Stablecoins have undergone a quiet but powerful transformation. Once seen merely as a utility for crypto traders, they are now positioning themselves as a foundational layer of the global financial system. Recent insights from Andreessen Horowitz (a16z crypto) highlight how regulation, usage patterns, and market structure are accelerating this shift.

Let’s break down what’s actually happening beneath the surface.

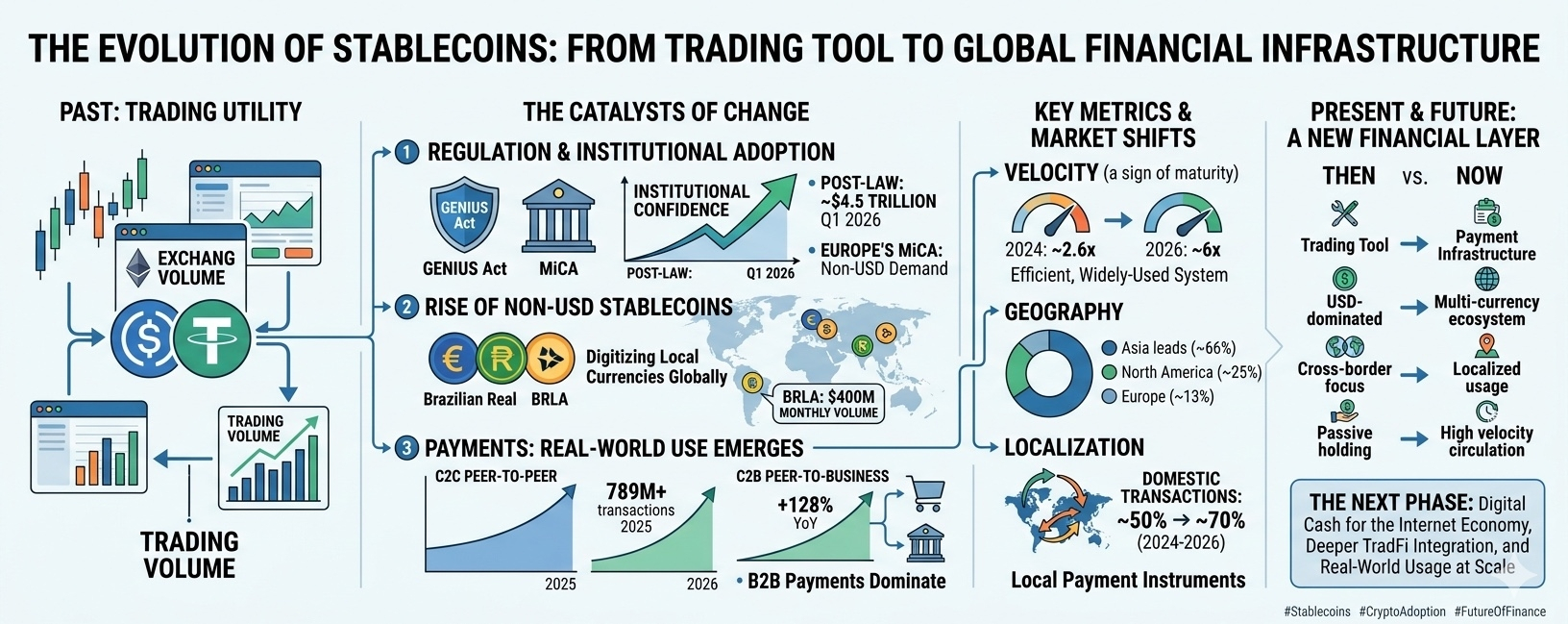

1. Regulation: From Uncertainty to Acceleration

For years, regulatory ambiguity kept major institutional players on the sidelines. That dynamic is now changing.

The introduction of the GENIUS Act marks a turning point. Rather than creating the trend, regulation is amplifying existing momentum.

Before the law: steady growth in trading volume

After implementation: surge to ~$4.5 trillion in Q1 2026

This signals something critical:

Institutional confidence follows regulatory clarity.

In parallel, Europe’s Markets in Crypto-Assets Regulation (MiCA) reshaped market structure by forcing compliance-driven changes, including delistings of non-compliant assets like Tether in certain regions.

The result?

A new demand wave for non-USD stablecoins, proving regulation doesn’t kill innovation—it redirects it.

2. Rise of Non-USD Stablecoins

Historically, stablecoins have been dominated by USD-backed assets. That dominance still exists—but cracks are forming.

MiCA and regional financial needs are driving the growth of alternatives:

Euro-backed stablecoins in Europe

Real-backed assets like BRLA in Brazil

BRLA’s growth—from near zero to $400M monthly volume—shows how local currencies + blockchain rails can unlock adoption.

Key insight:

Stablecoins are no longer just exporting the US dollar—they are digitizing local currencies globally.

3. Payments: The Real Use Case Is Emerging

The biggest misconception?

That stablecoins are mainly for trading.

That narrative is breaking down.

C2C Still Dominates — But C2B Is Exploding

Peer-to-peer (C2C): largest volume (789M+ transactions in 2025)

Peer-to-business (C2B): fastest growth (+128% YoY)

This indicates a transition:

From speculative usage → real-world economic activity

4. Stablecoin Cards and Spending Infrastructure

Payment infrastructure is evolving rapidly.

Projects using card rails (e.g., Etherfi Cash, Kast, Wallbit) are enabling users to:

Hold stablecoins

Spend them seamlessly in real-world transactions

Collateral deposits surged from near zero to $300M/month.

Even though these are technically collateral systems, the implication is clear:

Stablecoins are integrating into everyday financial behavior.

5. Velocity: A Sign of a Mature Network

One of the most overlooked metrics is velocity—how often each unit of money is used.

2024: ~2.6x

2026: ~6x

This nearly 2x increase signals:

Higher demand than supply growth

More active usage, not passive holding

In traditional finance, high velocity is a hallmark of:

Efficient, widely-used payment systems

6. Shift in Transaction Structure

If you strip away trading and DeFi mechanics, something interesting appears:

Estimated real payment volume: $350B–$550B annually

B2B payments dominate

This is crucial.

Businesses are:

Paying suppliers

Settling invoices

Managing treasury flows

All using stablecoins.

Translation:

Stablecoins are quietly entering the backbone of commerce.

7. Geography: Asia Leads the Charge

Stablecoin adoption is not evenly distributed.

Asia: ~66% of volume (Singapore, Hong Kong, Japan)

North America: ~25%

Europe: ~13%

Others: minimal

Asia’s dominance reflects:

Faster fintech adoption

Higher demand for digital dollar alternatives

Strong trading + payment ecosystems

8. Localization Over Globalization

Stablecoins were originally seen as cross-border tools.

That narrative is fading.

Domestic transactions: ~50% → ~70% (2024–2026)

Cross-border share: declining

This signals a major shift:

Stablecoins are becoming local payment instruments built on global rails.

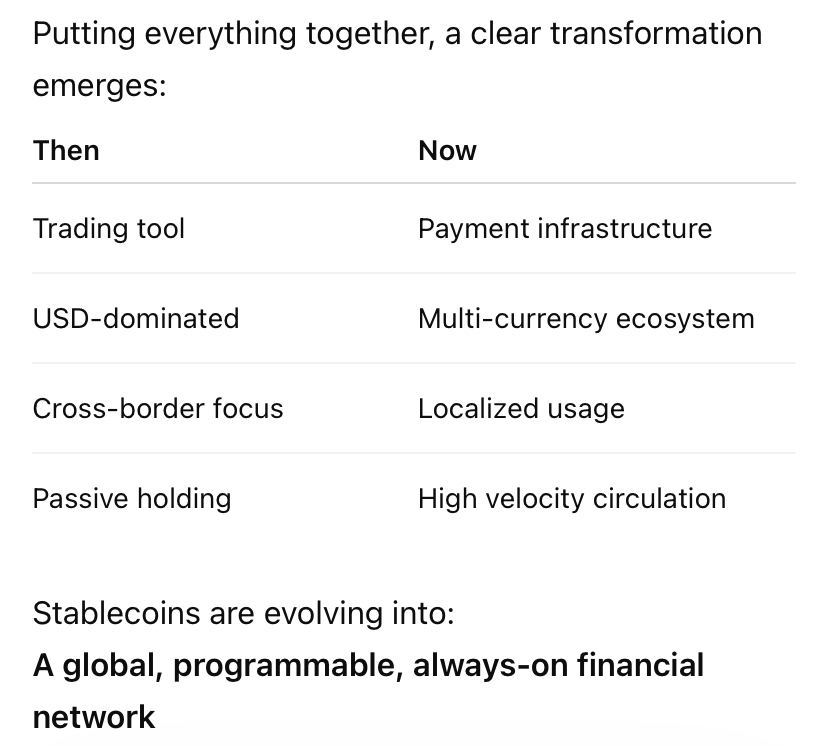

9. The Bigger Picture: A New Financial Layer

Final Takeaway

The data challenges the popular narrative.

Stablecoins are not just:

A hedge

A trading pair

A remittance tool

They are becoming:

Digital cash for the internet economy

Still early—but the direction is no longer unclear.

The next phase will likely be defined by:

Deeper integration with traditional finance

Expansion of local currency stablecoins

Increased regulatory standardization

And most importantly:

Real-world usage at scale