The battle over a 20 billion valuation / Sports as a funnel for breaking into new markets / The ultimate moat in the agent era

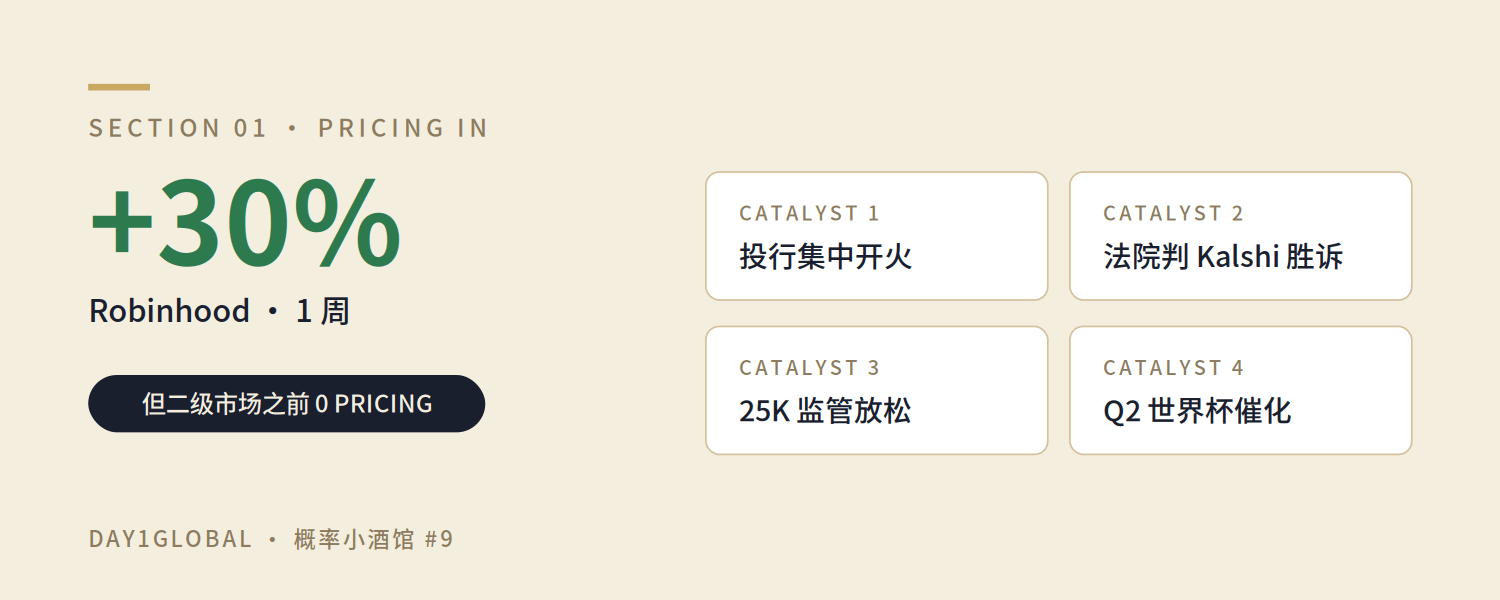

Over the past week, Robinhood$HOOD $HOODon Coinbase has risen by 30% cumulatively.$COINon It also rose accordingly.

Most people attribute this to "the continuation of the AI bull market" or "expectations of Fed easing." But if you talk to people on the front lines of the secondary market, you'll find that the real engine is actually the prediction market—a story that hasn't yet been seriously priced into by the secondary market.

In this episode of 【Probability Tavern】, we invited Zheng Di (General Manager Di), who has a dual background of seven or eight years in traditional financial securities firms and investment banking + Web3. He is one of the few guests who can thoroughly explain the logic of the cryptocurrency circle and the analysis of US stock companies.

We discussed six key questions surrounding the recent moves by Robinhood and Coinbase:

1️⃣ Behind Robinhood's 30% Surge: The Secondary Market Has Just Begun Pricing in Prediction Markets

2️⃣ Kalshi's stock price surged 80% in January: How did sports "save" Kalshi?

3️⃣ The battle for a $20 billion valuation: Kalshi vs Polymarket, who is more stable?

4️⃣ Robinhood vs Coinbase: Who is the biggest beneficiary of the prediction market?

5️⃣ Two Ways Out for CEXs + The "Killer Weapon" of Tokenization in US Stocks

6️⃣ The Ultimate Moat in the Agent Era: Community and Narrative

Finally, here are a few of my own takeaways.

The full audio version can be listened to by searching for "Day1Global Podcast" on Day1Global, Apple Podcasts, and Spotify.

1️⃣ Behind Robinhood's 30% Surge: The Secondary Market Has Just Begun Pricing in Prediction Markets

In the past week, Robinhood rose 10 points in a single day, and another 5 points in pre-market trading; Coinbase also followed suit with a few points of increase.

The immediate trigger was two Wall Street reports:

Cantor Fitzgerald (backed by the investment bank long helmed by current U.S. Commerce Secretary Howard Lutnick) released a report specifically naming Coinbase and Robinhood, arguing that they are "the best way to participate in predicting market booms."

Bernstein followed suit, giving Robinhood a price target of $130.

Mr. Di's on-site assessment was that, prior to last night, the secondary market had almost no pricing in this prediction market story.

The reason is simple—when Robinhood's stock price fell recently, the company propped it up with share buybacks, not with institutional bargain hunting. If the market truly believed in the story of predicting the market, the valuation wouldn't be so flat.

So why are investment banks launching their offensives at this particular time? Mr. Di identified three catalysts:

Macroeconomic conditions are improving: Expectations of war with Iran are cooling; the AI theme has expanded from Nvidia to optical, electronic, storage, nebula, and computing power sectors, and pro-cyclical assets are beginning to be revalued.

Fundamental BreakthroughThe Third Circuit Court of Appeals just ruled in favor of Kalshi, classifying the sports contract as a swap (equity swap) rather than betting—this is a major positive for the prediction market industry (more on that later).

Second-quarter catalysts: The World Cup and the US midterm elections are two major factors that will drive up betting activity in the second quarter. Sports betting typically begins 2-3 months in advance.

But neither Polymarket nor Kalshia are publicly listed yet, so if the secondary market wants to buy into this story, Robinhood is the only direct target left—which is why investment banks have to bring it to the forefront.

Dill added an extra piece of good news: US regulators have just relaxed the frequency limits for intraday trading for accounts with less than $25,000. Robinhood's average account balance is exactly $12,000, making it almost a perfect fit.

💡 Key Takeaways: Investment bank report + court ruling + regulatory easing + World Cup catalyst – four positive factors combined, but the market hadn't priced them in at all. This is the first wave of market narrative revaluation in the secondary market.

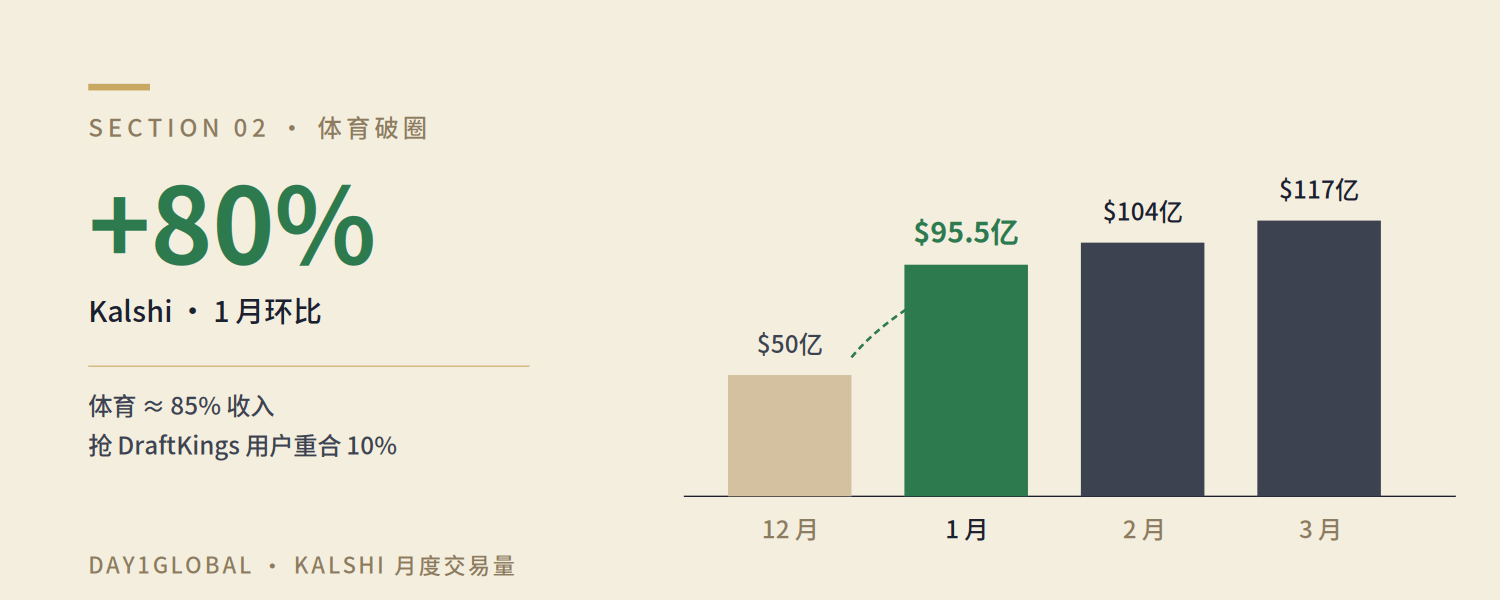

2️⃣ Kalshi's stock price surged 80% in January: How did sports "save" Kalshi?

Kalshi is a company that was actually quite unfamiliar to people in the cryptocurrency circle in the past—because it does 100% of its business in the United States and has no offshore operations.

But if you trade US stocks, you'll be very familiar with it, because for a long period last year, Robinhood contributed 50% of Kalshi's trading volume.

The turning point is in January 2025. Kalshi's monthly trading volume data:

December: Over 5 billion US dollars

January: US$9.55 billion (up 80% month-over-month)

February: ~10.4 billion US dollars

March: Further Growth

Why was January so intense? Mr. Di's speculation and analysis:

The first reason was that "they had to generate numbers." Kalshi was closing a funding round with a valuation of $22 billion at the time and had to prove to investors that "even if Robinhood leaves, I can still grow on my own." So, the investment in marketing on Twitter and in the sports section was pushed to the limit.

The second layer is a structural change—Kalshi is stealing users from DraftKings. A third-party survey in January of this year showed that Kalshi and DraftKings had a user overlap of up to 10%. This is a very alarming number, because it means that traditional sports betting users are being siphoned off by the prediction market.

Direct evidence is that sports betting companies like DraftKings have established a lobby group (PAC) to fund legislation against prediction markets. Reports from major banks like Merrill Lynch have even characterized DraftKings as a "continuous target for shorting"—shorting it on every rebound because prediction markets will keep it under pressure.

The third layer is Kalshi's "all-or-nothing" gamble. After the 2024 presidential election, Kalshi found that most of the traffic from political futures was lost—you can't have a presidential election every day. So it simply went all in on sports.

The result is a comparison of the current income structure:

Kalshi: Sports account for ~85-90% (Echo data shows approximately 85%)

PolymarketThe market is divided into three parts: sports (~40%), cryptocurrency (~33%), and politics (~30%).

💡 Key InsightsSports are the true "breakthrough funnel" for the prediction market. It's not because sports themselves are particularly attractive, but because sports offer daily matches and weekly major events, providing a stable source of liquidity and customer acquisition. Political futures are like a "family reunion dinner," while sports are like a "daily meal."

This echoes a judgment that CEO Di has repeatedly emphasized: true large-scale adoption must rely on sports, because it represents the largest entry point for the global population willing to bet on sports events daily. Once these people are included, cross-selling crypto, political, and esports becomes much easier.

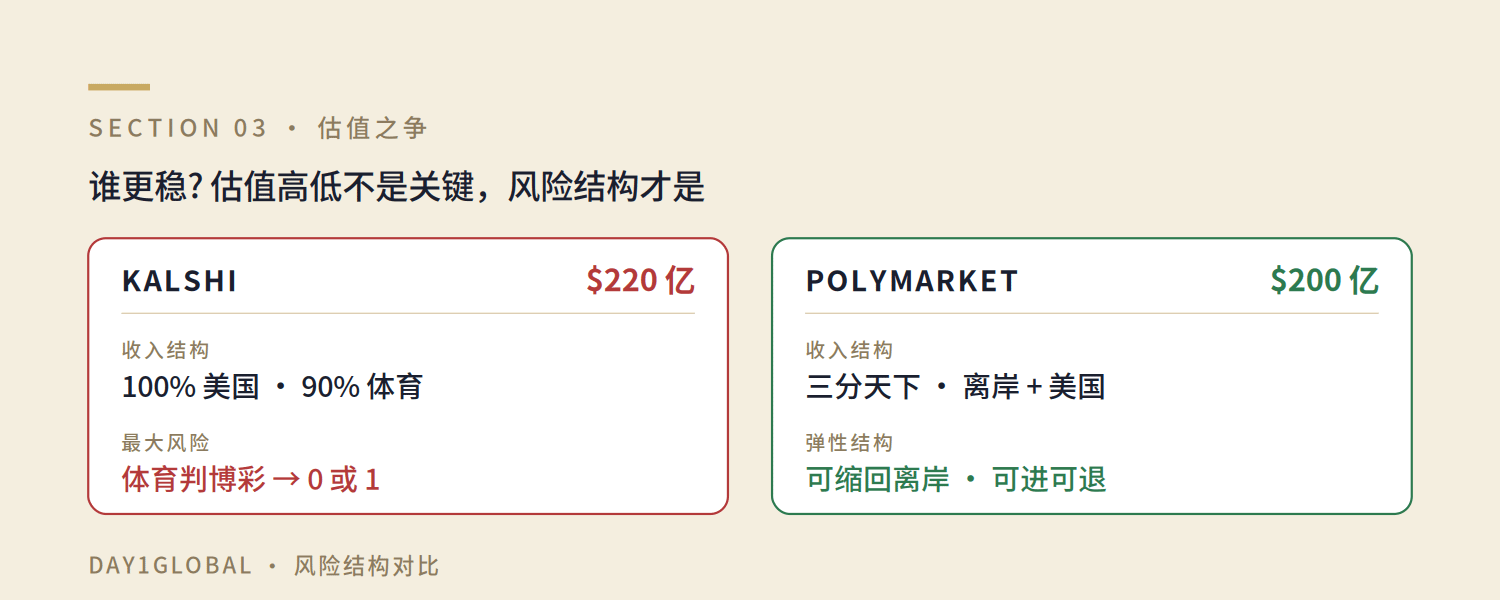

3️⃣ The battle for a $20 billion valuation: Kalshi vs Polymarket, who is more stable?

Current valuation and pricing:

Kalshi: Latest round of funding: $22 billion

Polymarket: Rumored to be preparing for a new round of financing with a valuation of $20 billion.

In comparison: ICE's investment in OKX valued the company at $25 billion in this round.

With valuations of 20 billion, 22 billion, and 25 billion, which is overvalued and which is undervalued?

Mr. Di's core point is that if we only look at market prediction, he prefers Polymarket. The reason is not that Polymarket is more aggressive, but that it is both offensive and defensive.

Let's examine the risk structures of the two companies:

Kalshi (22 billion):

100% dependent on the United States

85-90% dependent on sports

High flexibility but concentrated risk

If the Supreme Court ultimately classifies sports contracts as gambling (under state law), it becomes a "0 or 1" question.

Polymarket ($20 billion):

Almost entirely offshore (only now "returning to the United States").

Income split into three parts

Flexible options – retreat offshore if things go wrong with the US.

Here we need to add the two fronts of regulation:

Frontline 1: Is sports gambling?

This is the biggest compliance issue in the prediction market. If a sports contract is classified as "gambling," it falls under the jurisdiction of individual states (there are more than 50 states in the US, and each state requires a license); if it is classified as a "financial product/equity swap," it falls under the jurisdiction of the federal CFTC.

The CFTC is now strongly supporting prediction markets. The Third Circuit Court of Appeals just ruled in favor of Kalshi from a "textualist" perspective—classifying it as a swap. But the state government won't be satisfied and will likely take it all the way to the Supreme Court.

Front Two: Insider Trading

This is a more sensitive issue. For example:

The market knew in advance about the US military's capture of Maduro—clearly, the soldiers involved in the operation placed their own bets.

The Israel Defense Forces have arrested several soldiers who were betting at Polymarket.

On the night of the Khamenei incident: the probability of him being attacked was consistently over 30%, but surged to 70% by 7 PM. Kalshi later cancelled the bet (citing the reason that "we bet on his removal from office, not on his life or death"), and the winners, who received $30-40 million, threatened to sue Kalshi; Polymarket did not refund the money.

Di's chilling version is: with the probability jumping from 30% to 70%, could the only people betting on it be those in the Revolutionary Guard who received the news first? That's why market predictions are so accurate—"there are moles everywhere."

Conversely, however, rigorous investigations into insider trading have become one of the main points of attack used by US lawmakers to criticize prediction markets—"If you allow insider trading, you are endangering US national security." That's a serious accusation.

Therefore, if the Democrats sweep at least one or even two houses of Congress in the midterm elections, it will pose significant uncertainty for prediction markets and regulatory legislation on sports contracts. Kalshi, with its $22 billion valuation, will be far less resilient than Polymarket in this scenario.

💡 Key takeaway: Valuation level isn't the key factor; risk structure is. Kalshi is a double-edged sword—a win can lead to a surge, a loss can wipe out everything; Polymarket offers a diversified portfolio with insurance.

4️⃣ Robinhood vs Coinbase: Who is the biggest beneficiary of the prediction market?

Although the reports by Cantor and Bernstein named both companies, Di's assessment is that Robinhood benefits more than Coinbase.

There are three reasons:

The first layer is the difference at the user level.

Robinhood's user base is getting wealthier—the average net worth per user has increased from a few thousand dollars to $12,000. While Robinhood's user growth last year was only in the single digits, its strong performance indicates it's effectively leveraging its existing user base.

Coinbase's user base is getting poorer—most retail investors who traded altcoins in the past two or three years are now bankrupt. Aside from those stubbornly holding onto Bitcoin, even ETH has suffered significant losses.

More importantly, online brokerages can poach users from centralized exchanges (CEXs), but CEXs can't poach users from brokerages. Robinhood and Futu already support cryptocurrency trading, but it's hard to imagine someone who trades US stocks opening a Coinbase account specifically for altcoins.

The second layer is the conflict of brand identity.

Coinbase's core narrative, built before 2020, was "safe, stable, institutionalized, and with a blue-blooded image." After its 2020 IPO, it listed a large number of altcoins to boost revenue, which has been criticized as "Binance-izing." Now, it suddenly wants to add prediction markets, a product with strong gambling attributes, which conflicts with its original image of "institutional friendliness" and stability, leaving long-time users confused.

Since Robinhood is YOLO's home base, its market predictions actually fit its image very well.

The third layer is product rhythm.

Robinhood, unwilling to be merely a distribution channel for Kalshi ("held hostage"), acquired a licensee, MIAXdx, rebranded it as Rothera, and prepared to build its own platform. Originally planned for Q1, the launch has now been postponed to Q2 or the second half of the year. Kalshi is also clearly moving away from Robinhood – Robinhood's share of Kalshi's transaction volume has dropped from 50% to 1/4-1/5.

💡 Di's assessment: Robinhood building its own platform is highly probable—it won't be content to be just a conduit. OKX has already accepted investment from ICE, which is a major shareholder of Polymarket. From a group strategy perspective, OKX receiving liquidity from Polymarket makes more sense than building its own platform.

Here's an interesting detail: Mr. Di specifically mentioned that Coinbase's most valuable asset is actually Circle, not Coinbase's own market predictions.

5️⃣ Two Ways Out for CEXs + The "Killer Weapon" of Tokenization in US Stocks

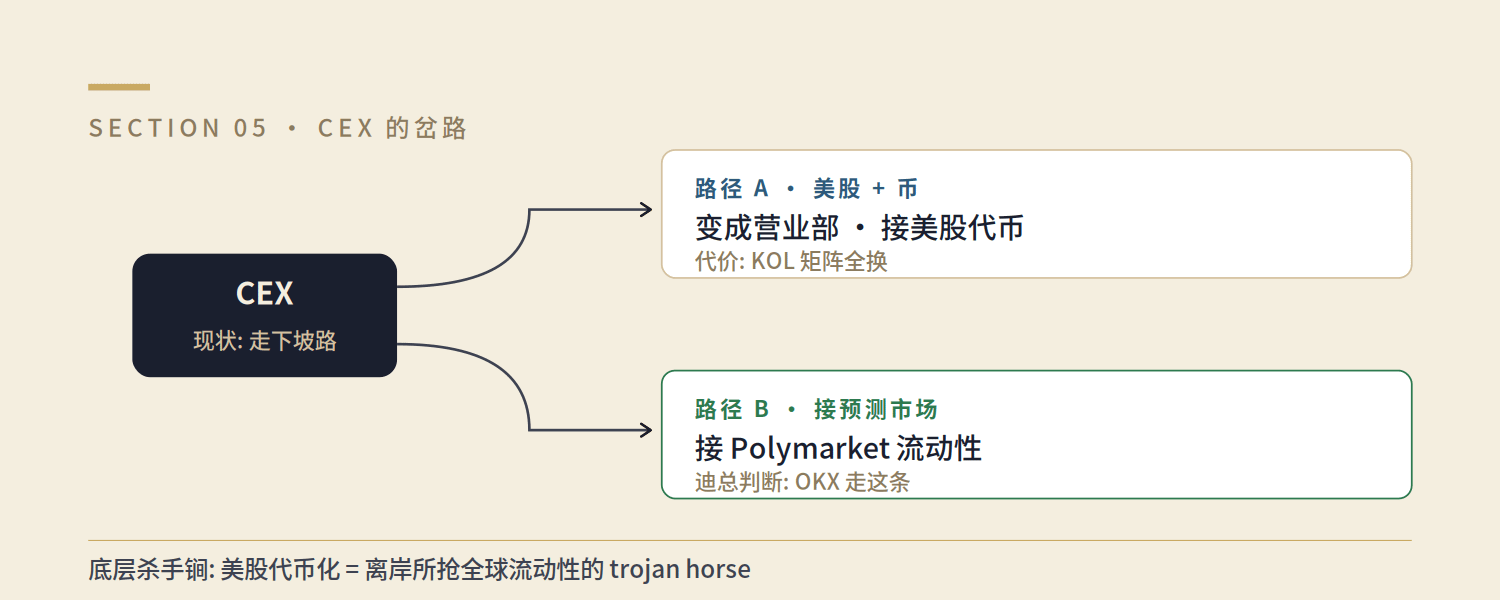

Mr. Di made a rather radical prediction: "CEXs as a whole have already started to decline. Prediction markets are the next generation of CEXs, and they will be many times stronger, because prediction markets may be the true 'exchange for everything'."

The core reason for the decline of CEXs is that their competitors are no longer other CEXs, but full-featured brokerages like Robinhood and Futu. Futu and Robinhood can steal users from Coinbase, Binance, and OKX, while CEXs cannot compete with brokerages.

So what's the way out for CEXs? CEO Di gave two options:

Solution 1: Become an exchange combining "US stocks + cryptocurrencies"

However, this path has a hidden cost—the entire KOL matrix needs to be rebuilt. The current KOLs on CEXs are all from the cryptocurrency circle; to operate in the US stock market, a new batch of US stock market KOLs is needed, meaning a major overhaul of the internal team is required. This is a major undertaking.

Solution Two: Respond to Market Predictions

You can either build your own platform or connect to the liquidity of Polymarket/Kalshi. But building your own platform has a major problem—who will provide the liquidity? It's difficult for a new platform to attract market makers from the start. Polymarket's pools are already deep enough, and most retail investors will prioritize trading on platforms with good liquidity.

This leads to a very important macroeconomic judgment—US stock tokenization is the key to offshore companies seizing global liquidity.

Mr. Di's logic chain is as follows:

The SEC's "open strategy" is to push the entire US financial system onto the blockchain.

Very few people worldwide know how to use Web3 wallets to trade US stocks on DeFi protocols.

However, there are many people around the world who are accustomed to trading cryptocurrencies on centralized exchanges (CEXs).

Once CEXs make it easy to trade US stocks and cryptocurrencies, a large influx of new users will come.

The pain point is that Futu, Webull, Tiger Brokers, and IB are all currently making it very difficult for Chinese users to open new accounts; OKX and Bybit, on the other hand, allow easy account opening.

If Nasdaq and NYSE's official US stock tokens are launched in Q3 or before the end of this year, offshore exchanges like OKX will directly become "overseas branches of US stocks".

Di's next prediction is that CEXs, securities firms, and prediction markets will eventually become "brokerage firms"—competing on who has more private domain users and stronger communities. In the agent era, this judgment becomes even more important—more on that below.

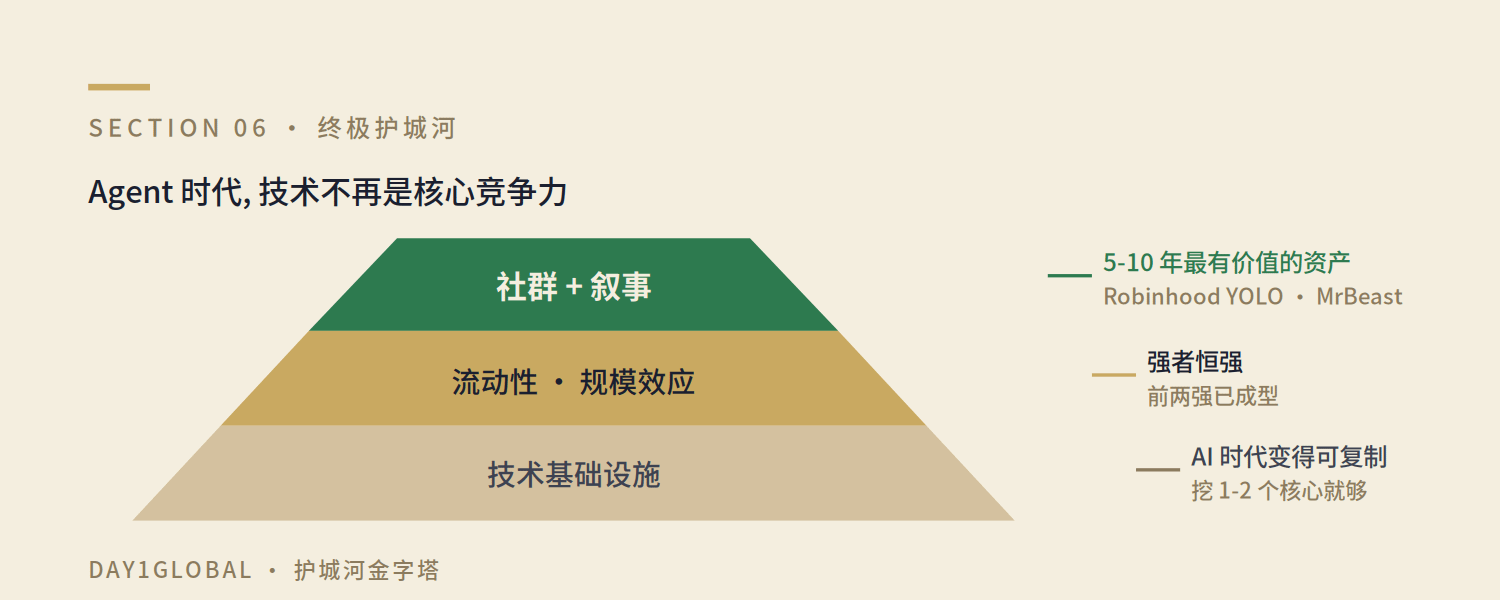

6️⃣ The Ultimate Moat in the Agent Era: Community and Narrative

This part is the one that impressed me the most in the whole episode.

Di's core argument is that, on a 5-10 year timeframe, technology is not a core competitive advantage.

The reason is:

In the era of Vibe Coding, one or two core technical personnel, along with AI programming skills, can replace an entire IT team.

The replication of abilities has become extremely easy.

When the Agent era arrives, all apps will disappear. Users will place orders by calling APIs using Agents, and small companies will be able to switch clients seamlessly—simply by changing the API.

So what becomes the core competitiveness? Community.

Why should you trade with me? Because I have a community, KOLs, and the "secret to wealth."

Cheap rates are useless if you can't make money; even the lowest rates are useless.

The Matthew effect is snowballing.

Mr. Di cited the example of Tom Lee (Fundstrat) investing in MrBeast's Beast Industry—valued at $200-300 million—which he sees as the "Robinhood of the Gen Z era." He believes that community is the most valuable asset in the next 5-10 years.

Extending from this, we see the power of narrative. Robinhood's greatest narrative weapon isn't actually "financial equality," but rather:

"You only live once"——YOLO

Robinhood's true underlying narrative is:"I'll lead you retail investors against Wall Street."All products (Pre-IPO, prediction markets, crypto, 24-hour trading) are extensions of this narrative.

Similar narratives include:

Zhipu = The Chinese version of Anthropic: Di Zong said that many people who buy Zhipu don't look at the financial statements because "according to its P/E and ARR, it's actually more expensive than Anthropic and OpenAI." But the narrative won.

The GME short squeeze myth: Subsequent investigations revealed that many "retail investor" posts on Reddit were actually fake posts from hedge fund firms. Following this, US hedge funds introduced a new requirement for hiring researchers—"proficiency in Reddit."

Allbirds transforms into a GPU companyThe stock surged 180% pre-market, transforming from a carbon-based bird to a silicon-based bird.

💡 Di's insightful quote: "In the end, what prevails in this world are various narratives. The truth of the matter is one thing, but you need to know what the mainstream narrative is—people don't believe the truth, they only believe the narrative."

My understanding / Take Aways

After listening to this episode, I've compiled 5 takeaways:

1. Prediction markets are not a track, but a paradigm shift in infrastructure.

The valuations of Kalshi at $22 billion and Polymarket at $20 billion seem expensive if viewed solely from the perspective of "event-based derivatives exchanges." However, if you accept the assertion that "prediction markets are the next generation of exchanges for everything," then it's a different story. This aligns with the logic of the five levels from A to E in my previous article, "Are Prediction Markets the Next ByteDance? A Breakdown of the 100 Billion Market Cap Model."

2. Alpha in the secondary market lies in "carrying on the story".

Before Robinhood's 30% surge, the secondary market had virtually no pricing in prediction markets. This suggests that for ordinary investors, focusing on the speed of narrative evolution in the primary market might be more advantageous than focusing on secondary market financial reports. Polymarket and Kalshi are not yet publicly listed, but their stories have already begun to revalue related assets in the secondary market—this is a window of opportunity for ordinary investors to benefit from beta.

3. Sports are a funnel for breaking into new circles, but the risks are concentrated on Kalshi.

Kalshi's 90% sports + 100% American background is a double-edged sword. If the Supreme Court ultimately rules that the sports contract is a swap, Kalshi will be incredibly powerful; but if it rules that it's gambling, it's a zero-sum risk. Polymarket's diversified structure is more stable amid the political uncertainty of the midterm elections.

4. CEX's next step: to integrate "US stocks + cryptocurrencies" and connect with prediction markets.

If you hold assets related to Binance, OKX, or Coinbase, this presents you with a choice between two options. OKX's acquisition of ICE investment and Polymarket liquidity is a logical path—it has chosen a coordinated approach.

5. In the agent era, bet on "companies with communities," not "companies with technology."

If you agree that all apps will be replaced by agents in 5-10 years, then companies with strong communities like Robinhood, Futu, Reddit, and MrBeast Industry will have a stronger competitive advantage than companies with only technology. This also echoes my previous optimism about X/xAI—X is already one of Musk's most important private community assets.

Finally, a personal reflection: Di's judgment that "facts are one thing, narrative is another" is particularly enlightening for content creators. If your content only conveys facts, it will be replaced by AI; but if your content shapes a narrative and builds a community, its moat will be very deep.

Listen to the full version

The full audio version (1 hour 2 minutes) can be listened to on the following platforms:

🎧 Search for 【Day1Global Podcast】 on Apple Podcasts and Spotify

📺 Search for 【Day1Global】 on YouTube.

【Probability Tavern】 is a live broadcast program on X and YouTube by Day1Global. Each episode invites builders, players, and analysts in the prediction market field to discuss hot news and investments. Due to the sensitivity of some topics, all past episodes are available in the playlist on the YouTube channel.

If you'd like to be among the first to see our in-depth analysis of Polymarket, Kalshi, Robinhood, Coinbase, and other similar projects, you're welcome to join our paid community, "Tea Room." See web3brand.io for details.

📌 Disclaimer: All discussions in this article are for informational purposes and sharing of thoughts only, and do not constitute any investment advice. All valuations and data mentioned are from podcast guest discussions or publicly available information and may differ from real-time data. Please be sure to DYOR.