Hey everyone, and welcome to the Weekly Market Roundup

Bitcoin entered the week under heavy pressure, with price action reflecting a market caught between macro uncertainty and structural support. After opening near $91,000 on January 20, BTC was repeatedly rejected at key resistance levels and sold off sharply, falling below $89,000 and briefly touching $86,000 as institutional outflows accelerated. Currently it’s trading in $87,500-$88,000 range. The drawdown, roughly 9% peak to trough, coincided with $1.22 billion in ETF redemptions between January 20–22, underscoring the sensitivity of price to liquidity and positioning rather than spot-led demand. While Bitcoin managed to recover modestly into the $89,500–90,000 range by week’s end, the broader setup remains fragile, with macro risks, policy uncertainty, and tightening financial conditions continuing to dominate near-term price behavior.

In this issue, I’ll break down what actually drove the movement, how macro catalysts are compressing into a high-impact window, what on-chain flows are revealing about holder behaviour, and where structural momentum may emerge next.

Let’s get into it.

1. Weekly Crypto Headlines at a Glance

Chainlink has launched 24/5 U.S. Equities Data Streams, giving decentralized finance ( DeFi) protocols continuous access to institutional-grade stock and exchange-traded fund (ETF) data

More than half of the top US banks have either started offering or announced plans to offer Bitcoin-related services such as trading or custody

Japan set to approve first crypto ETFs by 2028

Web3 Security leader Certik prepares IPO after Binance Investment

2. Macro Backdrop

1. A Weak Dollar Without Broad Risk Rotation

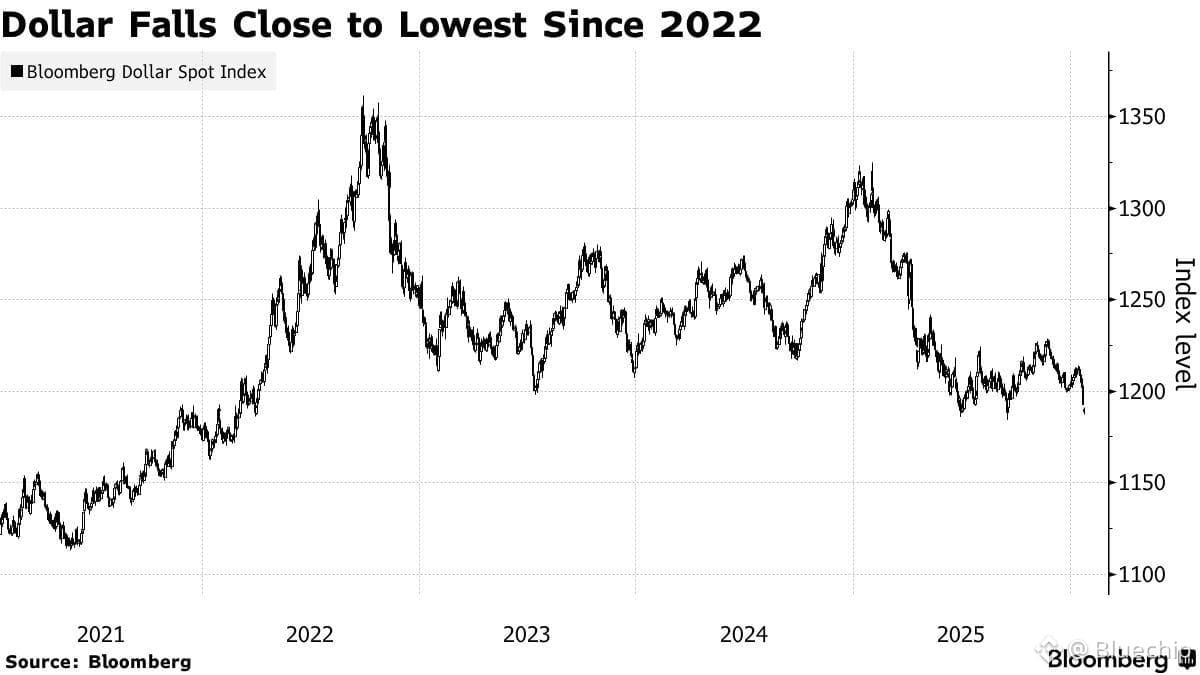

The U.S. dollar has weakened sharply, with the DXY falling to 97.2, its lowest level since 2022. This move reflects a growing loss of confidence in U.S. policy consistency, driven by erratic tariff threats around Greenland followed by abrupt reversals, alongside rising speculation of coordinated currency intervention between the U.S. and Japan after the New York Fed checked USD/JPY levels with dealers.

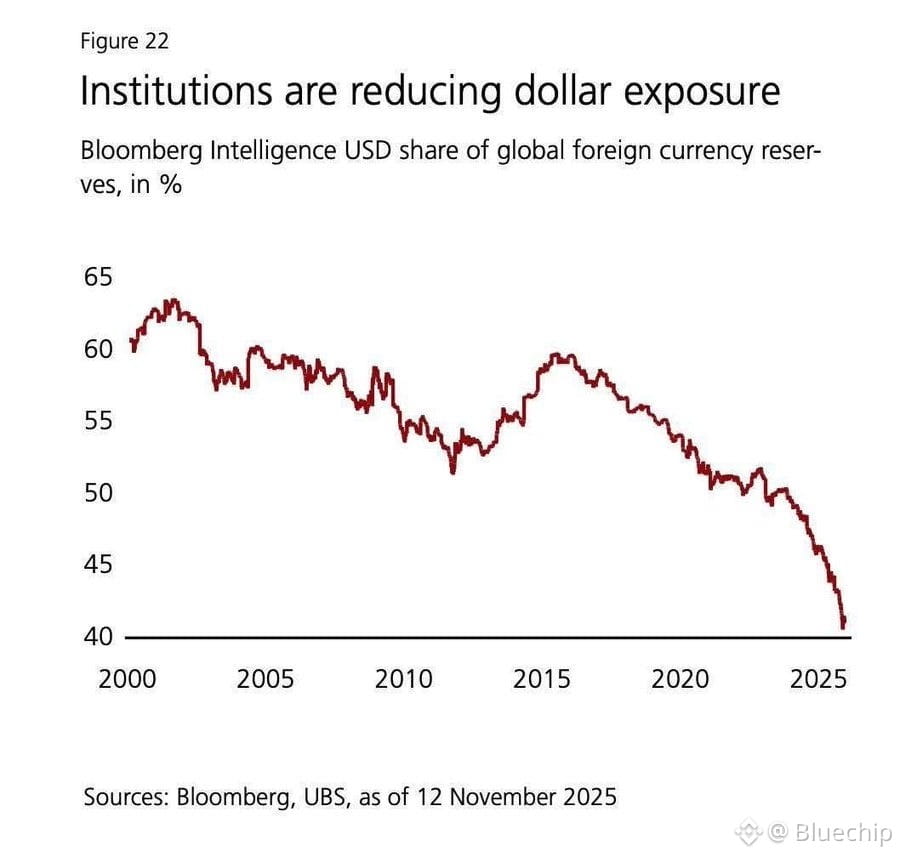

The US dollar’s share of global foreign exchange reserves has fallen to around 40%. Major institutions and central banks are gradually reducing their exposure to the dollar, diversifying reserves into other currencies and assets.

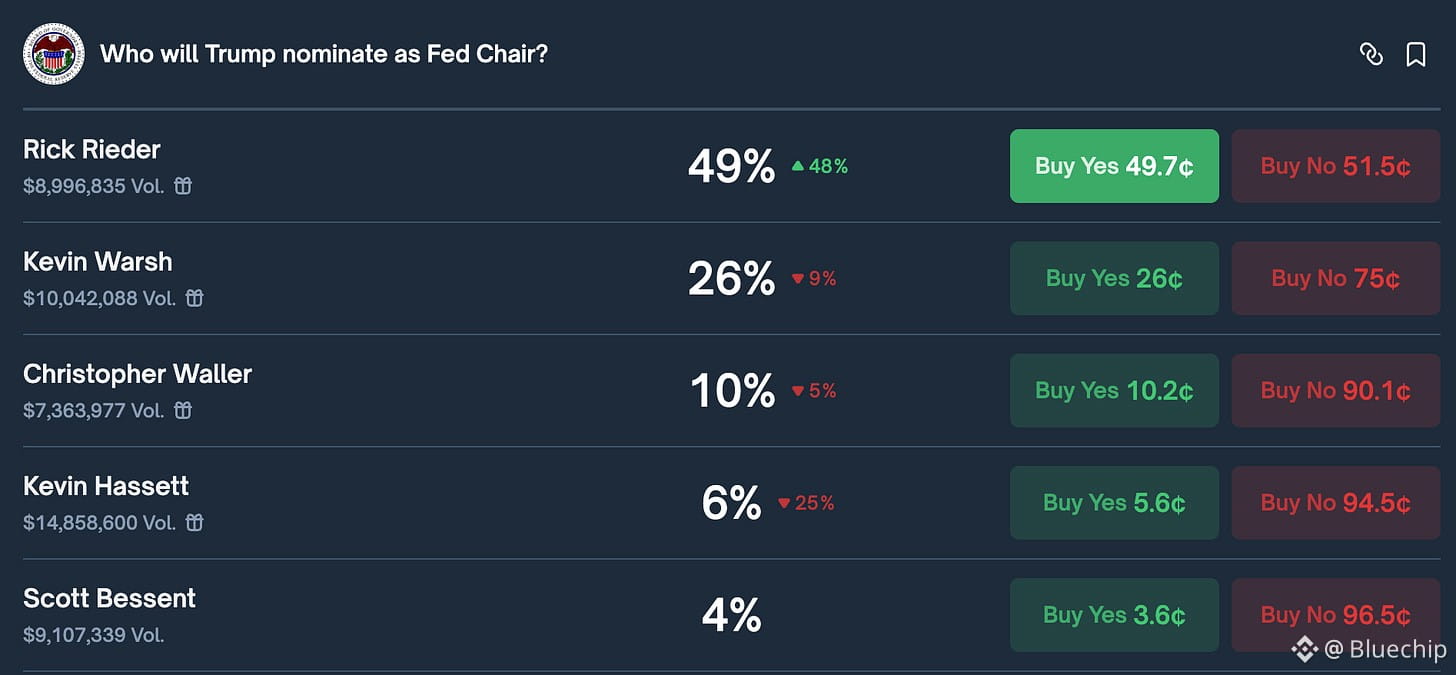

At the same time, markets are now pricing more aggressive U.S. rate cuts relative to other major central banks, and expectations are building that Trump may nominate a dovish Fed Chair as early as May. Together, these factors point to a structurally weaker dollar, which historically provides a supportive backdrop for risk assets and crypto.

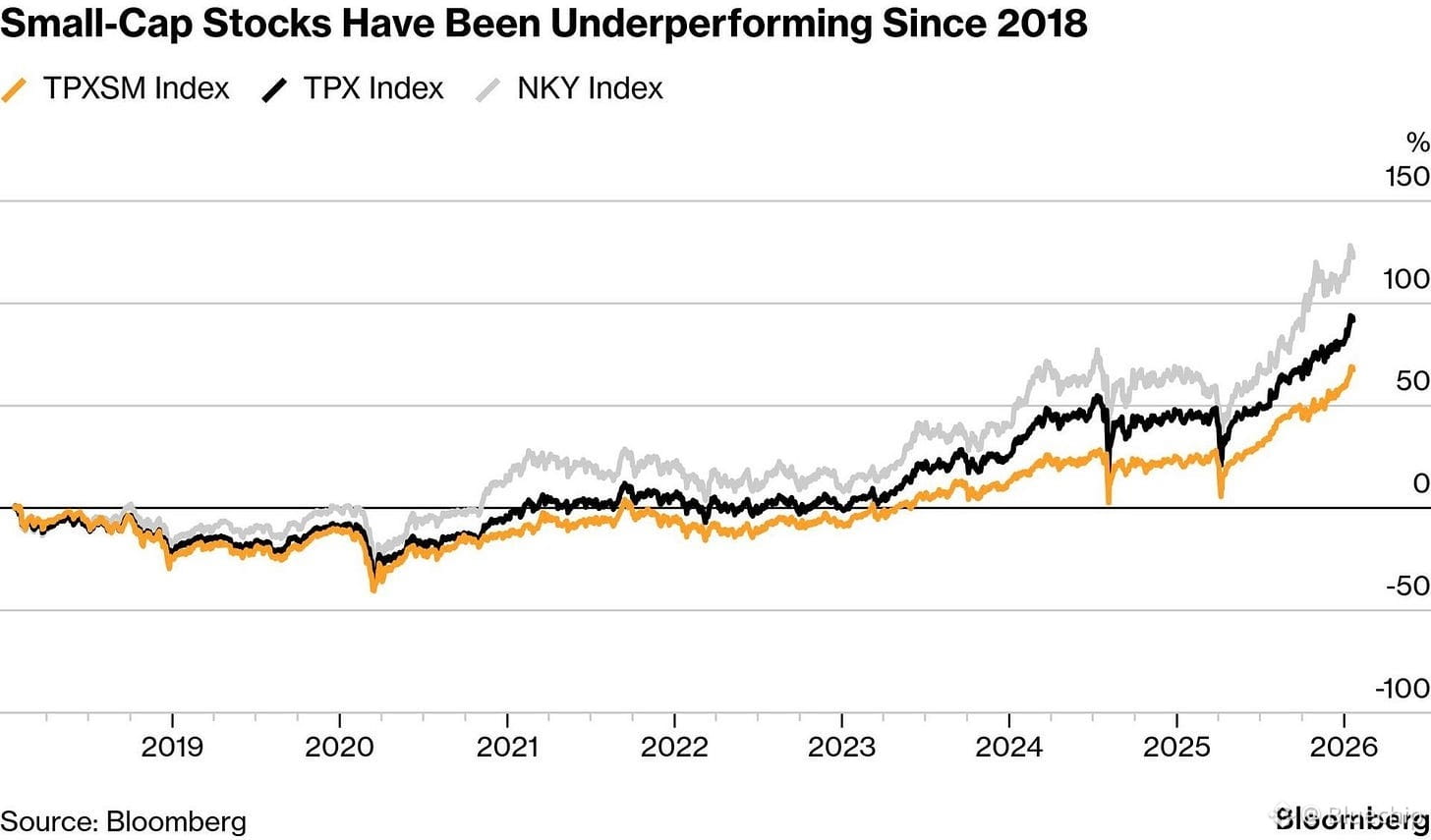

Despite this seemingly constructive macro environment, capital allocation remains highly selective. Small-cap equities continue to underperform meaningfully, a dynamic that closely mirrors crypto markets today. Bitcoin dominance is hovering near 59%, while the CMC Altcoin Season Index sits at 17, indicating that roughly 83% of altcoins have underperformed Bitcoin. Even large, high-conviction tokens have struggled, with Solana down ~35% through year-end 2025. Much like small-cap stocks that trade at deeply discounted valuations but fail to attract inflows, altcoins remain stuck in a liquidity desert, where capital refuses to rotate broadly and instead chases isolated, narrative-driven moves.

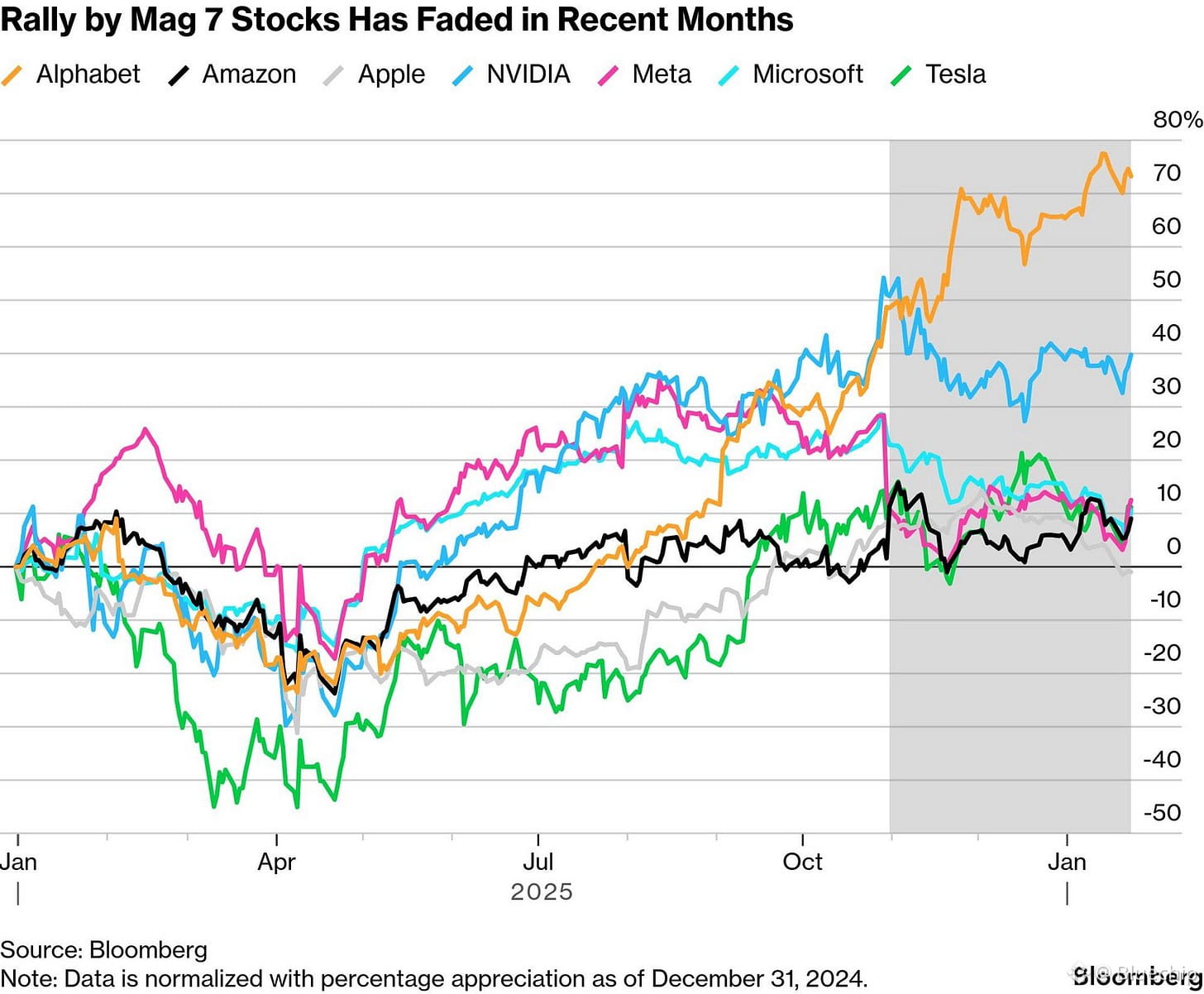

This concentration dynamic is not limited to crypto. In equities, the long-standing dominance of mega-cap technology is beginning to crack. The so-called Magnificent 7 are up just 0.5% year-to-date, materially lagging the broader S&P 500’s 1.8% gain, marking the first period since 2022 where most of the group has underperformed the index. Investors are increasingly questioning stretched valuations, particularly as former leaders such as Meta and Apple have slipped into negative territory for the year, signaling fatigue in what has been the market’s most crowded trade.

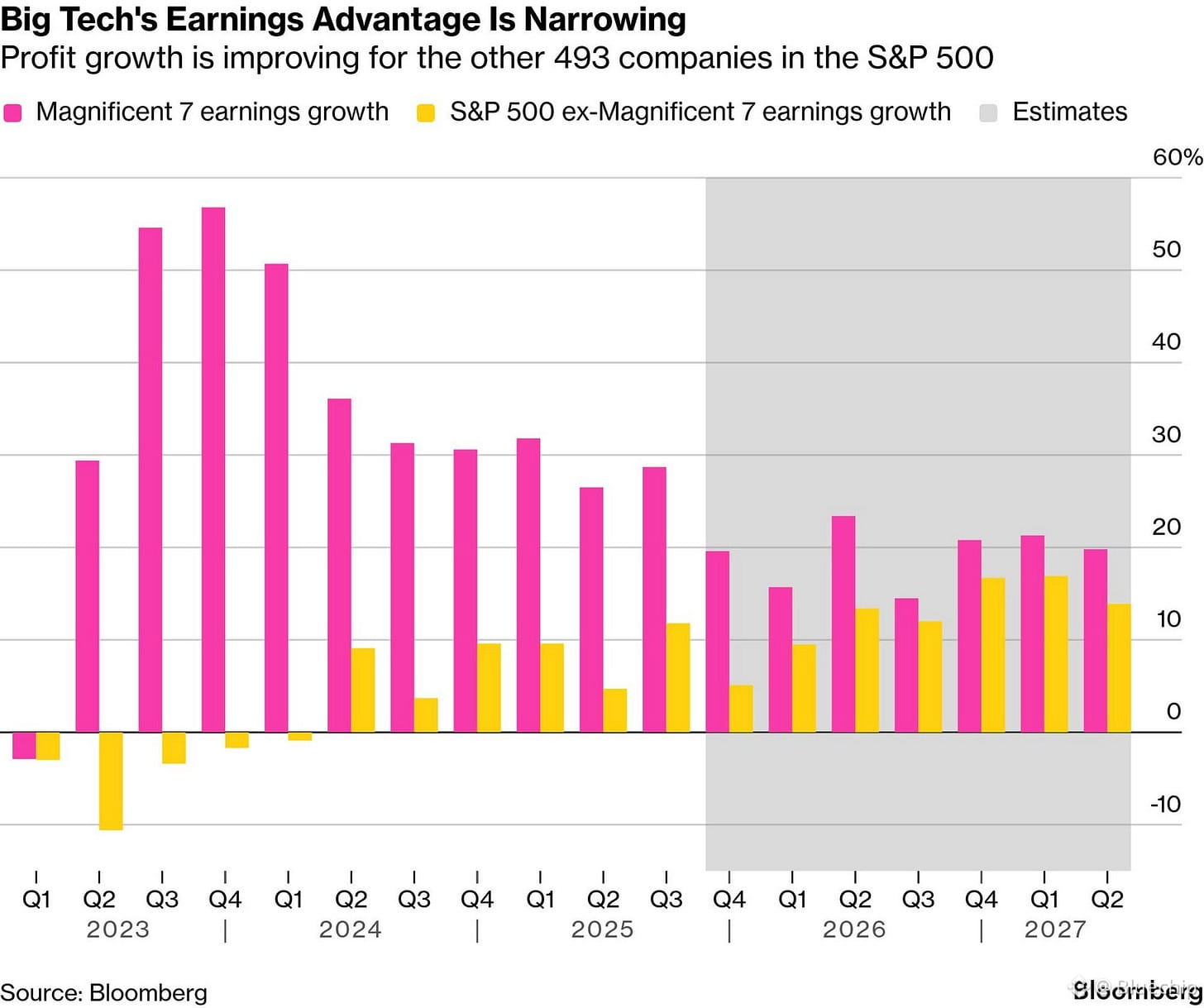

The underlying reason for this shift is a rapid compression in earnings leadership. Consensus expectations now point to Magnificent 7 earnings growth of around 18% in 2026, only modestly above the 13% projected for the rest of the S&P 500. When Big Tech was growing at multiples of the broader market, premium valuations and extreme concentration were justified. With that growth advantage now narrowed to a low single-digit spread, the economic case for capital crowding into a handful of winners has weakened significantly, echoing similar dynamics playing out between Bitcoin and the broader altcoin market.

The macro setup, therefore, is increasingly clear but unresolved. Dollar weakness should, in theory, support risk assets, earnings growth is normalizing across markets, and concentrated leadership in both equities and crypto is showing early signs of strain. Yet liquidity has not rotated in a meaningful way, leaving small caps and altcoins sidelined despite improving conditions. The key question heading into 2026 is whether sustained dollar weakness finally breaks the concentration trade and unlocks a broader risk rally, or whether capital continues to hide in proven winners while the rest of the market remains starved of inflows.

2. JGB Market Sell-Off and Global Risk Repricing

A sharp sell-off in Japan’s government bond market has triggered a broader repricing of global risk. Long-duration JGBs have led the move, with yields rising rapidly amid shifting inflation expectations and persistent fiscal concerns. With government debt exceeding 250% of GDP, Japan remains highly sensitive to any perception of policy expansion. This week, the JP10Y moved sharply higher, while the JP30Y recorded one of its largest daily increases since 2003, pushing yields to new highs near 3.9%.

Rising Japanese yields threaten to unwind the JGB-funded carry trade that has long acted as a global liquidity anchor. Japan’s ultra-low rates historically compressed global funding costs and enabled leverage into higher-beta assets, including crypto. While the Bank of Japan has so far tolerated higher yields, its approach has shifted toward managing liquidity and market functioning rather than suppressing yields outright. If bond-market stress persists, this implies less global liquidity support and greater sensitivity across risk assets.

For crypto, this matters because Bitcoin’s correlation with global liquidity tightened meaningfully through 2025. In this episode, the transmission has been most visible through institutional positioning, particularly via ETFs. During periods of macro stress, ETF flows tend to reflect de-risking early, and this week marked the largest daily outflow of the year, leaving crypto vulnerable in risk-off environments as tighter funding conditions feed directly into positioning.

Cross-asset behavior highlights the current regime. Gold has absorbed the stress signal from rising Japanese yields, consistent with defensive demand, while Bitcoin has remained inversely sensitive to moves in JP10Y yields. This suggests BTC is currently trading as a liquidity-sensitive risk asset rather than benefiting from its longer-term hedge narrative.

Looking ahead, Bitcoin has historically stabilized once initial macro shocks are absorbed. If higher yields begin to undermine confidence in sovereign debt sustainability, BTC’s hedge narrative could regain relevance. Alternatively, any credible policy signal that eases stress in the JGB market could improve global liquidity conditions and provide room for crypto to recover.

Recent policy signals offered limited near-term relief. Japan CPI and the Bank of Japan’s January 23 decision left rates unchanged around 0.75%, with guidance emphasizing vigilance around bond-market volatility and financial stability, particularly at the super-long end of the curve. If volatility persists, policy action is more likely to focus on smoothing market functioning through targeted bond purchases, adjustments to issuance, or curve-specific measures rather than a return to yield caps.

3. U.S. Consumer Sentiment and the Growth Disconnect

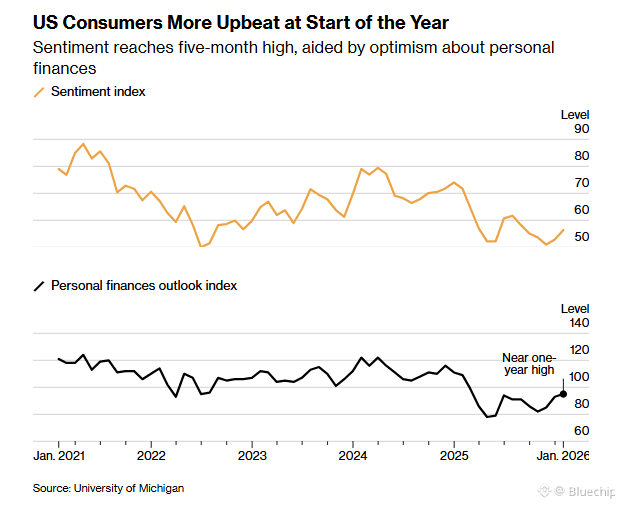

U.S. consumer sentiment continued to improve in January, with the final University of Michigan survey showing a meaningful upside revision. The headline sentiment index was raised to 56.4 from an initial 54.0, up from 52.9 in December, marking the second consecutive monthly increase and the largest jump since June. The improvement suggests households are gradually regaining confidence despite elevated rates and lingering inflation concerns.

Inflation expectations also eased modestly, reinforcing the improving sentiment backdrop. One-year inflation expectations fell from 4.2% to 4.0%, the lowest level since January last year, while five-year expectations edged down from 3.4% to 3.3%, remaining only slightly above December’s 3.2%. While still elevated relative to pre-pandemic norms, the direction of travel suggests reduced near-term inflation anxiety among consumers.

Forward-looking indicators were similarly constructive. The expectations index reached a six-month high, and expectations around personal finances climbed to their highest level in a year, pointing to improving household balance-sheet confidence. Early January activity data from S&P Global also indicated a modest uptick in momentum, reinforcing the view that economic activity remains resilient.

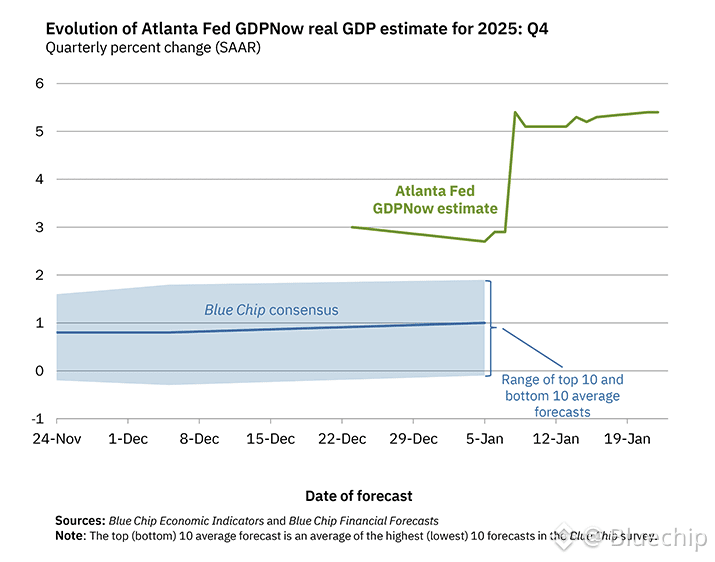

Growth data continues to surprise to the upside. Q3 GDP was revised higher to a robust 4.4%, while the Atlanta Fed’s GDPNow model is currently tracking Q4 growth near 5.4%, underscoring strong underlying demand and momentum heading into year-end.

The tension lies in how markets are interpreting this strength. Despite resilient growth and improving sentiment, the DXY continues to weaken, Treasury yields remain elevated, and gold prices are flashing a clear safe-haven signal. This divergence suggests markets are less focused on near-term growth and more concerned about policy credibility, fiscal dynamics, and the sustainability of current conditions, setting up a macro environment where headline economic strength coexists with defensive positioning.

4. Trade Shock and Fiscal Risk Re-Emerge

Trump escalated trade rhetoric against Canada, threatening 100% tariffs on Canadian imports if Canada proceeds with limited trade arrangements with China. The stated concern is preventing Canada from acting as a conduit for Chinese goods into the U.S., reintroducing trade policy uncertainty despite deep U.S.–Canada economic integration.

Canada pushed back, with PM Mark Carney dismissing the threat as bluster and clarifying that recent engagement with China is narrow and not a comprehensive trade agreement. Despite this, the rhetoric raises risks for supply chains tied to energy, metals, and agriculture.

U.S. government shutdown risk has surged, with prediction markets now pricing roughly 80% odds of a shutdown by January 31. The spike reflects deepening political fractures around a $1.2tn funding package, DHS appropriations, and immigration-related disputes.

Market implication: renewed trade threats and elevated shutdown risk reinforce policy uncertainty, weaken confidence in forward guidance, and add to the growing disconnect between strong economic data and defensive asset positioning.

3. ETF / ETP Flow Insights

Crypto ETFs went through one of their toughest weeks of 2026, with selling pressure building steadily after the U.S. market holiday on January 19 and continuing through January 23. Risk appetite weakened across the board, leading to large and persistent outflows from the biggest and most liquid ETF products, pointing to clear institutional de-risking rather than short-term rotation.

Bitcoin spot ETFs saw $1.33 billion in net outflows for the week, the second-largest weekly exit on record. Selling was concentrated in core institutional vehicles. BlackRock’s IBIT led the outflows with $537.49 million redeemed, followed by Fidelity’s FBTC at $451.50 million. Grayscale’s GBTC continued its ongoing bleed, losing around $172 million. Other Bitcoin ETFs also saw steady exits, including ARK & 21Shares’ ARKB (~$76 million), Bitwise’s BITB (~$66 million), Franklin’s EZBC ($10.36 million), Valkyrie’s BRRR ($7.59 million), and VanEck’s HODL ($6.3 million), showing that selling pressure was widespread.

Ether spot ETFs also faced heavy redemptions, with $611.17 million in net outflows during the week. BlackRock’s ETHA accounted for most of the selling, with about $431.50 million leaving the fund. Fidelity’s FETH lost roughly $78 million, while Bitwise’s ETHW saw outflows of about $46 million. Grayscale’s ETHE recorded around $52 million in redemptions, partly offset by $17.82 million in inflows into its Ether Mini Trust. VanEck’s ETHV finished the week down nearly $10 million.

XRP ETFs recorded their first weekly net outflow since launch, with total redemptions of $40.64 million. Grayscale’s GXRP drove the move, losing more than $55 million, which outweighed combined inflows of just over $15 millioninto Franklin’s XRPZ, Bitwise’s XRP, and Canary’s XRPC. This marked the first real test of sustained institutional demand for XRP exposure.

Solana ETFs were the clear outlier, ending the week with $9.57 million in net inflows despite the broader risk-off environment. Fidelity’s FSOL led demand with $5.28 million, while Bitwise’s BSOL, VanEck’s VSOL, and Grayscale’s GSOL also saw steady inflows, more than offsetting a small pullback from 21Shares’ TSOL.

Overall, the week highlights a sharp shift in institutional positioning. Bitcoin and Ether absorbed the bulk of selling, reinforcing their role as the main outlets for risk reduction during periods of macro uncertainty. Solana’s relative strength points to selective confidence rather than broad risk-taking, while XRP’s first outflow suggests that appetite outside the largest assets may be starting to soften.

4. Options & Derivatives

January 23 expiry passed with elevated positioning, involving ~$2.1–2.3B notional across BTC and ETH, but failed to provide upside follow-through. Markets remained rangebound, suggesting options were largely used for hedging and short-term positioning, not directional conviction.

Attention now shifts to the January 30 expiry (~$8.5B notional), which carries greater risk for volatility.

Bitcoin options show mixed but fragile positioning. Total BTC options open interest remains high at ~$36–58B, with calls making up ~57–62% of OI, signaling selective upside interest rather than broad bullishness.

The Jan 23 expiry saw ~$1.8–1.94B notional roll off with a put/call ratio of 0.74–0.81, leaning bullish, but max pain at $92k sat above spot (~$89–90k), limiting upside and keeping price action unstable.

Post-expiry BTC positioning is defensive. Near-term max pain has shifted lower to ~$90k, while puts are increasingly clustered between $85k–88k (~$1.1B OI) and $75k–85k, where downside hedging dominates.

ETH options reflect clearer bearish pressure. Total ETH options OI sits near $8B, but positioning is more defensive than BTC. The Jan 23 expiry (~$337–347M notional) showed put/call ratios ranging from 0.86 to 1.65, with max pain at $3,200–3,250, well above spot (~$2,900–2,950). This gap suggests continued downside sensitivity rather than mean reversion.

ETH strike concentration reinforces downside bias. Elevated put interest sits around $2,900–2,950, while the $3,200 zone remains the dominant max pain cluster, acting as resistance. Net futures flows remain weak (~-$538M in 24h), spot demand is muted, and ETH continues to consolidate after a sharp drop from 2025 highs.

Overall takeaway: options positioning confirms a risk-off regime with rising leverage but limited directional confidence. BTC remains vulnerable to downside liquidity grabs as OI rebuilds below max pain, while ETH positioning is more outright defensive. The Jan 30 expiry is likely to act as the next volatility trigger, with focus on $100k BTC calls and whether ETH can hold the $2,900 zone under continued macro pressure.

5. On-Chain Forensics

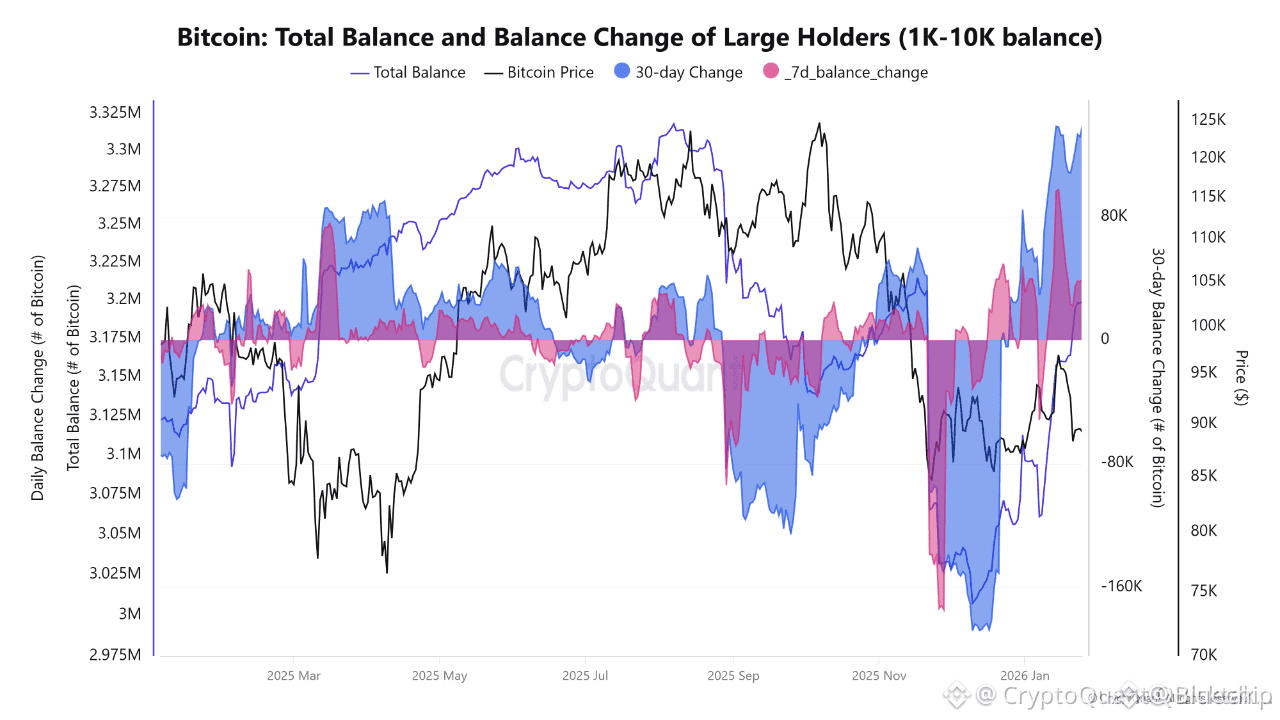

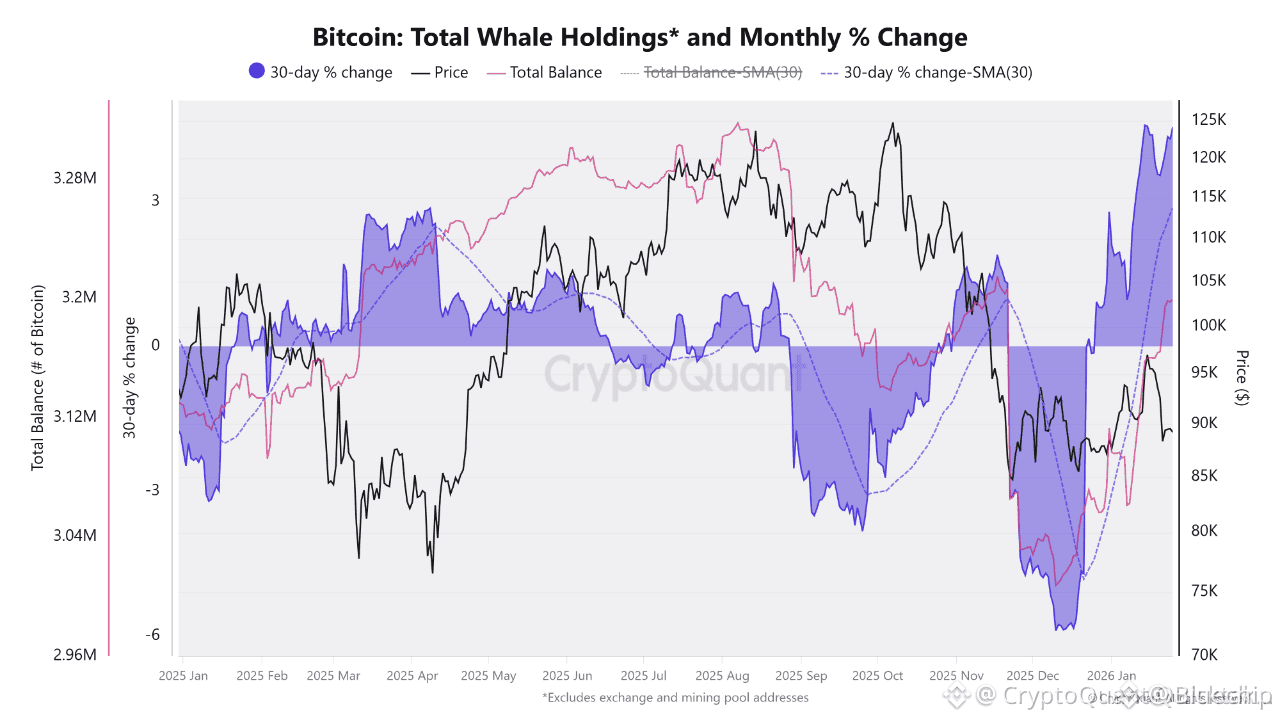

On-chain tracking of large Bitcoin holders (1K–10K BTC, excluding exchanges and miners) indicates a shift in behavior after a prolonged distribution phase through late 2025. Whale balances peaked around mid-2025 and then declined steadily while prices stayed elevated, pointing to intentional selling into strength rather than stress-driven exits.

The distribution trend was clearly visible in the 30-day balance change data. Throughout Q3 and early Q4, whale balances consistently registered negative monthly changes, occurring alongside rising volatility and weakening price momentum. This divergence suggested that upside moves were increasingly supported by short-term or marginal buyers rather than fresh accumulation from large holders.

Recent data marks a clear change in direction. Both 7-day and 30-day balance changes have flipped positive, and total whale holdings have begun to stabilize after hitting local lows. Historically, this type of transition from net selling to early accumulation tends to appear during consolidation phases or after corrections, rather than near cycle peaks.

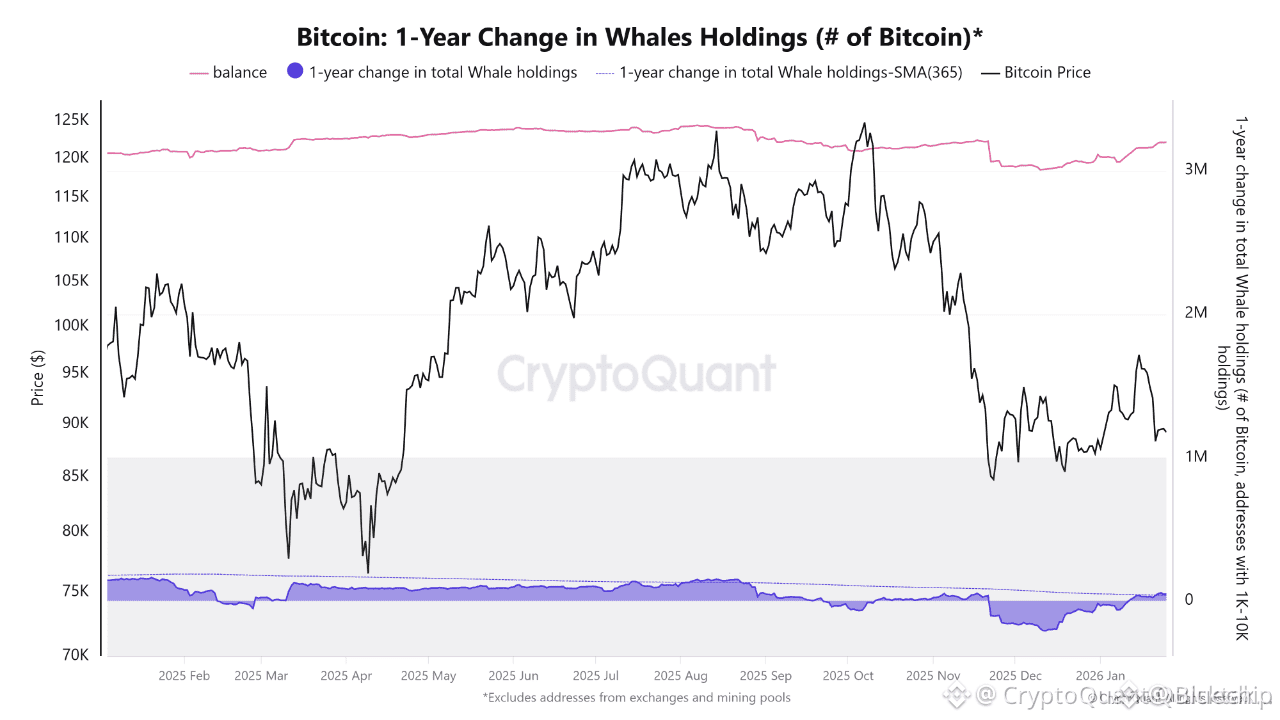

On a longer time frame, the 1-year change in whale balances remains broadly flat, signaling that the market has not yet entered a sustained accumulation phase. This points to tactical re-positioning by large holders rather than high-conviction, long-term buying.

Overall, whale behavior is no longer adding persistent sell pressure to Bitcoin’s circulating supply. While this shift alone does not imply an immediate upside breakout, it meaningfully lowers near-term downside risk and supports the view that the market is entering a stabilization phase, with future direction dependent on whether accumulation meaningfully builds from current levels.

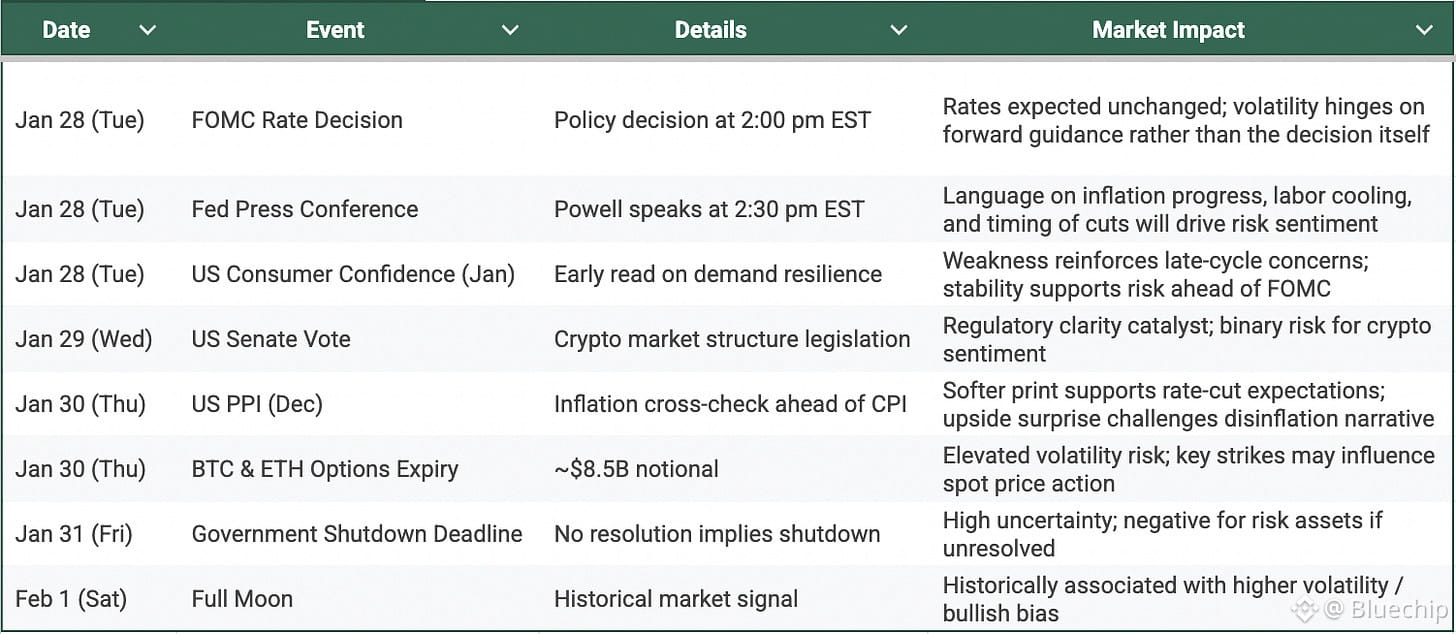

6. The Week Ahead

Investor Takeaway

This is a policy-driven volatility week, not a data-driven one.

Powell’s tone matters more than the rate decision itself.

A dovish read-through supports risk and crypto beta; a firm stance risks position unwinds.

Expect sharp intraday moves, especially around the FOMC press conference and options expiry.

Bias toward reaction over anticipation, with disciplined positioning given overlapping macro and crypto catalysts.

7. Conclusion

Macro conditions are improving on the surface, but capital remains defensive and concentrated, with liquidity tightening rather than rotating. Until policy clarity improves and flows stabilize, markets remain vulnerable to volatility-driven moves rather than broad, durable risk-on trends. This is evident from Fear & Greed Index as well which is currently at 29-Fear territory.

In a market driven by liquidity swings and institutional flow, our Crush Circle platform by CryptoCrush gives investors direct access to expert research, real-time guidance, and the frameworks needed to stay ahead of the next big move