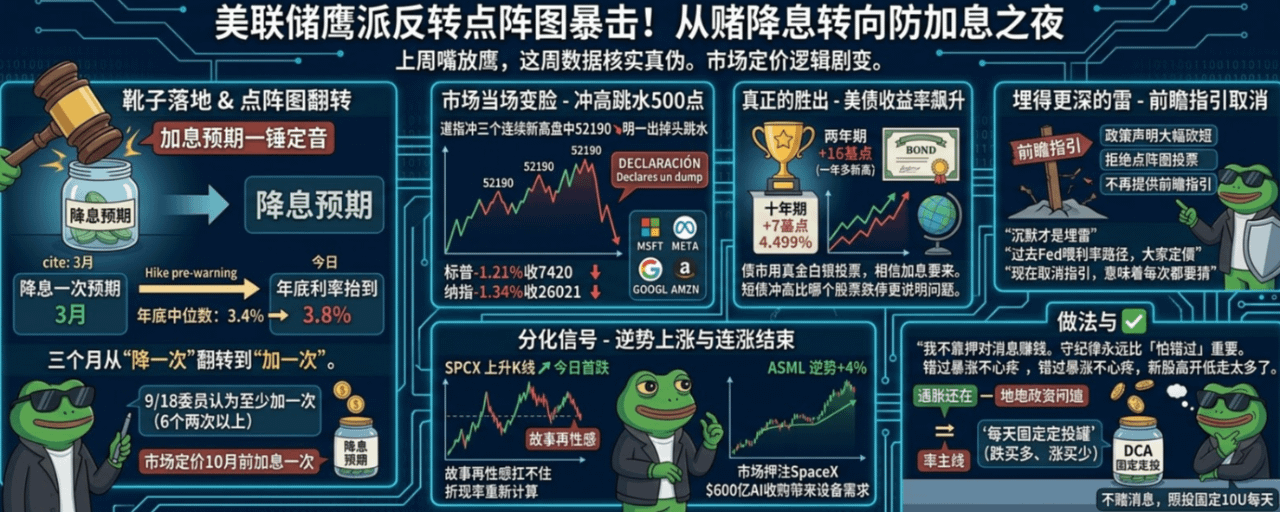

Just got back from a long weekend (the market was closed last Friday for Juneteenth) and the US stock futures are dipping ahead of Monday's open. You probably guessed it, it's all about Iran.

The plot thickens. The US and Iran kicked off the first round of high-level talks on Monday, which is usually a good sign, but Trump threw a wrench in the works, saying if Hezbollah continues to attack Israel, he'll strike back and warned Iran not to think about closing the Strait of Hormuz again.

Iranian media hinted at a pause in negotiations due to protests, although insiders say talks are still ongoing. Oil prices are being yanked around by this news; Brent initially surged over 2% pre-market, then pulled back to around 80.

See, that signed "peace agreement" from last week is already showing cracks as soon as the week opens. I mentioned before, when the switch for ups and downs is in Trump's hands, no removal of negative news is a sure thing. So-called peace could also be a serial drama playing out in installments.

[But the real main dish isn't Iran, it’s Thursday]

Although pre-market was stirred by geopolitics, the market's attention has actually shifted to this Thursday—PCE inflation data.

Let's clarify last week first. Despite the Fed being hawkish, U.S. stocks overall actually rose last week, with the Nasdaq leading up 2.43%, S&P up 0.93%, and Dow up 0.71%. This indicates that the market is temporarily choosing to believe the logic of "the economy is strong enough to withstand rate hikes." Whether this optimism can continue will be tested by Thursday's PCE.

It's the inflation indicator that the Fed truly uses for decision-making, and current expectations are for it to continue rising, not falling. If the data confirms stubborn inflation, last week's gains could be quickly reversed.

[A signal directly related to our positions: storage chips are strengthening against the trend]

This one is worth pulling out separately. Last week, the entire market was shaken by geopolitics and rate hikes, but storage chip stocks hit new highs against the trend—Micron, SanDisk, Seagate, Western Digital all set new records, with SanDisk leading up 3% overnight.

This signal is significant. It means that even in an environment of rising rate hike expectations and overvalued tech stocks being discounted, funds are still willing to dive into "storage chips backed by solid AI demand." This Wednesday, Micron is set to release its earnings report—its data center guidance will directly validate whether this storage stock rally is supported by fundamentals or just emotional impulse. For those tracking NVDA, AMD, this Micron report is the first hard reference point of the week.

Also, Intel deserves a mention. It jumped over 5% overnight, and just last Thursday, it surged 10.6% in a single day due to Trump announcing, "Intel will make chips for Apple in the U.S.," hitting a historical high. There's a clear divergence in strength among chip stocks.

[How to view this week]

Linking today with this week, the main storyline is clear. In the short term, let's see if Iran's drama will spook the market again. Mid-term, keep an eye on Micron's chip guidance on Wednesday and Thursday's PCE inflation data.

Today, Monday, is likely a "low open wait-and-see, waiting for data" pattern—geopolitics has added some chaos, but no one dares to heavily bet on direction before Thursday's PCE comes out.

⚠️ Risk Warning: Investing carries risks. This week’s geopolitical fluctuations, PCE data, and multiple earnings reports could trigger severe volatility. The above is purely personal observation and sharing, not constituting any investment advice. Please make rational decisions based on your own risk tolerance #美股超话 .