Author: Daniel Li, CoinVoice

MegaETH might be one of the most controversial Layer 2 projects recently.

On one hand, it quickly gained popularity with the 'Realtime Blockchain' narrative, boasting 10ms block times, 100k TPS, and close to Web2-like on-chain interaction; on the other hand, MEGA rapidly shifted from bullish to bearish after its TGE, with prices dropping from a high of $0.37 to about $0.088, falling below the public sale price of $0.099, and experiencing a decline of over 70% in a short period.

With the first KPI achieved, market sentiment heated up quickly. MEGA spiked shortly after its launch, with the market briefly assigning MegaETH a fully diluted valuation (FDV) of nearly $2 billion. Meanwhile, MEGA also listed on mainstream exchanges like Binance, Coinbase, and OKX. However, as market enthusiasm started to cool, the 'Realtime Blockchain' narrative that MegaETH promotes began to face real market tests.

01 From V God to Dragonfly, MegaETH's early financing has gained core resource support

MegaETH is a high-performance Ethereum Layer 2 network that focuses on the concept of 'real-time blockchain', aiming to provide on-chain applications with an interaction experience close to that of Web2.

MegaETH's core team possesses both foundational technical research capabilities and experience in the Ethereum ecosystem, with members' backgrounds spanning distributed systems research, engineering implementation, and Web3 business development.

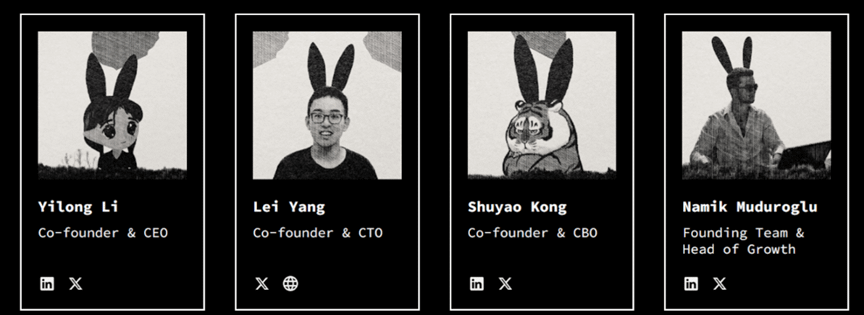

Co-founder and CEO Shuyao Kong entered the blockchain industry early, previously serving as the global BD head at ConsenSys (the company behind the MetaMask wallet) and graduating from Harvard Business School, giving him a deep understanding of Ethereum's ecosystem development logic and the global Web3 industry landscape. Compared to purely technical entrepreneurs, his strengths lie more in ecosystem resource integration, industry cognition, and long-term strategic aspects.

The technical team has a strong academic background and foundational engineering capabilities. Co-founder Yilong Li has a PhD from Stanford University, while CTO Lei Yang graduated from MIT and has long focused on distributed systems, consensus mechanisms, synchronization algorithms, and other foundational infrastructure research. These technologies are core to building a high-performance blockchain execution layer. Overall, the MegaETH team possesses both theoretical research depth and practical engineering experience, which is one of the key reasons why the market maintains interest in its 'real-time blockchain' route.

In terms of financing, since 2024, MegaETH has accumulated nearly $30 million in funding. In June 2024, MegaETH completed a $20 million seed round financing led by top institutions such as Dragonfly, with participation from well-known funds like Figment Capital, Robot Ventures, Big Brain Holdings, and others. Additionally, this round of financing attracted several industry key figures, including Vitalik Buterin, Joseph Lubin (founder of ConsenSys), Sreeram Kannan (founder of EigenLayer), and well-known KOL Cobie.

Subsequently, in December 2024, MegaETH raised approximately $10 million through a community round of funding, further strengthening the alignment of interests between the project and the user community.

02 MegaETH tokenomics: From KPI incentives to USDM buybacks

MegaETH's native token is $MEGA, with a total supply of 10 billion tokens. The token adopts a KPI-driven distribution mechanism, meaning that token releases are linked to the actual growth data of the network; when the network reaches specific performance and ecosystem goals, a new round of token releases will be triggered.

2.1, The token distribution logic of MEGA: High ecosystem incentives and long-term release mechanisms

Among the MEGA token distribution, it is noteworthy that approximately 53% is allocated to the KPI reward pool. This ratio is quite aggressive in the current crypto projects, indicating that more than half of the tokens will be gradually released according to the ecosystem's development, rather than being directly circulated at the TGE. From a positive perspective, this design helps reduce initial circulation pressure and establishes a long-term flywheel through the 'ecosystem growth - reward release' mechanism. However, this model also carries significant risks. With a large number of incentive tokens continuing to be released, the market will face continuous new supply pressure.

Meanwhile, the initial public circulation ratio of MEGA is only about 5%, making the overall circulation relatively limited. While this helps enhance early market attention, it also means that the token price is more easily influenced by market sentiment, and short-term volatility may be more pronounced.

The specific allocation of MEGA tokens is as follows:

• The public sale accounts for about 5%, all tokens will be fully allocated to purchasers, and the issuer will not retain any assets directly.

• The KPI reward pool accounts for about 53%, only staking users can participate, with a staking period between 10–30 days. The longer the staking time, the higher the yield weight. Network metrics indicate that performance-based staking rewards will be distributed over time.

• Other investors and early rounds account for about 24.7%, including institutional investors accounting for about 14.7%, Echo round investors about 5%, Fluffle purchasers about 2.5%, and Sonar reward pools about 2.5%.

• The team and advisors account for about 9.5%, with a 1-year lock-up period, and gradually unlocking linearly over 3 years.

• The foundation and ecosystem reserve account for about 7.5%, used for ecosystem development, strategic partnerships, and protocol sustainability maintenance.

2.2, MEGA token value capture mechanism

The crypto industry has long faced an awkward problem: many Layer 2 projects' tokens seem to have no other practical use besides governance and speculation. MegaETH attempts to address this issue through two mechanisms:

(1) Proximity Markets

Proximity Markets can be understood as the core high-frequency trading infrastructure within the MegaETH ecosystem, logically similar to 'selling low-latency capabilities'.

As MegaETH emphasizes millisecond response and real-time trading experience, the project plans to build a dedicated market around low-latency resources near the Sequencer. For example, traders in the future may bid or stake $MEGA to obtain server seats (Proximity Seats) closer to the Sequencer, thereby achieving lower latency and faster order responses in high-frequency trading.

Meanwhile, MegaETH also plans to launch Proximity Feed, a real-time data stream service based on global clock synchronization, to reduce software layer latency in high-frequency trading. This means that in the future, fees generated from low-latency trading services, auction revenues, and related protocol earnings may all enter MegaETH's value cycle and further link to $MEGA.

(2) USDM buyback mechanism

USDM is the native stablecoin of the MegaETH ecosystem, with a circulating scale close to $480 million, serving as the core financial layer of the entire ecosystem. USDM is issued based on Ethena's stablecoin architecture, with its underlying reserve income primarily derived from real-world asset yields like US Treasury bonds.

According to MegaETH's official disclosure: all profits obtained by the foundation from USDM will be used for market buybacks and accumulating $MEGA.

In simple terms, as more applications utilize USDM, the scale of the stablecoin expands, and the yields generated from USDM will continue to increase, ultimately translating into a buyback demand for $MEGA. This is also the flywheel model that MegaETH repeatedly emphasizes: 'ecosystem growth → income increase → token buyback → token value enhancement'.

Currently, MegaETH has officially launched this buyback mechanism. According to official disclosures, the MegaETH Foundation completed its first buyback of $MEGA on May 7, 2026, with all funds used coming from the net profits accumulated from USDM as of the end of April. However, as of now, the official has not publicly disclosed the specific number of $MEGA bought back or the actual amount, only stating that future buybacks will gradually achieve 'programmatic' and 'fully on-chain' execution, dynamically executed based on the supply scale and yield of USDM.

03 How does MegaETH operate? How does it achieve real-time performance?

MegaETH officially claims that its network can achieve approximately 100,000 TPS (transactions per second) and about 10ms block confirmation time, aiming to support low-latency scenarios such as real-time chain games, social interactions, trading, and AI Agents. This near real-time interaction experience akin to Web2 applications is primarily due to the following technical features.

3.1, Web2 + Crypto hybrid architecture

MegaETH adopts a 'role division' architectural design, where different types of nodes are responsible for specific tasks, thus requiring different hardware configurations. Compared to traditional blockchains that make all nodes repeat the same tasks, MegaETH is more like a clearly divided high-performance system that enhances overall throughput and execution efficiency by splitting responsibilities.

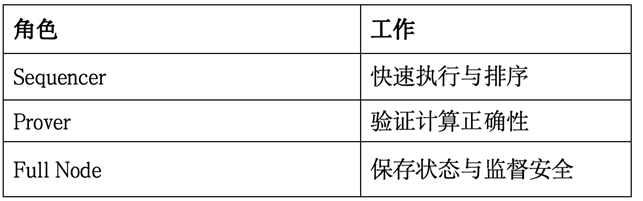

In MegaETH, there are three core roles: Sequencer, Provers, and Full Nodes. MegaETH achieves more specialized division of labor by distributing responsibilities such as transaction execution, verification, and state storage among different nodes, thereby avoiding the performance waste caused by 'all nodes repeating the same tasks' in traditional blockchains.

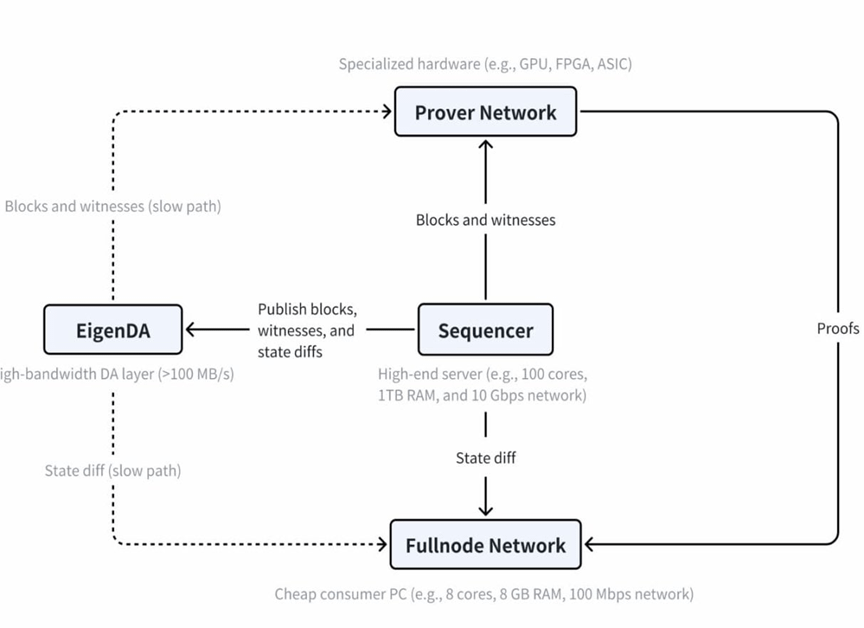

(1) Sequencer: Responsible for 'accounting and block production'

The Sequencer is responsible for transaction ordering and execution and is the core scheduling node of the entire network. Currently, MegaETH has only set up a centralized Sequencer, meaning the network does not require a large number of nodes to repeatedly participate in consensus like traditional public chains, thereby saving a lot of synchronization and voting overhead. After executing transactions, the Sequencer uploads the generated blocks, witness data, and state differences to the EigenDA data availability layer, ensuring that this data can be accessed and verified by other nodes in the network.

However, the most controversial aspect of MegaETH lies precisely in this 'single point of control' design. Since the entire network has only one node responsible for transaction ordering and block production, the Sequencer effectively holds the core block production rights. If this node fails, crashes, or is attacked, the entire network may halt block production, and user transactions will not be processed. Thus, compared to traditional public chains maintained by numerous validating nodes, MegaETH is relatively weaker in fault tolerance and decentralization, which is the primary concern regarding its centralization risks.

(2) Provers: Responsible for 'verification'

Provers are responsible for verifying whether the transaction execution results are correct. They obtain blocks and witness data from the Sequencer and use specialized hardware for 'Stateless Verification'. Stateless Verification means that Provers do not need to store the entire blockchain state to independently verify the correctness of a block. This design not only reduces node storage pressure but also allows multiple blocks to be verified asynchronously, in parallel, or even out of order, significantly improving overall system efficiency.

(3) Full Nodes: Responsible for 'maintaining the final state'

Full Nodes are more focused on maintaining the final state of the chain. They continuously receive state differences published by the Sequencer and update their local state database accordingly. At the same time, Full Nodes can check the validity of blocks to verify whether the Sequencer is making errors or acting maliciously, thus ensuring the consistency and security of the entire blockchain system.

Therefore, MegaETH's architecture indeed carries strong 'Web2 + Crypto hybrid architecture' characteristics. It is not a completely decentralized blockchain in the traditional sense, but rather a system built on the high-performance architecture of Web2, layered with the verifiability and asset attributes of Crypto.

Traditional Web3 public chains (like Ethereum) emphasize the joint participation of all nodes in consensus, execution, and storage to achieve maximum decentralization. However, this model comes at the cost of lower performance and higher latency. MegaETH has clearly made trade-offs, sacrificing some decentralization by concentrating transaction ordering and execution in a single Sequencer, which is very similar to the logic of 'centralized servers' in Web2 internet.

In other words, MegaETH's Sequencer is like the main server of an internet company, responsible for real-time request processing and fast result return; while Provers and the data availability layer are like backend auditing systems that verify the server's integrity.

In other words, the Web2 part is responsible for 'performance', while the Crypto part ensures 'trustworthiness'.

3.2, Based on the Ethereum ecosystem, MegaETH conducts targeted reconstruction of the underlying architecture

In response to the long-standing performance bottlenecks of traditional EVM blockchains, MegaETH has almost 'prescribed' a targeted reconstruction of the underlying architecture.

(1) Redesign the state Trie structure

One of the biggest bottlenecks of traditional blockchains is 'slow state reading'. The so-called state refers to all data on-chain, such as account balances, smart contract data, NFT information, etc. Traditional EVM chains like Ethereum often require frequent disk access when reading this data, and hard disk I/O (input/output) is very slow. As on-chain data grows larger, this problem becomes more severe.

To address this issue, MegaETH has redesigned the state Trie structure and optimized memory and I/O usage. Simply put, it has made 'data indexing' and 'data retrieval methods' more efficient. Even if the on-chain state data reaches TB levels in the future, MegaETH still hopes to read quickly without performance degradation due to frequent disk access. This means MegaETH has rewritten the blockchain database, making 'checking balance, modifying data' much faster.

(2) Parallel execution strategies

The execution model of Ethereum is essentially serial, like having only one lane; if the transactions in front are not processed, those behind have to wait. This severely limits TPS.

MegaETH allows the Sequencer to use parallel execution strategies. This means multiple transactions can be processed simultaneously, more like a multi-lane highway system rather than a single-lane queue. This is also one of the key reasons MegaETH can achieve ultra-high throughput.

(3) JIT compiler

Additionally, traditional EVM is essentially still an 'interpreter'. Smart contract code does not run directly; rather, it is first read, then translated line by line, and then executed. This process incurs significant performance losses.

MegaETH utilizes JIT (Just-In-Time) compilation technology, based on the core idea of pre-compiling code into a form closer to machine language for direct execution. Therefore, it does not execute 'translating and running' like traditional EVM, but rather resembles a game engine or high-performance server program that pre-compiles code, allowing complex DApps to achieve near bare-metal performance.

Lastly, there is a very practical problem that synchronizing data between blockchain nodes is very bandwidth-intensive, especially when chain transactions are large, requiring frequent state updates that propagate constantly across the network. Traditional chains often experience slow synchronization and high node pressure. To address this, MegaETH has designed a state difference (State Diff) compression and efficient transmission mechanism. In simple terms, it does not repeatedly send the complete state but only syncs 'what has changed' and also performs advanced compression. This way, even with limited network bandwidth, it can synchronize a large number of transaction updates.

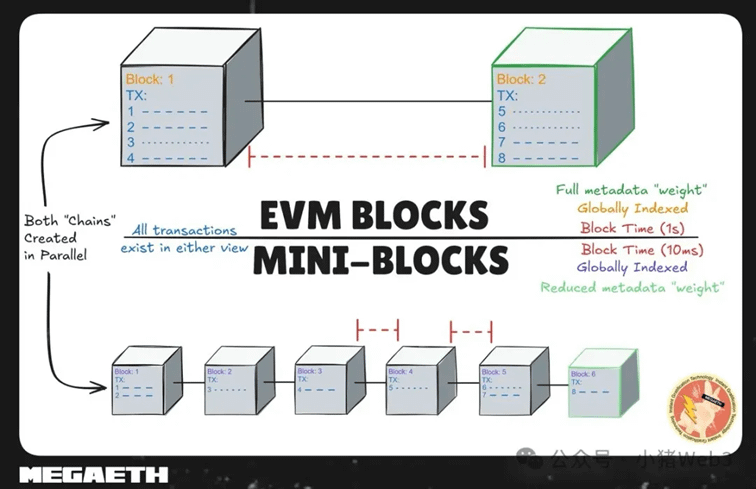

3.3, The lighter and faster 'Mini Blocks' mechanism

To achieve a 'real-time on-chain experience', MegaETH does not rely entirely on the traditional EVM block production method but additionally designs a lighter and faster 'Mini Blocks' mechanism.

One of the core problems of traditional blockchains is that block production is too slow. Even for many high-performance chains, the user's transactions can take hundreds of milliseconds to seconds to be packed into blocks and broadcast across the network. MegaETH aims to achieve a real-time interaction experience close to that of Web2 Apps, further compressing confirmation speeds to the 10-millisecond level.

MegaETH's approach is to generate a Mini Block every 10ms, quickly informing the network 'which transactions have been accepted' by broadcasting a simplified version.

This means that users do not need to wait for a complete block to be generated to know in advance: their transaction has entered the Sequencer, is likely to be officially packed, and can update the interface status in advance. Thus, users will feel that on-chain interactions are almost 'real-time feedback'.

Thus, two types of elements coexist in the network: Mini Blocks (ultra-light real-time blocks for real-time feedback) and standard EVM Blocks (for final settlement). Essentially, MegaETH uses a method of 'high-frequency lightweight pre-confirmation + low-frequency formal settlement' to solve the traditional blockchain issues of 'slow confirmation and interaction lag'.

04 The High-Performance Public Chain Competition: MegaETH, Monad, Hyperliquid

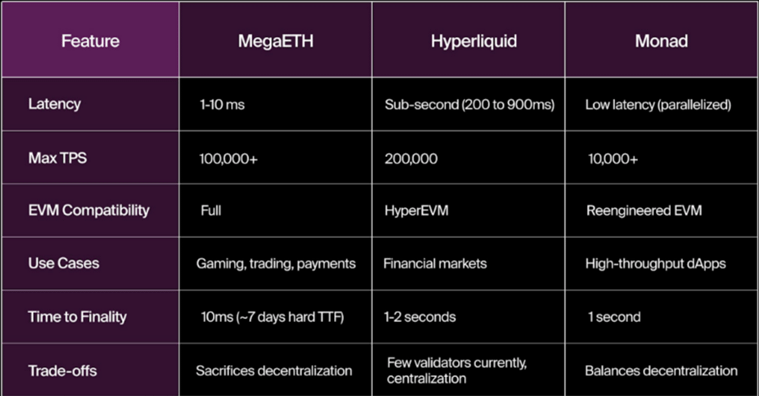

MegaETH, Hyperliquid, and Monad respectively represent three different routes of high-performance blockchain today, all trying to break through the performance bottlenecks of traditional EVM, but with different emphases.

Among them, MegaETH emphasizes the 'real-time blockchain' experience, particularly excelling in terms of latency and TPS. Through centralized Sequencer, Mini Blocks, and highly optimized execution architecture, MegaETH can achieve a near real-time interaction experience akin to Web2 applications, making it very suitable for scenarios like chain games, social interactions, and real-time data applications where low latency is critical. However, its single Sequencer design has also sparked controversy regarding centralization, censorship risks, and trust assumptions.

Hyperliquid is more like a high-performance chain built specifically for financial trading. With HyperBFT consensus, HyperEVM, and deep liquidity integration, Hyperliquid is extremely competitive in financial scenarios such as perpetual contracts, on-chain trading, and high-frequency matching, with trading experiences even approaching those of centralized exchanges. However, due to its architecture being highly optimized for financial scenarios, compared to MegaETH, it has relatively limited expansion capabilities in general dApp ecosystems and application diversity.

Monad's approach leans more towards 'finding a balance between decentralization and performance'. It enhances TPS through parallel execution, asynchronous processing, and deep optimization of the EVM while striving to maintain an Ethereum-like decentralized structure and development experience. Therefore, Monad provides developers with a general high-throughput blockchain solution that balances performance, compatibility, and decentralization.

As for which of the three is more advanced, it fundamentally depends on the specific application scenarios. If the goal is trading, liquidity, and high-frequency financial applications, Hyperliquid, with its focus on financial infrastructure design, remains one of the most competitive players. If the goal is to build a broader real-time dApp ecosystem, MegaETH has more evident advantages in low latency and real-time performance. For developers who wish to achieve high throughput without excessively sacrificing decentralization, Monad's parallelized EVM architecture offers a more balanced choice.

05 Notable projects within MegaETH

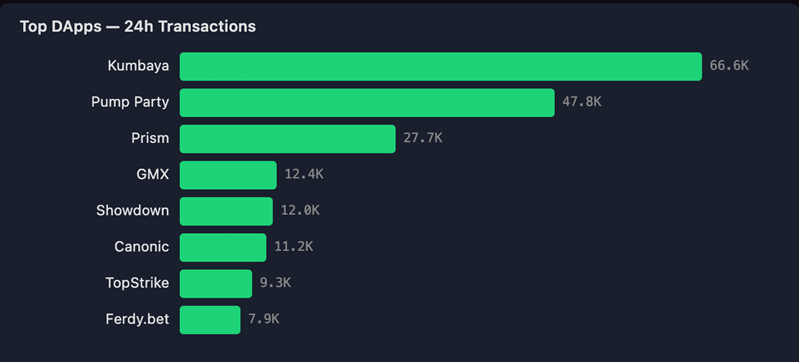

With the TGE landing, the flow of funds within the MegaETH ecosystem and on-chain activity has gradually become the market's core focus. Key protocols such as Cap, Kumbaya, Brix, Euphoria Finance, and World Capital Markets are respectively undertaking crucial financial scenarios such as stablecoins, DEX, yield-bearing assets, derivatives trading, and unified margin systems, gradually building up MegaETH's native DeFi and trading ecosystem.

As the early chips of MEGA enter the redistribution phase following its launch, whether market funds will further flow back into the ecosystem has become an important indicator of whether MegaETH's popularity can be sustained. To some extent, these leading protocols not only bear the liquidity absorption function of the ecosystem but also will become the core observation window for whether the narrative of MegaETH’s 'real-time blockchain' can truly translate into user and capital growth on-chain.

5.1, Kumbaya

Kumbaya positions itself as the fastest and deepest liquidity cultural asset creation and trading platform, currently with a total locked value (TVL) of approximately $32.66 million, and a 30-day DEX trading volume of about $288 million. Its core gameplay focuses on creating a 'cultural-value flywheel', emphasizing the preservation of cultural asset value and liquidity accumulation, as opposed to the 'buy, pump, and dump' trading mode created by pump.fun. This also avoids the problem of liquidity disconnection and cultural value cycle collapse after tokens leave the issuance platform and move to Raydium.

According to the latest on-chain data, the TVL of the MegaETH ecosystem has rapidly grown from about $100 million at the beginning of the TGE to a range of approximately $780 million to $1 billion, making it one of the fastest-growing Layer 2 ecosystems in recent times. However, the problem of concentrated liquidity still exists.

Among them, Kumbaya remains one of the most core DeFi protocols within MegaETH. According to the latest data from DefiLlama, Kumbaya currently has a TVL of approximately $32.66 million, with 30-day DEX trading volume nearing $290 million, and cumulative trading volume exceeding $500 million. Although its share in the ecosystem's overall TVL has decreased compared to about 60% at the beginning of the TGE, it still plays the most important role as a liquidity entrance for the MegaETH ecosystem.

This highly concentrated liquidity structure reflects the rapid aggregation of early funds to leading protocols, but also means that MegaETH's ecosystem still has a high dependency on a single protocol. If Kumbaya experiences a contract vulnerability, liquidity withdrawal, or a decline in trading activity, the overall on-chain ecosystem of MegaETH may still face significant impacts.

5.2, Emerging market tokenized yield platform Brix

Brix aims to open up on-chain yield channels for DeFi users in emerging markets. Through tokenized yield-bearing stablecoins and assets, users can gain high yield exposure on-chain.

Currently, one of its core products is iTRY, a tokenized Turkish lira currency market product, with an annual yield of about 45%. In the future, Brix also plans to launch more emerging market currency products, including Brazilian real (BRL) and Indian rupee (INR).

According to the crypto asset data platform RootData, just this April, Brix completed $5.5 million in financing, led jointly by FRWRD and IS Asset Management; participants included Circle Ventures, ConsenSys, and Borderless Capital.

5.3, The derivatives trading market of Euphoria Finance

Euphoria's core gameplay is the 'Tap Trading' mechanism, where users can predict short-term price trends just by clicking on a grid in the interface, further gamifying and socializing the trading experience. However, Euphoria's mainnet is still in closed testing, only open to AMA participants and early testing users. However, as the full public test approaches in mid-May, the market generally believes it will become one of the most anticipated consumer applications in the MegaETH 2.0 ecosystem.

According to the crypto asset data platform RootData, Euphoria raised $7.5 million last August, led by Karatage.

5.4, DeFi trading platform World Capital Markets

World Capital Markets is a unified margin order book system covering spot, perpetual contracts, and lending, with a single collateral usable across three types of services, aiming to realize the vision of 'trading any market, anywhere, anytime'. Leveraging MegaETH's high-performance infrastructure, World Markets can fully exploit the advantages of on-chain high-frequency order books and ensure that margin updates, risk checks, and clearing processes can be completed within the same block in cross-margin trading scenarios, enhancing overall capital efficiency. MegaETH's high throughput and low latency characteristics are the core basis supporting such applications.

5.5, Stablecoin engine CAP

CAP is an innovative stablecoin engine that combines stablecoins with high-efficiency on-chain strategies to provide users with native yield opportunities. Users can mint cUSD using USDC or USDT at a 1:1 ratio and further stake it for stcUSD to earn yields from authorized strategy providers.

According to the crypto asset data platform RootData, Cap completed $11 million in financing last April, with participation from Triton Capital and others. As MEGA is expected to conduct TGE on April 30, 2026, the market generally anticipates that Cap will become one of the key projects for early token issuance within the MegaETH ecosystem.

It is worth mentioning that Aave V3, GMX, and Chainlink Scale projects completed integration from the first day of MegaETH's mainnet launch, providing access to flagship assets worth nearly $14 billion (including wstETH and LBTC). The presence of these blue-chip DeFi protocols further solidifies MegaETH's position as a production-grade infrastructure, rather than relying solely on native applications to sustain the illusion of ecosystem prosperity.