Japan has spent years looking like a country that should have owned a larger piece of the crypto market. It had the exchanges, the banks, the retail appetite and the technical talent. What it also had was a tax regime harsh enough to push people into silence, delay or departure.

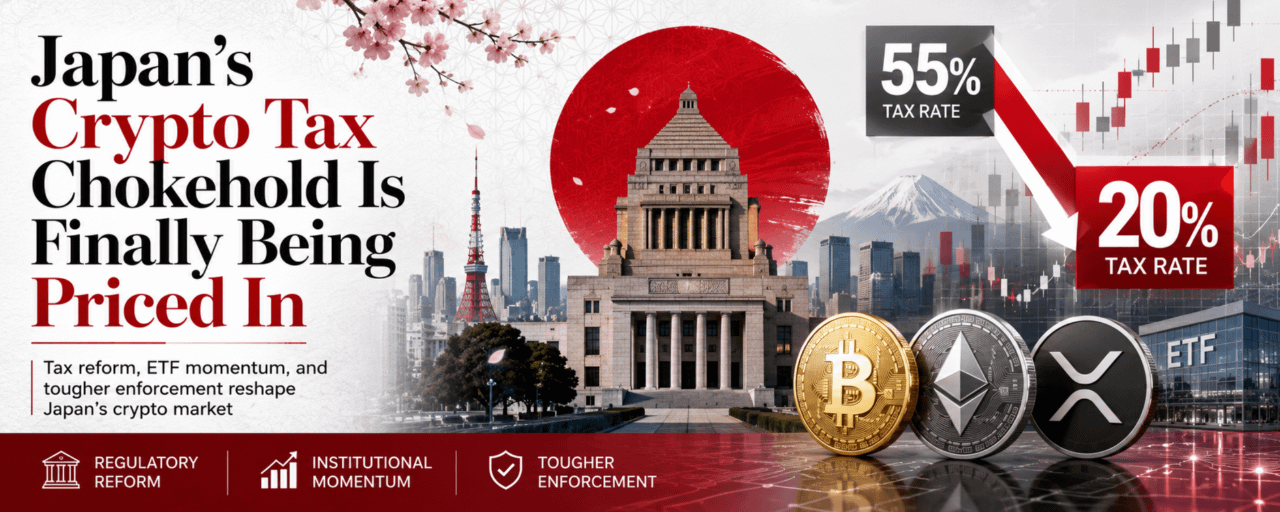

A Tokyo trader could make a clean Bitcoin, Ethereum or XRP trade and still face a progressive tax bill running as high as 55%. That number sits inside the trade before the order is even placed. It changes position size. It changes whether a founder stays in Tokyo or takes meetings in Singapore’s Marina Bay offices. It changes whether a fund manager builds a local product or leaves crypto in the same half-open drawer where Japanese institutions have kept it for years.

On Thursday, June 11, Japan’s House of Representatives approved amendments to the Financial Instruments and Exchange Act, sending the bill to the House of Councillors for final passage. If it clears that chamber, crypto assets such as Bitcoin, Ethereum and XRP would be pushed much closer to the legal treatment of stocks and bonds.

The tax change is the part traders will feel first. Crypto profits that can now be taxed at rates of up to 55% would move to a fixed 20% rate from 2028. For retail traders, that is not a branding exercise around “digital asset innovation.” It is the difference between keeping enough profit to justify the risk and watching more than half of a good year disappear into the tax bill. For institutions, it is the difference between a product memo getting killed by the tax team and one that survives long enough to reach the investment committee.

The ETF calendar gives the reform a harder edge. Japan Exchange Group has been looking toward Bitcoin and crypto ETFs by 2027, which means brokers, custodians, fund administrators and compliance teams in Tokyo do not have the luxury of treating this as some distant policy debate. If crypto is brought into the FIEA framework as a financial product, spot Bitcoin ETFs and other crypto ETFs become easier to structure without pretending every token exposure lives in a separate legal universe.

Inside firms, the arguments will be less elegant than the public language. Legal teams will be asking who gets to see token listing discussions before they go live. Compliance officers will be deciding whether a research note, custody mandate or ETF seed conversation creates material nonpublic information. Operations teams will have to separate wallet control, brokerage activity, custody reporting and product structuring in ways that satisfy rules built for listed equities but now being stretched over crypto rails.

The harder side of the bill is enforcement. Insider trading restrictions similar to those used for listed equities would extend into cryptocurrency trading, and penalties for selling unregistered digital assets would rise from three years to as much as 10 years in prison. That changes the room. A token issuer arguing with counsel over whether an asset is “unregistered” is no longer arguing over paperwork or delay. Under this framework, the wrong answer could become a criminal sentence measured in a decade.

The Financial Services Agency has described the changes as a way to improve trading conditions and support innovation in digital assets. Koichi Kano, head of QCP Group Japan, told Bloomberg the reform could reduce uncertainty for crypto companies by giving businesses and investors a more uniform framework. The official version is clean. The working version is messier: rewrite the manuals, redraw the walls between teams, document every internal conversation that might later look like market-sensitive information.

SBI Holdings is already moving while that work begins. Through SBI VC Trade, it recently launched Solana trading and custody services, adding another major network to its crypto business just as Japan’s regulatory ground starts shifting toward securities-style treatment. A bank-linked crypto operation does not add Solana as if it is just another retail ticker. It adds wallet procedures, custody controls, trading permissions, reporting lines, legal reviews and internal sign-offs around an asset that may soon sit much closer to Japan’s securities perimeter.

Somewhere inside SBI, a compliance officer has a Monday morning problem that no policy speech can soften: Solana is live, ETFs are moving toward the calendar, the tax regime may be changing, and the wrong unregistered sale could carry a 10-year sentence.

#SPCXxIPOCampaignOnBinanceWallet #JapanPassesCryptoFinancialProductsBill #USIranConflictLiftsOilAsianStocksFall #USCPISurgesToThreeYearHighOf4.2% #CFTCProposesRulesForPredictionMarkets