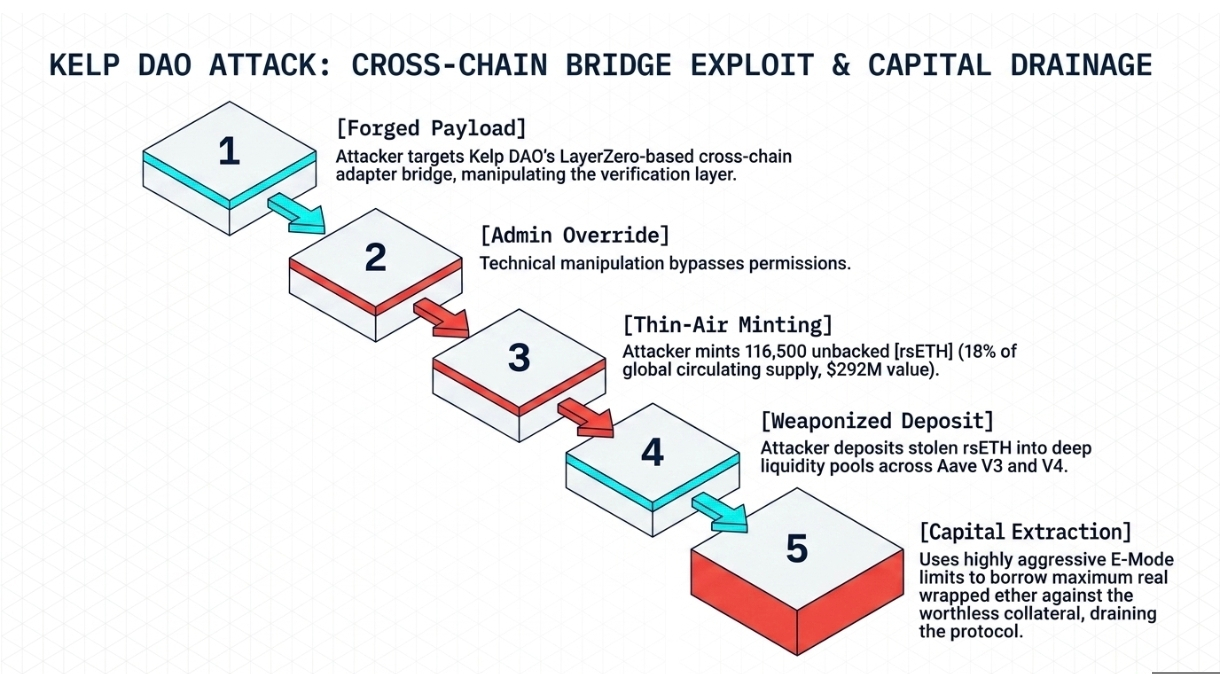

The exploit targeted the LayerZero-based cross-chain adapter bridge operated by Kelp DAO. The system relied on complex verification layers. Attackers utilized forged messaging payloads. They manipulated the verification layer of the bridge infrastructure to gain admin-level permissions. This technical manipulation allowed them to drain 116,500 rsETH tokens directly to an attacker-controlled wallet. This massive amount represented roughly 18 percent of the global circulating supply. The stolen tokens carried a value of over $292 million.

The attackers weaponized the stolen tokens immediately. They targeted the deep liquidity pools on Aave. They deposited the stolen rsETH as collateral across V3 and V4 deployments. They utilized Aave Efficiency Mode to maximize their capital extraction.

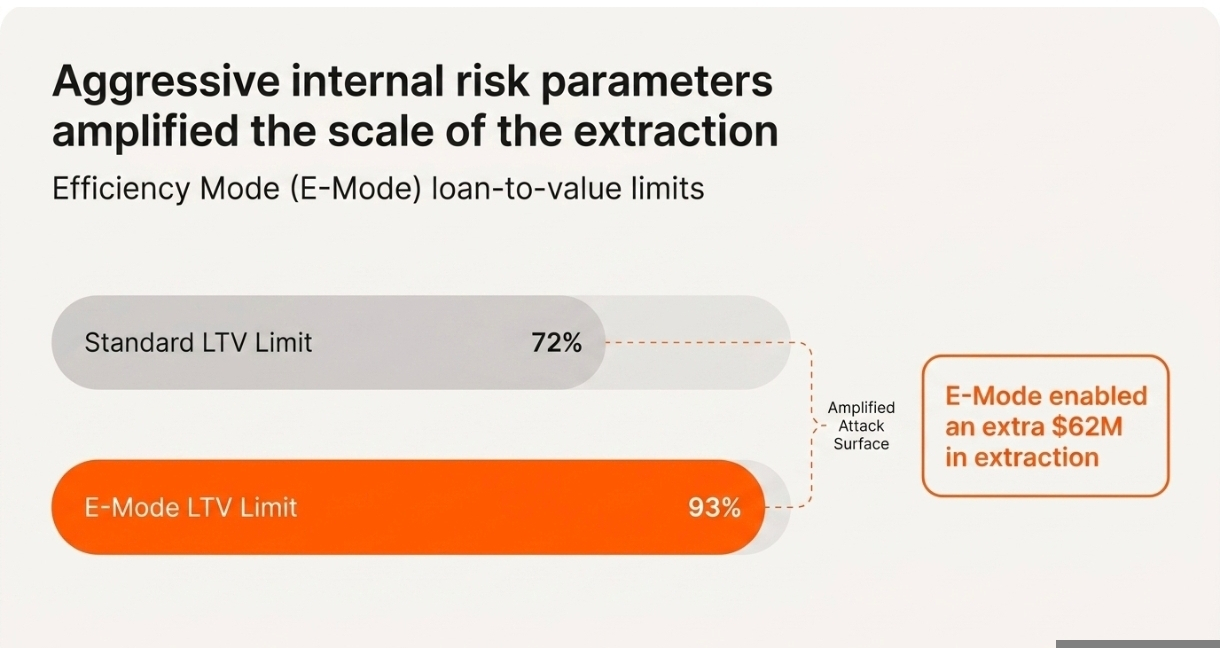

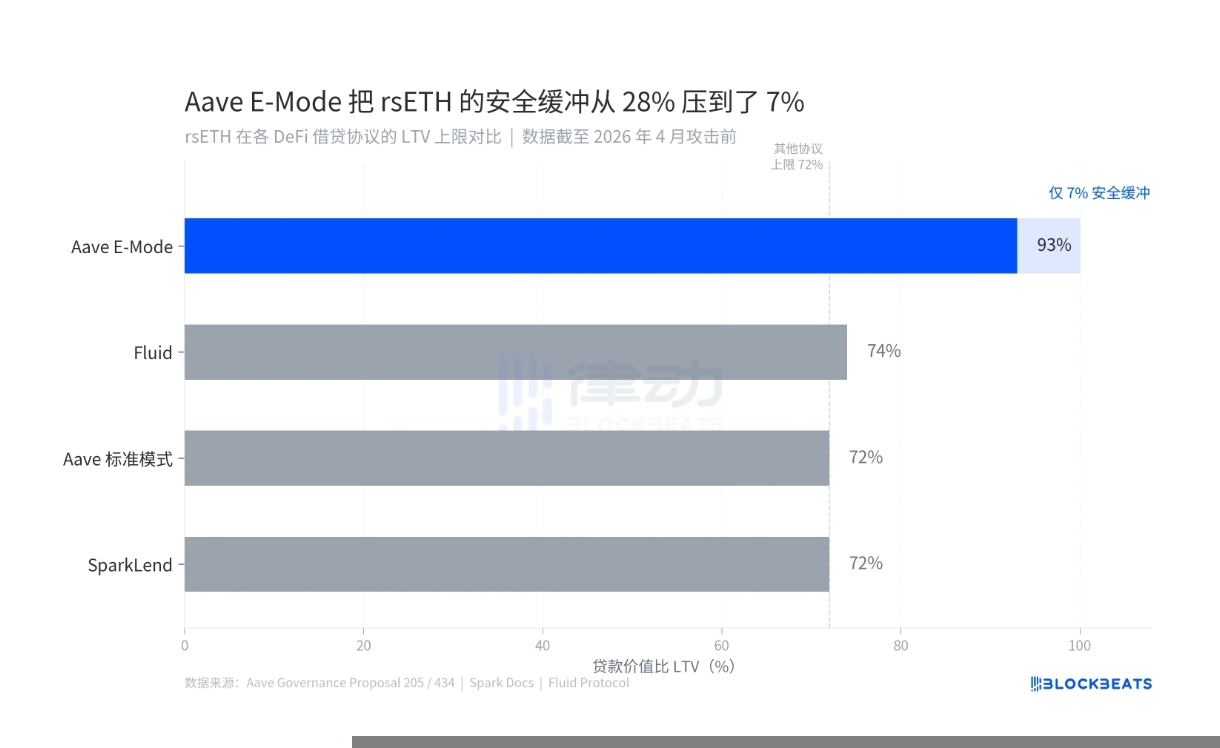

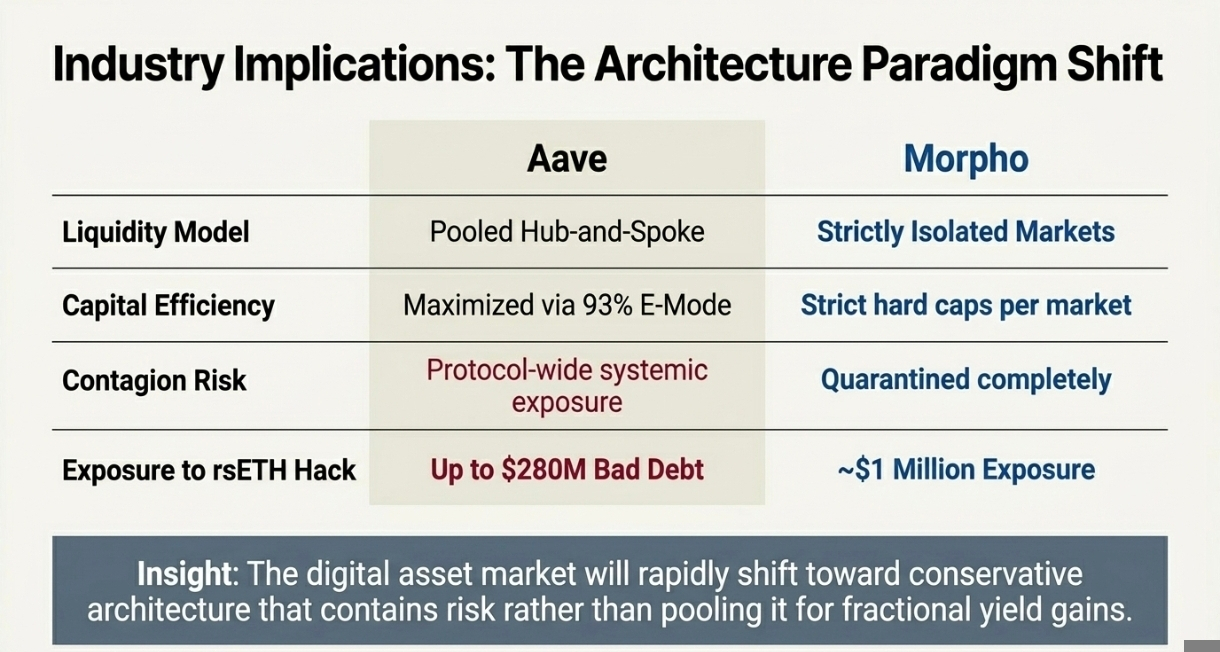

The protocol categorized rsETH as highly correlated to native ether. The E-Mode parameters permitted a 93 percent loan-to-value ratio. Under standard risk parameters, the borrowing limit would have been strictly capped at 72 percent.

This aggressive parameter allowed the attackers to borrow $272 million in WETH against the unbacked collateral. The 93 percent ratio enabled the extraction of $62 million more than a standard configuration would have permitted. The true market value of rsETH collapsed instantly following the hack. The internal Aave logic continued to view the devalued collateral at its old price. This delay locked the protocol into a massive deficit.

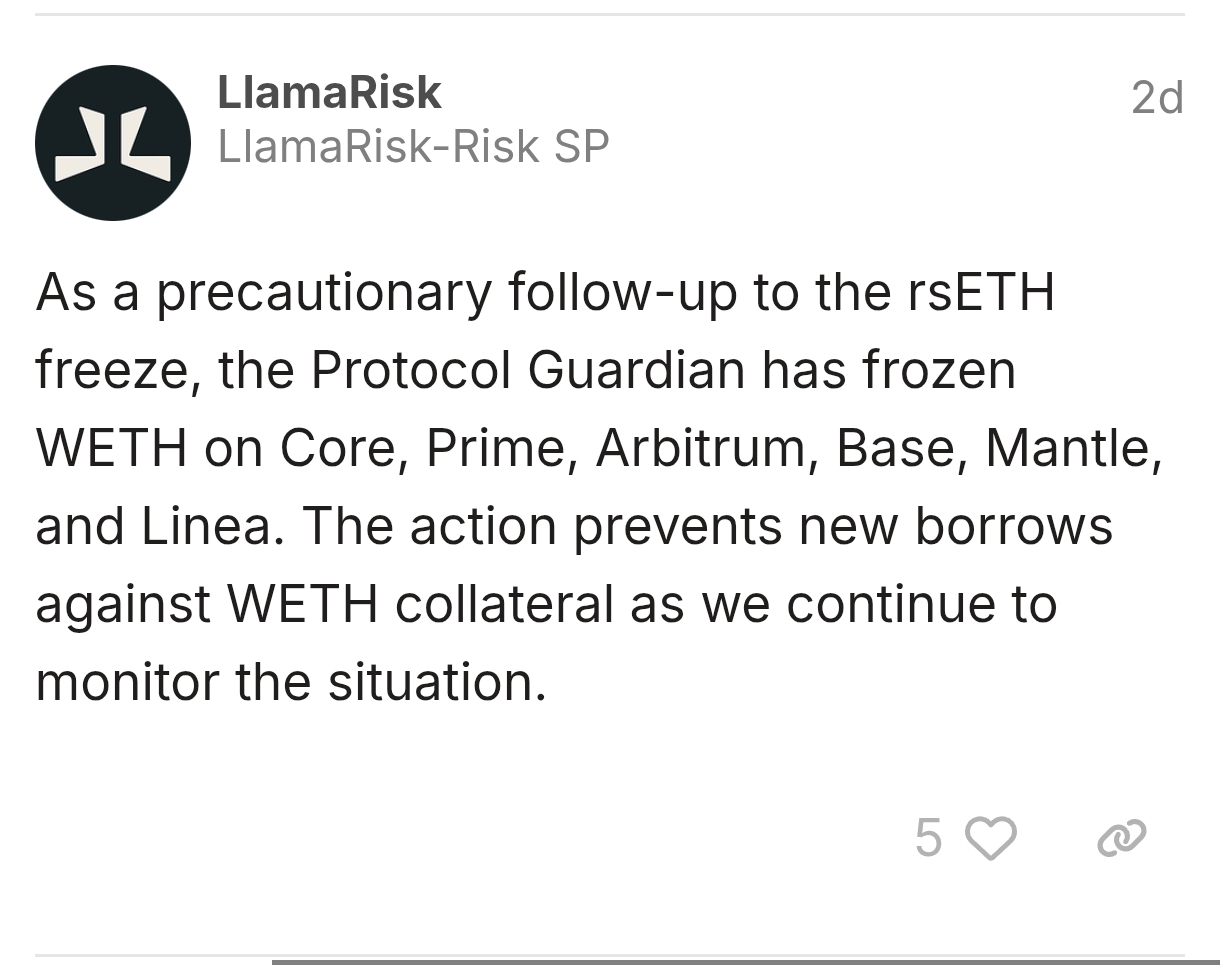

Aave absorbed massive amounts of worthless collateral. Estimates of the resulting bad debt ranged between $177 million and $280 million. The extraction pushed the utilization rate of the WETH pool to exactly 100 percent. Legitimate depositors could not withdraw their funds. Aave Guardians executed emergency protocols. They halted all rsETH and wrsETH markets across both V3 and V4 deployments to contain the contagion.

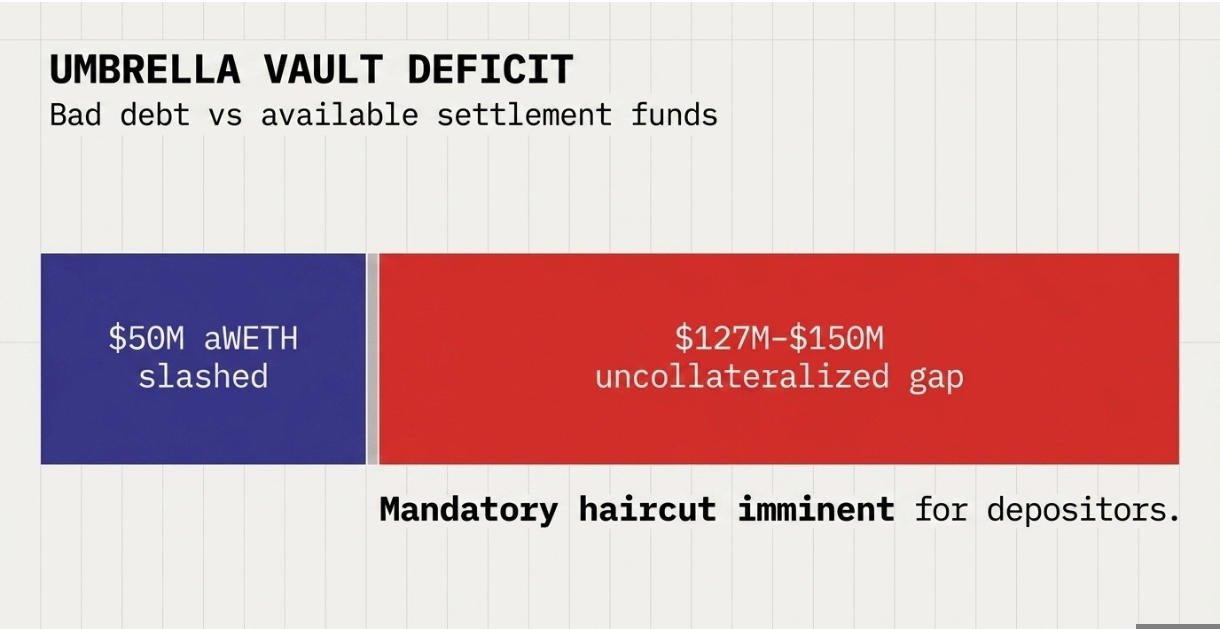

The protocol triggered the Umbrella settlement module. Umbrella is an automated onchain risk management system. It launched at the end of 2025 to replace the legacy Safety Module. It allows users to stake assets like aWETH into a safety vault to earn additional yield. The system automatically burns these staked assets to cover bad debt during a protocol deficit. It requires no governance vote. The withdrawal cooldown is set to 20 days.

Umbrella held only $50 million worth of staked aWETH available for immediate slashing. The protocol faced an unresolvable funding gap ranging from $127 million to $150 million.

The remaining deficit fell directly onto ordinary WETH depositors. Official protocol documentation states that once the Umbrella collateral assets burn completely, remaining WETH suppliers face a mandatory haircut. This signifies a permanent partial loss of principal deposits.

The core smart contracts of Aave executed flawlessly. The exploit originated entirely at the external Kelp DAO bridge. The aggressive internal parameterization of Aave facilitated the extraction of millions of dollars. The system demonstrated a fatal flaw in relying entirely on mathematical logic without conservative human oversight.

7. Root Causes and Systemic Lessons

The collapse of the Aave WETH markets followed a clear sequential causality. The initial governance conflict directly catalyzed the departure of the most experienced technical and risk management contributors. The exit of Chaos Labs removed the conservative oversight required to safely manage highly complex parameters. The 93 percent E-Mode limit required constant monitoring. Technical anomalies clearly signaled system degradation. The deployment of the V4 architecture continued unabated. The external Kelp DAO exploit simply utilized the existing Aave parameters to amplify the damage across the ecosystem.

The disaster exposes fundamental architectural flaws regarding permissionless risk limits. Efficiency Mode maximizes capital efficiency for perfectly correlated assets. Applying a 93 percent limit to a liquid restaking token represents a gross miscalculation of tail risk. The token relies on highly complex cross-chain messaging layers. The protocol treated wrapped restaked ether exactly the same as base layer ether. It entirely ignored the severe technological dependencies embedded within the asset. When the external LayerZero bridge failed, the correlation broke instantly.

The crisis highlights the deep tension between decentralization and coordinated safety. Aave Labs succeeded in consolidating token voting power. They passed the "Aave Will Win" proposal to centralize revenue and development focus. They optimized the protocol for rapid financial growth and brand uniformity. They dismantled the coordinated network of independent service providers. These providers supplied essential operational friction. Without organizations like BGD Labs and the Aave Chan Initiative to challenge assumptions publicly, the protocol became an echo chamber. It prioritized capital efficiency over survival.

The systemic reliance on highly complex oracles proved fatal. The CAPO glitch demonstrated that internal safety mechanisms misfire easily due to simple mathematical errors. The rsETH exploit proved definitively that Aave is only as secure as the weakest external protocol listed in its lending markets. This extreme composability acted as a rapid transmission vector for systemic collapse.

The threat landscape continues to expand rapidly. Security benchmarks demonstrate that artificial intelligence agents can now identify vulnerabilities in 92 percent of historical DeFi exploits. A purpose-built AI security agent performs far better than general-purpose coding models. Attackers will utilize these tools to aggressively target complex cross-chain dependencies in the future. The defense requires immense funding and dedicated human oversight.

8. What This Means for Aave, DeFi, and Beyond

Aave must navigate a brutal liquidity recovery process immediately. The resolution of the massive bad debt is the most critical challenge in protocol history. The WETH pool remains frozen at 100 percent utilization. The $150 million burden falls directly onto ordinary depositors. Forcing a severe haircut on retail and institutional users destroys the foundational premise of the platform. Trust breaks easily at this scale. Capital flight remains a permanent threat. Blockchain data already confirms a massive $5.4 billion ETH exodus.

The community will apply immense governance reform pressure. Token holders who supported the centralization of power must reckon with the consequences. The sharp decline in the AAVE token price reflects deep market skepticism. The DAO must decide whether to deploy massive amounts of treasury reserves to compensate victims or force the haircut on depositors. Reimbursing the lost funds will completely wipe out the revenue gains secured during the recent governance wars.

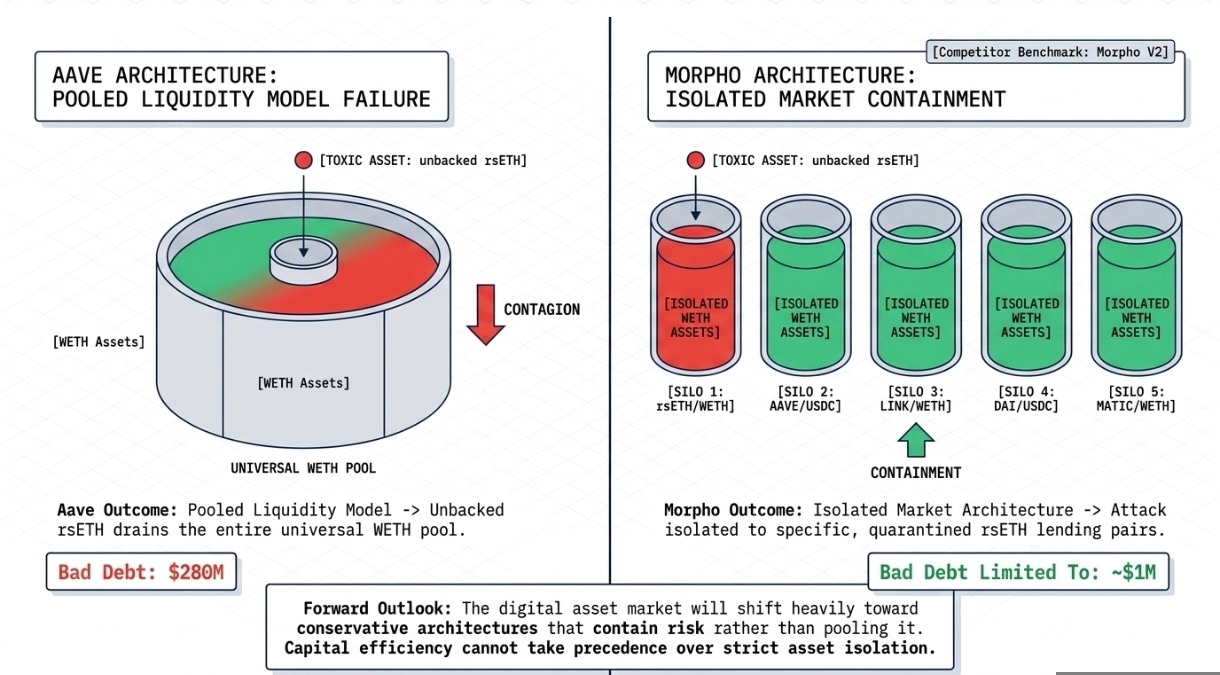

The crisis serves as a real-world stress test for the entire decentralized finance industry. The assumption that strict overcollateralization protects against all risks shattered completely. Protocols must reassess their cross-protocol risk awareness. Integrating liquid restaking tokens requires a fundamental redesign of risk parameters. Capital efficiency cannot take precedence over strict asset isolation mechanisms.

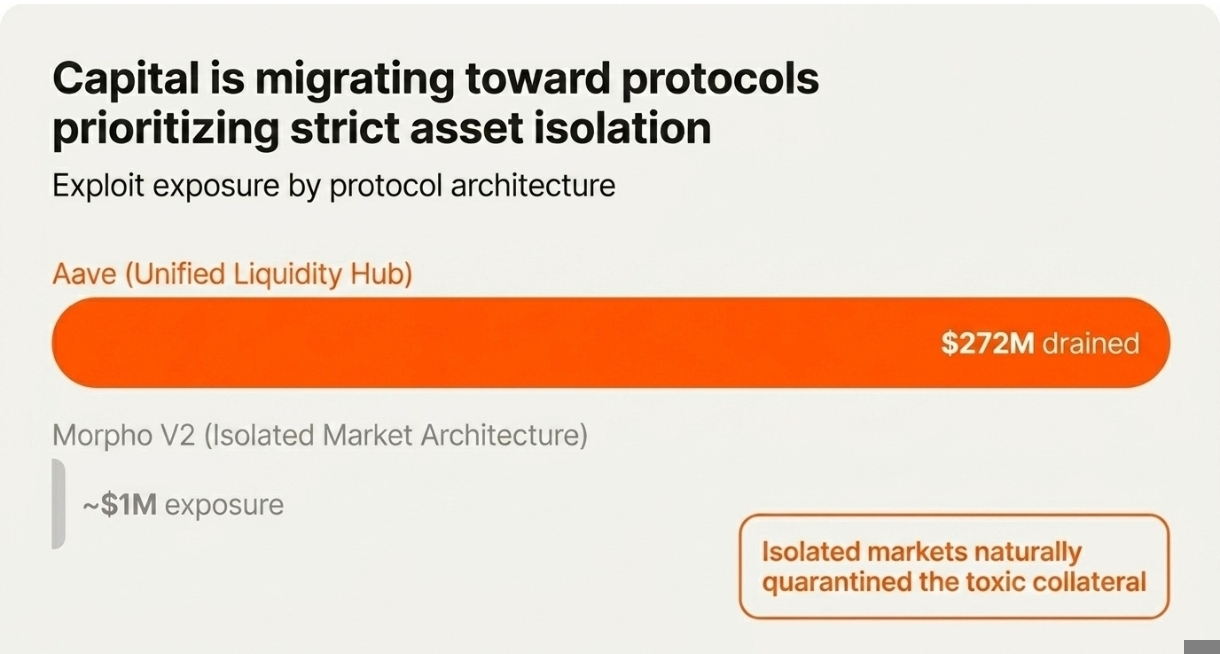

Competitor platforms that prioritize strict asset isolation will rapidly capture the fleeing market share. Morpho V2 utilizes an isolated market architecture. This specific design limited its exposure to the rsETH exploit to roughly $1 million. The digital asset market will shift heavily toward conservative architecture that contains risk rather than pooling it.

The financial structure of risk management requires a total overhaul. Traditional finance banks typically spend 6 to 10 percent of total revenue on risk and compliance. Aave generated $142 million in revenue but offered its risk manager only $5 million. Decentralized platforms must align their spending with the massive liabilities they carry.

9. So, What's Next ?

The catastrophic events spanning December 2025 to April 2026 illustrate systemic failure within a highly complex financial architecture. The chaos did not result from a single smart contract vulnerability. It was the predictable byproduct of an ecosystem prioritizing aggressive growth over fundamental resilience.

The warning signs were highly visible. The governance friction over CoW Swap fees started the chain reaction. The oracle glitches confirmed the technical stress. The departure of the primary risk stewards removed the final safety net. A bridge exploit provided the spark.

The "Aave Will Win" framework restructured the financial flow of the protocol. It ensured that branded product revenue accrued to the DAO while heavily funding the core development team. This economic victory means nothing when toxic collateral drains the underlying lending pools.

Rebuilding requires a total philosophical reset from the protocol leadership. The platform must return to a state of strict risk discipline. Extreme composability requires extreme isolation. Experimental assets belong in quarantined markets. The future viability of Aave depends entirely on restoring the critical alignment between developers, risk managers, and governance delegates. The protocol will remain inherently vulnerable until independent voices enforce conservative limits on untested assets.