It shows how deep the affordability crisis has become and how far the American dream has slipped out of reach.

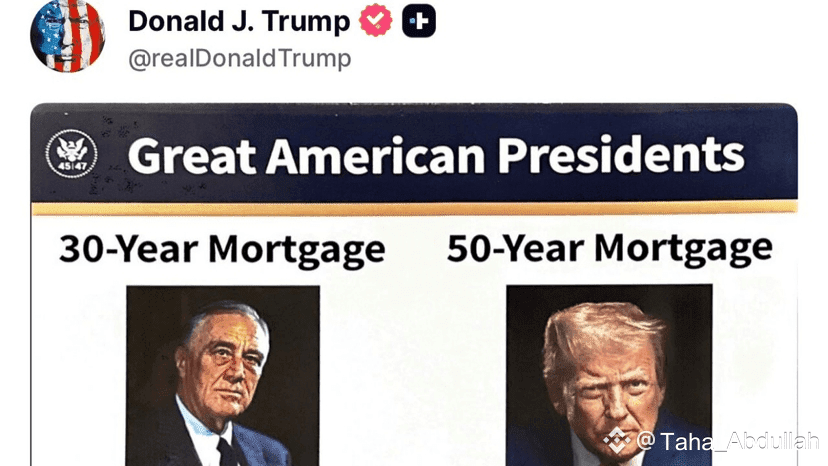

It seems that the lower payment is tempting on the surface. A $400,000 loan at 6% drops by about $166 a month when extended from 30 years to 50. But that small comfort comes at a huge cost.

Total interest approaches nearly double, from about $418,000 to over $860,000. Lenders also tend to add a slightly higher rate for longer loan terms, which wipes out most monthly savings anyway.

The biggest trap is what you don't see at first glance. With a 50-year mortgage, almost every early payment is swallowed up by interest. You earn almost no equity while someone with a 30-year loan is actually building equity and giving themselves the option to refinance. The longer term pushes your wealth-building years further into the future, exacerbating those delays against you.

But none of this solves the real problem. Home prices have detached from real wages. The national price-to-income ratio is around 5 to 1, while historically it has hovered around 3 to 1. Zoning limits supply, construction lags behind demand, and large investors continue to buy homes to rent to families who can no longer afford to buy. Longer mortgages do not solve this gap. They only extend the burden over more years.

The only scenario that makes a 50-year mortgage make sense is if you treat it as a short-term breathing space with a plan to refinance later. This requires timing, stability, and discipline, which is rarely provided by today's economy.

The average age of first-time buyers says everything, shifting from 28 in 1980 to 40 today. The new mortgage term is not a solution. It’s an offer for a program that needs real structural change, not more years of debt.