Original Title: Prediction Markets at Scale: 2026 Outlook Original Author: INSIGHTS4.VC Translated by: Peggy, BlockBeats

Editor's Note: In 2025, the prediction market is expected to accelerate towards the mainstream: brokers, sports platforms, and crypto products will enter simultaneously, and the demand has been validated. The real watershed is no longer product innovation, but whether scalability can be achieved within the regulatory framework.

This article highlights the global regulatory comparisons, the divergence between on-chain and compliant pathways, and the 2026 World Cup as a 'system-level stress test', indicating that the prediction market is entering a knockout stage centered on compliance, settlement, and distribution. The winner will be the platform that can operate stably under peak load and strong regulation.

The following is the original text:

The U.S. event contract market significantly accelerated in 2025, resonating with the approach of a 'generational-level' catalyst.

Kalshi's valuation doubled to $11 billion, and Polymarket is also reportedly seeking a higher valuation; meanwhile, platforms targeting the mass market—including DraftKings, FanDuel, and Robinhood—are launching compliant prediction products ahead of the 2026 FIFA World Cup (to be held in North America). Robinhood estimates that the event market has generated approximately $300 million in annualized revenue, becoming its fastest-growing business line, indicating that 'opinion-based trading' is entering the financial mainstream on a scalable basis.

However, this growth is colliding head-on with regulatory realities. As platforms prepare for the participation peak driven by the World Cup, prediction markets are no longer just a product issue, but increasingly a 'regulatory design' issue. In reality, the focus of team building is shifting from merely meeting user needs to designing legal qualifications, jurisdictional boundaries, and settlement criteria. The importance of compliance capabilities and distribution collaborations is gradually being equated with liquidity; the competitive landscape is more shaped by 'who can scale operations within allowed frameworks' rather than 'who can launch the most markets'.

The intersecting forces of regulation

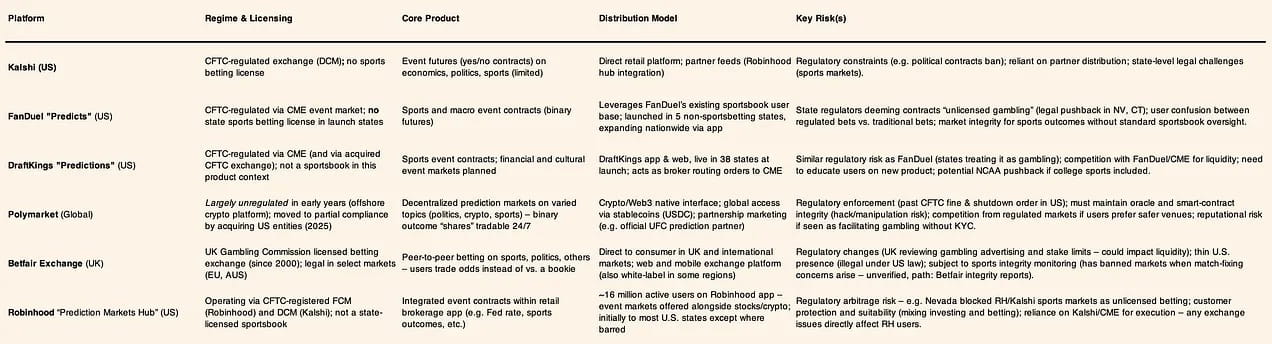

The U.S. Commodity Futures Trading Commission (CFTC) only allows a small category of event contracts tied to economic indicators while deeming other types as unacceptable gambling. In September 2023, the CFTC blocked Kalshi's attempt to launch political futures; however, a subsequent court challenge granted limited approval for contracts related to presidential elections.

At the state level, regulatory attitudes are tougher towards 'sports-like' markets. In December 2025, Connecticut's gaming regulator issued a cease-and-desist order to Kalshi, Robinhood, and Crypto.com, ruling that their sports event contracts constituted unlicensed gambling; Nevada also sought judicial action to halt similar products, forcing relevant platforms to remove them from that state.

In response, established giants like FanDuel and DraftKings are limiting prediction-type products to jurisdictions where 'legal sports gambling is not yet available', highlighting that distribution strategies are increasingly driven by regulatory boundaries rather than user demand. Its core implication is already quite clear: what determines scale is not product innovation but regulatory tolerance. Contract design, settlement terms, marketing language, and geographic expansion paths are being systematically engineered to pass legal qualification reviews; platforms that can operate within an acceptable regulatory framework will gain more durable advantages. In this market, regulatory clarity itself constitutes a moat, while uncertainty directly limits growth.

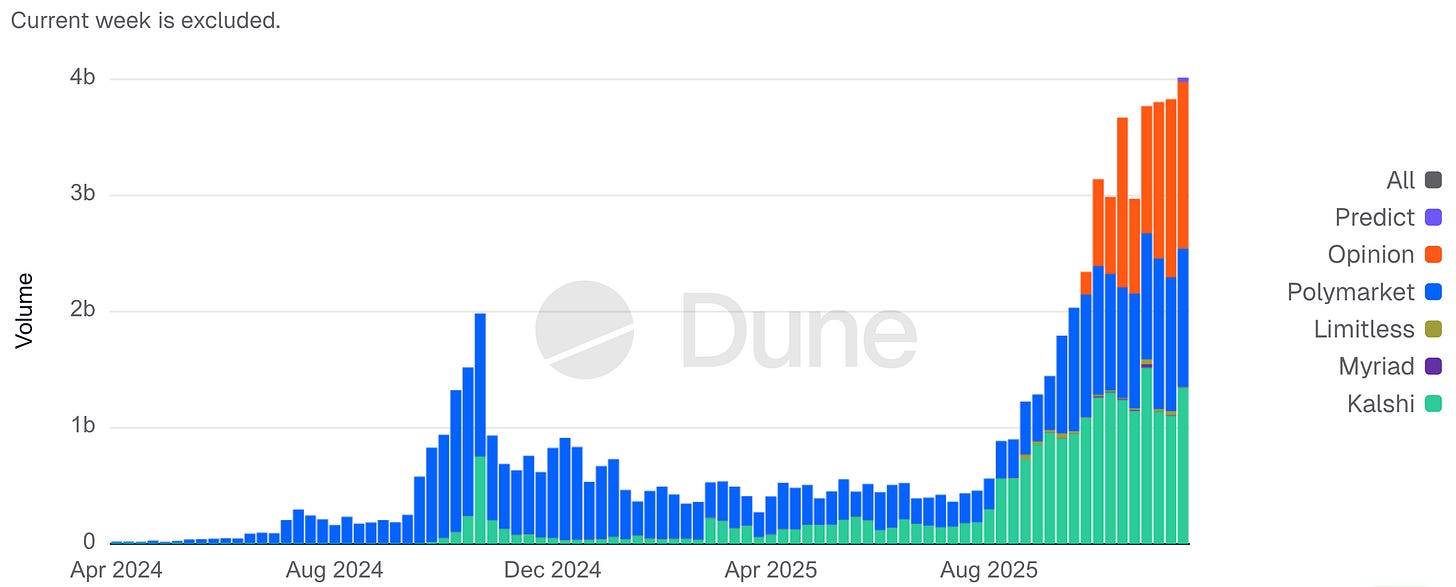

Weekly Prediction Market Notional Volume

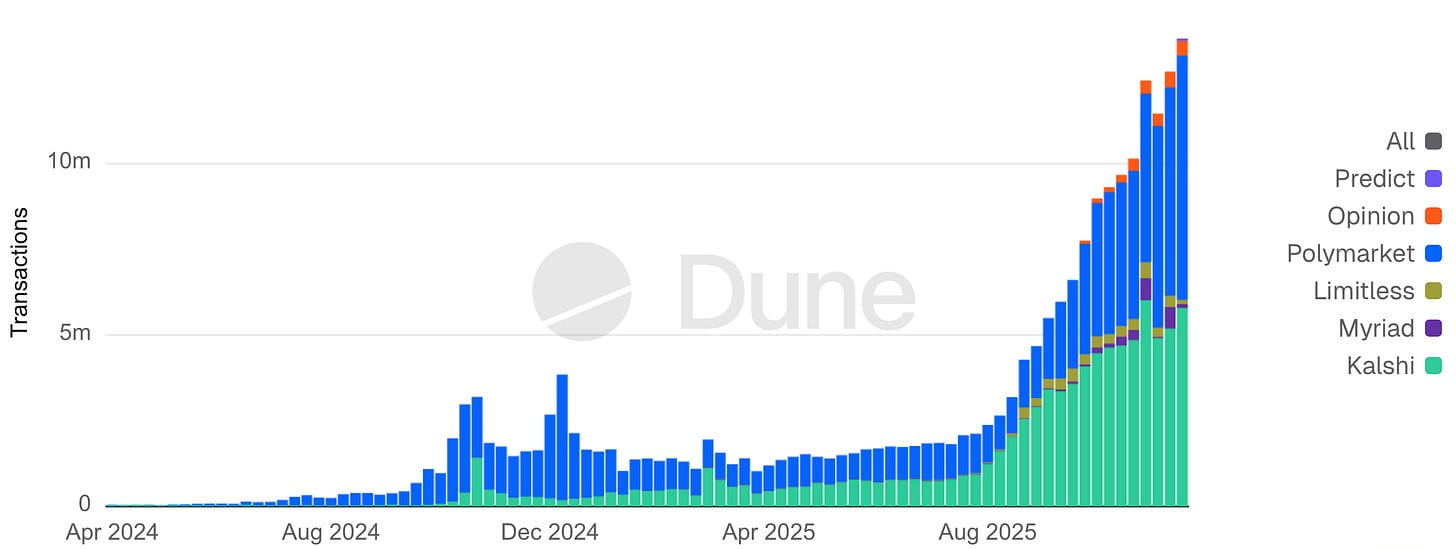

Weekly Prediction Market Transactions

Global comparable cases

Outside the U.S., mature betting platforms and newer licensing regimes indicate that under gambling regulation, event-type markets can achieve liquidity, but their economics and product boundaries are significantly constrained. The UK's Betfair Exchange proved that market depth can also form within a gambling license framework, though strict consumer protection rules limit profitability. Betting in Asian markets is often monopolized by state-run or offshore platforms, reflecting both strong potential demand and ongoing enforcement and fairness challenges. Latin America is moving towards formalization: Brazil opened its regulated gambling market in January 2025, attempting to convert the long-standing gray area into taxable, regulated activities.

The overall trend across regions is consistent: regulation is closing loopholes. Lotteries relying on 'free tokens + prize mechanisms' and social casino models have been restricted or banned in multiple jurisdictions, significantly raising the compliance threshold for any products walking the gambling boundary. The global direction is stricter regulation rather than indulgence in gray areas.

On-chain platform vs Compliance

Decentralized prediction markets once exchanged faster, global access for compliance deficiencies. Taking the crypto platform Polymarket as an example: in January 2022, it was fined $1.4 million by the Commodity Futures Trading Commission (CFTC) for unregistered event swaps and was forced to implement geographical restrictions on U.S. users. Following this, Polymarket underwent a pivot: strengthening internal controls (introducing former CFTC advisors) and acquiring a licensed entity in 2025, allowing it to return to the U.S. in a testing capacity in November 2025. Its trading volume then skyrocketed—reportedly, bets on a single election issue reached $3.6 billion in 2024, with monthly transaction volume reaching $2.6 billion by the end of 2024; and in 2025, it introduced blue-chip investors at a valuation of approximately $12 billion.

On-chain platforms rely on oracles to achieve rapid market establishment and settlement but face the trade-off between speed vs fairness: governance and oracle disputes may delay results, and anonymity raises concerns about manipulation or insider trading. Regulators remain vigilant: even if the code is decentralized, organizers and liquidity providers may still become targets for enforcement (as seen in the Polymarket case). The challenge in 2026 lies in combining 24/7 global markets and crypto's instant settlement innovations with sufficient compliance without sacrificing openness.

User behavior and transaction trends

In 2025, prediction markets experienced simultaneous surges in sports and non-sports events. Industry estimates show that total nominal transaction volume expanded more than tenfold compared to 2024, reaching approximately $13 billion/month by the end of 2025. The sports market became the main 'transaction engine', with high-frequency events generating continuous small transactions; political and macro markets act as 'capital magnets', with fewer transactions but larger individual amounts.

Structural differences are clear: at Kalshi, sports contracts contribute the majority of cumulative transaction volume, reflecting repeated participation by entertainment users; however, open positions are more concentrated in politics and economics, indicating heavier single-position funding. At Polymarket, the political market also dominates open positions, although trading frequency is lower. Conclusion: sports maximize turnover, non-sports concentrate risk.

This creates two types of participants:

Sports users: more like 'traffic traders', multiple small transactions driven by entertainment and habit;

Political/macroeconomic users: more like 'capital allocators', few but large, pursuing information advantages, hedging, or narrative influence.

Platforms therefore face dual optimization: maintaining traffic participation while providing trust and fairness for capital-driven markets.

This also explains the concentration of risks: controversies in 2025 mainly arose in non-sports areas, including objections from U.S. collegiate sports regulators to contracts related to student athletes. Platforms quickly delisted related contracts, indicating that governance risks rise with funding concentration and information sensitivity, rather than merely with pure transaction volume growth. Long-term growth depends on whether high-impact non-sports markets can operate without crossing regulatory or reputational red lines.

2026 World Cup: System-level stress test

The FIFA World Cup will be jointly hosted by the United States, Canada, and Mexico, and should be regarded as a full-stack stress test of event trading and compliant betting infrastructure. Historical analogies suggest:

The 1994 World Cup primarily tested entities and venues; the 1996 Atlanta Olympics shifted critical paths towards communication, information distribution, and emergency response. IBM's 'Info '96' concentrated on timing and results, telecoms expanded cellular networks, and Motorola deployed large-scale intercom systems; the Centennial Olympic Park explosion on July 27 of that year underscored the importance of system integrity and resilience under pressure.

The pressure points in 2026 will clearly enter the digital + financial coupling layer: the tournament expands to 48 teams, 104 matches, and 16 cities, resulting in multiple concentrated bursts of attention and trading over approximately five weeks. The global betting scale for the 2022 World Cup is widely estimated to be hundreds of billions of dollars, with peak windows bringing extreme short-term liquidity and settlement loads.

The North American compliance track will carry a larger proportion of activities—38 states in the U.S. along with Washington D.C. and Puerto Rico have legalized sports betting to varying degrees, and more funds will flow through KYC, payment, and monitoring systems rather than offshore channels. App-based distribution further tightens the coupling: live broadcasts, real-time contracts, deposits, and withdrawals are often completed in a single mobile session.

For event contracts/prediction markets, observable operational pressure points include: liquidity concentration and volatility during event windows; settlement integrity (data delays, dispute resolution); product and judicial design across federal/states; KYC/AML/responsible gambling/cash withdrawal scalability under peak demand.

The same regulatory and technical stack will also be tested again by the 2028 Los Angeles Olympics, making the 2026 World Cup more like a selection event: it may trigger regulatory intervention, platform consolidation, or market exits, distinguishing the infrastructure built for peak phases from sustainable, compliant scaled platforms.

Payment and settlement innovation

Stablecoins are transitioning from speculative assets to operational infrastructure. Most crypto-native prediction markets complete deposits and settlements in U.S. dollar stablecoins, and regulated platforms are also testing similar pathways. In December 2025, Visa launched a pilot in the U.S., allowing banks to use Circle's USDC for on-chain settlements 24/7, building on cross-border stablecoin experiments that began in 2023. In event-driven markets, stablecoins (when permitted) provide instant access, global coverage, and settlement advantages that match continuous trading periods.

In practice, stablecoins resemble settlement middleware: users treat them as faster deposit and withdrawal tools; operators benefit from lower failure rates, improved liquidity management, and nearly instant settlements. Thus, stablecoin policy has a second-order impact on prediction markets: restricting stablecoin channels increases friction and slows withdrawals; clear regulation benefits deep integration of mainstream gambling and brokerage platforms.

However, there are also resistances. Christine Lagarde warned in 2025 about the currency stability risks of private stablecoins and reiterated support for the central bank digital euro; the European Central Bank also indicated in its November 2025 (financial stability assessment) that stablecoin expansion could weaken banks' funding sources and disrupt policy transmission. A more gradual integration is likely to occur in 2026: more gambling platforms accept stablecoin deposits, payment institutions bridge cards to crypto while strengthening licensing, reserve auditing, and disclosures, rather than fully endorsing native crypto payment tracks.

Macro liquidity background

Evaluating the prosperity of 2025 requires skepticism: loose funds will amplify speculation. The Federal Reserve's shift to end quantitative tightening by the end of 2025 may result in slight liquidity improvements in 2026, affecting risk preferences rather than adoption direction. For prediction markets, liquidity impacts participation intensity: abundant funds → transaction amplification; tightening → marginal speculation cools.

However, the growth in 2025 occurred in a high-interest-rate environment, indicating that prediction markets are not primarily driven by liquidity. A more reasonable framework is to view macro liquidity as an accelerator rather than an engine. Long-term factors—mainstream distribution of brokerage/gambling, product simplification, and enhanced cultural acceptance—better explain baseline adoption. Monetary conditions affect amplitude but do not determine whether it occurs.

'Missing elements': super app distribution and moats

The key suspense lies in: who controls the user interface for integrated trading/gambling?

A consensus is forming: distribution is king, and the true moat lies in super app-like user relationships.

This drives intensive collaboration: exchanges want retail users (like the collaboration between CME Group and FanDuel/DraftKings), while consumption platforms seek differentiated content (like the collaboration between Robinhood and Kalshi, and DraftKings acquiring a small CFTC exchange).

The model resembles integrated brokerage: stocks, options, crypto, and event contracts are offered side by side, allowing users to remain on the platform.

Prediction markets are exceptionally sensitive to liquidity and trust: thin markets can fail quickly, while depth compounds. Platforms with existing users, low customer acquisition costs, ready KYC, and funding channels are inherently superior to independent venues that need to build depth from scratch. Therefore, it resembles options trading rather than social networking: depth and reliability outweigh novelty. This is also why the 'function vs product' battle is increasingly decided by distribution rather than technology.

Robinhood's early success supports this judgment: in 2025, it launched event trading to some active traders, rapidly increasing volume; ARK Invest estimates its recurring revenue reached $300 million by year-end. The moat comparison is clear: independent prediction markets (even with innovation) struggle to compete against existing users. For example, FanDuel has over 12 million users and, by integrating CME event contracts, quickly established liquidity and trust in five states; DraftKings replicated a similar path in 38 states. In contrast, Kalshi and Polymarket spent years building depth from scratch and are now more actively seeking distribution partnerships (Robinhood, Underdog Fantasy, even UFC).

Possible outcomes: a few large aggregation platforms gain network effects and regulatory endorsements; smaller platforms either specialize (e.g., only doing crypto events) or get acquired. Meanwhile, the fusion of fintech and media's super apps is approaching: PayPal and Cash App may in the future parallel prediction markets with payments and stocks; Apple, Amazon, and ESPN have explored sports betting collaborations from 2023 to 2025, potentially evolving into broader event trading. The real 'missing element' may be the moment when tech giants fully embed prediction markets into super apps—integrating news, betting, and investment into a moat that few competitors can match.

Before this, the user lock-in competition among exchanges, bookmakers, and brokers will continue. The key question in 2026 is whether prediction markets will become a function of large financial apps or continue to exist independently. Early evidence points towards integration.

However, regulators may also remain vigilant towards super apps that seamlessly switch between investing and gambling. The ultimate winner will be the platform that can persuade both users and regulators—its moat comes not only from technology and liquidity but also from compliance, trust, and experience.

Opinion Trade (by Opinion Labs): A macro-focused on-chain challenger

Opinion Trade (launched by Opinion Labs) positions itself as a 'macro-first' on-chain prediction trading platform, with its market form resembling a dashboard for interest rates and commodities rather than betting products dominated by entertainment events. The platform launched on BNB Chain on October 24, 2025, and by November 17, 2025, its cumulative nominal transaction volume had exceeded $3.1 billion, with an average daily nominal transaction volume of approximately $132.5 million during the early stage. From November 11 to 17, the platform's weekly nominal transaction volume was about $1.5 billion, ranking among the leading prediction market platforms; by November 17, its open contract size reached $60.9 million, still trailing behind Kalshi and Polymarket at that time.

At the infrastructure level, Opinion Labs announced a partnership with Brevis in December 2025, introducing a zero-knowledge proof-based verification mechanism into the settlement process, aiming to reduce the trust gap in market outcome determination. The company also disclosed that it completed a round of $5 million seed financing led by YZi Labs (formerly Binance Labs), with other investors participating, providing not only funding support but also strategically connecting tightly with the BNB ecosystem.

Moreover, platforms implementing clear geographical restrictions on the U.S. and other limited jurisdictions further highlight a core trade-off facing on-chain prediction markets in 2025-2026: how to achieve rapid global liquidity aggregation under regulatory boundary constraints.

Consumer-level prediction markets as the distribution channel for 'ICO 2.0'

Sport.Fun (formerly Football.Fun) provides a concrete case of how consumer-level prediction markets are evolving into a new generation of token distribution infrastructure. This emerging 'ICO 2.0' model is directly embedded into consumer-grade applications that generate real revenue. Sport.Fun launched on Base in August 2025, initially focusing on event trading similar to fantasy soccer, then expanding into NFL-related markets.

By the end of 2025, Sport.Fun revealed that its cumulative trading volume had exceeded $90 million, with platform revenue surpassing $10 million, indicating that before any public token issuance, the product had validated a clear product-market fit.

The company completed a round of $2 million seed financing, led by 6th Man Ventures, with Zee Prime Capital, Sfermion, and Devmons participating. This investor structure reflects a rising market interest in consumer-facing crypto applications—these projects combine financial jargon with entertaining participation methods, rather than merely betting on underlying infrastructure. More importantly, this funding round came after user engagement and monetization capabilities had been validated, overturning the traditional sequence of 'selling tokens first, then finding users' seen in early ICO cycles.

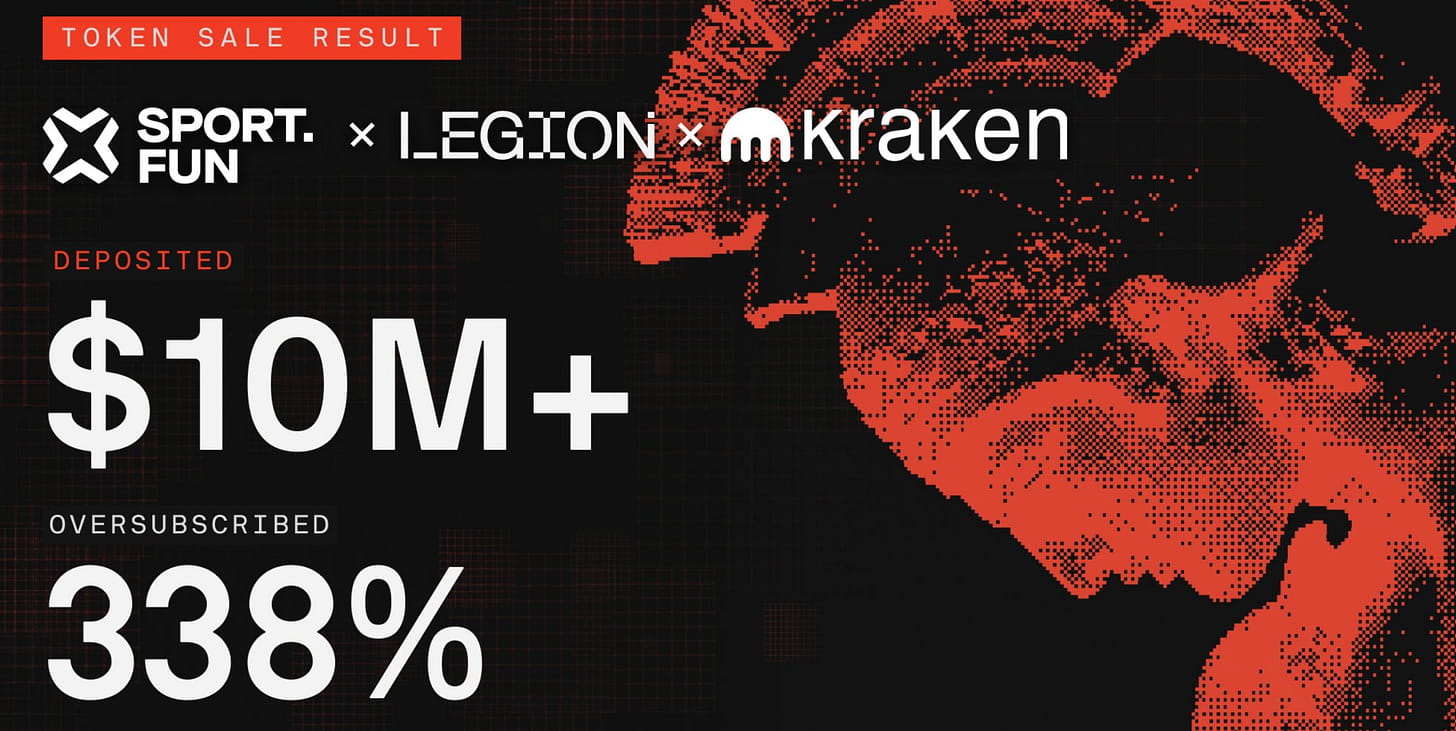

The public token issuance of Sport.Fun further confirms this shift.

$FUN's public offering took place from December 16 to 18, 2025, through the Kraken Launch platform and was completed via a contribution and qualification-driven Legion distribution path. This offering attracted over 4,600 participants, with total subscription amounts exceeding $10 million; the average participation size per wallet was approximately $2,200. Demand exceeded the $3 million soft cap by about 330%. The final fundraising was $4.5 million, with a token price of $0.06, corresponding to a fully diluted valuation (FDV) of $60 million; after exercising the green shoe mechanism to expand, a total of 75 million tokens were sold.

The design of the token economic model aims to strike a balance between liquidity and stability after launch.

According to the plan, 50% of the tokens will be unlocked at the token generation event (TGE) in January 2026, with the remaining portion released linearly over six months. This structure is markedly different from the 'immediate full unlock' commonly seen in early ICO cycles, reflecting lessons learned and corrections from past experiences driven by volatility that ultimately led to price collapses. Functionally, this token issuance feels less like a purely speculative financing and more like a natural extension of the existing consumer market—allowing users who are already actively trading on the platform to 'invest' in the products they are using.

Conclusion

By the end of 2025, prediction markets have transitioned from marginalized experiments to credible, mass-market categories. Growth is driven by mainstream channel distribution, product simplification, and visible user demand. The current core constraint is no longer 'whether to be adopted', but how to design within the regulatory framework: legal qualification, settlement integrity, and cross-jurisdictional compliance determine who can achieve scalability.

The FIFA World Cup should not be simply understood as a growth narrative but rather as a system-level stress test under peak load—a comprehensive examination of liquidity, operational capacity, and regulatory resilience. Those platforms that can pass the test without triggering enforcement risks or suffering reputational harm will define the next phase of industry consolidation; those that fail will accelerate the industry's move towards higher standards, stronger regulation, and fewer but larger winners.

[Original link]