« Doms? Where we’re going, we don’t need doms. »

In traditional markets, we have a Depth of Market (DOM) to see the depth of the order book: where the big buyers are, where the sellers are hiding, how far an order will push the price.

But in the Alpha market… there is no DOM. 🥶

How to place orders in geometric progression, manage risk, feel if the market is deep or shallow when we can't see the order book? 🤔

We will reconstruct an implicit depth from the price movement between the Bollinger bands, with a small discrete energy (graph / Laplacian). 💪

1. Why DOM is so valuable (and what we lose without it)

On a classic Spot pair (BTCUSDT, ETHUSDT…), the DOM gives you:

the best bids and asks,

the volumes at each price level,

the cumulative depth up to ±0.1%, ±0.5%, ±1%, etc.

For a trader, it serves to:

identify the walls (large limit order blocks),

spread a ladder of orders (geometric progression of sizes/prices),

know if a large order will move the price by 0.05% or 2%.

On the Alpha market, all this is invisible.😱

You only see the traces of transactions in the price.🤷♂️

The idea: use these traces to guess the hidden depth.💪

2. Place the price in a Bollinger tunnel

We start from a series of prices, at regular time intervals (for example every second or every minute).

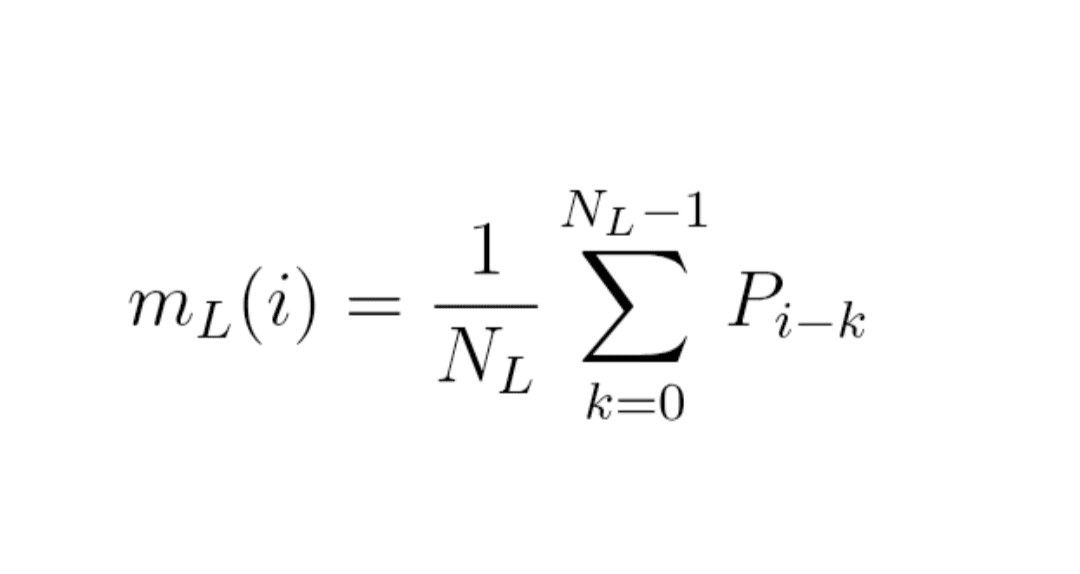

2.1. Moving average and standard deviation

On a window of length (for example 20 or 60 points), we define:

Formula (1): moving average

m_L(i) = (1 / N_L) × sum for k from 0 to N_L − 1 of P_{i − k}

In other words,

m_L(i) = (P_i + P_{i−1} + … + P_{i−N_L+1}) / N_L.

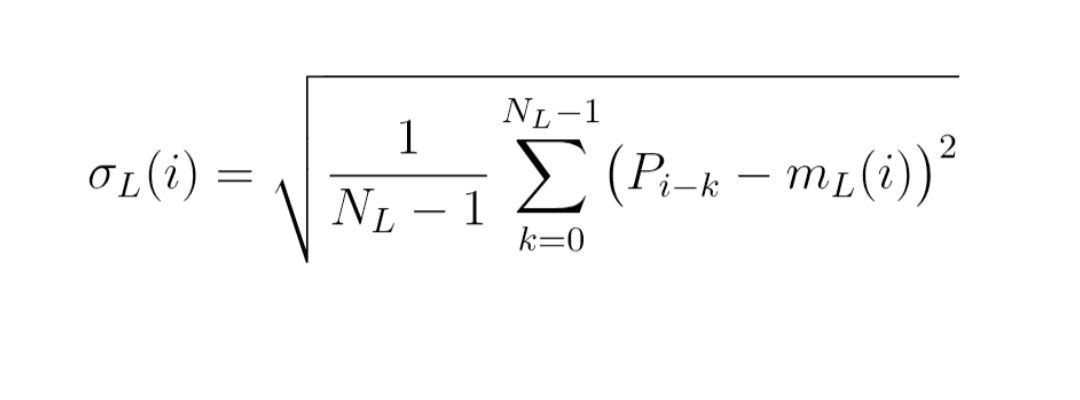

Formula (2): moving standard deviation

σ_L(i) = square root of

[ 1 / (N_L − 1) × sum for k from 0 to N_L − 1 of (P_{i−k} − m_L(i))² ]

It's just the classical standard deviation, calculated on the sliding window of the last prices.

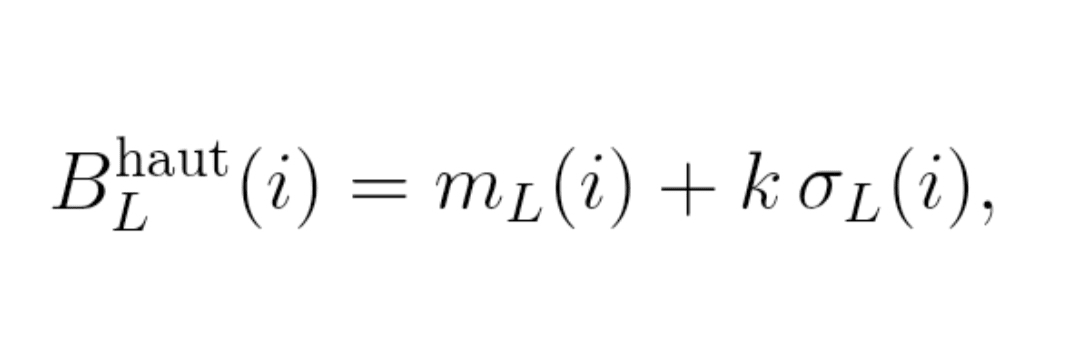

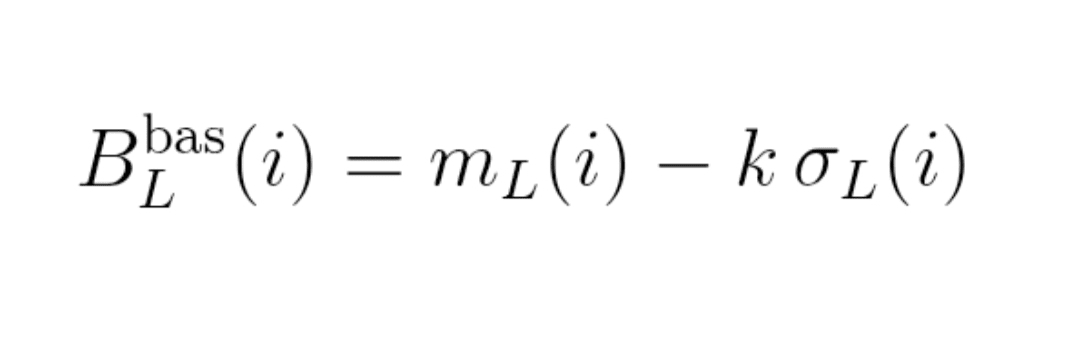

2.2. Bollinger Bands

Bollinger bands at standard deviations (typically k = 2) are:

Formula (3): bands

Upper band: B_L^high(i) = m_L(i) + k × σ_L(i)

Lower band: B_L^low(i) = m_L(i) − k × σ_L(i)

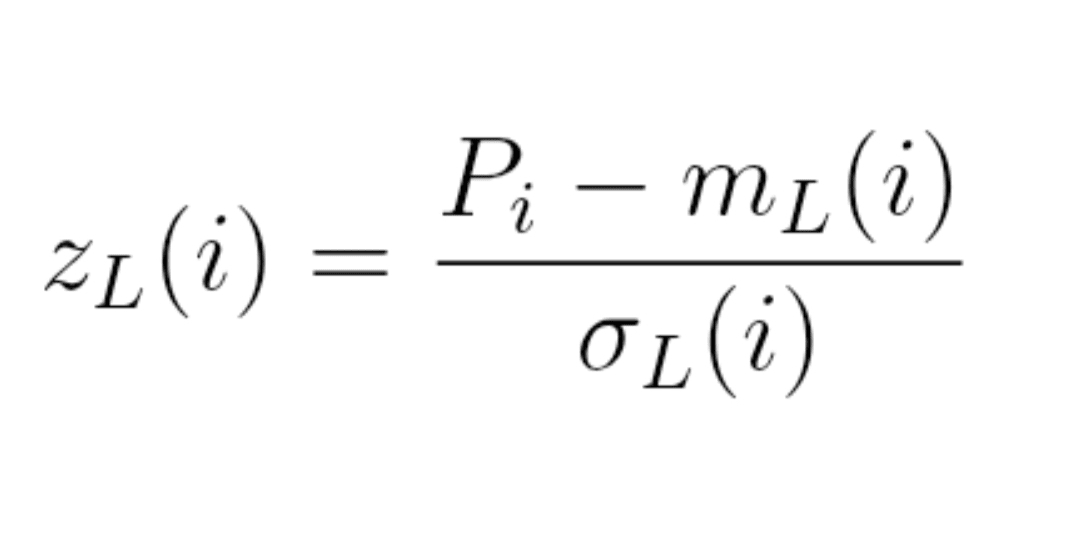

2.3. Normalized price in the tunnel

We then look at where the price is in terms of number of sigmas:

Formula (4): normalized price

z_L(i) = (P_i − m_L(i)) / σ_L(i)

z_L(i) ≈ 0: price at the center of the tunnel,

|z_L(i)| ≈ 1, 2, 3: price approaching or hitting the bands.

Everything that follows happens in this normalized framework z_L.

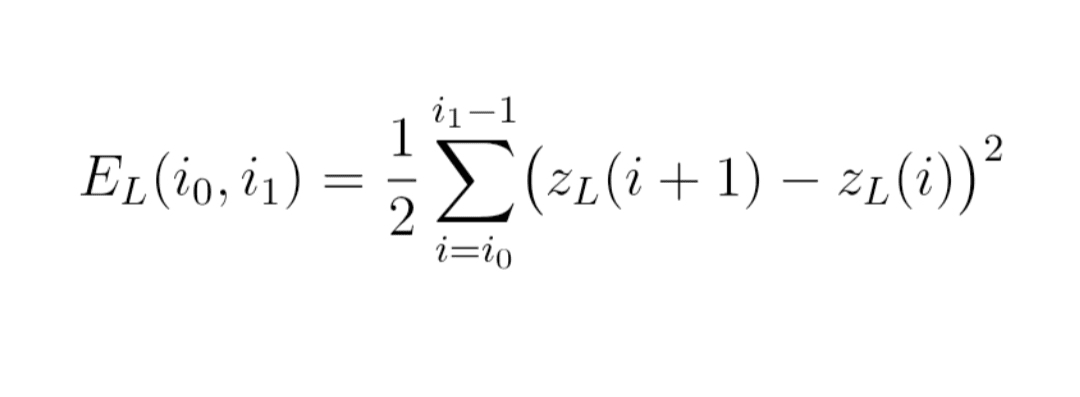

3. Measure the 'ruggedness' of the price between the bands

Intuition:

Deep market → the price slides rather smoothly in its tunnel.

Hollow market → the price is nervous, choppy, jumps very quickly from one side to the other of the tunnel.

We measure this ruggedness with discrete Dirichlet energy.

We consider a window of indices from i_0 to i_1.

Formula (5): energy E_L

E_L(i_0, i_1)

= 1/2 × sum for i from i_0 to i_1 − 1 of [ z_L(i+1) − z_L(i) ]²

Then we normalize by the length of the window to obtain a density:

Formula (6): energy density ε_L

ε_L(i_0, i_1) = E_L(i_0, i_1) / (i_1 − i_0)

Reading:

small ε_L → rather smooth z_L trajectory,

large ε_L → very choppy z_L trajectory.

In short, ε_L measures how much the price 'wiggles' inside its Bollinger tunnel, regardless of the price scale (thanks to normalization by σ_L).

4. Implicit depth: a simple score Λ_L

We now want to link this ruggedness to market depth.

4.1. Small stylized model

We note:

Formula (7): elementary return

r_i = log(P_{i+1}) − log(P_i)

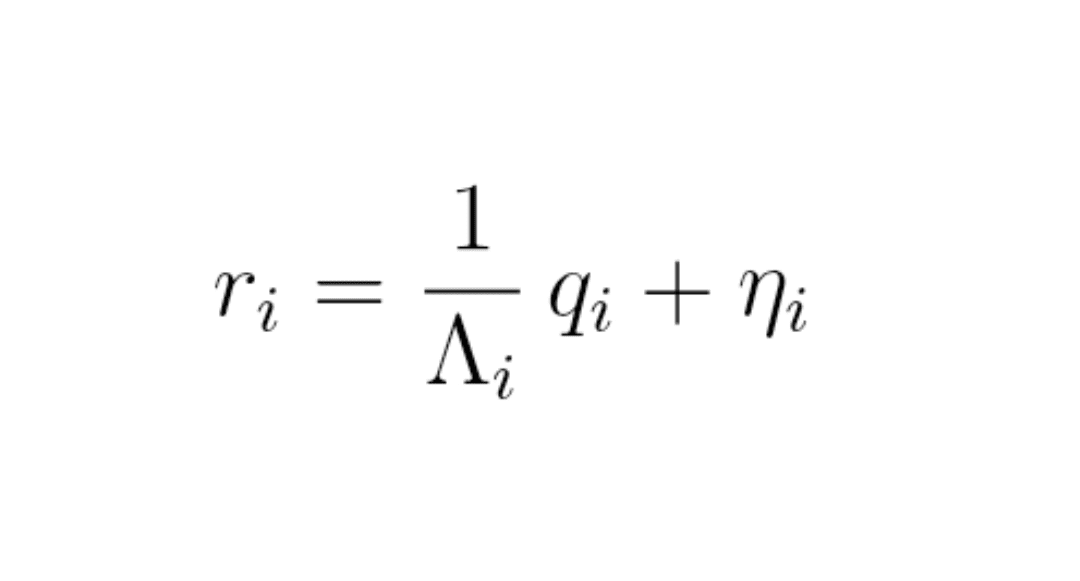

We assume a very simple model:

Formula (8): microstructural model

r_i = (1 / Λ_i) × q_i + η_i

where:

q_i = order imbalance (market buys − market sells) over the interval,

Λ_i = local market depth,

η_i = 'noise' (news, fundamental flow…).

Without DOM, we see neither q_i nor Λ_i.

But we see r_i, therefore z_L, hence ε_L.

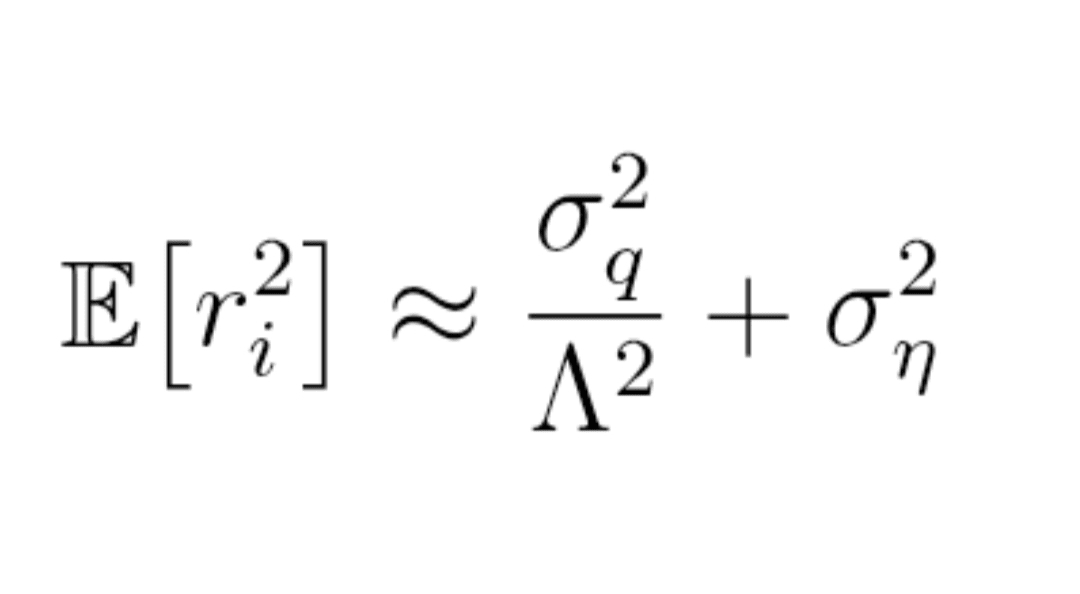

By reasoning on variances and grouping constants, we arrive at a relationship of the type:

Formula (9): variance of returns (diagram)

E[r_i²] ≈ σ_q² / Λ² + σ_η²

(on average over the window, σ_q and σ_η are constants, Λ the typical depth).

The key idea: the smaller Λ is, the larger the term σ_q² / Λ² is, thus the larger r_i² is → the more the price is shaken for the same order flow.

By linking z_L and r_i (z_L is roughly the return divided by σ_L), we find that ε_L increases when Λ decreases.

Thus, a very simple implicit depth score 👇

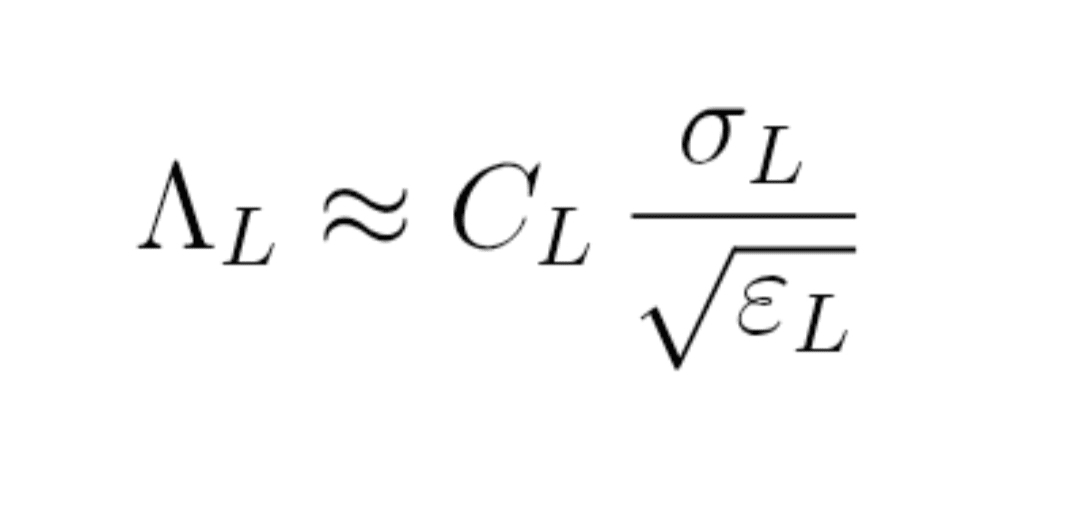

4.2. Practical definition of score Λ_L

Formula (10): implicit depth score

Λ_L ≈ C_L × σ_L / square root of ε_L

where:

σ_L = local volatility,

ε_L = energy density,

C_L = constant to calibrate on a pair where the DOM is visible.

Reading:

large Λ_L → the market absorbs order flows well → strong depth.

small Λ_L → the price 'jumps' a lot for the same σ_L → hollow market.

You now have an implicit depth index without seeing the book. 🤩

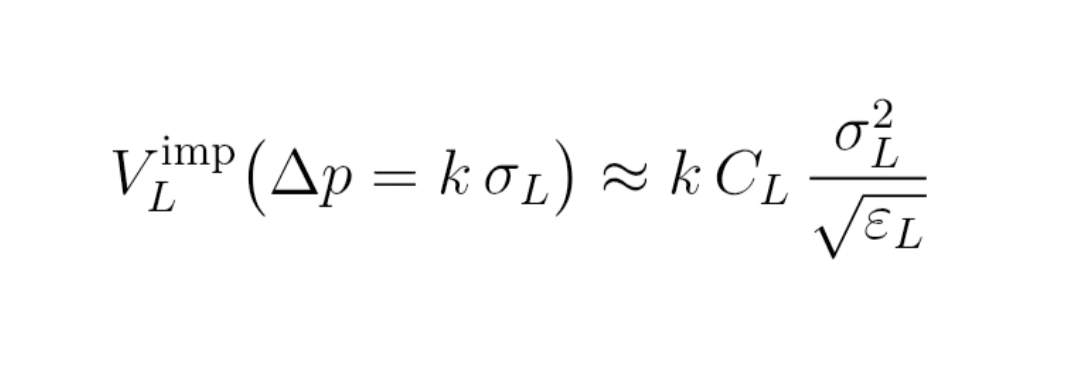

5. Implied volume up to the bands

In many microstructure models, the volume needed to move the price by a certain Δp is proportional to Λ_L × |Δp|.

If we look at what happens up to the bands at k standard deviations:

Δp = k × σ_L.

We can then define an implied volume up to the bands:

Formula (11): implied volume V_L^imp

V_L^imp (Δp = k σ_L)

≈ k × C_L × σ_L² / square root of ε_L

This V_L^imp is an order of magnitude of the volume that would be needed (on average) to sweep the hidden book up to the Bollinger bands.

On a pair with DOM, you can compare:

V_L^imp ↔ actual cumulative volume in the book.

On the Alpha market, you only have V_L^imp… but it's already a compass. 🧭

6. How to implement this on Binance

6.1. Phase 1: calibration on a pair with visible DOM

1. Choose a very liquid pair (BTCUSDT, ETHUSDT Spot).

2. In live:

retrieves prices (trades or 1s candles),

retrieves DOM snapshots (cumulative depth up to ±0.1%, ±0.5%, ±1%, etc.).

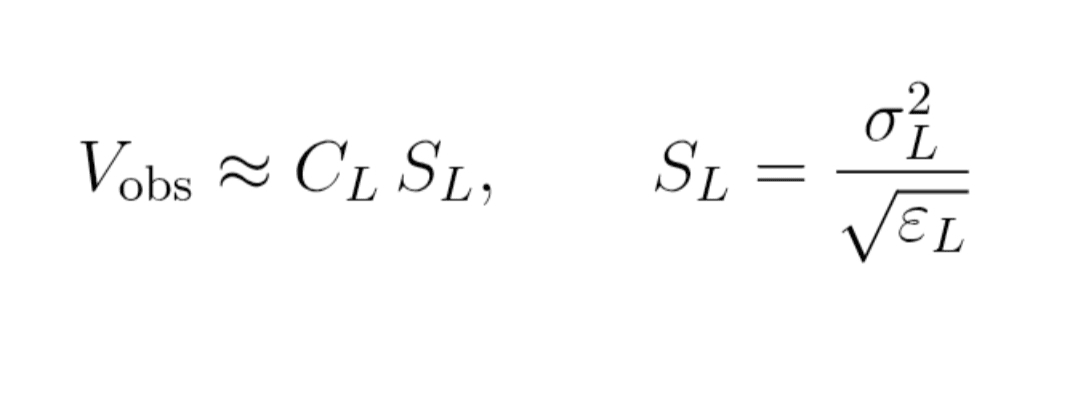

3. For each window:

calculate m_L, σ_L, ε_L,

calculate the raw indicator S_L = σ_L² / square root of ε_L,

measures the actual cumulative volume V_obs in the DOM up to Δp = k σ_L.

4. Perform a simple regression:

Formula (12): empirical relationship

V_obs ≈ C_L × S_L

(with S_L = σ_L² / √ε_L)

You deduce the constant C_L for this scale L.

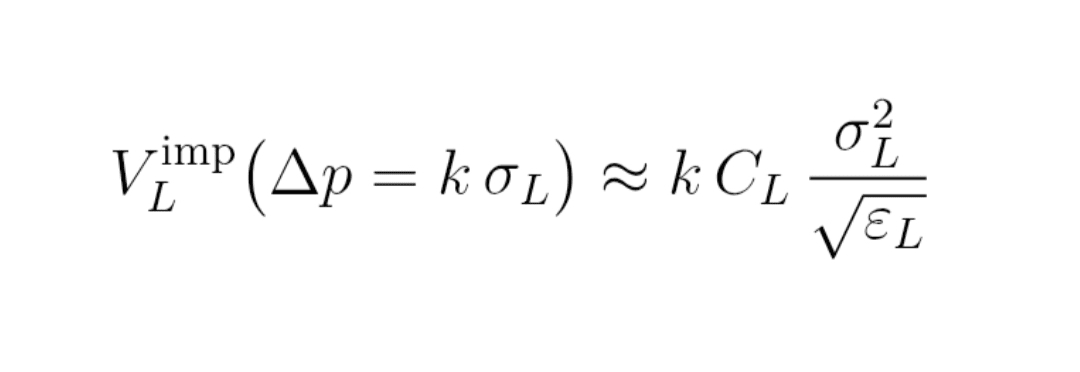

6.2. Phase 2: application on the Alpha market (without DOM)

1. On your Alpha pair:

retrieves prices live,

calculate m_L, σ_L, ε_L.

2. Apply the formula:

Formula (13): final implied volume

V_L^imp (Δp = k σ_L) ≈ k × C_L × σ_L² / √ε_L

3. Display in real time:

the score Λ_L,

the curve Δp ↦ V_L^imp (your phantom DOM).

7. Concrete use for your orders

7.1. Build a ladder depending on Λ_L

If Λ_L is high: deep market,

you can:

bring the levels of your geometric progression closer,

keep order sizes fairly regular.

If Λ_L is low: hollow market,

you can:

space the levels further apart,

reduce the size of orders close to the price,

keep volume for further levels.

7.2. Read the implicit 'liquidity holes'

By looking at Λ_L in real time:

Λ_L drops sharply while σ_L does not change much:

alert: the market is becoming fragile,

you can reduce leverage, widen stops, avoid aggressive 'market'.

Λ_L rises after a shock:

sign of resilience: depth returns, the market recovers.

8. Limits and common sense

It is not an oracle:

does not see the spoofers,

does not include macro news,

does not replace your money management.

The indicator depends:

the choice of the window N_L,

on the quality of calibration C_L,

the granularity of the data.

To use as:

an implicit depth radar, complementing your technical analysis,

not as a magic 'buy/sell' button.

9. To go further

This article gives the 'trader' version.

Behind, there is a small theory:

function z_L viewed as a function on a chain (graph),

Dirichlet energy,

link with the heat equation and progressive smoothing.

In a separate math article, we will detail all this properly, with demonstrations supporting it on the TikTok account @Maths4Traders 💪🤩