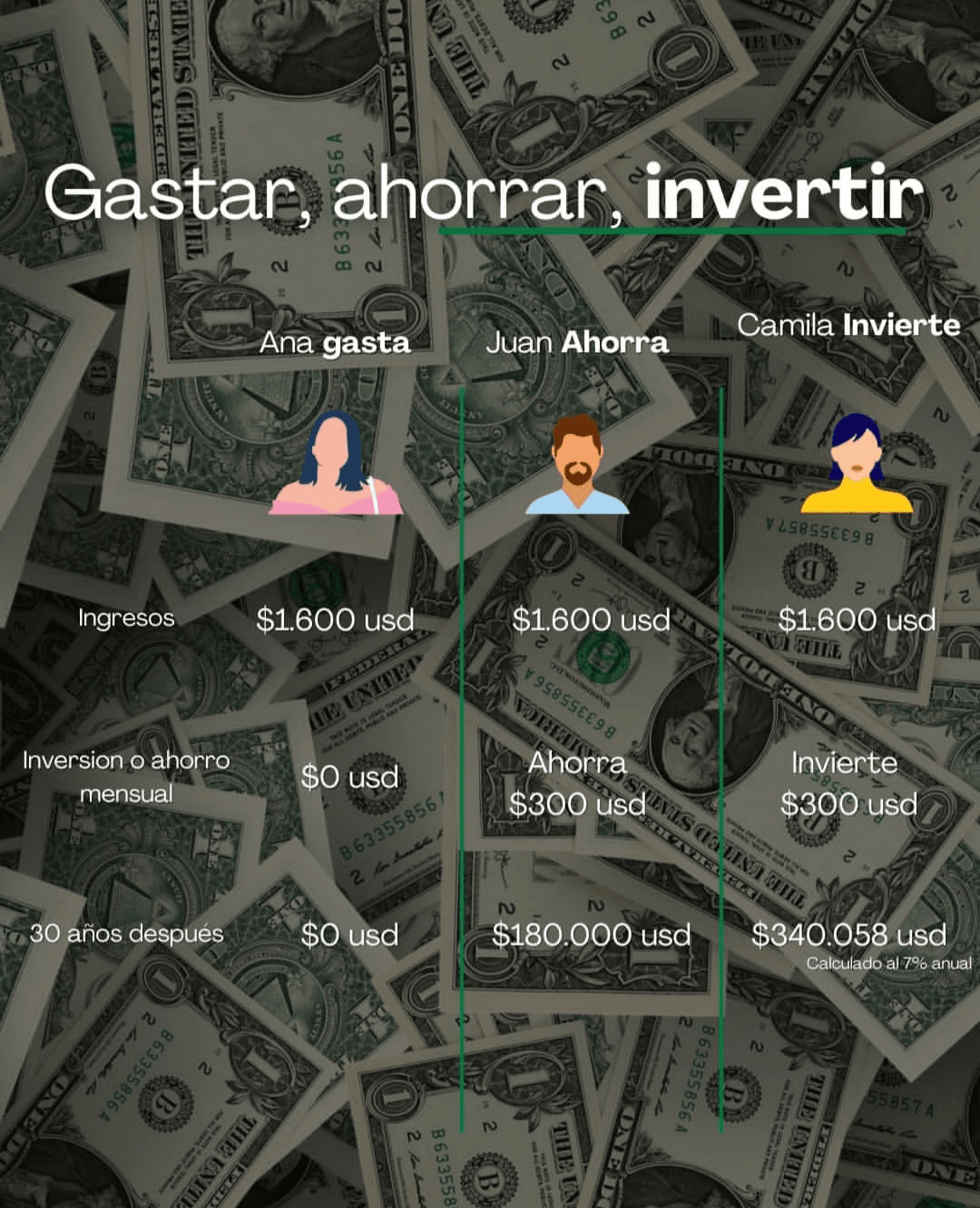

👉1. The Person Who Does Not Save

· Analogy: It's like having fertile land, but instead of planting or saving the seed, you eat it all immediately.

· Mindset: "I spend all that I earn." Lives day by day, without planning for the future. Their focus is on present consumption.

· Action: Their money goes directly to expenses (necessary and unnecessary). They do not set anything aside for the future.

· Result:

· Advantage: Maximum immediate satisfaction. Enjoys their money in the moment.

· Disadvantage: Extreme vulnerability. Any unforeseen event (an illness, a car repair, job loss) becomes a serious crisis. They do not build a financial future and depend entirely on their active income. Money in the checking account loses value over time due to inflation.

---

👉2. The Person Who Only Saves

· Analogy: It's like taking your seeds and storing them in a safe jar. You protect them from being eaten, but you don't plant them to grow.

· Mindset: "I have to save a portion of what I earn for emergencies or future goals." It is prudent and planning-oriented.

· Action: Set aside a portion of your income and deposit it in low or no-risk instruments, such as a savings account, a fixed term deposit, or under the mattress.

· Outcome:

· Advantage: Security and peace of mind. Has a cushion for emergencies and can plan purchases in the short/medium term (a car, a vacation). The capital is nominally "protected."

· Disadvantage: Purchasing power erodes. Inflation (the general rise in prices) means that with the same money, in the future, you can buy fewer things. If the bank gives you 1% interest but inflation is 3%, you are actually losing 2% of value each year. It's money that "sleeps."

---

👉3. The Person Who Invests

· Analogy: It's like taking your seeds and planting them in the field. With care and time, these seeds grow and bear fruit, producing more seeds.

· Mindset: "My money must work for me." Understands that saving is the first step, but not the last. Seeks to grow their capital in the long term.

· Action: Takes a portion of their savings and allocates it to assets that have the potential to generate returns (gains) above inflation. This includes stocks, index funds, bonds, real estate, etc. Accepts a level of risk in exchange for potential growth.

· Outcome:

· Advantage: Creates long-term wealth. Your money multiplies thanks to compound interest. It not only preserves purchasing power but also increases it. Builds wealth that can provide financial freedom.

· Disadvantage: Assumes risks. Markets fluctuate, so there may be periods of losses (sometimes significant). Requires financial education, patience, and a long-term strategy. Not for money you need in the short term.

---

📍Key conclusion:

The most financially intelligent person does not choose just one of these options, but follows a process:

1. Stop being the person who does not save.

2. Becomes the person who saves, first building an emergency fund (3-6 months of expenses).

3. Evolves into the person who invests, once they have their emergency fund, using their excess savings to seek long-term growth.

Saving is for security, investing is for prosperity. Both are essential in a solid financial plan.

#LibertadFinanciera #Write2Earn #BinanceSquareFamily #InvestSmart #dyor $BTC $XRP $SOL