Related assets:

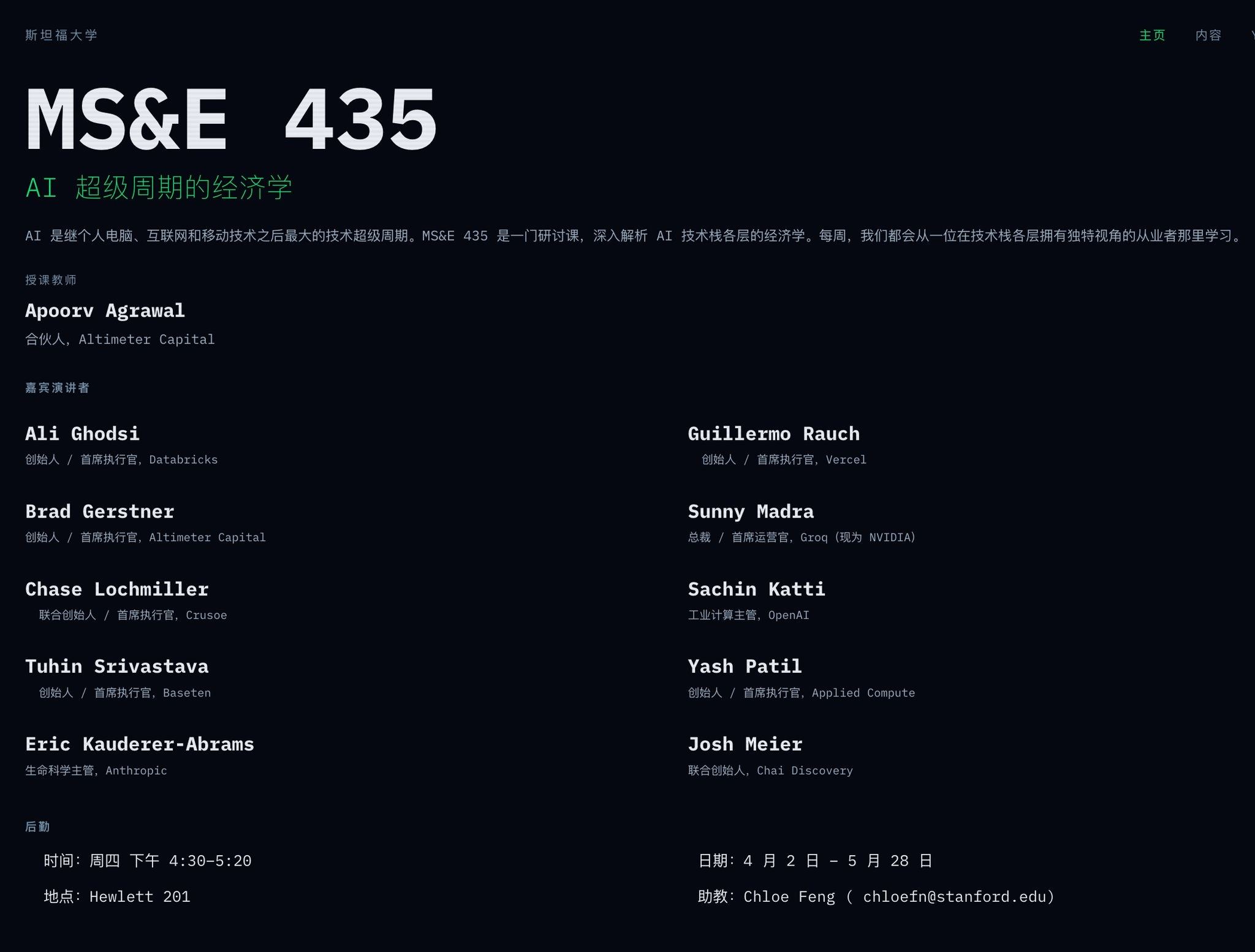

Stanford launched a course this spring called Economics of the AI Supercycle (MS&E 435), taught by Apoorv Agrawal, a partner at Altimeter Capital. Altimeter is a major shareholder in NVIDIA and OpenAI, and each week they invite a key industry player to break down the AI economy—Databricks CEO Ali Ghodsi, Vercel CEO Guillermo Rauch, Crusoe CEO Chase Lochmiller; it's a true all-star lineup from Silicon Valley's AI scene.

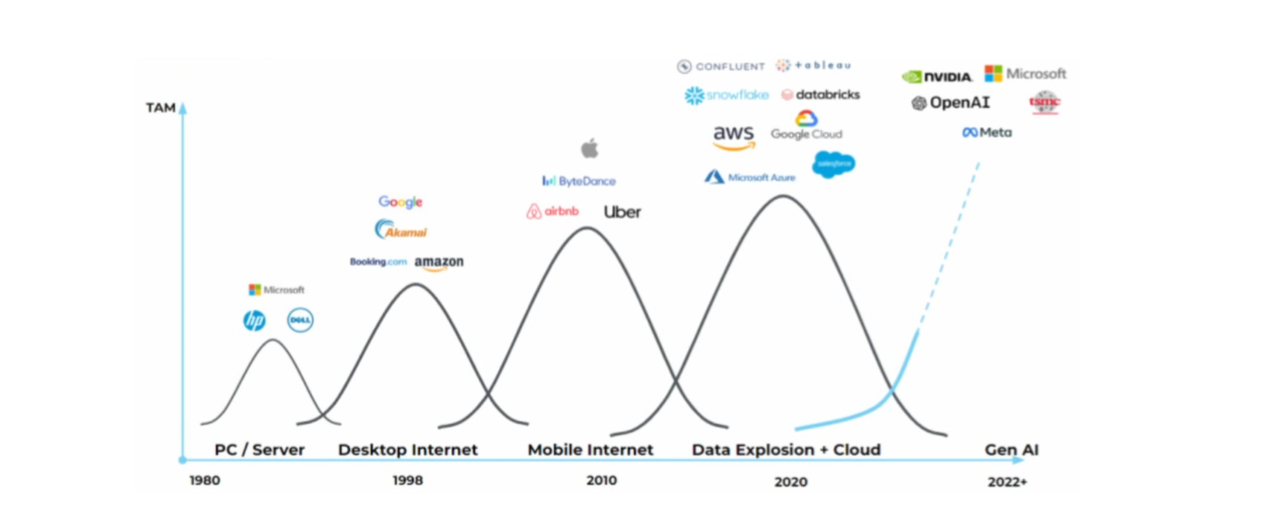

After watching the first three classes, I created an 8-layer panorama of the AI industry. Here are the most shareable insights from the course.

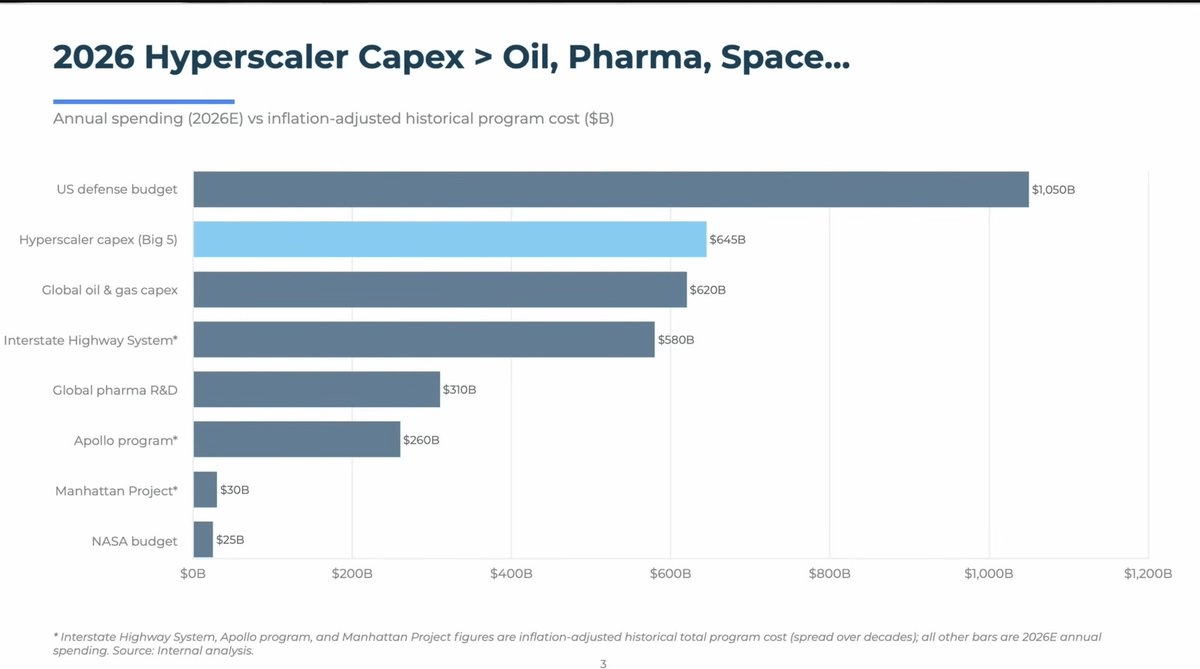

1/ AI is already the second largest expenditure globally, second only to the US defense budget.

In 2026, the big five (Amazon, Microsoft, Google, Meta, Oracle) are projected to spend over $600 billion on AI, tripling in just three years. But revenue is growing even faster—overall AI revenues are set to climb five times in the same period, with Anthropic hitting 10x year-on-year for three straight years. This isn't a 2000-style bubble; revenues are catching up to expenditures.

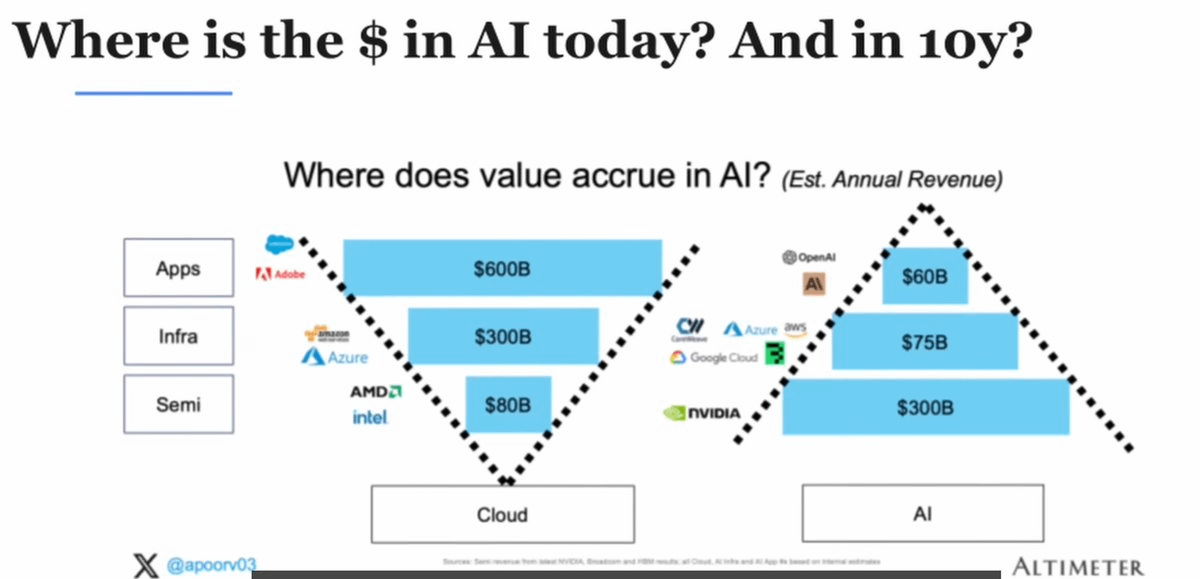

2/ The value distribution of the AI industry is completely opposite to the cloud computing era.

The cloud computing era was an inverted triangle: the application layer (Adobe, Salesforce) took 70% of the revenue, while semiconductors only grabbed 6%.

The AI era is flipping entirely: semiconductors are taking 79% of the gross profit, while the application layer only gets 7%. Computing power remains a bottleneck, and everyone is queuing up to buy GPUs. But the trend is shifting—by 2024, model companies will only have a gross profit of 38%, rising to 70% by 2026, as bargaining power shifts toward the model layer.

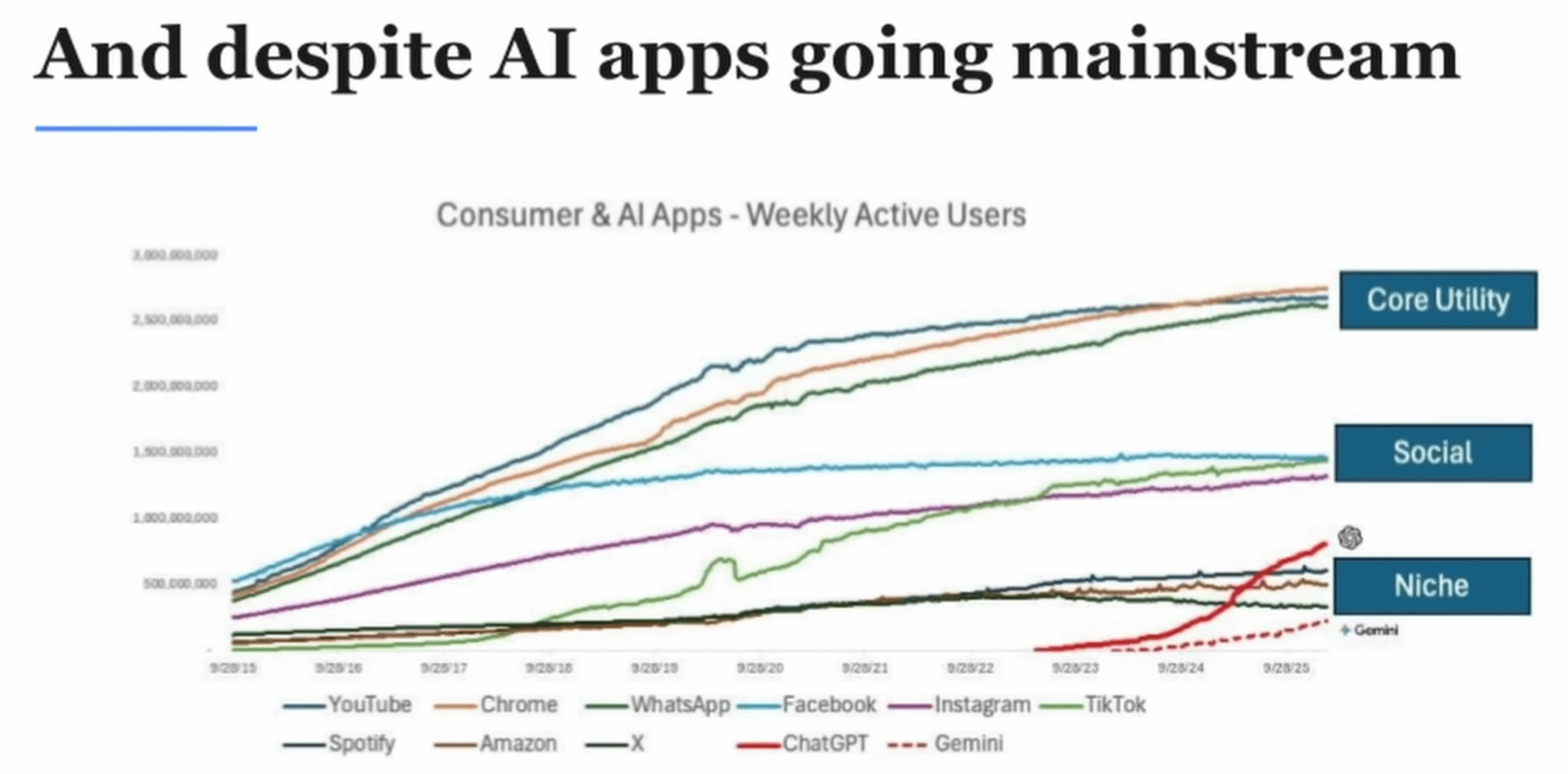

3/ ChatGPT has 1 billion monthly active users, but AI penetration is still in its early stages.

Placing ChatGPT in a global C-end application comparison: YouTube, Chrome, WhatsApp have nearly 3 billion weekly users; social apps (Facebook, Instagram, TikTok) are around 1.5 billion, while ChatGPT has just surpassed vertical apps (music, e-commerce, news). The stock price has risen tenfold, but from a user penetration perspective, we are still very early.

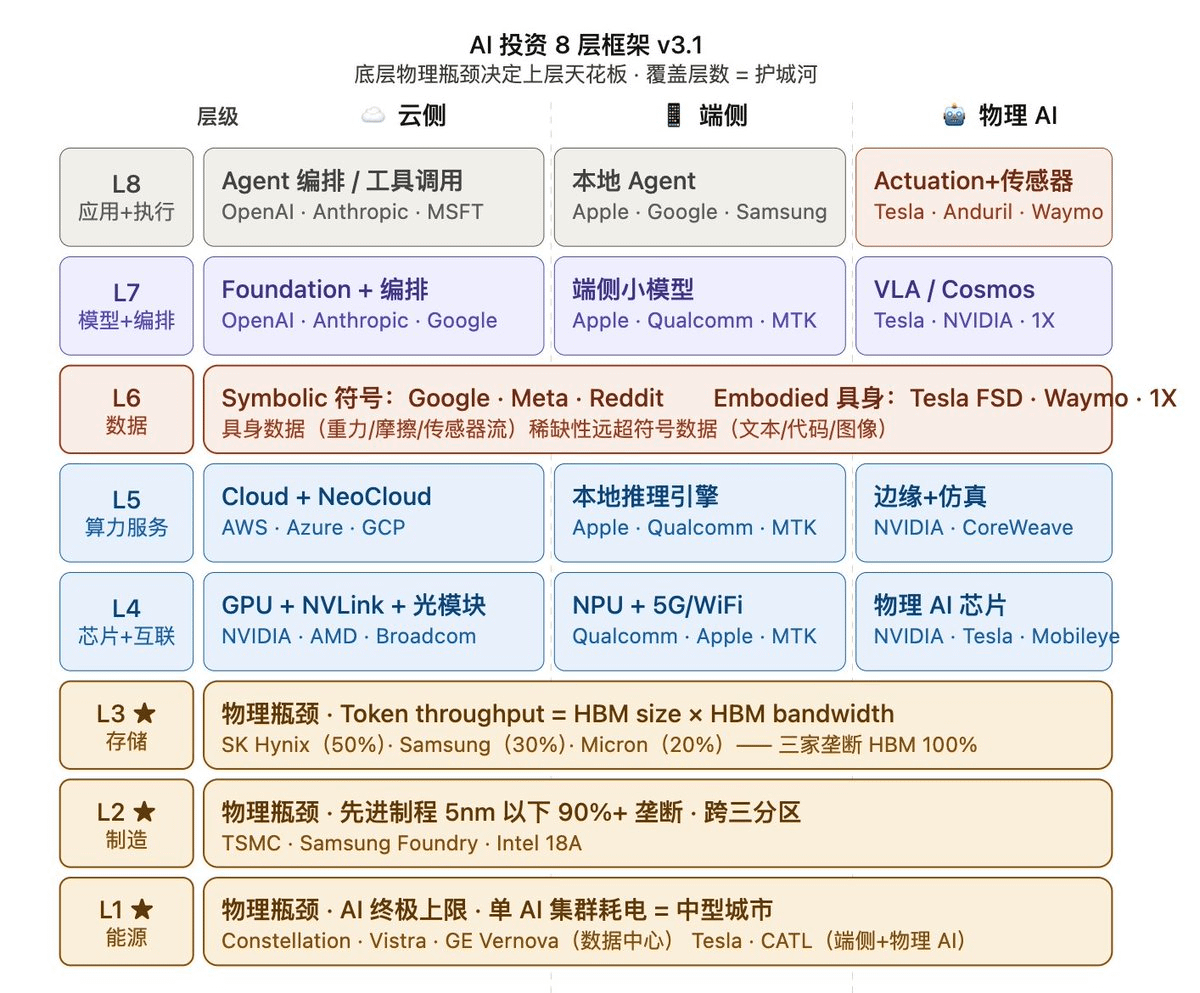

4/ I created a panoramic view of the eight layers of the AI industry.

Jensen Huang divides the AI industry into five layers, but there are too many concepts, so I’ve broken it down into eight: Energy → Manufacturing → Storage → Chip Interconnect → Computing Services → Data → Models → Applications. Each layer further divides into cloud side, edge side (mobile devices), and physical AI (autonomous driving/robots).

A few key judgments:

Energy layer: The power consumption of an AI training cluster equals that of Houston. Crusoe is building a data center for the OpenAI Stargate project; nuclear energy, fuel cells, and other new energies are still in very early stages.

Manufacturing layer: TSMC holds 90% of the advanced process capacity below 5nm, making it the biggest physical bottleneck in the AI industry besides power. Musk founded TerraFab to venture into manufacturing, but hardware production isn't as simple as just writing code.

Storage layer: Short-term chip shortage, long-term energy shortage, and an ongoing shortage of storage. As models grow larger and agent memory increases, HBM becomes the scarcest resource; the stock prices of Hynix, Samsung, and Micron have already surged.

Computing service layer: Traditional clouds (AWS, Google Cloud) weren't designed for producing Tokens, and architectural renovation takes time. NVIDIA is supporting a series of NeoClouds (CoreWeave, Lambda, IREN) to build AI-native infrastructure from scratch.

Data layer: Many investment frameworks overlook this layer, but it serves as a moat for vertical models. Tesla FSD has accumulated nearly 10 billion miles of driving data, and healthcare data is some of the most private and unavailable data on the internet—this is why WHOOP's investors include the Mayo Clinic and sovereign funds.

Model layer: The top three are OpenAI, Anthropic, and Google. TPU theoretical performance rivals that of GPUs, but the ecological barrier is too high—Anthropic can use TPU because they have former core TPU engineers on the team; others would struggle. Only Google can challenge NVIDIA.

Application + physical AI layer: Cloud AI addresses the issues of knowledge workers, while physical AI tackles problems for everyone else—Tesla Optimus, FSD, Anduril's defense drones, even SpaceX rockets, are essentially physical forms carrying AI models.

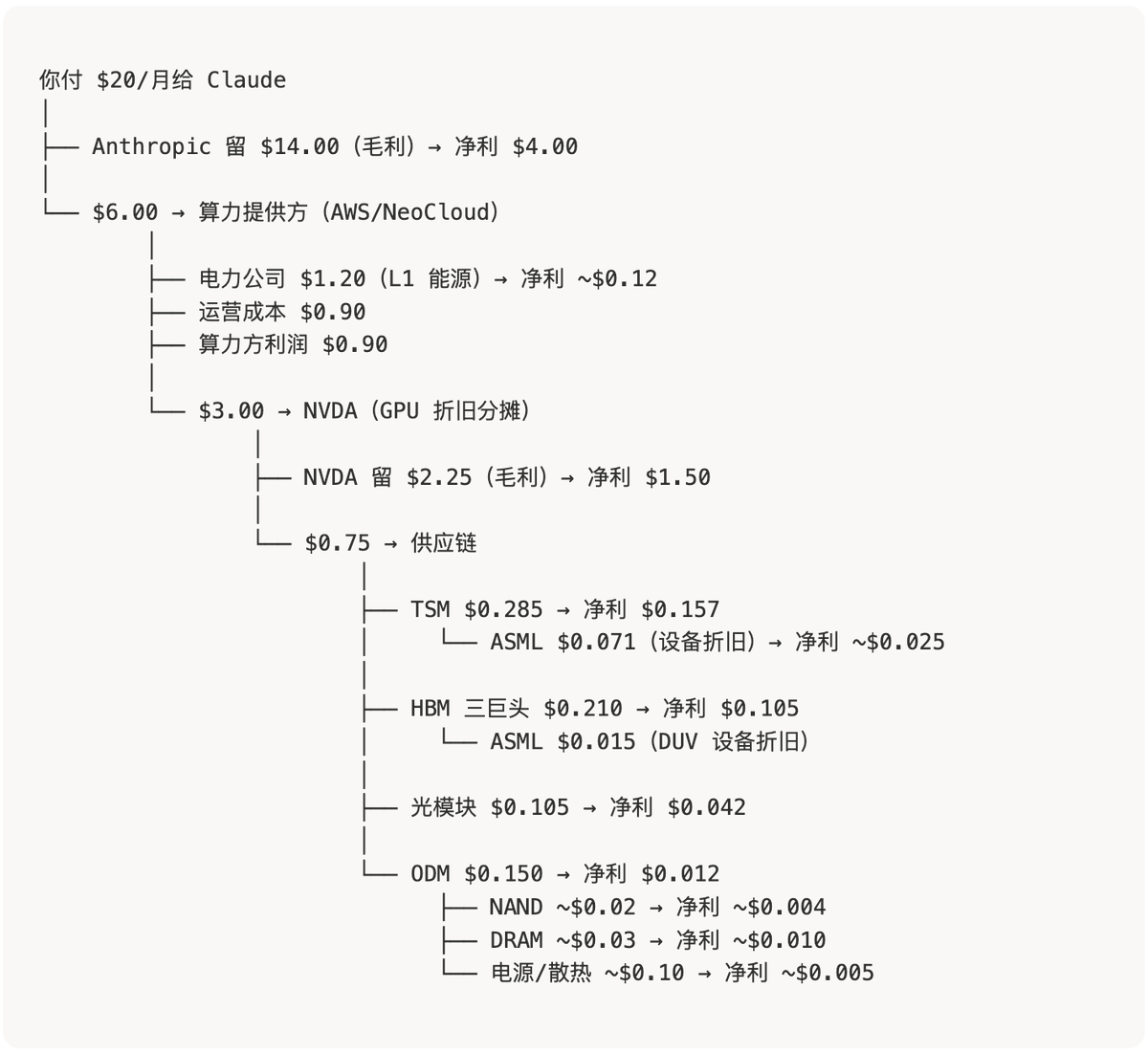

5/ Where exactly is your $20 subscription fee going?

The $20 you pay to Claude monthly, the profit distribution chain looks like this:

Anthropic nets $4 in profit (gross margin 70%, net margin 20%), NVIDIA takes $1.5 (net margin 50%, highest), NeoCloud grabs $0.9, TSMC takes $0.15, and power companies only make $0.1 from $1.2 in revenue. ASML, the three storage giants, and optical modules split the remaining crumbs.

No matter who profits in the AI era, NVIDIA and TSMC are skimming off every link—that's why Jensen Huang is always smiling during his talks.

6/ When selecting AI companies, consider three dimensions.

First, how large is the future space? The model layer might still have 10x potential.

Secondly, how strong is the profit acquisition power? NVIDIA and TSMC extract profits from each link.

Third, how indispensable is it? The lithography machine only exists at ASML, advanced processes are only at TSMC, GPUs are currently exclusive to NVIDIA, and storage is limited to three players—monopoly = sustained pricing power. The counterexample: NeoCloud has decent profit margins, but competition is fierce, and the moat is limited.

Note: Value and stock price are two different things. SanDisk makes very little profit in the supply chain, but its stock price has already soared.

7/ Two practical recommendations.

Apoorv Agrawal says if you can only read one material due to limited energy, the highest priority is the earnings call—companies discuss what they care about most; everything else is noise.

Crusoe CEO Chase Lochmiller presented a bearish perspective: currently, energy-related companies are highly hyped—transformers, outlets, Schneider. But from first principles: what will the energy structure look like in 5-10 years? What innovations will emerge? Just because something is popular now doesn't guarantee it will still be needed in the future.

The course is continuously updated; I recommend checking directly: mse435.stanford.edu