Hey guys, the US stock market is closed this weekend, but when it opens on Monday, it's going to be a week packed with hard-hitting news.

Last week, the Fed made some hawkish comments, and this week it's time for real data to confirm whether they have the backbone to back it up. I’ve lined up the confirmed highlights for you day by day.

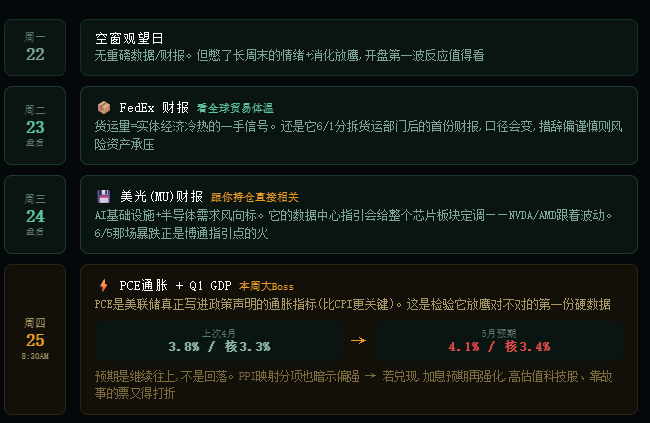

[Monday 6/22 · No Major Events]

Let's be clear, there are no major earnings reports or data releases on Monday (multiple economic calendars note that June 22nd has no significant events). But that doesn't mean it's all quiet—it's a day to digest the Fed's hawkish stance while waiting for a few bombshells to drop. Last Friday's market closure due to Juneteenth means traders have been holding their breath through a long weekend, so the initial response when the market opens on Monday is definitely worth watching.

(Correction on the date: June 22 is Monday. The following is arranged by the actual date.

[Tuesday 6/23 after market close · FedEx earnings report, gauging the pulse of global trade]

FedEx will publish its FY2026 Q4 report after market close on June 23. Why is this worth watching? Because it serves as a barometer for global trade and supply chain demand—how well freight volumes perform directly reflects the health of the real economy, providing firsthand signals that government data cannot.

There's also a special context: This is FedEx's first earnings report after splitting off its freight division (FedEx Freight) for independent listing on June 1, so its metrics and guidance will differ from the past. The market will be keen to see how it interprets the post-split business. If it adopts a cautious tone regarding global demand, risk assets usually feel the pressure.

[Wednesday 6/24 after market close · Micron (MU) earnings report, this is directly related to your holdings]

This is the key watch for the crypto and tech audience this week. Micron is holding its Q3 earnings call on June 24 in the afternoon.

Its significance lies in the fact that Micron is one of the most important indicators of AI infrastructure spending and semiconductor demand. Its forward guidance on data center investments is closely watched by institutions. In plain terms, what Micron says will directly influence the tone of the entire chip sector—including NVDA, AMD, and others.

Remember how this all started? The catalyst for the crash on June 5 was Broadcom's AI chip guidance not meeting expectations. Now it's Micron's turn to provide a new reference for the market; whether its guidance is strong or weak will likely lead to short-term volatility in a bunch of AI stocks.

[Thursday 6/25 at 8:30 AM · This week's real big Boss: PCE inflation data]

This is the core of the week and the moment of suspense revelation. The May PCE price data and the final valuation of Q1 GDP will be released simultaneously on June 25 at 8:30 AM.

Why is PCE more critical than the previous CPI? Because PCE is the inflation indicator that the Fed actually writes into its policy statements and uses for decision-making—CPI uses a fixed basket while PCE captures changes in consumer behavior. During energy-driven inflation periods, they can diverge significantly. Last week, the Fed dared to be hawkish based on its inflation judgment, and this PCE is the first hard data to test whether that judgment is right.

What’s even more critical is the market's expected direction. Last time (April), the PCE was headline 3.8% and core 3.3%, with core 3.3% being the largest annual increase since the end of 2023. This time, the expectation for May isn't a drop but a continued rise—some economists (Wells Fargo) expect the headline to spike to 4.1% due to energy costs, with core hitting 3.4%. Moreover, a professional signal from last month's PPI has already hinted that this PCE will show a strong reading.

Translating to plain speak: If the PCE really moves up as expected, it would provide the Fed with another solid piece of evidence for its hawkish stance, further strengthening rate hike expectations. Overvalued tech stocks and those propped up by stories are going to get repriced. This data will be the real exam for the question of 'are we hiking rates or not?' for the past two weeks.

[About 'Russell Index Rebalancing'—I must honestly say this]

Someone mentioned that the Russell Index annual rebalancing is also happening this week (usually brings massive trading volume). Historically, Russell rebalancing does occur on a Friday at the end of June, but I couldn't confirm the exact date or whether it falls this week from authoritative calendars, so I won't state it definitively. We'll wait for official confirmation before discussing; no unverified info here.

[How to view this week]

Putting this week together, it actually forms a clear 'verification chain': FedEx verifies trade demand, Micron verifies AI chip demand, and Thursday's PCE verifies whether inflation is actually retreating and whether the Fed's hawkish stance holds water.

Last week, the market was jumping back and forth between 'hawkish sell-off' and 'next-day bounce', indicating that everyone was uncertain. After this week, at least the PCE, the hardest number, will be on the table—whether it will continue to ferment rate hike fears or ease up due to not-so-bad data will become much clearer. Before Thursday's data comes out, this kind of jittery tug-of-war is likely to persist.

⚠️ Risk alert: Investing involves risks. This week’s PCE inflation data and multiple earnings reports may trigger significant volatility as market pricing logic shifts from 'betting on rate cuts' to 'hedging against rate hikes'. The above is purely personal observation and forward-looking sharing, not investment advice. Please make rational decisions based on your risk tolerance #美股超话 .