The U.S. Bureau of Economic Analysis (BEA) released its delayed Personal Income and Outlays report on Jan. 22, publishing Personal Consumption Expenditures (PCE) inflation data for both October and November at the same time.

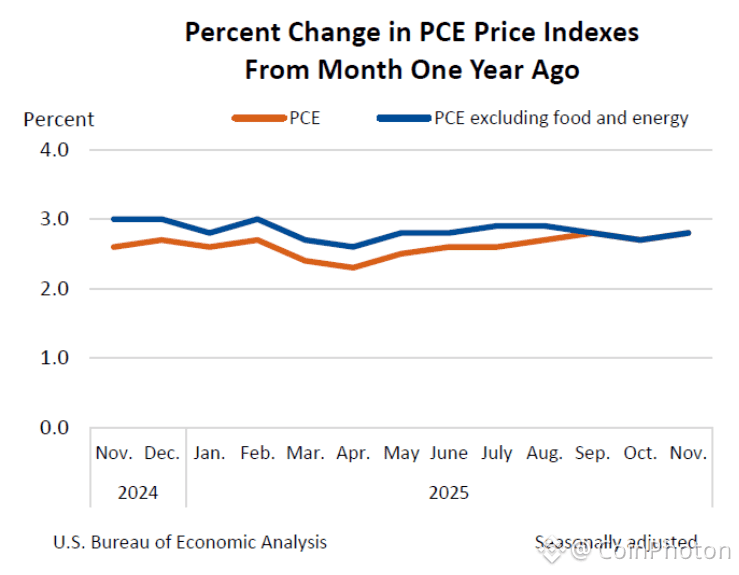

The figures showed headline PCE rising 0.2% month over month in both months. On a year-over-year basis, headline PCE came in at 2.7% in October and 2.8% in November. Core PCE also increased 0.2% month over month in both readings, with annual core inflation likewise at 2.7% and 2.8%, respectively.

Bitcoin’s reaction to the release was notably muted. On Jan. 22, BTC traded in a range of roughly $88,454 to $90,283 and closed near $89,507, up about 0.16% on the day.

That subdued price action is itself the key signal, because this was not a dramatic inflation surprise. The main issue surrounding this report was data quality. The BEA had to publish PCE using “patched” inputs after disruptions affected parts of the data pipeline normally used in its calculations.

In that context, the macro implications for Bitcoin can be broken into three parts: the underlying pace of core inflation, the policy path markets infer from it, and movements in real yields — the channel that most directly transmits macro forces into risk assets.

This PCE release traded as an uncertainty event, not a pure inflation event

PCE is a constructed index built from multiple data sources, with CPI serving as a key input for many categories that rely on detailed price changes. When part of that input stream is missing, the final inflation print becomes more dependent on estimation methods.

This time, the BEA filled gaps using CPI data from surrounding months along with seasonal adjustments to stand in for missing pieces — a process that can smooth away month-specific volatility.

That matters more than it may seem. A 0.2% monthly core reading can mean two different things. In a “clean” month, it is a straightforward measure of that month’s inflation pace. In a “patched” month, it can be a blend of actual price movements and statistical interpolation. The number still carries information, but with less certainty about what truly changed within that month.

A simple way to interpret the Jan. 22 core print is to focus on the level and persistence of inflation. Core PCE near 2.8% year over year keeps inflation above the Federal Reserve’s 2% target, and a 0.2% monthly pace — if sustained — tends to keep the annual rate sticky. That is enough to constrain expectations for aggressive rate cuts, even in the absence of an upside shock.

The next step is how markets translate that inflation baseline into a policy path.

The Fed does not react to a single report in isolation, but markets constantly update probabilities. With this release, the key question was whether traders would treat the data as strong enough to delay easing, or uncertain enough to wait for a cleaner read before placing large policy bets. A patched report often pushes markets toward the latter, because conviction is harder to justify.

Bitcoin typically reacts less to the inflation figure itself than to what happens in rates markets around it.

Real yields are a clean shorthand for the opportunity cost of holding a non-yielding asset like BTC, and they also reflect broader liquidity conditions. When real yields rise, the hurdle rate for Bitcoin increases and financial conditions tighten. When real yields fall, that hurdle declines and conditions ease.

That is why the best way to treat a messy PCE release is as a context setter, then follow the rate market’s verdict.

A steady 0.2% monthly pace with core inflation near 2.8% is not a green light for rapid easing, but it also does not force an immediate repricing if traders doubt the precision of the data. In that environment, Bitcoin often ends up trading the follow-through in rates rather than the inflation headline itself.

The final piece of the framework is what happens next. When a report is patched, the next clean release tends to carry extra weight because it can confirm or contradict the smoothed path. If the next clean month comes in hotter, earlier calm may look like an artifact of estimation methods. If it comes in similar, the patched data becomes easier to accept as a reasonable stand-in.

Bitcoin’s lack of reaction this week fits that setup. There was no clean shock to digest — just an update that mattered, but came with enough caveats to limit short-term conviction.

GDP was background noise unless it moved yields

The same day also brought an updated estimate of Q3 2025 GDP, revised slightly higher to 4.4% annualized from 4.3%. For Bitcoin, growth data typically matters only if it moves the bond market.

GDP influences markets through two often-conflicting channels. Stronger growth can keep the Fed cautious and real yields elevated — usually a marginal headwind for BTC. At the same time, stronger growth can support risk appetite and earnings expectations across markets, which can benefit speculative assets. Which force dominates depends on what happens to yields, not the GDP headline alone.

In this case, the revision was small and backward-looking, making it a weak standalone input for Bitcoin. The main takeaway is that a solid growth backdrop gives the Fed room to be patient if inflation does not fall convincingly toward target. A patched core PCE reading near 2.8% year over year, paired with strong prior growth, supports a baseline of patience rather than urgency.

That baseline helps explain why BTC can trade flat even when inflation data initially looks benign. If the macro mix is strong growth plus sticky core inflation, it becomes harder to price in aggressive rate cuts. That tends to keep real yields from falling quickly — and that lever often matters more for Bitcoin than the growth print itself.

The practical macro read for the week is therefore compact. GDP adds context, but it is not the driver. The driver is how the inflation story feeds into yields. If yields drift higher because growth optimism lifts term premia or because inflation uncertainty keeps policy expectations firm, BTC can feel heavy even without a scary headline.

If yields drift lower because markets gain confidence that inflation is cooling, BTC can hold up and build support even while the inflation narrative remains messy.

This week’s PCE release offered a useful reminder of how Bitcoin trades macro. The most important aspect was not a tenth of a percentage point in the PCE table, but the reliability of the data behind it and the rate-market reaction that followed.

The BEA published two months of PCE at once using patched inputs, reducing confidence in month-specific precision even if the overall direction still carries information. Bitcoin reflected that uncertainty with a tight trading range and a small day-over-day gain.

The next clean inflation report will matter more than usual, as it can confirm whether the patched months accurately captured the underlying trend. Until then, the clearest macro signal for Bitcoin sits in the rates market rather than in any single line of the Jan. 22 data release.