Brothers

The boots have dropped, and they landed in the most uncomfortable direction.

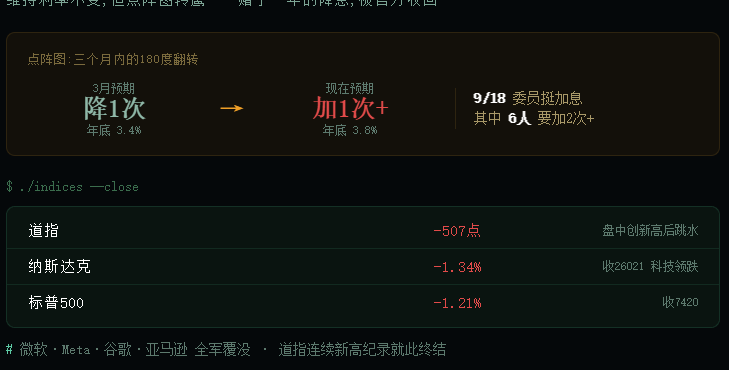

Last night, the Fed held its meeting, and the interest rates stayed unchanged at 3.50% to 3.75% as expected. But the real bombshell was in the dot plot: 9 out of 18 committee members believe there should be at least one rate hike this year, with 6 thinking it needs to be more than two. The median expectation for year-end rates shot up from 3.4% in March to 3.8%. The market reacted fast and has already fully priced in a rate hike before October.

You gotta realize that just three months ago, the Fed's dot plot was saying there’d be one rate cut this year. In just three months, it flipped from a cut to a hike. That’s the weight of this hammer.

The market flipped on the spot. The Dow was still setting a third consecutive new high at 52190 when the Fed's statement dropped, causing a dive and a close down 507 points at 51492. The S&P fell 1.21% to close at 7420, and the Nasdaq dropped 1.34% to 26021, with tech heavyweights like Microsoft, Meta, Google, and Amazon all getting wrecked.

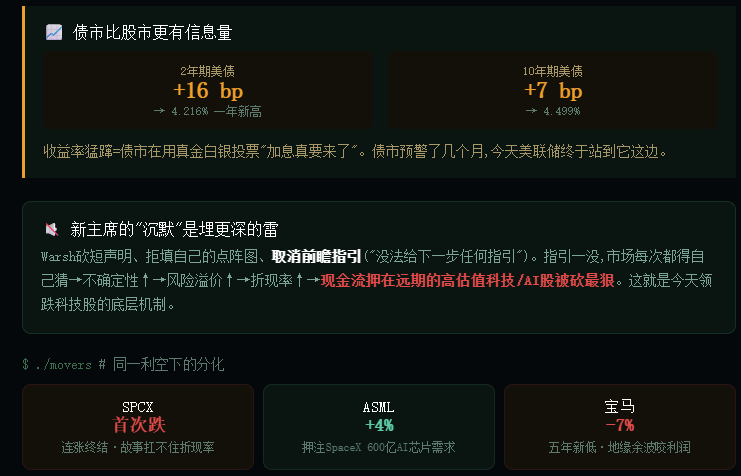

[The bond market has more informative declines than the stock market.]

What we should really be looking at this time is not the stock indices, but bonds. The two-year U.S. Treasury yield surged by 16 basis points in a day to hit 4.216%, marking a new high in over a year. The ten-year yield also rose nearly 7 basis points to 4.499%.

Why is the bond market more worthy of attention? Because it most directly reflects interest rate expectations. The yields skyrocketing means the bond market is voting with real money, believing that rate hikes are really coming. There's a saying that hits the mark: this is a victory for the bond market, as it has been warning about rate hikes for several months. Today, the Fed finally aligned with the bond market. The surge in short-term bond yields speaks volumes, even more than stocks hitting their limit down.

[The new chairman's "silence" is actually a deeper landmine.]

This time, there's an easily overlooked change: the new chairman, Warsh, significantly shortened the Fed's policy statement and unusually refused to fill in his own vote on the dot plot, clearly stating that he would no longer provide forward guidance. His exact words were, 'I can't give you any guidance on the next steps.'

This situation is more subtle than the rate hikes themselves. For the past decade, the market has gotten used to the Fed spoon-feeding the interest rate path, allowing everyone to price accordingly based on expectations. Now that the forward guidance has been removed, it means that every meeting will require the market to guess, structurally increasing uncertainty.

And with uncertainty rising, the most affected are precisely the tech and AI high-valuation growth stocks. The reasoning lies in valuation models: a stock's price is the result of future cash flows discounted to today. The discount rate includes both interest rates and risk premiums. With forward guidance gone and uncertainty rising, risk premiums are pushed higher, leading to elevated discount rates. As the discount rate rises, companies betting on cash flows far in the future get hit the hardest. The AI and semiconductor sectors almost perfectly correspond to this definition. This also explains why tech stocks are leading the declines today instead of others.

[On the stock level, there are a few details worth noting.]

SPCX ended its consecutive gains since listing and saw its first decline. This stock, sustained by one story after another, bowed for the first time in the face of such a tangible negative from rate hikes, confirming an old truth: no matter how sexy the story, it can't withstand the recalibration of the discount rate.

An interesting counterexample is ASML, which rose 4% against the tide because the market is betting that SpaceX's $60 billion AI acquisition will drive more demand for chip equipment. In the same bearish environment, some got hit hard due to story breakdowns, while others are seeing their expectations rise due to real orders. This divergence itself is a signal of selective funding during the rate hike cycle.

There's also an overseas alarm: BMW's stock price has dropped to a five-year low, plummeting nearly 7%. They lowered their full-year profit expectations while also citing two key issues: weak demand in China and rising energy prices due to the Iran conflict dragging down global consumer sentiment. Note the latter part; it shows that the so-called geopolitical headwind that was supposedly resolved still has its aftershocks, biting into corporate profits through oil prices and energy costs, not something that can just be wiped away with a signed agreement.

This week has seen a rollercoaster from the crash on June 5 to a rebound, new highs, and now the Fed's decisive hammer. The main storyline is clear: after a year of betting on rate cuts, the market has officially retracted that expectation today. Geopolitics are just a subplot, SpaceX is fireworks; the real drivers remain the basics of interest rates and inflation.

⚠️ Risk Reminder: Investing carries risks. The Fed has signaled rate hikes, and the market's pricing logic has shifted from betting on rate cuts to guarding against rate hikes. High-valuation sectors are facing re-evaluations, and subsequent volatility may increase. The above is purely my personal observation and sharing; it does not constitute any investment advice. Please make rational decisions based on your risk tolerance #美股超话 .