For a long time, my criteria for determining whether a token was worth staking was pretty simple: is the APR high? If I thought the APR was high, I figured there'd be returns, and staking meant making profits. It wasn't until much later that I realized this standard only scratched the surface.

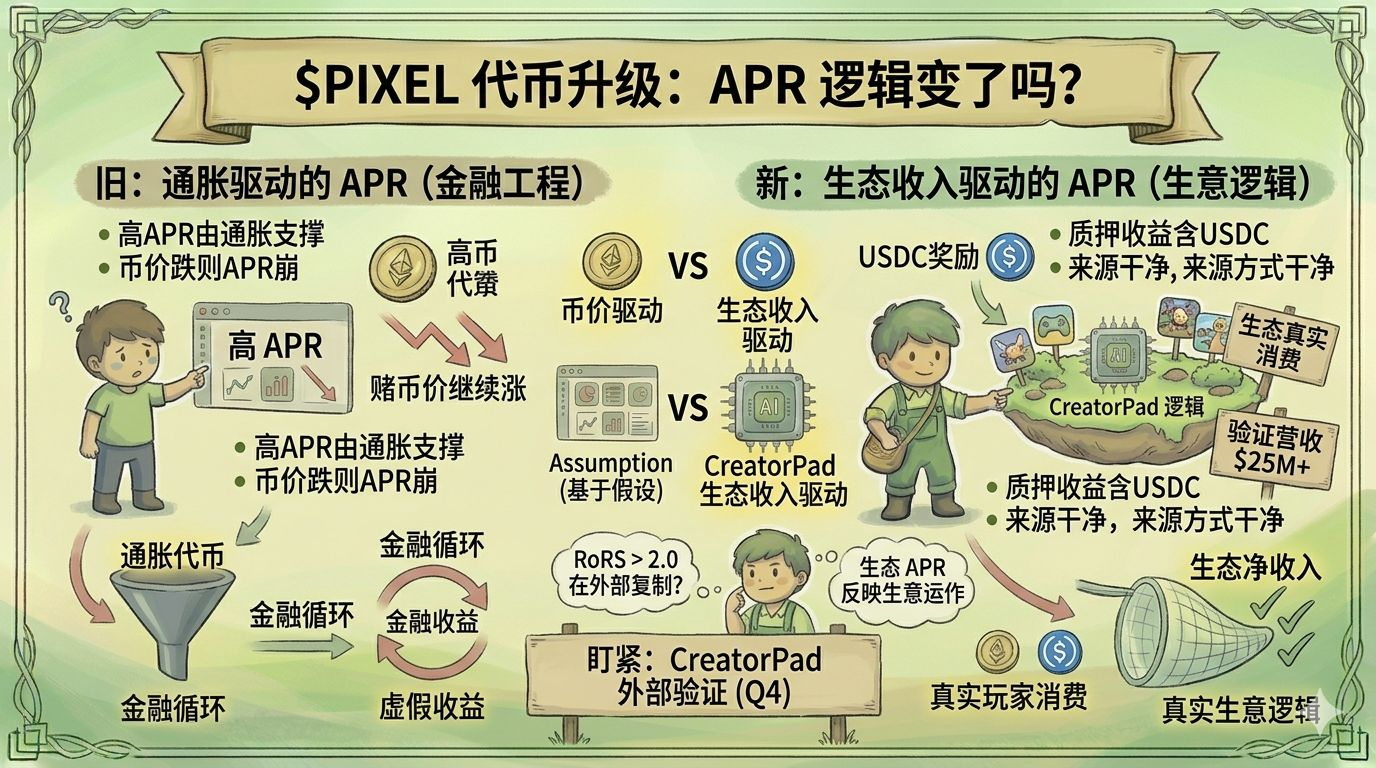

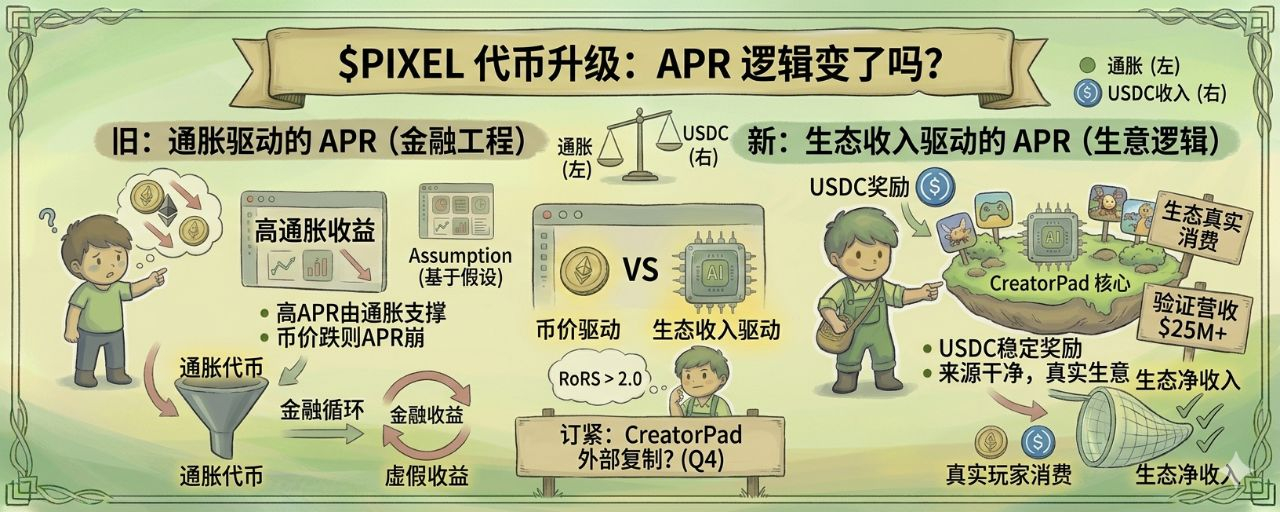

Most P2E tokens' staking APRs sound high, but in reality, most of it is just inflation propping things up. This isn't a problem with any specific project; it's a structural flaw. When the token price goes up, the APR looks good, but when the price drops, the APR crashes alongside it. Essentially, users who stake are betting on the token price continuing to rise, rather than because the system itself offers real returns.

$PIXEL After the token upgrade, this logic had an exception.

On the day the USDC incentives launched, I looked at the staking data, originally wanting to find the APR number, but I saw something else: the composition of the APR. In staking returns, how much comes from price inflation, and how much comes from actual consumption income. These two sources look completely different on the data dashboard.

After the USDC incentives went live, the staking APR for $PIXEL no longer solely depended on price volatility. A significant portion of the APR now comes from actual consumption income in the ecosystem (USDC rewards), which is stable and won't disappear with price fluctuations.

These two APRs are not the same thing. A high price-driven APR means 'the token inflation rate is high, and those willing to stake are betting on the price continuing to rise'. An eco-driven APR means 'this system is genuinely operating, retained players are truly consuming, and stakers are sharing a portion of the ecosystem's income'.

The former is financial engineering, while the latter is business logic.

Why is this distinction important?

Once the APR turned into eco-driven income, its value began to have reference significance—it's not just about 'is anyone willing to lock up tokens', but rather 'is this ecosystem actually generating real revenue'.

I checked some data: $PIXEL's current market cap is about $25 million, corresponding to $25M+ revenue generated internally by CreatorPad. This $25M+ is the real consumption income generated by this ecosystem, and it has been validated. After CreatorPad goes live and integrates across games, whether this income can continue to grow is what we need to keep an eye on next.

As stakers, what should we be monitoring next?

After the official launch of CreatorPad, watch the growth rate of the USDC reward pool. In May, there will be a token unlock (89.36M PIXEL), and the changes in staking data before and after the unlock will also be a monitoring window. If the APR share from the USDC reward part is increasing, it indicates that the ecosystem is genuinely expanding. If it stalls, it means we haven't passed the external validation test yet.

I'm not saying this logic is perfect. Before the official launch of CreatorPad, the $25M+ was a number generated internally by Pixels. What stakers can do now is to monitor whether this number can be replicated in external games. I won't make that judgment now; we need to wait for external data to speak.