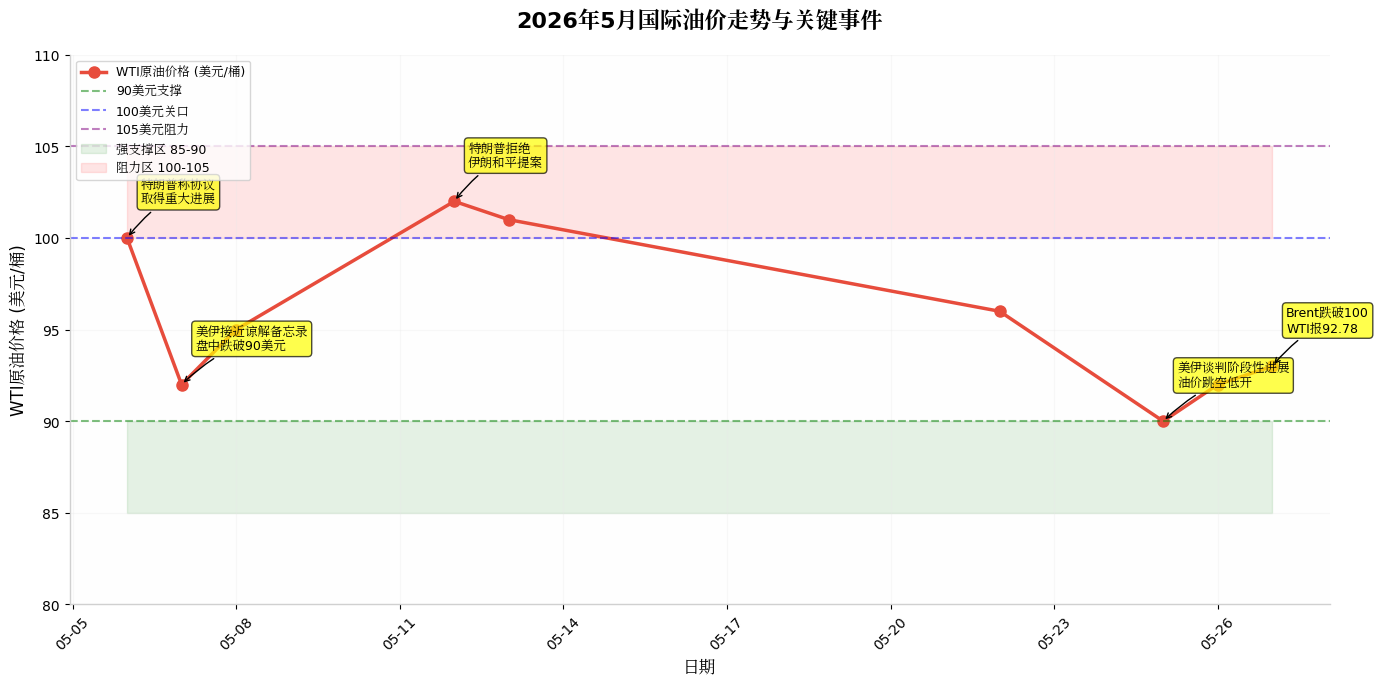

📊 1. Current Oil Price Trend Overview In late May, oil prices exhibited a 'high-level consolidation and retreat' pattern: WTI Crude Oil: On May 27, prices were around $92.78 per barrel, while Brent dipped below the $100 mark, hitting a nearly 5-week low. May's trading range was approximately $90-105 per barrel, revolving around the psychological barrier of $100 with intense volatility. Trend characteristics: Geopolitical news dominates, reflecting a 'negotiation progress → sharp oil price drop, escalation of conflict → price rebound' back-and-forth pattern.

🔥 2. Core Drivers Analysis

Geopolitics: US-Iran Conflict and Strait of Hormuz Blockade (Major Variable) This is the decisive factor behind current oil price volatility: On May 6, Trump announced significant progress in the US-Iran agreement, pausing the Strait of Hormuz escort, causing oil prices to retreat to around $100. On May 7, the US and Iran approached a memorandum of understanding, with prices briefly dipping below $90 in a V-shaped reversal, ultimately maintaining high levels. On May 12, Trump rejected Iran's peace proposal, stating the ceasefire agreement was 'precarious,' pushing oil prices back above $100. On May 25, US-Iran negotiations reached a phased progress with an additional 60-day ceasefire, leading to a gap down and significant pullback. On May 26, the US military conducted self-defense strikes in southern Iran, leaving geopolitical risks unresolved and oil prices returning above $90.

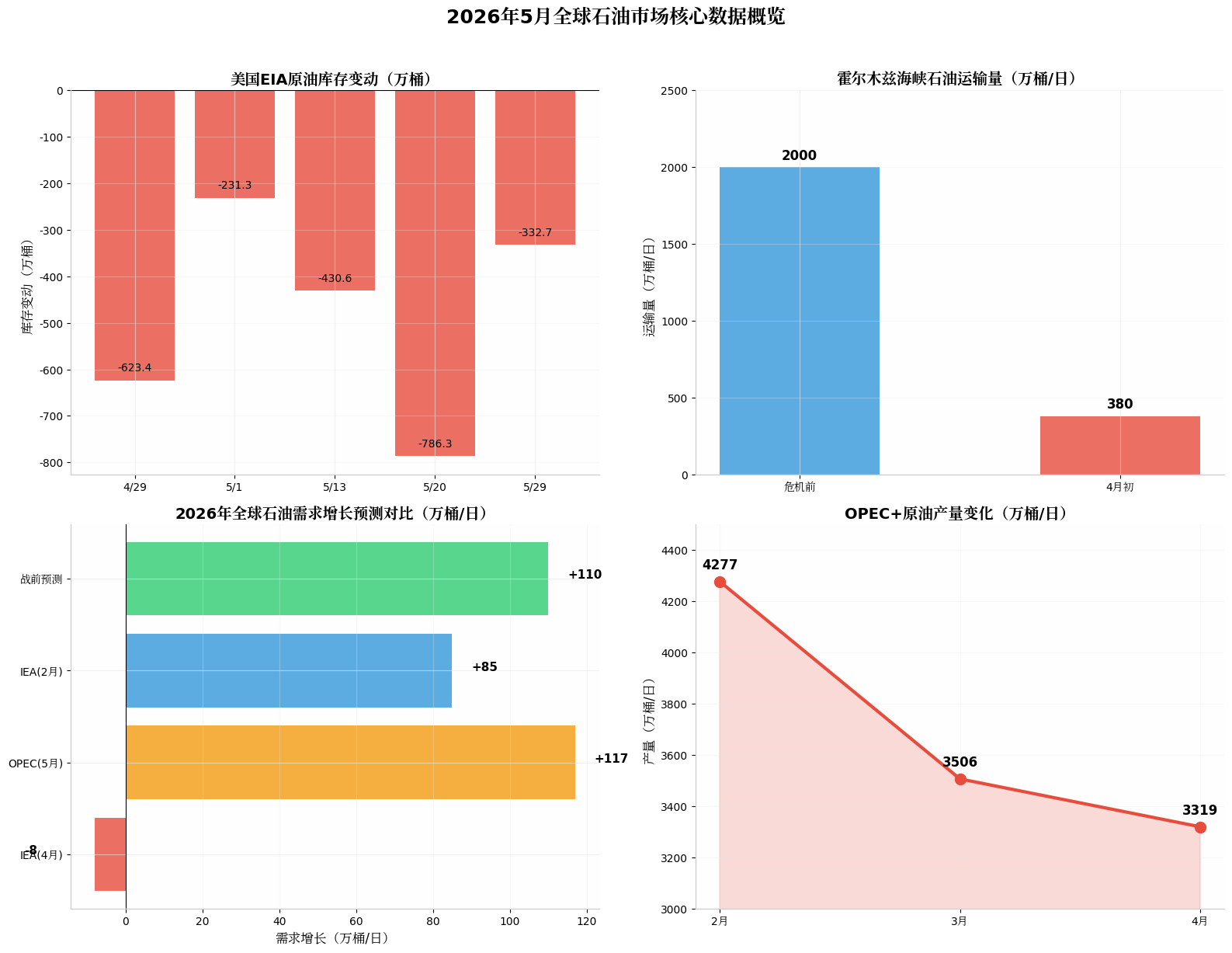

Key Data: The volume of transport through the Strait of Hormuz has plummeted from 20 million barrels per day pre-crisis to 3.8 million barrels per day, a drop of over 80%. This strait carries about 20% of global oil transport; the blockade has caused the largest supply disruption in history. Chevron CEO Mike Wirth pointed out that even if a ceasefire agreement is reached, the negative impact on energy prices will continue for several months.

Supply Side: OPEC+ output increase is more 'symbolic' than actual. The core seven OPEC+ countries (Saudi Arabia, Russia, Iraq, Kuwait, etc.) plan to raise July production targets by 188,000 barrels per day in the June 7 meeting, but there are significant real constraints.

1. Actual production plummeted: OPEC+ output fell from 42.77 million barrels per day in February to 33.19 million barrels per day in April, a monthly decrease of about 7.7 million barrels per day. 2. Production increase is limited: The blockade of the Strait of Hormuz has hindered exports from major producers like Saudi Arabia, Iraq, and Kuwait, leaving very little room for actual production increases. 3. UAE withdrawal: The UAE has exited OPEC+, weakening the overall influence of the alliance, but possibly strengthening internal cohesion. 4. Conclusion: Planned output increases on paper have little significance for actual supply increments, and the supply-tight pattern has not fundamentally eased.

Inventories and Strategic Reserves: Historic depletion. U.S. inventories continue to decline: For the week of May 20, EIA crude oil inventories fell by 7.863 million barrels (far exceeding expectations). For the week of May 13, a decrease of 4.306 million barrels. For the week of May 29, a decrease of 3.327 million barrels.

Strategic Petroleum Reserve (SPR) is declining at an unprecedented rate: The U.S. strategic oil reserves are decreasing at a speed rarely seen in recent years. The IEA coordinates member countries to release a record 400 million barrels. The strategic reserves are stabilizing prices, but commercial crude oil inventories are also at low levels (consistent with your screenshot).

Demand Side: High oil prices suppress consumption, with forecasts being significantly revised downwards. The IEA has rarely downgraded demand to negative growth: The April monthly report cut global oil demand from an increase of 640,000 barrels per day in 2026 to a contraction of 80,000 barrels per day, marking the first annual decline since the 2020 pandemic. In Q2, the year-on-year decline reached 1.5 million barrels per day, the highest since the pandemic. High oil prices lead to demand destruction, causing chaos in the Asian petrochemical supply chain.

OPEC is relatively optimistic but still revised down: The May report lowered the projected demand growth for 2026 from 1.38 million barrels per day to 1.17 million barrels per day. Demand is expected to rebound to a growth of 1.54 million barrels per day in 2027.

The Dollar and Macroeconomics: The Fed is hawkish: Strong employment data lowers interest rate cut expectations, keeping the dollar strong and suppressing dollar-denominated commodities. Global economic weak recovery: Major economies are slowing down, energy transition is advancing, and long-term demand is under pressure.

📈 3. Technical Analysis: The 5-day and 10-day moving averages have formed a death cross, indicating short-term adjustment pressure. MACD green bars are shrinking, and a high-level death cross is noted. Bearish momentum is weakening, but the trend remains unchanged. RSI has retreated from the overbought zone to around 50, showing a neutral to strong bias, with upward momentum slowing. Key support levels are at $90 and within the $85-88 range. Strong support area. Key resistance levels are at $100 and within the $103-105 range, which are psychological barriers and resistance points.

Technical Conclusion: Oil prices are in a high-level consolidation pattern. $90 is a critical bull-bear line; a break below could open up downward space. Stabilizing above $100 may lead to a renewed push towards $105-110.

🔮 4. Future Outlook and Scenario Analysis: Scenario 1: The Strait of Hormuz gradually resumes (baseline scenario, probability 40%). If U.S.-Iran negotiations continue to progress, navigation through the strait may gradually resume in July-August, and oil prices could fall back to the $80-95 per barrel range. OPEC+ will likely release actual production capacity, bringing back a loose supply pattern.

Scenario 2: Ongoing/ escalating conflicts (risk scenario, probability 35%): The blockade of the strait continues into the second half of the year. Oil prices could potentially re-challenge the $100-110 per barrel mark, or even higher. Global inventories continue to deplete, and strategic reserves are running low. The prediction from Chevron's CEO that 'oil prices are likely to rise this summer' may come true.

Scenario 3: Economic recession suppressed (pessimistic scenario, probability 25%): High oil prices trigger a global economic recession, leading to a significant contraction in demand. Oil prices may fall below $80, potentially dipping to $70, aligning with 2026 academic predictions (Brent average price $53-63).

Timeline Forecast (reference institutional outlook): 5-6 months: $95-106 per barrel (geopolitics dominate). 7-9 months: $80-91 per barrel (if the strait opens). 10-12 months: $70-89 per barrel (oversupply + economic slowdown).

🎯 5. Core Conclusion: 1. Short-term (1-2 months): Oil prices will remain in a high oscillation range of $90-105, driven by geopolitical news. The prediction from Chevron's CEO is supported— even if a ceasefire occurs, supply recovery will take time, and oil prices are likely to stay high this summer.

2. Mid-term (3-6 months): This depends on the navigation timing through the Strait of Hormuz. If it does not resume soon, there is an upward risk for oil prices; if it does, OPEC+ production increases combined with weak demand will push the price center downward.

3. Long-term (over 6 months): A loose supply-demand pattern is likely to return, with oil prices potentially gradually retreating to the $70-90 range, but the 'long-term effects' of geopolitical conflicts cannot be ignored.

4. Key Monitoring Indicators: Progress of U.S.-Iran negotiations and Strait of Hormuz navigation status. OPEC+ decision on actual production at the June 7 meeting. Trends in U.S. EIA inventory changes. Global refinery utilization rates and the degree of demand destruction.

Summary: Current oil prices are caught in a tug-of-war between 'geopolitical premiums' and 'demand shrinkage'. The judgment of Chevron's CEO in your screenshot—'oil prices are likely to rise this summer'—has high credibility in the short term (1-2 months), as even if conflicts ease, the repair of supply chains and rebuilding of inventories will take time, and OPEC+'s actual production capacity is constrained. However, in the medium to long term, weak demand and potential supply recovery will exert downward pressure.